The Impact of Zakat Compliance Among Taxpayers on Enhancing Institutional Performance: An Applied Study Using Structural Equation Modeling (SEM) at the General Authority for Zakat – Sanaa, Yemen

This study examined the causal impact of zakat compliance on the institutional performance of Yemen’s General Authority for Zakat. It employs a novel integrated theoretical framework that combines the Theory of Planned Behavior, Social Exchange Theory, and Organizational Legitimacy Theory-a comprehensive approach not previously applied in the context of zakat institutions with this level of comprehensiveness. A quantitative research design was adopted, and data were collected from 398 managerial staff members using a validated electronic questionnaire. The relationships among five dimensions of zakat compliancereligiosity, trust, awareness, zakat as a tax deduction, and the administrative and regulatory system-were examined using Partial Least Squares Structural Equation Modeling (PLS-SEM). The findings reveal that zakat compliance has a substantial effect on institutional performance, explaining 90.8% of its variance (R² = 0.908).

## I. INTRODUCTION

Zakat, the third pillar of Islam, is a religious obligation with profound social and economic significance. It serves as a mechanism for redistributing wealth and promoting social justice. The

Holy Qur'an commands: "Take from their wealth a charity by which you purify them and cause them to increase" (Surah Al-Tawbah, 103). This divine injunction underscores the dual role of Zakat in both personal purification and societal stability.

In Yemen, despite the deeply rooted religious values of society, official compliance with zakat remains relatively low due to administrative and legislative challenges, which have weakened public trust in governmental institutions.

To what extent does zakat compliance behaviour among obligated individuals contribute to improving the institutional performance of the General Authority for Zakat in Yemen?

## II. LITERATURE REVIEW AND HYPOTHESES DEVELOPMENT

### a) Institutional Performance

Institutional performance is a cornerstone of organisational effectiveness and a strategic imperative for achieving competitiveness in dynamic environments.

It reflects the efficiency and effectiveness with which an organisation utilises its resources to accomplish strategic objectives. In the context of globalisation, economic integration, and rapid technological change, improving institutional performance has become essential for long-term success and sustainability (Kaplan & Norton, 2010).

Modern perspectives on institutional performance extend beyond traditional economic outcomes to encompass qualitative dimensions such as customer satisfaction, innovation, and process improvement. The Balanced Scorecard framework identifies four key perspectives (Kaplan & Norton, 1996, 2001, 2004):

1. Economic Perspective - Evaluates the economic health of the organisation and the efficient use of resources.

2. Customer Perspective – Assesses client satisfaction and responsiveness to stakeholder needs.

3. Internal Processes Perspective - Focuses on operational efficiency, productivity, and quality improvement.

4. Learning and Growth Perspective - Emphasises continuous innovation and the development of human capital.

### b) Zakat Compliance

Zakat compliance refers to the extent to which Muslims fulfil their Zakat obligations under Islamic law and relevant state regulations. It reflects both religious commitment and recognition of Zakat as a divinely mandated duty that must be distributed fairly (Bin Khamis et al., 2011; Sawmar & Mohammed, 2021). Based on this understanding, the study proposes the primary hypothesis:

H1: Zakat compliance behaviour has a statistically significant effect on improving institutional performance at the General Authority of Zakat.

### c) Religiosity

Religiosity denotes the degree to which individuals adhere to religious values and practices, encompassing belief systems, worship, ethics, and daily conduct. According to the Theory of Planned Behavior, normative beliefs shape intentions through social and religious norms that influence payment behaviour (Ajzen, 1985, 1991). Empirical studies have shown that religiosity positively influences compliance with both Zakat and taxation systems (Al-Mamun & Haque, 2015; Bin-Nashwan et al., 2021; Mokhtar et al., 2018; Febriandika., 2023).

H1a: Religiosity has a statistically significant effect on improving institutional performance at the General Authority of Zakat.

### d) Trust

Trust represents confidence in the credibility and integrity of an institution, reflecting the belief that it operates ethically, transparently, and effectively (Beach, 2018). In Zakat administration, trust fosters voluntary compliance and strengthens the relationship between payers and institutions (Bin-Nashwan et al., 2021; Muhammad & Saad, 2016; Abioyea et al., 2013).

H1b: Trust has a statistically significant effect on improving institutional performance at the General Authority of Zakat.

### e) Awareness

Awareness involves understanding the rules, purposes, and social significance of Zakat. Public awareness campaigns, educational programs, and community engagement initiatives have been shown to increase compliance rates (Bonang et al., 2023; Haji-Othman et al., 2019; Ramlee et al., 2023).

H1c: Awareness has a statistically significant effect on improving institutional performance at the General Authority of Zakat.

### f) Zakat as a Tax Deduction

The concept of zakat as a tax deduction refers to the possibility of deducting the amount of zakat paid from a taxpayer's total tax obligations. This mechanism serves as a Economic incentive that reduces the tax burden on taxpayers and encourages them to comply by paying zakat through official institutions (Djatmiko, 2019). Several studies in Malaysia and Indonesia have demonstrated the effectiveness of zakat deduction as an Economic incentive in enhancing voluntary zakat compliance (Halim et al., 2025; Wijayanti et al., 2022). However, some studies suggest that the impact of Economic incentives may be limited in environments characterized by weak governance. Djatmiko (2019), for example, cautioned against the potential misuse of deduction systems in countries suffering from poor institutional oversight. Accordingly, this study proposes the following sub-hypothesis:

H1d: Zakat as a tax deduction has a statistically significant effect on improving institutional performance at the General Authority of Zakat.

### g) Administrative and Regulatory System

An efficient administrative and regulatory system ensures transparency, accountability, and proper governance. Elements such as internal controls, technology adoption, and capacity building are critical in promoting compliance and improving institutional performance (Drumaux & Joyce, 2017; Sofyani et al., 2022).

H1e: The administrative and regulatory system has a statistically significant effect on improving institutional performance at the General Authority of Zakat.

### h) Research Gap

A review of the existing literature indicates that numerous studies have examined various aspects of Zakat compliance behaviour. Nevertheless, to the best of the researcher's knowledge, there is a lack of empirical research that explicitly investigates how Zakat compliance contributes to enhancing the performance of Zakat institutions. This gap highlights the need for a more holistic approach that not only explores compliance as an individual act but also situates it within institutional outcomes.

To address this gap, the present study proposes a comprehensive framework that integrates religious, administrative, behavioural, and social dimensions to analyse the role of Zakat compliance in strengthening institutional performance. By focusing on the Yemeni context- characterised by unique economic, social, and regulatory challenges- the study seeks to capture the contextual dynamics that shape taxpayers' compliance behaviour.

Moreover, the study employs an advanced methodological approach, namely Partial Least Squares

Structural Equation Modelling (PLS-SEM), which enables a rigorous examination of the complex relationships among the study's constructs. This methodological choice enhances the validity of the findings. It ensures the generation of practical insights that can guide policymakers at the General Authority of Zakat in developing strategies to improve performance and accountability.

