The management of hidden costs in organizations requires compliance with the precepts of socio-economic theory, which imply reaching the four stages of investigation: situational diagnosis, strategic worksheet, prescription and predictive test. To this end, a proposal for a solution is conceived that suggests knowing its effectiveness through a test through reobservation of the motivations achieved among workers after implementing some measures contained in the presented solution. It is in this event that the investigation was developed, with the application of interventionist research, the frequency of malfunctions that cause hidden costs evaluated at 8,392, 259.29 Kz in the investigation carried out in December 2022 was observed and applied through the Plan of Priority Activities (PAP) tool, a short-term tool with seventy-two (72) proposed activities, however, it was tested with the frequency´s subsequent reobservation of the same dysfunctions. Forty-seven (47) took the name of strategic activity, those activities with a value that appeared in the range of 1.5 to 2 according to the results of the spss software, that can mitigate the frequency of dysfunctions and associated hidden costs.

## I. INTRODUCTION

The production of accounting information linked to the costs that companies assume during operation is, therefore, fundamental when it comes to the concept of survival, continuity of the company, economic-financial and social satisfaction of shareholders and workers. This requirement is supported on the one hand by cost and management accounting through the recording of internal accounting economic facts, i.e. costs of a visible nature and on the other hand by socio-economic theory through the accounting recording of internal economic facts but, hidden nature that give rise to hidden costs, since external accounting economic facts are the responsibility of financial accounting to register them.

Costs of a visible nature are known to be easy to account for because they are, in principle, identifiable in the company's financial statements and in the different reports whenever a certain expense is assumed internally.

This reality is not analogous when it comes to accounting for hidden costs, because these costs are not, in principle, documented in the statements or even cost information reports, these are only subject to measurement through the use of socio-economic methodology. Therefore, this fact is achieved with the diagnosis of dysfunctional "pathologies" that prevent the normal company'sfunctioning.

Once known, they deserve an interpretation and, therefore, a prescription or even adoption of a conduct to be followed for their control, mitigation and termination, at least in the short term, since, in the medium and long term, they would happen again if they are not accompanied by judging from the permanence of interaction between the company's structures and the behavior of workers in the informal environment.

According to socio-economic theory, the identified malfunctions and the accounting of the hidden costs resulting from these malfunctions deserve treatment through the presentation of factual solutions taking into account the peculiar reality of each company. However, it obliges the conception of a solution to the identified dysfunctions in order to minimize them or even put an end to them in the short term, in the medium and long term to proceed with measures to monitor the company's operation.

Thought already approached by Savall & Zardet (1987), when referring that, the socio-economic theory methodologically possesses theoretical and practical conditions to solve the dysfunctions that result in hidden costs during the functioning of the organizations, in that it presents the tools to choose given the reality of each company and, therefore, the explanatory variables of the solution domain. That is, did you diagnose a malfunction or pathology during the operation of the company? It interprets it and then solves the referred dysfunction for the ortho functioning of the company.

This condition takes us back to the algorithm followed by a doctor when dealing with a patient in the hospital. The patient is diagnosed by exposing him to the symptoms, the doctor questions and, in order to confirm or refute the diagnosis, resorts to interpretation through the results of the analyzes recommended by him. These results for the doctor serve as a barometer for the conclusions of the types of drugs to prescribe or even advise a conduct to be followed by the patient. This cycle does not stop there, if not, the doctor monitors the patient's evolution taking into account the given prescription or the recommended conduct. If it does not have substantiated positive effects in improving the patient's health, the doctor will certainly evolve to another prescription according to the degree of the drugs.

In the investigation of Deco, Napoleão, Tamo, & Simbo (2023), malfunctions were diagnosed that caused hidden costs linked to the absenteeism indicator and, therefore, in this article, the results of all the indicators studied were presented, and then the proposed solution was presented. Those dysfunctions that, with the measurement of its effectiveness by means of a predictive test, weconcluded that the proposed solution is a solution to be able to reduce the dysfunctions that caused the hidden costs accounted for, naturally in a later period with reference to the same variables.

### a) Problematic Context

The need to see organizations as living beings, as Tamo (2014) refers, is imperative, as it provides positive indicators to approach the best management practices of organizations. This is a thought materialized in the socio-economic theory Savall & Zardet (1975), regardless of the fact that they did not equate organizations with human beings.

In this investigation, therefore, it was possible to sustain this thought, that of adopting the patient management model by the doctor, making the methodology richer and more proactive in favor of the survival and continuity of organizations, substantiated in the presentation of a proposal for solutions to malfunctions found and that cause hidden costs and that deserved a predictive test for its validation.

Allied to this, the concept of follow-up is also adopted, which derives from the idea of solutions to be proposed to safeguard a positive position that prevents the return of those dysfunctions that caused the aforementioned hidden costs.

At first, the object studied was unaware of the existence of dysfunctions of an occult nature, unaware of the theory that studies dysfunctions and, therefore, the possibility of existing in the investigative scope a feasible solution to the dysfunctions diagnosed to the specific reality of the company, constituting facts that animated the investigation and which resulted in the results presented below.

To this end, the solution conceived in the light of the company's reality was tested by developing a new investigation, in a period different from that of the first investigation, taking into account the same hidden cost indicators studied, the same diagnosed malfunctions that caused the hidden costs in view of the activities regarded as strategic because they are capable of addressing the malfunctions found or at least reducing their frequency.

With these questions verified by the studied object, he suggested proposing the following scientific question: how can a proposal for a solution to the diagnosed malfunctions be conceived to contribute to the mitigation of the hidden costs levels accounted for in the organizations regular functioning?

For this purpose, the general objective consisted of designing a proposed solution to the malfunctions found and which caused the hidden costs accounted for during the first investigation.

In order to achieve this objective, specific objectives were achieved by carrying out the following activities in the research space: to substantiate the theoretical basis that sustains the socio-economic theory; present the results of the first investigation object of a proposed solution; identify the explanatory and solution domain variables adaptable to the reality of the studied object; propose activities in each variable; verify the reliability and adjustment to normality of the new data structure; carry out a descriptive analysis to identify strategic activities; perform predictive testing of strategic activities; count the paid time (hours) without any counter-work taking into account the related indicator; accounting for hidden costs according to the time of each indicator; ensure the qualimetric approach for accounting for all costs incurred during operation from: determination of the production cost and cost price with and without hidden costs, determination of the analytical result without and with hidden costs and measuring the hidden costs weight resulting from predictive testing in the company's visible cost structure; reveal the visible and unknown economic performance provided by the predictive test.

## II. MATERIALS AND METHODS

### a) Theoretical Framework

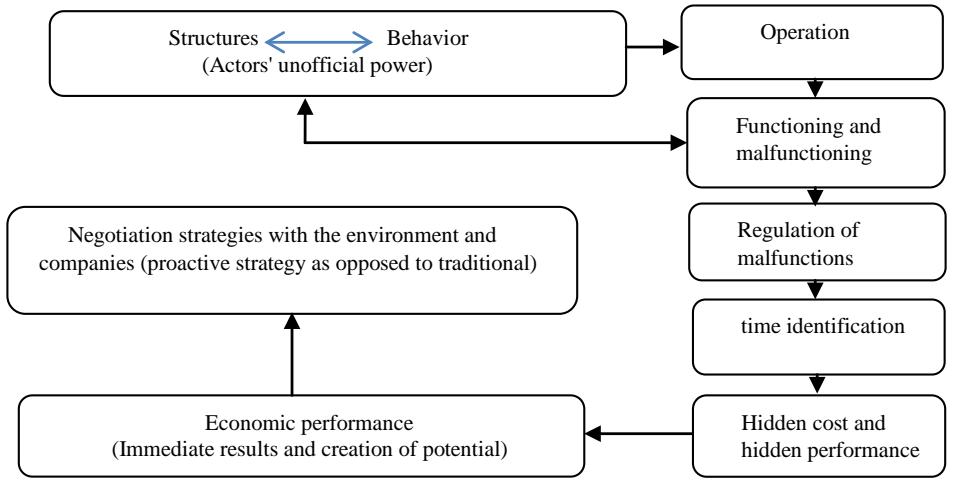

Based on the investigations developed by the authors Savall (1975); Savall (1979); Savall (1987), Savall & Zardet (2009) and Savall & Zardet (2010), when stating that the structure variable overlaps the behavior variable, and that having a variation in structures can vary the way workers act, this reality makes the behaviorist theory to the detriment of the structuralist theory taken into account.