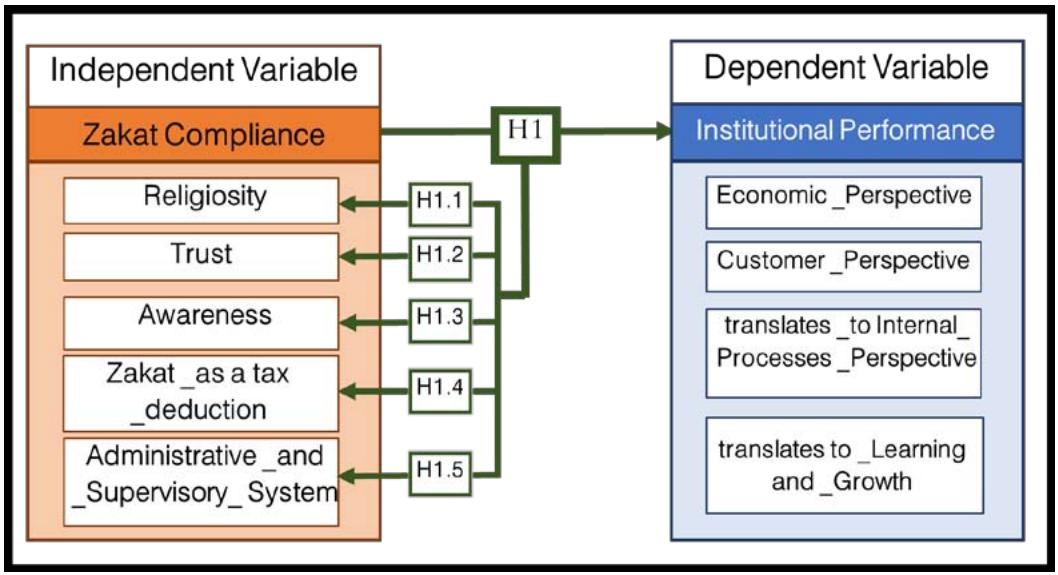

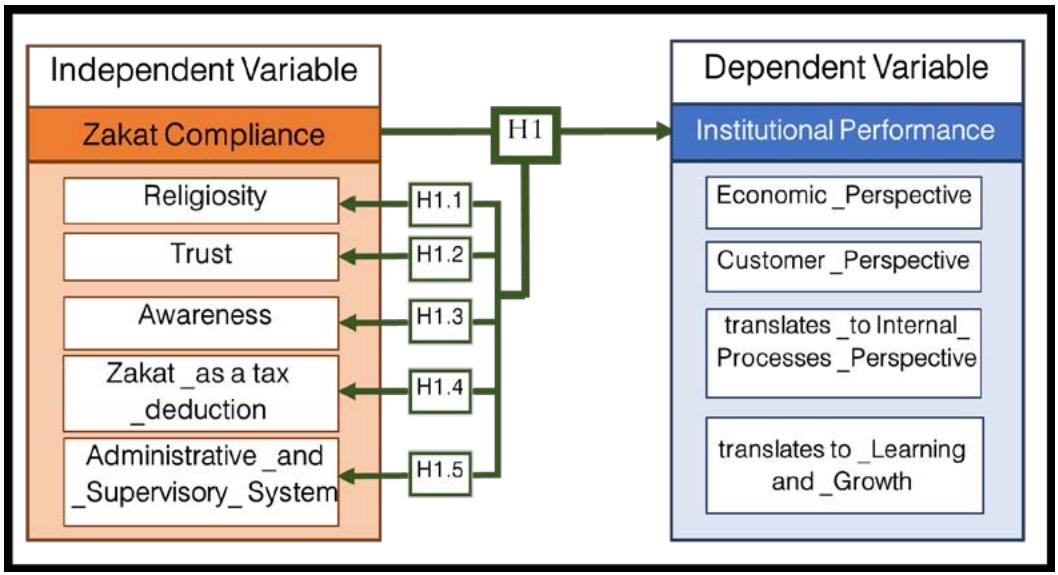

## III. CONCEPTUAL FRAMEWORK OF THE STUDY

The variables of the study are structured as illustrated in Figure 1 and are categorised as follows:

1. Independent Variable: Zakat Compliance and its dimensions: (Religiosity, Trust, Awareness, Zakat as a tax deduction, Administrative and Supervisory System).

2. Dependent Variable: Institutional Performance and its dimensions: (Economic Perspective, Customer Perspective, Internal processes dimension, Learning and growth dimension).

Figure 1: Conceptual Model

## IV. RESEARCH METHODS

This study adopted a quantitative research design to examine the impact of zakat compliance on institutional performance at the General Authority of Zakat in Yemen. Data were collected through a structured, closed-ended questionnaire based on a five-point Likert scale (1 = Strongly Disagree, 5 = Strongly Agree). The instrument was adapted from previously validated studies (Bonang et al., 2023; Haji-Othman et al., 2019; Ummulkhayr, 2018), with modifications to align with the Yemeni context.

### a) Population and Sampling

The study population consisted of 515 managerial employees at the headquarters of the

General Authority for Zakat and its Capital Secretariat branch in Sana'a. Leadership staff, including department heads and directors, were selected because they are most knowledgeable about both the Economic and operational dimensions of institutional performance, and play a central role in formulating and implementing zakat policies and strategies. This makes them highly representative of the study phenomenon. To ensure comprehensive coverage and minimize bias, questionnaires were distributed to the entire population (515), of which 417 were returned, and 398 were retained after data screening. This sample size is considered sufficient for Partial Least Squares Structural Equation Modeling (PLS-SEM), given the complexity of the research model (Hair et al., 2017).

Although purposive sampling is often criticized for potential bias, it is widely used in research conducted in fragile or conflict-affected contexts, where access to respondents is restricted (Etikan, Musa, & Alkassim, 2016). To further mitigate bias, the study targeted all available leadership staff within the specified locations.

### b) Instrument Validity and Reliability

The questionnaire measured five independent variable dimensions- religiosity, trust, awareness, zakat as a tax deduction, and administrative- regulatory systems- and four dependent variable- dimensions-economic perspective, customer perspective, internal processes perspective, and learning and growth perspective. Content validity was ensured through expert review by four academics in Islamic finance and public policy, followed by a pilot test with 45 participants to refine clarity and wording.

Reliability was confirmed using Cronbach's Alpha and Composite Reliability (CR), with all values exceeding the 0.70 threshold. Convergent validity was assessed using Average Variance Extracted (AVE), and discriminant validity was verified through the Fornell-Larcker criterion and Heterotrait-Monotrait Ratio (HTMT), consistent with established guidelines (Hair et al., 2019).

### c) Ethical Considerations

Ethical approval was granted by the Research Committee of the Yemeni Academy for Graduate Studies. Participants were informed of the study's purpose, assured confidentiality, and provided informed consent before completing the survey. No personal identifiers were collected, and the data were used solely for academic purposes.

### d) Data Analysis

Given the exploratory nature of the study and the model's complexity, Partial Least Squares Structural Equation Modeling (PLS-SEM) was chosen over covariance-based SEM. PLS-SEM is appropriate for moderate sample sizes and non-normal data distributions (Hair et al., 2017). Data analysis was conducted using SmartPLS 4 software following a two-step process:

1. Measurement Model Evaluation - testing internal consistency, convergent validity, and discriminant validity.

2. Structural Model Evaluation - assessing the coefficient of determination $(R^2)$, effect sizes $(f^2)$, predictive relevance $(Q^2)$, and hypothesis testing.

## V. RESULTS

### a) Descriptive Analysis Results of the Sample's Demographic Characteristics:

Table 1 and Figures 1-5 summarize the demographic characteristics of the respondents (N = 398), including age, educational level, job position, years of service, and entity.

In terms of age, the majority of respondents were between 30-40 years old (46%), followed by those below 30 years (28%), while 17% were between 40-50 years and 10% above 50 years. This indicates that the Authority relies on a relatively young workforce, which may enhance adaptability to modern administrative practices and digital compliance systems.

Regarding educational level, bachelor's degree holders represented the largest group (46%), followed by those with general secondary education (31%) and post-secondary diplomas (18%). Only 6% of the respondents held postgraduate qualifications (master's and doctorate). This distribution suggests that while the majority of staff have medium to higher education, additional training may be required to strengthen specialized knowledge of zakat and institutional governance.

With respect to job position, section heads formed the largest category (71%), followed by department managers (20%), while general managers and top leadership together accounted for only 9%. This highlights the study's emphasis on middle-level managerial staff, who serve as the operational link between strategic policies and implementation.

In terms of years of service, $33\%$ of the respondents had 5-10 years of experience, $26\%$ had less than 5 years, $21\%$ had 10-15 years, and $20\%$ had more than 15 years. This reflects a balanced mix of younger staff and experienced employees, which enriches perspectives on zakat compliance and institutional performance.

Finally, $64\%$ of respondents were from the headquarters of the General Authority for Zakat, while $36\%$ were from the Capital Secretariat branch, providing balanced representation of both central and branch-level administration.

Table 1: Demographic Characteristics of the Respondents

<table><tr><td>Variable</td><td>Category</td><td>Frequencies</td><td>Percentage</td></tr><tr><td rowspan="5">Age</td><td>Less than 30 years</td><td>110</td><td>28%</td></tr><tr><td>30-40 years</td><td>184</td><td>46%</td></tr><tr><td>40-50 years</td><td>66</td><td>17%</td></tr><tr><td>More than 50 years</td><td>38</td><td>10%</td></tr><tr><td>Total</td><td>398</td><td>100%</td></tr><tr><td rowspan="6">Educational Level</td><td>General Secondary</td><td>122</td><td>31%</td></tr><tr><td>Diploma after General</td><td>71</td><td>18%</td></tr><tr><td>Bachelor's</td><td>183</td><td>46%</td></tr><tr><td>Master's</td><td>16</td><td>4%</td></tr><tr><td>Doctorate</td><td>6</td><td>2%</td></tr><tr><td>Total</td><td>398</td><td>100%</td></tr><tr><td rowspan="5">Job Level</td><td>Authority Leadership</td><td>16</td><td>4%</td></tr><tr><td>General Managers</td><td>18</td><td>5%</td></tr><tr><td>Department Managers</td><td>81</td><td>20%</td></tr><tr><td>Section Heads</td><td>283</td><td>71%</td></tr><tr><td>Total</td><td>398</td><td>100%</td></tr><tr><td rowspan="5">Years of Service</td><td>Less than 5 years</td><td>105</td><td>26%</td></tr><tr><td>5-10 years</td><td>130</td><td>33%</td></tr><tr><td>10-15 years</td><td>82</td><td>21%</td></tr><tr><td>More than 15 years</td><td>81</td><td>20%</td></tr><tr><td>Total</td><td>398</td><td>100%</td></tr><tr><td rowspan="3">Entity</td><td>The General Zakat Authority</td><td>256</td><td>64%</td></tr><tr><td>Capital Secretariat Branch</td><td>142</td><td>36%</td></tr><tr><td>Total</td><td>398</td><td>100%</td></tr></table>

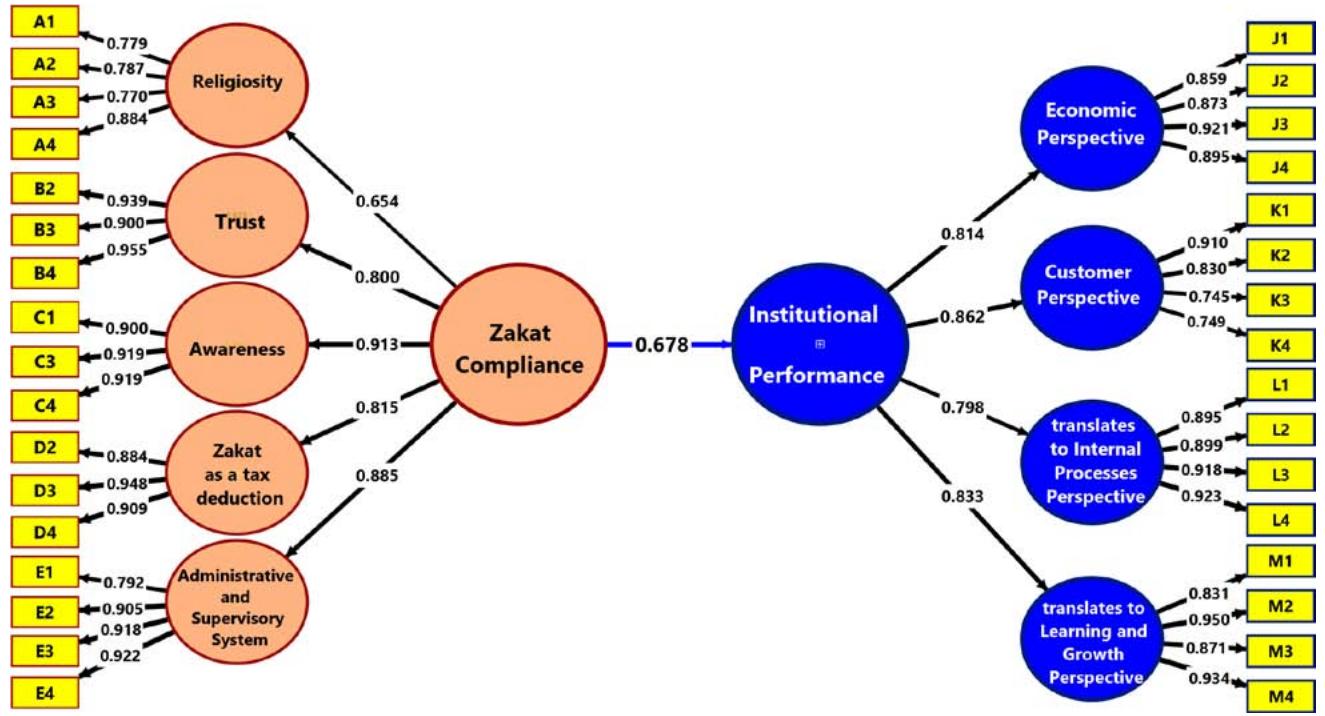

### b) Measurement Model Evaluation

The measurement model was assessed to ensure reliability and validity before testing the structural model. This evaluation included four key criteria:

construct validity, internal consistency reliability, convergent validity, and discriminant validity, as illustrated in Figure 2 and Table 2.

Figure 2: Measurement Model

1. Construct Validity: All item loadings exceeded the recommended threshold of 0.70, indicating that each indicator reliably measures its intended construct and thus confirming strong construct validity (Hair et al., 2019).