To support this thought Savall & Zardet (1987), studied two identical structures, but produce different results in terms of personnel, given the differentiation of working conditions and levels of motivation that each structure provides to its workers.

Thus, the central hypothesis lies in the behavior to be presented by the employees in face of the organizational structures placed at their disposal, hence Savall et al (2008) apud Moreno et al (2020), refer that the hypothesis that guides the socio-economic methodology recognizes the unofficial power of the company's employees, taking into account the organizational structures.

Figure 1: Fundamental Hypothesis of Socio-Economic Theory

Source: Adaptation to Figure Saval Et AI (2008) For the successful measurement of hidden costs, the fundamental hypothesis rests around two concepts, one of which is added to this investigation: dysfunctions generated by the interaction between the behavior of workers and the structures of the organization in the informal sphere, time as the moment in which they occur and regulation of dysfunctions and the hidden costs generated.

The first concept, the malfunctioning that they are, is the result of the workers' unofficial power vis-à-vis the company's structures Savall et al (2008), representing the difference between normal functioning and the real or effective functioning obtained by workers in the performance of their duties.

The second concept is variable time, which allows measuring hidden costs in the face of malfunctions. For the regularization of dysfunctions, time is taken as a unit (hours, minutes...) translated into currency Savall & Zardet (2010).

This thought was applied by the author Lobo (1999), apud Oliveira et al (2019), when making an accounting connotation to hidden costs over time, noting that excessive overtime, excessive waiting hours in staff rotation, idleness due to production scheduling errors and consecutive time devoted to reducing failures and time spent to respond to customer complaints, are the basis for dealing with hidden costs in companies and organizations through the anticipated measurement of the corresponding time.

The third concept is, therefore, the hidden cost that is the result of malfunctions as the generating factor through the measurement ahead of time in the face of a certain indicator Savall et al (2008); corroborating with the emphasis mentioned by Martins (2013), when he says that identifying hidden costs is the initial step for companies and knowledge-based organizations to achieve their objectives.

Thus, the hidden costs respect the expression of the informal power of the employees of the organizations that is expressed through behavior, Brand, Vivanco and González (2017) and that are grouped into five (5) components (Over wages, overtime, overconsumption, non-production and non-creation of potential) with also five (5) indicators of hidden costs (absenteeism, accidents at work, staff turnover, quality defects, deviation in direct productivity and idleness) at the time of their evaluation.

## III. METHODOLOGY

The research focuses on the management of organizations, referring to the main theory, which is socio-economic, and the accounting of visible costs was through absorption costing, according to the thoughts of Ferreira, Caldeira, Asseiceiro & Vicente (2019), Caiado (2011), Tepa (2012) and Martins (2013) and, regarding hidden costs, was based on the socioeconomic method in the thinking defended by the authors Savall et al (2008) and Savall & Zardet (2010) through a specific qualification for simultaneous management of costs in organizations.

Based on the thinking of Tamo (2012), the requirement of a peculiar methodology capable of leading the researcher to achieve research results and with quality is fundamental in the originality of empirical knowledge.

The viability of the investigation was achieved, as always, by bringing together works by various authors, such as: books, newspapers, scientific articles that highlight the state of the art of the referenced theories, the results achieved for the second time in the field and which figured as the second structure of data to be analyzed and interpreted. The results were processed with software spss.

The software in the first instance was used to verify: reliability of the results achieved through Cronbachs Alpha and for the descriptive analysis of the data contained in the Capacity Grid, adapted to the competence grid of Savall & Zardet (2010), also adapted to the Likert scale, in order to identify the strategic activities capable of mitigating the levels of hidden costs observed in the first analysis.

However, the average was used as a determining indicator in identifying activities understood as strategic with a tendency to reduce the frequency of appearance of dysfunctions that caused the high level of hidden costs accounted for.

The set of activities in each explanatory variable and domain of solution originated the elaboration of the Capacity Grid for each indicator adapted to the competence grid Savall & Zardet (2010) and Tamo, (2012), resorting to the adaptation of the Likert scale where (1 - unimportant, 2- important) and, one (1) corresponds to "No" and two (2) corresponds to "Yes" in the structured interview carried out.

The strategic activities that can mitigate the dysfunctions that cause hidden costs are those that have average values that are in the range of 1.5 to 2 and are considered "important" and emphasize that the worker has little theoretical and practical knowledge on the referred variables and, therefore, the worker has difficulties in putting the knowledge into practice, meking it difficult for him to master the activities associated with the variables, thus causing dysfunctions that originate hidden costs through the generation of marginal time, hence the explanatory and domain variables solution in relation to the activities identified as being important and subject to re-observation after the mirror effect.

Activities with average values between 1 and 1.4 indicate that workers have theoretical and practical knowledge of explanatory and solution domain variables, and therefore, workers do not have difficulties in putting this knowledge into practice theorists. These activities cannot effectively cause hidden costs, hence they are not important in mitigating the frequency of malfunctions that cause hidden costs.

The interpretation of the results considers that, the higher value of the average score, the greater degree of the activity importance to the point of taking on the strategic name for the worker, and with that, thinking about monitoring it to mitigate the time of delays, absence and regulation of dysfunctions.

### a) Validation of Proposed Activities for Strategic Activities

The verification of the activities pertinence in the proposed solution is conditioned by the average value to have to conclude whether or not it takes the name of strategic activity. For this purpose, the spss software was used to determine the average value of each activity.

To this end, the behavior of the same department workers was again observed, in March 2023, in order to measure the degree of motivation achieved by them after the company had improved some working conditions, given training, had reinforced security levels, improved channels and means of communication and ways of controlling, after the mirror effect that occurred in the first survey.

Therefore, only the significant indicators were re-observed, as well as the malfunctions that caused the hidden costs during the first investigation. Refers to the indicators: absenteeism, staff turnover, quality defects, deviation in direct productivity and idleness, taking into account the malfunctions that caused the hidden costs accounted for.

b) Surveys, Techniques and Instruments Built for Data Collection

Following the thinking of Savall, et al (2008), the research-intervention was applied as the main one and which allowed direct contact with the Port Company of Cabinda-EP, information/knowledge was co-produced between the researchers and the workers of the referred company.

For data collection, two of the three techniques recommended in the socio-economic methodology were used and implemented simultaneously: participant observation and document analysis Savall & Zardet (2010). Two instruments were built: questionnaire, questionnaire grid and an observation grid or card.

The questionnaire was applied to the department head and the three (3) heads of each shift, and with every worker whenever necessary during observation and accidentally by a group of two or three technicians. The questionnaire served as a basis for identifying the activities considered strategic, with the worker simply stating that this activity can motivate him to better perform his duties.

From the participant observation it was possible to re-observe the dysfunctions for each worker in order to account for the frequency of occurrence of each dysfunction of hidden costs through the observation grids. Therefore, each form corresponded to a worker, satisfying eighty-nine (89) copies and were coded with the first letters of the first name and last name of the observed.