2. Internal Consistency Reliability: Cronbach's Alpha $(\alpha)$ and Composite Reliability (CR) were used to assess internal consistency. All constructs reported $\alpha$ and CR values above the 0.70 benchmark, demonstrating satisfactory reliability of the scales (Hair et al., 2019).

3. Convergent Validity: assessed through the Average Variance Extracted (AVE), showed that all constructs exceeded the recommended threshold of 0.50, confirming that the indicators adequately represent their respective constructs (Chin, 1998; Hair et al., 2019). Table 2 presents the results for factor loadings, Cronbach's Alpha, CR, and AVE.

Table 2: Internal Consistency, Composite Reliability, and Convergent Validity

<table><tr><td>Latent Variable</td><td>Question</td><td>Factor Loading</td><td>Cronbach's Alpha (α)</td><td>CR</td><td>AVE</td></tr><tr><td rowspan="4">Religiosity</td><td>A1</td><td>0.779</td><td rowspan="4">0.819</td><td rowspan="4">0.820</td><td rowspan="4">0.650</td></tr><tr><td>A2</td><td>0.787</td></tr><tr><td>A3</td><td>0.770</td></tr><tr><td>A4</td><td>0.884</td></tr><tr><td rowspan="3">Trust</td><td>B2</td><td>0.939</td><td rowspan="3">0.923</td><td rowspan="3">0.924</td><td rowspan="3">0.867</td></tr><tr><td>B3</td><td>0.900</td></tr><tr><td>B4</td><td>0.955</td></tr><tr><td rowspan="3">Awareness</td><td>C1</td><td>0.900</td><td rowspan="3">0.900</td><td rowspan="3">0.901</td><td rowspan="3">0.833</td></tr><tr><td>C3</td><td>0.919</td></tr><tr><td>C4</td><td>0.919</td></tr><tr><td rowspan="3">Zakat_as a tax_deduction</td><td>D2</td><td>0.884</td><td rowspan="3">0.902</td><td rowspan="3">0902</td><td rowspan="3">0.836</td></tr><tr><td>D3</td><td>0.948</td></tr><tr><td>D4</td><td>0.909</td></tr><tr><td rowspan="4">Administrative_and_Supervisory_System</td><td>E1</td><td>0.792</td><td rowspan="4">0.907</td><td rowspan="4">0.917</td><td rowspan="4">0.785</td></tr><tr><td>E2</td><td>0.905</td></tr><tr><td>E3</td><td>0.918</td></tr><tr><td>E4</td><td>0.922</td></tr><tr><td rowspan="4">Economic_Perspective</td><td>J1</td><td>0.859</td><td rowspan="4">0.910</td><td rowspan="4">0918</td><td rowspan="4">0.787</td></tr><tr><td>J2</td><td>0.873</td></tr><tr><td>J3</td><td>0.921</td></tr><tr><td>J4</td><td>0.895</td></tr><tr><td rowspan="4">Customer_Perspective</td><td>K1</td><td>0.910</td><td rowspan="4">0.824</td><td rowspan="4">0834</td><td rowspan="4">0.658</td></tr><tr><td>K2</td><td>0.830</td></tr><tr><td>K3</td><td>0.745</td></tr><tr><td>K4</td><td>0.749</td></tr><tr><td rowspan="4">translates_to/Internal_Processes_Perspective</td><td>L1</td><td>0.895</td><td rowspan="4">0.930</td><td rowspan="4">0930</td><td rowspan="4">0.826</td></tr><tr><td>L2</td><td>0.899</td></tr><tr><td>L3</td><td>0.918</td></tr><tr><td>L4</td><td>0.923</td></tr><tr><td rowspan="4">translates_to_Learning_and_Growth_Perspective</td><td>M1</td><td>0.831</td><td rowspan="4">0.919</td><td rowspan="4">920</td><td rowspan="4">0.806</td></tr><tr><td>M2</td><td>0.950</td></tr><tr><td>M3</td><td>0.871</td></tr><tr><td>M4</td><td>0.934</td></tr></table>

#### 4. Discriminant Validity: Discriminant validity was examined using two complementary approaches:

Fornell-Larcker Criterion: The square root of the AVE for each construct was greater than its highest correlation with any other construct, meeting the criterion suggested by (Fornell & Larcker, 1981). Table 3 presents the Fornell-Larcker matrix.

Table 3: Discriminant Validity - Fornell-Larcker Criterion

<table><tr><td>Variable (Structure) - Fornell-Larcker</td><td>ASS</td><td>A</td><td>CP</td><td>FP</td><td>R</td><td>T</td><td>ZD</td><td>TIPP</td><td>TLGP</td></tr><tr><td>Administrative and Supervisory System</td><td>0.886</td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td></tr><tr><td>Awareness</td><td>0.805</td><td>0.913</td><td></td><td></td><td></td><td></td><td></td><td></td><td></td></tr><tr><td>Customer Perspective</td><td>0.633</td><td>0.61</td><td>0.811</td><td></td><td></td><td></td><td></td><td></td><td></td></tr><tr><td>Economic Perspective</td><td>0.486</td><td>0.338</td><td>0.681</td><td>0.887</td><td></td><td></td><td></td><td></td><td></td></tr><tr><td>Religiosity</td><td>0.608</td><td>0.663</td><td>0.441</td><td>0.312</td><td>0.806</td><td></td><td></td><td></td><td></td></tr><tr><td>Trust</td><td>0.77</td><td>0.716</td><td>0.515</td><td>0.367</td><td>0.654</td><td>0.931</td><td></td><td></td><td></td></tr><tr><td>Zakat as a tax deduction</td><td>0.726</td><td>0.765</td><td>0.602</td><td>0.443</td><td>0.553</td><td>0.535</td><td>0.914</td><td></td><td></td></tr><tr><td>translates to Internal Processes</td><td>0.661</td><td>0.679</td><td>0.748</td><td>0.516</td><td>0.568</td><td>0.599</td><td>0.605</td><td>0.909</td><td></td></tr><tr><td>translates to Learning and Growth Perspective</td><td>0.616</td><td>0.561</td><td>0.701</td><td>0.661</td><td>0.398</td><td>0.500</td><td>0.587</td><td>0.633</td><td>0.898</td></tr></table>

HTMT Ratio: All HTML values were below the conservative threshold of 0.85, confirming discriminant validity among the constructs (Henseler, Ringle, & Sarstedt, 2015). Table 4 summarizes the HTMT results.

Table 4: Discriminant validity, HTMT

<table><tr><td>Variable (Structure) - HTMT</td><td>ASS</td><td>A</td><td>CP</td><td>FP</td><td>R</td><td>T</td><td>ZD</td><td>TIPP</td><td>TLGP</td></tr><tr><td>Administrative_and_Supervisory_System</td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td></tr><tr><td>Awareness</td><td>0.853</td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td></tr><tr><td>Customer_Perspective</td><td>0.729</td><td>0.709</td><td></td><td></td><td></td><td></td><td></td><td></td><td></td></tr><tr><td>Economic_Perspective</td><td>0.518</td><td>0.359</td><td>0.777</td><td></td><td></td><td></td><td></td><td></td><td></td></tr><tr><td>Religiosity</td><td>0.704</td><td>0.772</td><td>0.538</td><td>0.350</td><td></td><td></td><td></td><td></td><td></td></tr><tr><td>Trust</td><td>0.845</td><td>0.785</td><td>0.592</td><td>0.388</td><td>0.749</td><td></td><td></td><td></td><td></td></tr><tr><td>Zakat_as a tax_deduction</td><td>0.796</td><td>0.850</td><td>0.699</td><td>0.476</td><td>0.640</td><td>0.585</td><td></td><td></td><td></td></tr><tr><td>translates_to/Internal_Processes_Perspective</td><td>0.72</td><td>0.742</td><td>0.856</td><td>0.545</td><td>0.650</td><td>0.646</td><td>0.658</td><td></td><td></td></tr><tr><td>translates_to_Learning and_Growth_Perspective</td><td>0.671</td><td>0.618</td><td>0.808</td><td>0.721</td><td>0.456</td><td>0.542</td><td>0.644</td><td>0.686</td><td></td></tr></table>

These results confirm that the measurement instruments used in the study are valid and reliable for accurately representing the latent variables.

using multiple criteria including the coefficient of determination $(\mathsf{R}^2)$, effect size $(\mathrm{f}^2)$, predictive relevance $(\mathbf{Q}^2)$, and model fit indices.

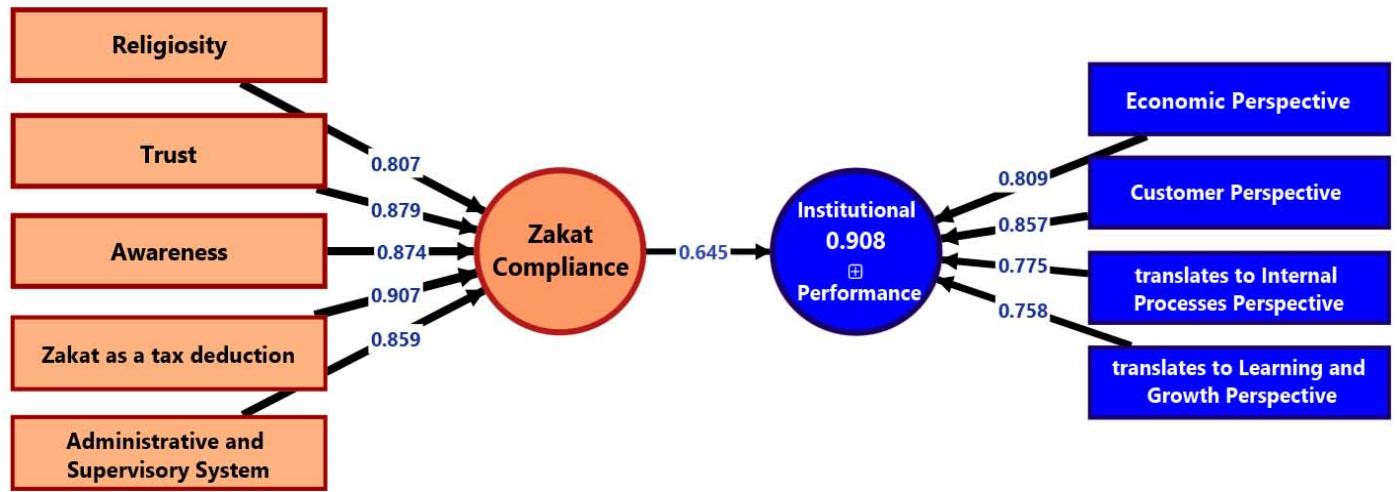

### c) Structural Model Evaluation

The structural model was assessed following the guidelines of Hair et al. (2019) and Cohen (1988),

Figure 3: Model Evaluation

The results revealed a strong explanatory power, with an $R^2$ value of 0.85 for institutional performance, indicating that the five independent constructs (religiosity, administrative system, trust, awareness, and economic incentives) collectively explained $85\%$ of the variance in institutional performance. According to Hair et al. (2019), an $R^2$ above 0.75 is considered substantial, which underscores the robustness of the model.

Regarding predictive relevance, the $Q^2$ value was 0.645, which exceeds the threshold of 0.50, thereby reflecting large predictive relevance based on Cohen's (1988) and Chin's (1998) guidelines. This suggests that the model not only explains the data well but also has strong predictive accuracy.

In terms of effect size $(\mathrm{f}^2)$, the analysis showed that religiosity and the administrative system had large effect sizes on institutional performance, while trust, awareness, and Economic incentives had moderate effects. Following Cohen's (1988) benchmarks $(0.02 =$ small, $0.15 =$ medium, $0.35 =$ large), these results highlight the relative importance of religious and administrative factors in shaping institutional outcomes.

Finally, the model fit was assessed using the Standardized Root Mean Square Residual (SRMR). The SRMR value of 0.073 falls below the conservative cut-off of 0.08 suggested by Hu and Bentler (1999), indicating an acceptable model fit.

Taken together, these findings demonstrate that the structural model is statistically sound, theoretically meaningful, and practically relevant for explaining and predicting institutional performance within zakat institutions.

## VI. HYPOTHESIS TESTING

### a) Testing the Main Hypothesis

The main hypothesis proposed that zakat compliance has a statistically significant effect on improving institutional performance in the General Authority of Zakat.

Table 5: Shows the Path Coefficients of the Main Hypothesis

<table><tr><td>N</td><td>Hypothesis</td><td>Q2</td><td>f2</td><td>R2</td><td>β</td><td>Standard Deviation</td><td>T statistics</td><td>P -Value</td><td>Result</td></tr><tr><td>H1</td><td>Zakat_Compliance -> Institutional _Performance</td><td>0.905</td><td>0.850</td><td>0.908</td><td>0.678</td><td>0.029</td><td>23.147</td><td>0</td><td>Accepted</td></tr></table>

As shown in Figure 3 and Table 6, the structural model strongly supports this hypothesis. The analysis revealed a statistically significant and practically meaningful standardized path coefficient $(\beta = 0.678, p < 0.001)$, with a t-value of 23.147—well above the critical threshold of 1.96. The effect size was large $(f^2 = 0.850)$ according to Cohen's (1992) guidelines, while the explanatory power demonstrated high predictive validity $(R^2 = 0.908)$, accounting for $90.8\%$ of the variance in institutional performance. All factor loadings exceeded the recommended threshold of 0.70, confirming convergent validity.

Beyond these statistical indicators, the findings carry important theoretical implications. From the perspective of the Theory of Planned Behavior (Ajzen, 1991), the results confirm that zakat compliance intentions, grounded in religiosity and internalized social norms, are translated into tangible institutional outcomes. Similarly, Social Exchange Theory (Blau, 2017) explains that taxpayers' compliance, when motivated by trust and perceptions of fairness, produces reciprocal benefits in the form of improved institutional efficiency. In addition, consistent with Organizational Legitimacy Theory (Suchman, 1995), fulfilling zakat obligations enhances the perceived legitimacy of the institution, thereby strengthening its overall performance and social acceptance.