Therefore, three (3) previously trained observation groups were created to collect data with the necessary quality and reliability, composed of four (4) elements, namely: the researcher, each shift manager (three managers) and two (2) department technicians.

And for the documentary analysis, we were provided with the payroll for the month of March 2023, shift scales, functional organization chart, vacation plans, financial execution and the company's status, which served as the basis for data collection.

### c) Practices for Accounting the Frequency of Results

It was possible to analyze and account for the frequency of dysfunctions, through the number of minutes, of hidden hours that each file contained, using the techniques of document analysis and analysis of questionnaire results according to Savall & Zardet (2010), so that, if the exhaustion of the information analysis that each file presented, exhausting the analysis of all the information contained in the observation grid.

The documental analysis was fundamental in the analysis of the content they contained, enabling the calculation of the unit hours in each form, through the each factor frequency occurrence generating hidden cost taking into account its indicators: absenteeism, staff turnover, defects in quality, deviation in direct productivity and idleness.

With the payrolls, it was possible to extract the salary of the employees placed in the Operations Department in March 2023, identify the employees who were in full enjoyment of the disciplinary leave and the employees who earned overtime in the period under analysis; and with the statute it was possible to characterize the company, from its functioning to the knowledge of the procedures that regulate the operational activity of the Company, fact completed with its functional organigram.

With the interviews it was possible to analyse, identify the strategic activities and using the descriptive analysis of the spss software, for a precision of the results that were presented again to the heads of the department (mirror effect); as emphasized (Savall & Zardet, 2010) that the mirror effect is an important lever for the progress of the innovation process; if none of the actors does it, the analysis of the interviews would not be recognized; the status and competence of the interveners would be strongly questioned, which would slow down the efficiency of the process.

Thus, the hidden costs were accounted for in part together with the heads of the department, additional questionnaire were organized with those in charge to calculate with them the hidden costs resulting from the frequencies that the cards presented during the mirror effect phase.

### d) Qualimetry in Cost Accounting

For the complete accounting of the visible and hidden costs that occurred in the services provided by the company during the period under analysis, the qualimetry was used that made it possible to incorporate hidden costs in the cost accounting and management maps, that is, the accounting of costs visible and simultaneous accounting of hidden costs was only possible for the purposes of calculating costs and results, incorporating both types of costs in the absorption costing maps. Thus, one can verify the complementarity between socio-economic theory and cost and management accounting in terms of cost management in organizations.

### e) Proposed Solution

In this investigation, a solution proposal was set up by Savall & Zardet (2010), which could at least mitigate the frequency of dysfunctions and, concomitantly, the hidden costs accounted for at the time of the first research in the company, since its complete elimination is a condition of medium and long term. For this, the Plan of Priority Actions tool was applied, using explanatory variables and solution domains, namely: improvement of competence, improvement of working conditions, control and improvement of internal communication in the company, through the formulation of a set of strategic activities substantiated to each of the explanatory and solution domain variables.

### f) Hidden Costs Accountedin the First Survey

At this point, the hidden costs accounted for in the research carried out in December 2022 are presented in a synchronized way, taking into account the combination between the components and the hidden cost indicators, for a general appreciation, as can be seen in the Table 1, according to the article published by the authors Deco, Napolião, Tamo and Simbo (2023), regarding the indicator of hidden costs of absenteeism.

Table 1: General Assessment of Accounted Hidden Costs (€1=58 Kwanza "kz")

<table><tr><td></td><td colspan="3">Sobrecargas</td><td colspan="3">Nãoirosudos</td></tr><tr><td>Components</td><td rowspan="2">Extra wages (1)</td><td rowspan="2">Overtime (2)</td><td rowspan="2">Overconsumpti on (3)</td><td rowspan="2">Non-productio n (4)</td><td rowspan="2">Not creating potential (5)</td><td rowspan="2">Total hidden costs (1)+(2)+(3)+(4)+(5)</td></tr><tr><td>Indicators</td></tr><tr><td>Absenteeism</td><td>5.681.308,80</td><td>2.752.092,82</td><td>0</td><td>0</td><td>0</td><td>5.843.590,63</td></tr><tr><td>Work accidents</td><td>0</td><td>0</td><td>0</td><td>0</td><td>0</td><td>0</td></tr><tr><td>Staff rotation</td><td>0</td><td>539.268,62</td><td>0</td><td>0</td><td>0</td><td>498.368,75</td></tr><tr><td>Quality defects</td><td>501.899,58</td><td>0</td><td>0</td><td>0</td><td>0</td><td>424.644,69</td></tr><tr><td>Deviation in direct productivity</td><td>0</td><td>1.232.342,72</td><td>622.817,27</td><td>0</td><td>0</td><td>1.389.216,87</td></tr><tr><td>Idleness</td><td>0</td><td>364.575,97</td><td>0</td><td>0</td><td>0</td><td>236.438,35</td></tr><tr><td>Litigation</td><td>0</td><td>0</td><td>0</td><td>0</td><td>0</td><td>0</td></tr><tr><td>Totals</td><td>3.669.937,58</td><td>4.888.280,13</td><td>622.817,27</td><td>0</td><td>0</td><td>8.392.259,29</td></tr></table>

When introducing the concept of the solution proposal, the result of the absenteeism indicator and other hidden cost indicators constitute, therefore, the bases of comparison with the results to be verified through the predictive test of the proposed solution to be conceived (PAP) according to the reality of the company and with that, conclude whether or not the referred solution proposal is effective.

## IV. RESULTS AND DISCUSSION

### a) Data Confidence Level

Beforehand, it was necessary to verify the confidence level of the data in the results presented in the capacity grides of the absenteeism, staff rotation, quality defect, direct productivity deviation, and Idle indicators by observing the Cronbach Alpha value obtained using the spss statistical software.

Table 2: Reliability Level Analysis

<table><tr><td>Indicators</td><td>Alpha of Cronbach</td><td>Number of items</td></tr><tr><td>Absenteeism Capacity</td><td>0,729</td><td>18</td></tr><tr><td>Staff rotation capacity</td><td>0,871</td><td>7</td></tr><tr><td>Capacity for quality defect</td><td>0,832</td><td>18</td></tr><tr><td>Capacity in direct productivity deviation</td><td>0,797</td><td>18</td></tr><tr><td>Idle capacity</td><td>0,888</td><td>11</td></tr></table>

The data collected as shown in the table above reveal a sufficient confidence level of Cronbach's Alpha, suggesting that the structure of the sample and the respective results obtained are confident.

### b) Conceived Solution Proposal Versus the Observed Hidden Costs

In accordance with the precepts of socioeconomic theory and, with the objective of contributing to the mitigation of the levels of malfunctions found that cause the hidden costs accounted for, at this stage a proposal for a solution was constructed in accordance with the peculiar reality of the company with the in order to maximize economic, financial and social results through the level of hidden performing costs to be recovered.

### c) Proposed Explanatory and Solution Domain Variables

As the hidden costs were categorized by indicators and each dysfunction is categorized in its indicator, then, it was possible to relate the activities proposed by each indicator of hidden costs. Therefore, it was understood to confine in four (4) families the six (6) variables that explain the domain of solution of the hidden costs, as it can be seen below and that, controlled and improved, can excite the motivation of the workers.

Thus, the explanatory and solution domain variables of the factors that generate the hidden costs presented for mitigating the levels of dysfunction found were:

- Competence, working conditions, control and internal communication.

However, the explanatory variable implementation of the strategy was applied during the diagnosis process of hidden costs and which should be subsequently implemented at all levels of the company; the explanatory variable work organization is incorporated in the adequacy of jobs within the explanatory variable: working conditions, for better interdependence of the areas that make up the operations department; the time management variable was coupled to the control variable; and the variable integrated training was developed in the explanatory variable competence, while the variable communication-coordination and concertation was summarized in the variable internal communication.