These results align with prior studies conducted in other Islamic contexts (e.g., Muhammad & Saad, 2016; Bin-Nashwan et al., 2021; Ramlee et al., 2023), which reported a positive impact of zakat compliance on institutional governance and performance. However, the Yemeni case reveals a much stronger explanatory power $(R^2 = 0.908)$ compared to similar studies, suggesting that in fragile governance settings, compliance with zakat obligations may play an even more decisive role in sustaining institutional legitimacy and effectiveness. This novel contribution indicates that zakat is not only a religious duty but also an administrative mechanism capable of reinforcing Economic justice and institutional resilience.

Despite these strong results, caution is warranted. The high explanatory power may partly reflect contextual dynamics specific to Yemen, such as weak alternative fiscal institutions, socio-religious sensitivities, and limited trust in tax authorities. Therefore, while zakat compliance emerges as a pivotal driver of institutional performance in this context, the generalizability of the findings to more stable governance environments may be limited.

Practically, this underscores the importance of policies that integrate religious motivation, trust-building strategies, awareness campaigns, and fiscal incentives such as zakat-tax deductions. However, these initiatives should be accompanied by structural reforms to ensure transparency, accountability, and long-term institutional legitimacy. In other words, zakat compliance should be seen as a catalyst rather than a substitute for broader governance reforms.

Finally, the robust psychometric properties of the "economic perspective" and "trust" constructs further validate their central role, yet they also highlight the need for future research to explore additional mediators and moderators- such as governance quality or digitalization of zakat systems- that may shape the compliance-performance nexus in different contexts.

### b) Testing Sub-Hypotheses

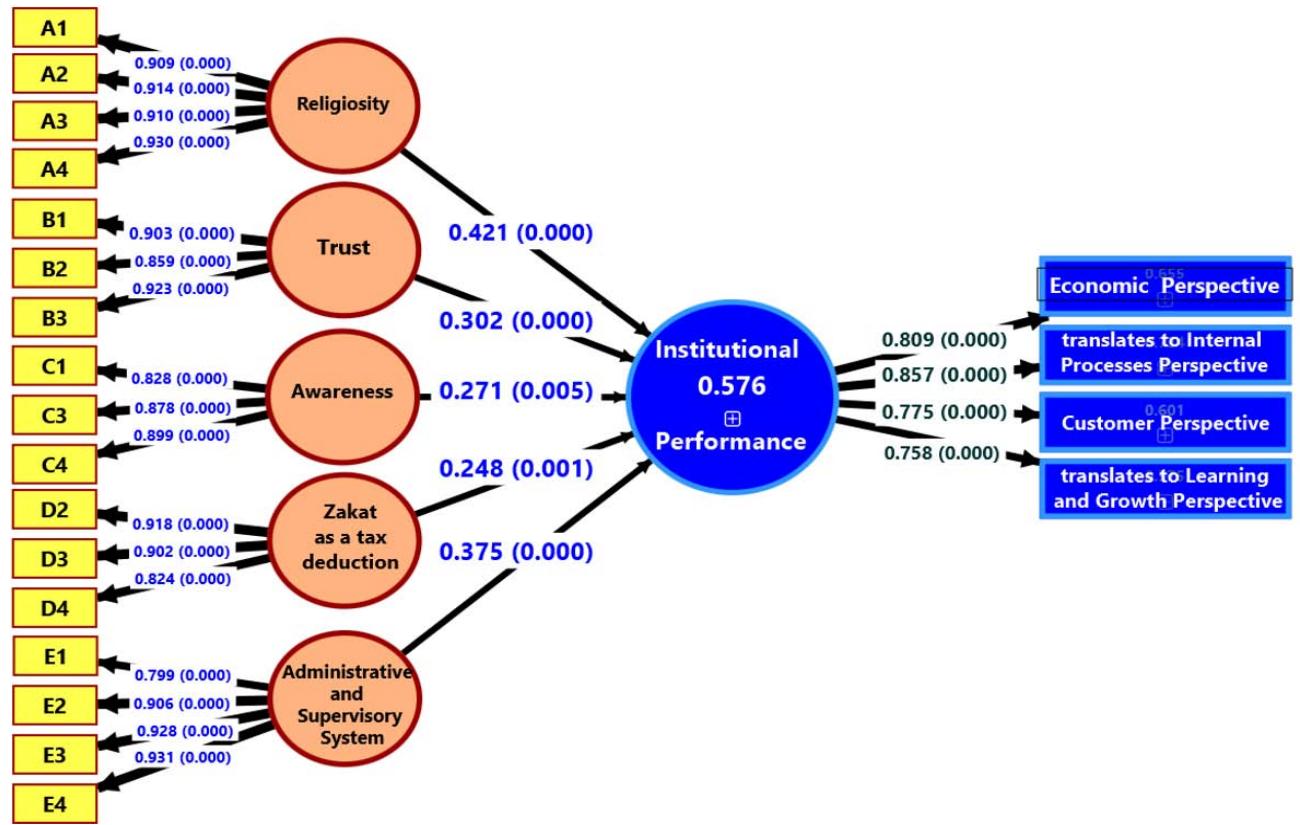

The main hypothesis branches into five subhypotheses, as illustrated in Figure 4 and Table 5, as follows:

Figure 4: Path analysis of sub-hypotheses from a to e

Table No. 6: Path analysis of sub-hypotheses from a to e

<table><tr><td>N</td><td>Hypothesis</td><td>β</td><td>S. D</td><td>T</td><td>P. V</td><td>f2</td><td>Result</td></tr><tr><td>H1a:</td><td>Religiosity -> Institutional _ Performance</td><td>0.421</td><td>0.081</td><td>5.212</td><td>0</td><td>0.749</td><td>Accepted</td></tr><tr><td>H1b:</td><td>Trust -> Institutional _ Performance</td><td>0.302</td><td>0.068</td><td>4.467</td><td>0</td><td>1.780</td><td>Accepted</td></tr><tr><td>H1c:</td><td>Awareness -> Institutional _ Performance</td><td>0.271</td><td>0.094</td><td>2.894</td><td>0</td><td>5.017</td><td>Accepted</td></tr><tr><td>H1d:</td><td>Zakat as a tax deduction -> Institutional _ Performance</td><td>0.248</td><td>0.07</td><td>3.535</td><td>0</td><td>1.978</td><td>Accepted</td></tr><tr><td>H1e:</td><td>Administrative and Supervisory System -> Institutional _ Performance</td><td>0.375</td><td>0.101</td><td>3.703</td><td>0</td><td>3.629</td><td>Accepted</td></tr></table>

#### 1. Sub-Hypothesis H1a: Religiosity → Institutional Performance

The results confirmed a statistically significant positive effect of religiosity on institutional performance $(\beta = 0.421, p < 0.001)$. This finding aligns with Bin-Nashwan et al. (2021) and Mokhtar et al. (2018), who emphasized the role of religious commitment in promoting Zakat compliance. However, the stronger effect in Yemen- compared to Southeast Asian contexts highlights the dominance of religious norms in shaping behavior in conservative societies. This supports Karakas (2010), who argued that religiosity's impact

varies across cultural settings. Practically, this underscores the need for faith-based outreach programs in Yemen to sustain institutional performance.