Therefore, the aforementioned explanatory and solution domain variables were associated with the strategic activities to be developed, and, satisfied and/or applied by the company, they mitigate the malfunctions that cause hidden costs.

### d) Activities Proposed in each Explanatory Variable

Because the four (4) families or explanatory and solution domain variables are interactive among themselves, taking into account the dysfunctions and hidden costs, seventy-two (72) activities were proposed according to each indicator of hidden costs that were the subject of a structured interview with the eighty (89) employees assigned to the studied department.

However, the intention in the interviews was that each worker indicated or opined which or which activities, once implemented, can improve their behavior in the workplace and combined with the results of the "average" descriptive analysis, therefore, the investigation concluded that they might or might not mitigate the levels of dysfunctions or at least reduce their frequency.

The hidden cost related to the overpayment component was not the subject of the creation of a strategy for its mitigation during the prescription phase because it depends on the Executive, that is, because it depends on the revision of the General Labor Law in force in the Republic of Angola. Refer to workers' benefits, such as the vacation subsidy, thirteenth month subsidy.

### e) Proposed Activities for the Absenteeism Indicator

The table below illustrates the capacity grid relative to the results of the absenteeism indicator according to the structured interview carried out, for the purpose of measuring the level of reliability and descriptive analysis of the data to identify the strategic activities likely to mitigate the dysfunctions found and which originated the hidden costs observed in this indicator.

Table 3: Absenteeism Capacity Grid

<table><tr><td rowspan="2">Indicator</td><td rowspan="2">Explanatory variable</td><td rowspan="2">Activities</td><td rowspan="2">Code</td><td colspan="2">Answers</td></tr><tr><td>1</td><td>2</td></tr><tr><td rowspan="18">Absenteeism</td><td rowspan="4">Competence</td><td>training by need</td><td>Cm1</td><td>47</td><td>42</td></tr><tr><td>On-the-job training offered by the person in charge</td><td>Cm2</td><td>70</td><td>19</td></tr><tr><td>Systematization of knowledge of each task</td><td>Cm3</td><td>54</td><td>35</td></tr><tr><td>Responsibility for each task</td><td>Cm4</td><td>37</td><td>52</td></tr><tr><td rowspan="7">Conditions of work</td><td>Modern and safe infrastructures</td><td>Ct1</td><td>20</td><td>69</td></tr><tr><td>Modern and cutting-edge technology</td><td>Ct2</td><td>66</td><td>23</td></tr><tr><td>Healthy sanitary facilities</td><td>Ct3</td><td>71</td><td>18</td></tr><tr><td>Safety at work</td><td>Ct4</td><td>78</td><td>11</td></tr><tr><td>Fair and adequate compensation</td><td>Ct5</td><td>77</td><td>12</td></tr><tr><td>pay equity</td><td>Ct6</td><td>21</td><td>68</td></tr><tr><td>reward valence</td><td>Ct7</td><td>28</td><td>61</td></tr><tr><td rowspan="3">Control</td><td>Monitoring the completion of the task</td><td>C1</td><td>26</td><td>63</td></tr><tr><td>Performance evaluation</td><td>C2</td><td>79</td><td>10</td></tr><tr><td>Request for results</td><td>C3</td><td>40</td><td>49</td></tr><tr><td rowspan="4">Internal Communication</td><td>Dissemination of information through conventional company channels</td><td>Ci1</td><td>85</td><td>4</td></tr><tr><td>Broadcasting a single message</td><td>Ci2</td><td>24</td><td>65</td></tr><tr><td>Dissemination of recognition of the merit of Workers</td><td>Ci3</td><td>36</td><td>53</td></tr><tr><td>Diffusion of reinforcement of values and good conduct in the Leadership</td><td>Ci4</td><td>26</td><td>63</td></tr></table>

As for absenteeism, it is necessary to highlight all the explanatory variables of the solution domain when the issue is addressing the dysfunctions that cause hidden costs.

### f) Results of the Descriptive Analysis to Identify Strategic Activities

The hidden cost indicator absenteeism is explained by the improvement of workers' skills, the improvement of some working conditions, the performance evaluation and the dissemination of internal information through conventional channels, as can be seen in the Table 4:

Table 4: Identification of Strategic Activities

<table><tr><td rowspan="2">Actividades</td><td rowspan="2">N</td><td colspan="2">Mean</td><td rowspan="2">Statistical deviation</td><td rowspan="2">Statistical variation</td></tr><tr><td>Statistica</td><td>Standard deviation</td></tr><tr><td>Com1_Training by necessity</td><td>89</td><td>1,76</td><td>0,050</td><td>0,475</td><td>0,226</td></tr><tr><td>Com2_On-job training</td><td>89</td><td>1,88</td><td>0,044</td><td>0,420</td><td>0,176</td></tr><tr><td>Com3_Systematization of the knowledge of each task</td><td>89</td><td>1,75</td><td>0,051</td><td>0,479</td><td>0,230</td></tr><tr><td>Com4_Accountability of the task</td><td>89</td><td>1,47</td><td>0,051</td><td>0,486</td><td>0,236</td></tr><tr><td>Ct1Modern and safe infrastructure</td><td>89</td><td>1,28</td><td>0,041</td><td>0,386</td><td>0,149</td></tr><tr><td>Ct2 Modern technology</td><td>89</td><td>1,65</td><td>0,038</td><td>0,355</td><td>0,126</td></tr><tr><td>Ct3_Healthy sanitary facilities</td><td>89</td><td>1,78</td><td>0,035</td><td>0,331</td><td>0,110</td></tr><tr><td>Ct4_Safety at work</td><td>89</td><td>1,80</td><td>0,032</td><td>0,303</td><td>0,092</td></tr><tr><td>Ct5_Fair and adequate compensation</td><td>89</td><td>1,98</td><td>0,035</td><td>0,331</td><td>0,110</td></tr><tr><td>Ct6_Wage equity</td><td>89</td><td>1,31</td><td>0,044</td><td>0,412</td><td>0,170</td></tr><tr><td>Nt7_Valency of the reward</td><td>89</td><td>1,15</td><td>0,046</td><td>0,434</td><td>0,188</td></tr><tr><td>C1_Self control</td><td>89</td><td>1,37</td><td>0,047</td><td>0,446</td><td>0,199</td></tr><tr><td>C2_Performance evaluation</td><td>89</td><td>1,67</td><td>0,036</td><td>0,343</td><td>0,118</td></tr><tr><td>C3_Request for results</td><td>89</td><td>1,44</td><td>0,053</td><td>0,503</td><td>0,253</td></tr><tr><td>Ci1_Diffusion of information through conventional channels</td><td>89</td><td>1,83</td><td>0,027</td><td>0,252</td><td>0,064</td></tr><tr><td>Ci2_Single message broadcast</td><td>89</td><td>1,31</td><td>0,044</td><td>0,412</td><td>0,170</td></tr><tr><td>Ci3_Dissemination of workers' merit recognition</td><td>89</td><td>1,14</td><td>0,050</td><td>0,475</td><td>0,226</td></tr><tr><td>Ci4_Dissemination of reinforcement of values and good leadership conduct</td><td>89</td><td>1,23</td><td>0,050</td><td>0,471</td><td>0,222</td></tr></table>

The high levels of hidden costs found in the absenteeism indicator are mitigated, in part by improving the competence of workers, namely: training by necessity, training must take place in the workplace "on the job" and systematize the knowledge of each task carried out in that department. It should be based on improving working conditions by adhering to new technologies, adequate sanitary facilities, safety at the height of the type of work carried out and receiving compensatory wages for the exerted effort. Based on self-control based on performance assessment and dissemination of information using the company's official channels (windows, circulars and intranet) so that all department workers are aware of the instructions issued by those responsible in time.

With this, time will be well managed to the point that each professional performs their duties in a timely manner by improving arrival time (being punctual), improving absences (being diligent at work), which actually inhibits procrastination, providing more individual and consequently collective productivity.

### g) Activities Proposed for the Staff Rotation Indicator

According to the capacity grid below, it was understood that the company should monitor control and focus on internal communication using more efficient channels, measuring the level of reliability and adjustment to normality of the collected data.

Table 5: Staff Rotation Capacity Grid

<table><tr><td rowspan="2">Indicator</td><td rowspan="2">Explanatory Variable</td><td rowspan="2">Strategic Activity</td><td rowspan="2">Code</td><td colspan="2">Answers</td></tr><tr><td>1</td><td>2</td></tr><tr><td rowspan="7">staff rotation</td><td rowspan="3">Control</td><td>Performance evaluation/Monitoring in carrying out the task</td><td>C1</td><td>21</td><td>68</td></tr><tr><td>Performance evaluation</td><td>C2</td><td>56</td><td>33</td></tr><tr><td>Request for results</td><td>C3</td><td>19</td><td>70</td></tr><tr><td rowspan="4">Internal Communication</td><td>Dissemination of information through the company's conventional channels</td><td>Ci1</td><td>66</td><td>23</td></tr><tr><td>Broadcasting a single message</td><td>Ci2</td><td>16</td><td>73</td></tr><tr><td>Dissemination of recognition of the merit of Workers</td><td>Ci3</td><td>24</td><td>65</td></tr><tr><td>Diffusion of reinforcement of values and good conduct in the Leadership</td><td>Ci4</td><td>38</td><td>51</td></tr></table>

As can be seen in the table above, the worker answered affirmatively or negatively, the activities that may or may not motivate him. Therefore, they were the subject of descriptive analysis to find those that would be figured as strategic and capable of reducing the time to replace the colleague at the job.

### h) Results of the Descriptive Analysis to Identify Strategic Activities

The Table 6 presents the results of the descriptive analysis for the identification of activities considered strategic according to the average value achieved.

Table 6: Identification of Strategic Activities

<table><tr><td rowspan="2"></td><td rowspan="2">Number</td><td colspan="2">Non-parametric test (a,b)</td><td colspan="3">Most extremes are different</td><td rowspan="2">Kolmogorov-Smirnov Z</td><td rowspan="2">Asymp. Sig. (2-tailed)</td></tr><tr><td>Mean</td><td>Standar deviation</td><td>Absolute</td><td>Positive</td><td>Negative</td></tr><tr><td>C1_Self control</td><td>89</td><td>1,31</td><td>0,412</td><td>0,484</td><td>0,484</td><td>-0,302</td><td>4,569</td><td>0,000</td></tr><tr><td>C2_Performance evaluation/task monitoring</td><td>89</td><td>1,85</td><td>0,434</td><td>0,468</td><td>0,284</td><td>-0,468</td><td>4,419</td><td>0,000</td></tr><tr><td>C3_Request for results</td><td>89</td><td>1,17</td><td>0,446</td><td>0,457</td><td>0,457</td><td>-0,273</td><td>4,316</td><td>0,000</td></tr><tr><td>Ci1_Dissemination of information through the company's conventional channels</td><td>89</td><td>1,75</td><td>0,355</td><td>0,513</td><td>0,340</td><td>-0,513</td><td>4,844</td><td>0,000</td></tr><tr><td>Ci2_Single message broadcast</td><td>89</td><td>1,29</td><td>0,395</td><td>0,495</td><td>0,495</td><td>-0,314</td><td>4,665</td><td>0,000</td></tr><tr><td>Ci3_Dissemination of workers' merit recognition</td><td>89</td><td>1,56</td><td>0,467</td><td>0,435</td><td>0,435</td><td>-0,250</td><td>4,105</td><td>0,000</td></tr><tr><td>Ci4_Dissemination of reinforcement of values and good leadership conduct</td><td>89</td><td>1,25</td><td>0,479</td><td>0,418</td><td>0,418</td><td>-0,261</td><td>3,944</td><td>0,000</td></tr></table>

According to the table above, in order to motivate workers so that they can show up at the ideal time to relieve their colleague, it is necessary to monitor control and carry out internal communication using more efficient channels. Therefore, adhering to the intratnet, showcases, circulars, briefing and internal phone calls and to a performance assessment combined with monitoring the performance of tasks is essential to be able to positively influence the worker, to the point of winning their job in the recommended time.

### i) Activities Proposed for the Quality Defect Indicator

The Table 7 illustrates the capacity grid of the indicator defect in the quality of the results of the structured interview for the purpose of measuring the level of reliability and testing the normality of the results.

Table 7: Capacity Grid for Quality Defect

<table><tr><td rowspan="2">Indicator</td><td rowspan="2">Explanatory variable</td><td rowspan="2">Strategic activity</td><td rowspan="2">Code</td><td colspan="2">Answers</td></tr><tr><td>1</td><td>2</td></tr><tr><td rowspan="9"></td><td rowspan="4">Competence</td><td>Training by need</td><td>Cm1</td><td>55</td><td>34</td></tr><tr><td>On-the-job training offered by the person in charge</td><td>Cm2</td><td>40</td><td>49</td></tr><tr><td>Sistemáticação dos acontecimentos de cada tarefa</td><td>Cm3</td><td>67</td><td>22</td></tr><tr><td>Responsibility for each task</td><td>Cm4</td><td>38</td><td>51</td></tr><tr><td rowspan="5">Conditions of work</td><td>Modern and safe infrastructures</td><td>Ct1</td><td>44</td><td>45</td></tr><tr><td>Modern and cutting-edge technology</td><td>Ct2</td><td>67</td><td>22</td></tr><tr><td>Healthy sanitary facilities</td><td>Ct3</td><td>64</td><td>25</td></tr><tr><td>Safety at work</td><td>Ct4</td><td>71</td><td>18</td></tr><tr><td>Fair and adequate compensation</td><td>Ct5</td><td>69</td><td>20</td></tr><tr><td rowspan="9">Absenteeism</td><td rowspan="2"></td><td>Pay equity</td><td>Ct6</td><td>66</td><td>23</td></tr><tr><td>Reward valence</td><td>Ct7</td><td>48</td><td>41</td></tr><tr><td rowspan="3">Control</td><td>Monitoring the completion of the task</td><td>C1</td><td>30</td><td>59</td></tr><tr><td>Performance evaluation</td><td>C2</td><td>58</td><td>31</td></tr><tr><td>Request for results</td><td>C3</td><td>50</td><td>39</td></tr><tr><td rowspan="4">Internal Communication</td><td>Dissemination of information through the company's conventional channels</td><td>Ci1</td><td>74</td><td>15</td></tr><tr><td>Broadcasting a single message</td><td>Ci2</td><td>66</td><td>23</td></tr><tr><td>Dissemination of recognition of the merit of Workers</td><td>Ci3</td><td>37</td><td>52</td></tr><tr><td>Diffusion of reinforcement of values and good conduct in the Leadership</td><td>Ci4</td><td>32</td><td>57</td></tr></table>

### j) Results of the Descriptive Analysis to Identify Strategic Activities

The decrease in paid time without any actual work departure for the quality defect indicator is explained by the improvement in workers' skills, in the improvement of some working conditions, in the improvement of some control actions and in the improvement of internal communication, as can be seen in the Table 8.