#### 2. Sub-Hypothesis H1b: Trust → Institutional Performance

- Trust showed a moderate yet significant effect $(\beta = 0.302, p < 0.001)$, consistent with Muhammad & Saad (2016). However, the weaker effect relative to religiosity contrasts with studies conducted in stable environments (e.g., Bin-Nashwan et al., 2021). This discrepancy is attributed to Yemen's institutional fragility and widespread distrust in public entities, as noted by Beach (2018). To enhance trust, transparency reforms and anti-corruption measures are critical.

3. Sub-Hypothesis H1c: Awareness → Institutional Performance

Awareness had a positive but limited effect ( $\beta = 0.271$, $p < 0.001$ ), aligning with Ramlee et al. (2023). However, its lower impact in Yemen reflects challenges such as Economic illiteracy and limited access to education, as highlighted by Bonang et al. (2023). Tailored awareness campaigns using simplified language and community-based outreach are recommended to address contextual barriers.

#### 4. Sub-Hypothesis H1d: Zakat as a Tax Deduction → Institutional Performance

The tax deduction mechanism showed the weakest effect ( $\beta = 0.248$, $p < 0.001$ ), contradicting (Mohd Ali et al., 2021; Hasan & Abdullah, 2019; Wijayanti et al., 2022) but supporting Djatmiko (2019)'s caution about Economic incentives in fragile states. In Yemen, religious motivations overshadow economic benefits, and systemic issues like tax evasion further limit its efficacy. Integrating tax incentives with religious appeals, rather than relying solely on monetary benefits, is advised.

#### 5. Sub-Hypothesis H1e: Administrative & Supervisory System $\rightarrow$ Institutional Performance

The administrative system demonstrated a strong effect ( $\beta = 0.375$, $p < 0.001$ ), consistent with (Abdelsalam et al., 2020; COSO, 2013; Hamid et al., 2021; Sofyani et al., 2022).

Its heightened importance in Yemen underscores the role of governance in contexts where institutional weaknesses amplify the impact of reforms. Digitalization of Zakat management and strengthened oversight mechanisms are urgently needed.

## VII. DISCUSSION OF RESULTS

The results revealed that Zakat compliance explains $90.8\%$ of the variance in institutional performance $(R^2 = 0.908)$. This exceptionally high explanatory power underscores the paramount importance of fulfilling Zakat obligations as a primary driver for enhancing Economic efficiency, transparency, and the achievement of strategic objectives within the Yemeni context. While this value indicates a very strong model fit, it also raises a common concern in social science research regarding potential overfitting. To mitigate this, the study followed rigorous methodological protocols, including the use of a large sample size relative to the model complexity and robust validation techniques like bootstrapping. The high $R^2$ is also interpreted as a reflection of the model's comprehensiveness in capturing the core determinants of performance in a setting where traditional economic factors may be overshadowed by religious and institutional drivers.

The effect sizes $(\mathrm{f}^2)$ were examined to determine the relative contribution of each construct, following Cohen's (1992) guidelines:

1. Religiosity was the strongest influential variable ( $\beta = 0.421$, $f^2 = 0.18$, medium effect). This confirms the central role of religious values in motivating institutional commitment, which is consistent with the findings of Dyreng et al. (2012) and Karakas (2010). In the Yemeni context, this dominant effect highlights how deeply ingrained religious norms serve as the most reliable motivator for compliance, potentially compensating for weaknesses in other institutional areas.

2. The administrative and regulatory system ranked second ( $\beta = 0.375$, $f^2 = 0.15$, medium effect). This reinforces the findings of Abdelsalam et al. (2020) and COSO (2013), which linked internal control efficiency to improved performance. For Yemen, this strong result suggests that even incremental improvements in governance and administrative processes can yield significant gains in institutional performance, likely because the baseline is currently low.

3. Trust showed a moderate effect ( $\beta = 0.302$, $f^2 = 0.10$, small-to-medium effect). This aligns with Zak and Knack (2001), who noted that institutional trust enhances voluntary compliance. However, its relative ranking- below religiosity and administrative systems- is telling for Yemen. It reflects the challenging environment of eroded public trust, indicating that rebuilding credibility is a necessary but longer-term endeavor that must be supported by tangible improvements in religiosity and administration.

4. Awareness had a positive but smaller effect ( $\beta = 0.271$, $f^2 = 0.08$, small effect). This supports the results of Ramlee et al. (2023) and Abdullah and Ismail (2020). Its modest impact in the Yemeni context may be attributed to high levels of intrinsic religious awareness, suggesting that while educational campaigns are beneficial, they may be less impactful than direct improvements in religious engagement or system efficiency.

5. Zakat as a tax deduction showed the smallest effect $(\beta = 0.248, f^2 = 0.06, \text{small effect})$. This suggests that Economic incentives alone are relatively weak levers for improving performance. This finding is particularly crucial for Yemen and supports the cautions of scholars like Djatmiko (2019); it implies that in complex, fragile states, extrinsic motivators are less effective than intrinsic religious values or systemic reforms.

These results affirm that enhancing institutional performance requires a multi-dimensional strategy. The high explanatory power of the model demonstrates that in contexts like Yemen, addressing the core pillars of religiosity, administration, and trust is not just beneficial but essential. Policymakers should prioritize:

1. Leveraging religious capital through faith-based initiatives.

2. Investing in administrative reforms to build transparent and efficient systems.

3. Launching targeted awareness campaigns that complement, rather than lead, these efforts.

4. Implementing Economic incentives only as part of a broader package of governance improvements, not as a standalone solution

## VIII. CONCLUSION AND RECOMMENDATIONS

### a) Theoretical and Practical Contributions

This study provides significant theoretical contributions by developing and validating an integrated framework that combines the Theory of Planned Behavior, Social Exchange Theory, and Organizational Legitimacy Theory to analyze Zakat compliance behavior- a novel approach in the context of Zakat institutions. Practically, it identifies context-specific determinants of institutional performance in a fragile state, offering actionable insights for policymakers in Yemen and similar environments.

### b) Contextualized Recommendations for the General Authority for Zakat

To enhance institutional performance, the following strategies are proposed, prioritized based on feasibility and impact:

## i. Short-term (0-12 months)

1. Strengthen Transparency: Publish quarterly Economic reports audited by independent bodies to rebuild public trust.

2. Religiosity-Driven Awareness: Collaborate with religious leaders to launch campaigns emphasizing the spiritual and social benefits of Zakat compliance.

3. Simplify Compliance Procedures: Streamline administrative processes to reduce bureaucratic hurdles for taxpayers. ii. Medium-term (1-3 years)

1. Digital Transformation: Develop a user-friendly digital platform for Zakat calculation, payment, and tracking to improve accessibility and efficiency.

2. Capacity Building: Train staff on modern Economic management tools and ethical governance practices.

3. Stakeholder Engagement: Establish forums for regular dialogue with taxpayers to address concerns and align policies with community needs. iii. Long-term (3+ years)

1. Technology Integration: Explore blockchain-based solutions for transparent fund tracking and disbursement, contingent on stabilized infrastructure and funding.

2. Policy Reform: Advocate for legal reforms to harmonize Zakat and tax policies, ensuring incentives are aligned with Islamic principles.

3. Regional Collaboration: Partner with international Islamic Economic institutions to adopt best practices and secure technical support.