Table 8: Identification of Strategic Activities

<table><tr><td rowspan="2">Activities</td><td rowspan="2">N</td><td colspan="2">Mean</td><td rowspan="2">Statistical deviation</td><td rowspan="2">Statistical variation</td></tr><tr><td>Statistics</td><td>Standaed deviation</td></tr><tr><td>Com1_Training by necessity</td><td>89</td><td>1,64</td><td>0,047</td><td>0,440</td><td>0,194</td></tr><tr><td>Com2_On-job training</td><td>89</td><td>1,74</td><td>0,053</td><td>0,501</td><td>0,251</td></tr><tr><td>Com3_Systematization of the knowledge of each task</td><td>89</td><td>1,79</td><td>0,048</td><td>0,457</td><td>0,209</td></tr><tr><td>Com4_Accountability of the task</td><td>89</td><td>1,64</td><td>0,053</td><td>0,501</td><td>0,251</td></tr><tr><td>Ct1Modern and safe infrastructure</td><td>89</td><td>1,88</td><td>0,053</td><td>0,503</td><td>0,253</td></tr><tr><td>Ct2Modern technology</td><td>89</td><td>1,68</td><td>0,044</td><td>0,420</td><td>0,176</td></tr><tr><td>Ct3_Healthy sanitary facilities</td><td>89</td><td>1,23</td><td>0,040</td><td>0,376</td><td>0,142</td></tr><tr><td>Ct4_Safety at work</td><td>89</td><td>1,69</td><td>0,044</td><td>0,412</td><td>0,170</td></tr><tr><td>Ct5_Fair and adequate compensation</td><td>89</td><td>1,56</td><td>0,050</td><td>0,475</td><td>0,226</td></tr><tr><td>Ct6_Wage equity</td><td>89</td><td>1,82</td><td>0,048</td><td>0,452</td><td>0,204</td></tr><tr><td>Nt7_Valency of the reward</td><td>89</td><td>1,34</td><td>0,053</td><td>0,503</td><td>0,253</td></tr><tr><td>C1_Self control</td><td>89</td><td>1,32</td><td>0,044</td><td>0,420</td><td>0,176</td></tr><tr><td>C2_Performance evaluation</td><td>89</td><td>1,69</td><td>0,044</td><td>0,412</td><td>0,170</td></tr><tr><td>C3_Request for results</td><td>89</td><td>1,77</td><td>0,053</td><td>0,497</td><td>0,247</td></tr><tr><td>Ci1_Diffusion of information through conventional channels</td><td>89</td><td>1,82</td><td>0,048</td><td>0,452</td><td>0,204</td></tr><tr><td>Ci2_Single message broadcast</td><td>89</td><td>1,62</td><td>0,048</td><td>0,452</td><td>0,204</td></tr><tr><td>Ci3_Dissemination of workers' merit recognition</td><td>89</td><td>1,26</td><td>0,051</td><td>0,483</td><td>0,233</td></tr><tr><td>Ci4_Dissemination of reinforcement of values and good leadership conduct</td><td>89</td><td>1,22</td><td>0,047</td><td>0,446</td><td>0,199</td></tr></table>

Therefore, the mitigation of malfunctions and hidden costs accounted for in the quality defect indicator is explained in the improvement of skills levels (preferably providing on-the-job training, systematization of tasks), in the improvement of control levels (evaluating performance and monitoring achievement of activities to carry out the task on time and issue a report on its execution), improving some working conditions (opting for modern infrastructure, opting for equipment with the latest technology, improving safety in handling

equipment, improving lighting in the park and facilities, improvement of dormitory conditions, salary equity and salary improvement) and the option of communication processed via personal telephone (mobile phone), i.e., the responsible person must communicate with the technicians through an existing fixed telephone and at mobile of each worker when it comes to guidelines.

### k) Activities Proposed for the Direct Productivity Deviation Indicator

For the direct productivity deviation indicator, the company should monitor the variables: competence, working conditions, control and internal communication, as can be seen in the capacity grid of the structured interview.

Table 9: Capacity grid in direct productivity deviation

<table><tr><td rowspan="2">Indicator</td><td rowspan="2">Explanatory variable</td><td rowspan="2">Strategic activity</td><td rowspan="2">Code</td><td colspan="2">Answers</td></tr><tr><td>1</td><td>2</td></tr><tr><td rowspan="18">Absenteeism</td><td rowspan="4">Competence</td><td>Training by need</td><td>Cm1</td><td>59</td><td>30</td></tr><tr><td>On-the-job training offered by the person in charge</td><td>Cm2</td><td>45</td><td>44</td></tr><tr><td>Sistematização dos acontecimentos de cada tarefa</td><td>Cm3</td><td>58</td><td>31</td></tr><tr><td>Responsibility for each task</td><td>Cm4</td><td>49</td><td>40</td></tr><tr><td rowspan="7">Conditions of work</td><td>Modern and safe infrastructures</td><td>Ct1</td><td>51</td><td>38</td></tr><tr><td>Modern and cutting-edge technology</td><td>Ct2</td><td>47</td><td>42</td></tr><tr><td>Healthy sanitary facilities</td><td>Ct3</td><td>73</td><td>16</td></tr><tr><td>Safety at work</td><td>Ct4</td><td>71</td><td>18</td></tr><tr><td>Fair and adequate compensation</td><td>Ct5</td><td>57</td><td>32</td></tr><tr><td>Pay equity</td><td>Ct6</td><td>41</td><td>48</td></tr><tr><td>Reward valence</td><td>Ct7</td><td>39</td><td>50</td></tr><tr><td rowspan="3">Control</td><td>Monitoring the completion of the task</td><td>C1</td><td>51</td><td>38</td></tr><tr><td>Performance evaluation</td><td>C2</td><td>79</td><td>10</td></tr><tr><td>Request for results</td><td>C3</td><td>61</td><td>28</td></tr><tr><td rowspan="4">Internal Communication</td><td>Dissemination of information through the company's conventional channels</td><td>Ci1</td><td>58</td><td>31</td></tr><tr><td>Broadcasting a single message</td><td>Ci2</td><td>56</td><td>33</td></tr><tr><td>Dissemination of recognition of the merit of Workers</td><td>Ci3</td><td>48</td><td>41</td></tr><tr><td>Diffusion of reinforcement of values and good conduct in the Leadership</td><td>Ci4</td><td>50</td><td>39</td></tr></table>

### i) Results of the Descriptive Analysis to Identify Strategic Activities

It can be understood from the table below that, in order to combat the level of dysfunctions related to the deviation in direct productivity, the company must experience improvements in all explanatory and solution domain variables presented: Skills, working conditions, control and internal communication.

Table 10: Identification of Strategic Activities

<table><tr><td rowspan="2">Actividades</td><td rowspan="2">N</td><td colspan="2">Mean</td><td rowspan="2">Statistical deviation</td><td rowspan="2">Statistical variation</td></tr><tr><td>Statistics</td><td>Standaed deviation</td></tr><tr><td>Com1_Training by necessity</td><td>89</td><td>1,72</td><td>0,052</td><td>0,489</td><td>0,239</td></tr><tr><td>Com2_On-job training</td><td>89</td><td>1,55</td><td>0,051</td><td>0,479</td><td>0,230</td></tr><tr><td>Com3_Systematization of the knowledge of each task</td><td>89</td><td>1,71</td><td>0,042</td><td>0,395</td><td>0,156</td></tr><tr><td>Com4_Accountability of the task</td><td>89</td><td>1,58</td><td>0,053</td><td>0,503</td><td>0,253</td></tr><tr><td>Ct1Modern and safe infrastructure</td><td>89</td><td>1,63</td><td>0,053</td><td>0,502</td><td>0,252</td></tr><tr><td>Ct2Modern technology</td><td>89</td><td>1,78</td><td>0,035</td><td>0,331</td><td>0,110</td></tr><tr><td>Ct3_Healthy sanitary facilities</td><td>89</td><td>1,85</td><td>0,039</td><td>0,366</td><td>0,134</td></tr><tr><td>Ct4_Safety at work</td><td>89</td><td>1,95</td><td>0,019</td><td>0,181</td><td>0,033</td></tr><tr><td>Ct5_Fair and adequate compensation</td><td>89</td><td>1,80</td><td>0,048</td><td>0,452</td><td>0,204</td></tr><tr><td>Ct6_Wage equity</td><td>89</td><td>1,34</td><td>0,053</td><td>0,499</td><td>0,249</td></tr><tr><td>Nt7_Valency of the reward</td><td>89</td><td>1,59</td><td>0,053</td><td>0,503</td><td>0,253</td></tr><tr><td>C1_Self control</td><td>89</td><td>1,48</td><td>0,053</td><td>0,501</td><td>0,251</td></tr><tr><td>C2_Performance evaluation</td><td>89</td><td>1,77</td><td>0,036</td><td>0,343</td><td>0,118</td></tr><tr><td>C3_Request for results</td><td>89</td><td>1,58</td><td>0,053</td><td>0,503</td><td>0,253</td></tr><tr><td>Ci1_Diffusion of information through conventional channels</td><td>89</td><td>1,78</td><td>0,047</td><td>0,440</td><td>0,194</td></tr><tr><td>Ci2_Single message broadcast</td><td>89</td><td>1,43</td><td>0,053</td><td>0,499</td><td>0,249</td></tr><tr><td>Ci3_Dissemination of workers' merit recognition</td><td>89</td><td>1,39</td><td>0,048</td><td>0,457</td><td>0,209</td></tr><tr><td>Ci4_Dissemination of reinforcement of values and good leadership conduct</td><td>89</td><td>1,28</td><td>0,052</td><td>0,489</td><td>0,239</td></tr></table>

The activities considered strategic can optimize the moments for making a decision on the part of those responsible for the Department and reduce the time to recover the equipment whenever it breaks down and help the workers to recover their work position as soon as possible after the meal period, due to the increased levels of control, improved working conditions, improved skills and adoption of more efficient internal communication channels. With this, workers will receive more knowledge substantiated in the know-how, know- how, know-how, through training linked to the explanatory variables and mastery of solutions to the malfunctions and hidden costs accounted for.

### j) Proposed Activities for the Idleness Indicator

The Table 11 illustrates the capacity grid of the results of the structured interview for the idleness indicator for the purpose of measuring the level of reliability and the normality adjustment test.

Table 11: Idle Capacity Grid

<table><tr><td rowspan="2">Indicator</td><td rowspan="2">Explanatory variable</td><td rowspan="2">Strategic activity</td><td rowspan="2">Code</td><td colspan="2">Answers</td></tr><tr><td>1</td><td>2</td></tr><tr><td rowspan="11">Idleness</td><td rowspan="7">Conditions of work</td><td>Training by need</td><td>Ct1</td><td>54</td><td>35</td></tr><tr><td>Modern and cutting-edge technology</td><td>Ct2</td><td>82</td><td>7</td></tr><tr><td>Healthy sanitary facilities</td><td>Ct3</td><td>70</td><td>19</td></tr><tr><td>Safety at work</td><td>Ct4</td><td>72</td><td>17</td></tr><tr><td>Fair and adequate compensation</td><td>Ct5</td><td>68</td><td>21</td></tr><tr><td>Pay equity</td><td>Ct6</td><td>24</td><td>65</td></tr><tr><td>Reward valence</td><td>Ct7</td><td>59</td><td>30</td></tr><tr><td rowspan="4">Internal Communication</td><td>Dissemination of information through the company's conventional channels</td><td>Ci1</td><td>73</td><td>16</td></tr><tr><td>Broadcasting a single message</td><td>Ci2</td><td>41</td><td>48</td></tr><tr><td>Dissemination of recognition of the merit of Workers</td><td>Ci3</td><td>39</td><td>50</td></tr><tr><td>Diffusion of reinforcement of values and good conduct in the Leadership</td><td>Ci4</td><td>35</td><td>54</td></tr></table>

According to the table above, the interviewees answered yes or no to the priority activities that the company must improve in order to increase motivation levels and consequently reduce the time spent at home compared to the vacation time granted by law.

### k) Results of the Descriptive Analysis to Identify Strategic Activities

There is good confidence in the data regarding the results found for the idleness indicator, as can be seen in the Table 2.

Table 12: Identification of Strategic Activities

<table><tr><td rowspan="2"></td><td rowspan="2">N</td><td colspan="2">Non-Parametric Test (a, b)</td><td colspan="3">Most Extremes are Different</td><td rowspan="2">Kolmogorov-Smirnov Z</td><td rowspan="2">Asymp. Sig. (2-tailed)</td></tr><tr><td>Mean</td><td>Standar Deviation</td><td>Absolute</td><td>Positive</td><td>Negative</td></tr><tr><td>Ct1Modern and safe infrastructure</td><td>89</td><td>1,58</td><td>0,502</td><td>0,354</td><td>0,325</td><td>-0,354</td><td>3,344</td><td>0,000</td></tr><tr><td>Ct2Modern technology</td><td>89</td><td>1,78</td><td>0,331</td><td>0,522</td><td>0,354</td><td>-0,522</td><td>4,924</td><td>0,000</td></tr><tr><td>Ct3Healthy sanitary installations</td><td>89</td><td>1,89</td><td>0,366</td><td>0,509</td><td>0,334</td><td>-0,509</td><td>4,802</td><td>0,000</td></tr><tr><td>Ct4Safety at work</td><td>89</td><td>1,87</td><td>0,181</td><td>0,540</td><td>0,426</td><td>-0,540</td><td>5,094</td><td>0,000</td></tr><tr><td>Ct5Fair and adequate compensation</td><td>89</td><td>1,79</td><td>0,452</td><td>0,452</td><td>0,267</td><td>-0,452</td><td>4,264</td><td>0,000</td></tr><tr><td>Ct6_Wage equity</td><td>89</td><td>1,35</td><td>0,499</td><td>0,372</td><td>0,372</td><td>-0,308</td><td>3,508</td><td>0,000</td></tr><tr><td>Nt7_Valency of the reward</td><td>89</td><td>1,59</td><td>0,503</td><td>0,343</td><td>0,343</td><td>-0,337</td><td>3,235</td><td>0,000</td></tr><tr><td>Ci1_Dissemination of information through the company's conventional channels</td><td>89</td><td>1,64</td><td>0,440</td><td>0,463</td><td>0,279</td><td>-0,463</td><td>4,368</td><td>0,000</td></tr><tr><td>Ci2_Single message broadcast</td><td>89</td><td>1,24</td><td>0,499</td><td>0,372</td><td>0,372</td><td>-0,308</td><td>3,508</td><td>0,000</td></tr><tr><td>Ci3_Dissemination of workers' merit recognition</td><td>89</td><td>1,69</td><td>0,457</td><td>0,446</td><td>0,446</td><td>-0,261</td><td>4,211</td><td>0,000</td></tr><tr><td>Ci4_Dissemination of reinforcement of values and good leadership conduct</td><td>89</td><td>1,34</td><td>0,489</td><td>0,401</td><td>0,401</td><td>-0,279</td><td>3,781</td><td>0,000</td></tr></table>

In order to monitor idleness, it is understood that the company must base its strategy on the continuous improvement of working conditions and, therefore, instill a communication culture through formal channels in addition to informal channels, as can be seen in the table above.

Improving working conditions and focusing on efficient internal communication can positively persuade workers to avoid staying at home longer than that established in the general labor law in force in the Republic of Angola regarding the enjoyment of disciplinary leave (article number 129 in section II of the chapter VII), regarding the right to leave and (in article number 131) of the same section and chapter where the duration of the same is foreseen, a measure also supported in the company's internal instructions.