## IX. LIMITATIONS AND FUTURE RESEARCH

### a) This Study has Several Limitations

1. Sampling Constraints: The use of a non-probability sampling technique (purposive sampling) limited to managerial staff in Sana'a may affect the generalizability of the findings to other regions or demographic groups.

2. Contextual Challenges: The ongoing political and economic instability in Yemen may have influenced respondents' behavior and perceptions, introducing potential biases.

3. Methodological Boundaries: While PLS-SEM is robust for predictive analysis, qualitative insights (e.g., interviews) could provide deeper contextual understanding.

b) Future Research Directions To address these limitations and extend this work, future studies should:

1. Expand the sampling framework to include Zakat payers from the private sector and diverse geographic regions within Yemen.

2. Incorporate comparative studies with Zakat institutions in stable Muslim-majority countries (e.g., Malaysia, Indonesia) to identify transferable strategies.

3. Investigate the moderating role of macroeconomic factors (e.g., poverty, inflation) on Zakat compliance behavior.

4. Employ mixed-methods approaches to explore nuanced cultural and institutional barriers to compliance.

Generating HTML Viewer...

References

42 Cites in Article

O Abdelsalam,A Al-Hadi,K Al-Yahyaee,M Elnahass (2020). Governance mechanisms and performance in Zakat institutions.

M Abdullah,A Ismail (2020). Zakat awareness impact on institutional efficiency.

M Abioyea,-O Mohamad,M,-S Adnan,M.-A (2013). Antecedents of Zakat payers' trust in an emerging Zakat sector: an exploratory study.

I Ajzen (1985). From intentions to actions: A theory of planned behaviour.

I Ajzen (1991). The theory of planned behaviour.

A Al-Mamun,A Haque (2015). Tax deduction through Zakat: an empirical investigation on Muslims in Malaysia.

S Beach (2018). Institutional trust and governance.

M Bin Khamis,A Salleh,A Nawi (2011). Compliance behaviour of business Zakat payment in Malaysia: a theoretical economic exposition.

S Bin-Nashwan,H Abdul-Jabbar,S Aziz (2021). Does trust in the Zakat institution enhance entrepreneurs' Zakat compliance?.

Peter Blau (2017). Exchange and Power in Social Life.

Dahlia Bonang,Tika Widiastuti,Hanifiyah Yuliatul Hijriah,Shafinar Ismail (2023). DETERMINANTS OF ZAKAT COMPLIANCE BEHAVIOR IN URBAN MUSLIM ENTREPRENEURS IN MATARAM CITY WEST NUSA TENGGARA.

W Chin (1998). The partial least squares approach to structural equation modelling.

Jacob Cohen (1992). A power primer..

Coso (2013). Internal control -Integrated framework.

H Djatmiko (2019). Reformulation Zakat system as a tax reduction in Indonesia.

Anne Drumaux,Paul Joyce (2017). Public Governance in Member States.

S Dyreng,W Mayew,C Williams (2012). Religious social norms and corporate economic reporting.

Ilker Etikan,S Musa,R Alkassim (2016). Comparison of Convenience Sampling and Purposive Sampling.

Nur Febriandika,Dilla Kusuma,Yayuli Yayuli (2023). Zakat compliance behavior in formal zakat institutions: An integration model of religiosity, trust, credibility, and accountability.

C Fornell,D Larcker (1981). Evaluating structural equation models with unobservable variables and measurement error.

Joseph Hair,G Hult,Christian Ringle,Marko Sarstedt,Kai Thiele (2017). Mirror, mirror on the wall: a comparative evaluation of composite-based structural equation modeling methods.

Joseph Hair,Jeffrey Risher,Marko Sarstedt,Christian Ringle (2019). When to use and how to report the results of PLS-SEM.

Yusuf Haji-Othman,Mohd Yusuff,Wan Mohamed Fisol (2019). Developing a Theoretical Framework for Compliance Behavior of Income Zakat.

S Halim,M,A Suhada,J Jalil,N Anasrul,A (2025). Implementation of Zakat as a Tax Incentive in Indonesia: A Comparative Analysis.

M Hamid (2021). Internal control systems in Islamic charities.

Z Hasan,M Abdullah (2019). Zakat as tax incentive: Measuring organisational outcomes in Indonesian Islamic banks.

J Henseler,C Ringle,M Sarstedt (2015). A new criterion for assessing discriminant validity in variance-based structural equation modelling.

(2022). Zakat and tax policy reforms in OIC member countries.

R Kaplan,D Norton (1996). The balanced scorecard: translating strategy into action.

R Kaplan,D Norton (2001). The Balanced Scorecard: You Can't Manage What You Can't Measure.

R Kaplan,D Norton (2004). Strategy maps: Converting intangible assets into tangible outcomes.

Robert Kaplan,David Norton,Shahid Ansari (2010). The Execution Premium: Linking Strategy to Operations for Competitive Advantage.

Fahri Karakas (2010). Spirituality and Performance in Organizations: A Literature Review.

Mohd Ali,N Abdul Rahman,R Othman,R (2021). The impact of Zakat tax deduction on corporate performance: Evidence from Malaysia.

S Muhammad,R Saad (2016). Determinants of trust on Zakat institutions and its dimensions on intention to pay Zakat: A pilot study.

S Ramlee,H Gazali,T Amboala (2023). Factors Influencing the Intention to Pay Zakat Online.

Abdulsalam Sawmar,Mustafa Mohammed (2021). Enhancing zakat compliance through good governance: a conceptual framework.

Hafiez Sofyani,Haslida Abu Hasan,Zakiah Saleh (2022). Internal control implementation in higher education institutions: determinants, obstacles and contributions toward governance practices and fraud mitigation.

M Suchman (1995). Managing legitimacy: Strategic and institutional approaches.

Jade Dawson,Cik Hibadullah,Munya Ba Matraf,Nor Harun,Nor Hashim,Rohaya Dahari (2018). Jungle Math: An Educational Mobile Games for Preschoolers Learning Mathematics.

P Wijayanti,F Amilahaq,O Muthaher,N Baharuddin,N Sallem (2022). Modelling Zakat as a tax deduction: A comparison study in Indonesia and Malaysia.

No ethics committee approval was required for this article type.

Data Availability

Not applicable for this article.

How to Cite This Article

Dr. Ali Nasser Yahya Al-Ahnomi. 2026. \u201cThe Impact of Zakat Compliance Among Taxpayers on Enhancing Institutional Performance: An Applied Study Using Structural Equation Modeling (SEM) at the General Authority for Zakat – Sanaa, Yemen\u201d. Global Journal of Management and Business Research - A: Administration & Management GJMBR A Volume 25 (GJMBR Volume 25 Issue A5).

Explore published articles in an immersive Augmented Reality environment. Our platform converts research papers into interactive 3D books, allowing readers to view and interact with content using AR and VR compatible devices.

Your published article is automatically converted into a realistic 3D book. Flip through pages and read research papers in a more engaging and interactive format.

Our website is actively being updated, and changes may occur frequently. Please clear your browser cache if needed. For feedback or error reporting, please email [email protected]

Thank you for connecting with us. We will respond to you shortly.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.

The Impact of Zakat Compliance Among Taxpayers on Enhancing Institutional Performance: An Applied Study Using Structural Equation Modeling (SEM) at the General Authority for Zakat – Sanaa, Yemen