### l) Plan of Priority Activities (Actions) Built

In order to combat the identified dysfunctions and the hidden costs accounted for in the first survey, a solution proposal was constructed, through the identification of activities considered to be strategic capable of mitigating the identified dysfunctions or at least reducing their frequency and, consequently, the costs accounted for and, therefore, summarized at this stage through the Priority Activities Plan (PAP) tool, as can be seen below:

Table 13: Priority Activities Plan (PAP)

<table><tr><td>Indicators</td><td>Observed Dysfunctions</td><td>Explanatory Variables</td><td>Proposed activities</td><td>Average value of the activity</td><td>Strategic activities</td><td>Strategic activities triggered immediately</td><td>Decrease or not of hidden costs</td></tr><tr><td rowspan="9">Absenteeism</td><td rowspan="3">Paid compensation time</td><td rowspan="4">Competence</td><td>training by need</td><td>1,7629</td><td>training by need</td><td></td><td rowspan="9">See the results of predictive test</td></tr><tr><td>On-the-job training offered by the person in charge</td><td>1,8753</td><td>On-the-job training offered by the person in charge</td><td>On-the-job training offered by the person in charge</td></tr><tr><td>Systematization of the knowledge of each task</td><td>1,7517</td><td>Systematization of the knowledge of each task</td><td>Systematization of the knowledge of each task</td></tr><tr><td rowspan="4">Paid vacation allowance time</td><td>Responsibility for each task</td><td>1,4708</td><td></td><td></td></tr><tr><td rowspan="5">Work conditions</td><td>Modern and safe infrastructures</td><td>1,2798</td><td></td><td></td></tr><tr><td>Modern and cutting-edge technology</td><td>1,6539</td><td>Modern and cutting-edge technology</td><td></td></tr><tr><td>Healthy sanitary facilities</td><td>1,7764</td><td>Healthy sanitary facilities</td><td>Healthy sanitary facilities</td></tr><tr><td rowspan="2">Thirteenth month</td><td>Safety at work</td><td>1,7989</td><td>Safety at work</td><td></td></tr><tr><td>Fair and adequate</td><td>1,9764</td><td>Fair and</td><td>Fair and</td></tr></table>

<table><tr><td rowspan="3" colspan="2">Quality defects</td><td colspan="101">Staff rotation</td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td></tr><tr><td>Time paid in hours spent to correct a fault by the colleague during the knowledge of each task</td><td colspan="100">Communication</td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td></tr><tr><td>Time paid in hours spent to correct a fault by the colleague during the knowledge of each task</td><td>Performance of his duties.</td><td>Training by need</td><td>1,739</td><td>1,7879</td><td>1,739</td><td>1,7879</td><td>1,739</td><td>1,739</td><td>1,739</td><td>1,739</td><td>1,739</td><td>1,739</td><td>1,739</td><td>1,739</td><td>1,739</td><td>1,739</td><td>1,739</td><td>1,739</td><td>1,739</td><td>1,739</td><td>1,739</td><td>1,739</td><td>1,739</td><td>1.5646</td><td>Dissertation of recognition of the merit of workers</td><td>of recognition of the merit of workers</td><td>Dissertation of recognition of the merit of workers</td><td>Dissertation of recognition of the merit of workers</td><td>Dissertation of recognition of the merit of workers</td><td>Dissertation of recognition of the merit of workers</td><td>Dissertation of recognition of the merit of workers</td><td>Dissertation of recognition of the merit of workers</td><td>Dissertation of recognition of the merit of workers</td><td>Dissertation of recognition of the merit of workers</td><td>Dissertation of recognition of the merit of workers</td><td>Dissertation of Recognition of Recognition of the merit of workers</td><td>Dissertation of Recognition of Recognition of the merit of workers</td><td>Dissertation of Recognition of Recognition of the merit of workers</td><td>Dissertation of Recognition of Recognition of the merit of workers</td><td>Dissertation of Recognition of Recognition of Recognition of the merit of workers</td><td>Dissertation of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition ofRecognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of</td><td>Dissertation of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of Recognition of</td><td>Dissertation</td><td>Evaluation</td><td>Performance</td><td>Evaluation</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>Performance</td><td>PERCENTHEATNESS</td><td>PERCENTAGE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENType</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYEATHEATNESS</td><td>PERCENTAGE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td><td>PERCENTYPE</td></tr></table>

<table><tr><td rowspan="15"></td><td rowspan="5"></td><td></td><td>Responsibility for each task</td><td>1,6393</td><td>Responsibility for each task</td><td>Responsibility for each task</td></tr><tr><td rowspan="4">Work conditions</td><td>Modern and safe infrastructures</td><td>1,8831</td><td>Modern and safe infrastructures</td><td>Modern and safe infrastructures</td></tr><tr><td>Modern and cutting-edge technology</td><td>1,6753</td><td>Modern and cutting-edge technology</td><td></td></tr><tr><td>Healthy sanitary facilities</td><td>1,2315</td><td></td><td></td></tr><tr><td>Safety at work</td><td>1,6865</td><td>Safety at work</td><td></td></tr><tr><td rowspan="10">Observed Dysfunctions</td><td rowspan="6">Control</td><td>Fair and adequate compensation</td><td>1,5629</td><td>Fair and adequate compensation</td><td>Fair and adequate compensation</td></tr><tr><td>pay equity</td><td>1,8191</td><td>pay equity</td><td></td></tr><tr><td>reward valence</td><td>1,3431</td><td></td><td></td></tr><tr><td>Monitoring the completion of the task</td><td>1,3247</td><td></td><td></td></tr><tr><td>Performance evaluation</td><td>1,6865</td><td>Performance evaluation</td><td>Performance evaluation</td></tr><tr><td>Request for results</td><td>1,773</td><td>Request for results</td><td></td></tr><tr><td rowspan="4">Internal communication</td><td>Dissemination of information through the company's conventional channels</td><td>1,8191</td><td>Dissemination of information through the company's conventional channels</td><td>Dissemination of information through the company's conventional channels</td></tr><tr><td>Broadcasting a single message</td><td>1,6191</td><td>Broadcasting a single message</td><td>Broadcasting a single message</td></tr><tr><td>Dissemination of recognition of the merit of workers</td><td>1,2596</td><td></td><td></td></tr><tr><td>Diffusion of reinforcement of values and good conduct in leadership</td><td>1,2197</td><td></td><td></td></tr><tr><td rowspan="8">Deviations in direct productivity</td><td rowspan="7">Time paid in hours derived from the difference between the time recommended to perform a task and the time actually spent to carry it out.</td><td rowspan="4">Competence</td><td>training by need</td><td>1,718</td><td>training by need</td><td></td></tr><tr><td>On-the-job training offered by the person in charge</td><td>1,5517</td><td>On-the-job training offered by the person in charge</td><td>On-the-job training offered by the person in charge</td></tr><tr><td>Systematization of the knowledge of each task</td><td>1,709</td><td>Systematization of the knowledge of each task</td><td></td></tr><tr><td>Responsibility for each task</td><td>1,5831</td><td>Responsibility for each task</td><td>Responsibility for each task</td></tr><tr><td rowspan="3">Work conditions</td><td>Modern and safe infrastructures</td><td>1,6281</td><td>Modern and safe infrastructures</td><td>Modern and safe infrastructures</td></tr><tr><td>Modern and cutting-edge technology</td><td>1,7764</td><td>Modern and cutting-edge technology</td><td></td></tr><tr><td>Healthy sanitary facilities</td><td>1,8527</td><td>Healthy sanitary facilities</td><td>Healthy sanitary facilities</td></tr><tr><td>Time paid in hours of</td><td></td><td>Safety at work</td><td>1,9463</td><td>Safety at work</td><td></td></tr></table>