Mobile payment refers to a payment method by which a consumer pays a bill for goods or services through a mobile terminal. mobile payment users can send payment instructions directly or indirectly to a bank via mobile devices, thereby enabling currency payments and funds transfers. It realizes the integration of terminal equipment, Internet, application providers and financial institutions, and completes financial business such as currency payment. However, the adoption rates of this payment method is relative low in Malaysia. This research aims to identify and explore key factors that affect the decision of whether to use mobile payments. Four wellestablished theories, Theory of Rational Action (TRA), Technology Acceptance Model (TAM), Unified Theory of Acceptance and Use of Technology (UTAUT), Compass Acceptance Model for the analysis and evaluation of mobile service (CAM) are applied to investigate user acceptance of mobile payments.

## I. INTRODUCTION

In recent two decades, the prevalence of e-commerce has greatly changed the way people trade and live. While in the past fifteen years, the progress of mobile technology has brought new development to electronic commerce. In the mobile Internet environment, the development of e-commerce starts to get rid of the limitation of time and space, and payment as an integral part of e-commerce, also shifts from traditional cash or credit card payment to mobile payment.

According to statistics, The number of mobile phone users in the world is expected to pass the five billion mark by 2019 (Statista, 2018). Similarly, from the viewpoint of the access amount, the proportion of Internet data accessed through mobile phone is also increasing. The statistics shows that people gradually accept the way of mobile Internet access.

From a global comparison perspective it is shown that the highest transaction value via mobile payment is reached in China. According to Statista, in China, transaction Value in the Mobile Payments segment amounts to US $414,327 million in 2018. Transaction Value is expected to show an annual growth rate (CAGR 2018-2022) of \(33.5\%$, resulting in the total amount of US\)1,317,924 million by 2022. In the Mobile Payments segment, the number of users is expected to amount to 581.4 million by 2022.

However, the development of mobile payment in the world is very lack of balance. In some countries, such as China, mobile payment has developed to a fairly mature stage, while it is still in the infant stage in Malaysia.

Despite the great potential of such technology in simplifying our lives, its uptake remains limited (Qasim & Abu-Shanab, 2016). Statistic shows that the number of MP users in Malaysia is only 3.2 million, and penetration is only $9.9\%$ (Statista-MCMC, 2018).

Though there are many advantages of mobile shopping and payment, the usage in Malaysia is still very low, and the attitude to the channel of mobile shopping remains unclear (Ghazali, 2018). Due to the rapid rise of communication technologies, mobile payment system has emerged as a popular method to facilitate payment transactions. Notwithstanding its widespread use, what affects intention of mobile users towards paying through mobile phones and why in the context of developing market remain largely unanswered(Ting et al, 2016). Thus the purpose of this paper is to study the factors of acceptance of mobile payment so as to establish competitive advantages of mobile payment and related enterprises in Malaysia. This paper builds a model that affects the acceptance of mobile payment in Malaysia, and makes a forecast on the long-term development of mobile payment in Malaysia and puts forward some useful suggestions.

## II. LITERATURE REVIEW

This paper's theoretical constructs are based on Theory of Reasoned Action (TRA), the Technology Acceptance Model (TAM), Unified Theory of Acceptance and Use of Technology (UTAUT), and the Compass Acceptance Model for the analysis and evaluation of mobile service (CAM). These four well-established theories can be helpful to build a rigid theoretical foundation for this research. They are the most influential theories in clarifying and predicting users' acceptance and adoption in a new system.

As a basic and one of the most influential theories about human behavior in social psychology field, TRA (Theory of Rational Action) points out that individual behavior can be reasonably deduced from behavioral intentions. While the behavior intention is influenced by the attitude and the subjective norm (Fishbein & Ajzen, 1975).

TAM (Technology Acceptance Model) was proposed by Davis and became a popular theory which has been mostly cited by researchers so far. According TAM, a technology adoption depends on Behavioral Intention, while Behavioral Intention is determined by Attitude toward Using and Perceived Usefulness. Attitude toward Using is determined by Perceived Usefulness (PU) and Perceived Ease of Use (PEOU). Perceived Usefulness is determined by Perceived Ease of Use and external variables, and Perceived Ease of Use is determined by external variables (Davis, 1989). PEOU and PU are the two core concept in TAM.

UTAUT (Unified Theory of Acceptance and Use of Technology) integrated eight adoption theory such as TRA, TAM, IDT, TPB, SCT, MM, C-TAM-TPB and model of PC Utilization. According to UTAUT, the four independent variables in UTAUT are Performance Expectancy (PE), Effort Expectancy (EE), Social Influence (SI), Facilitating Condition (FC). UTAUT supposed that the four independent variables are direct determinant of usage intention and behavior (Venkatesh et al., 2003). Gender, age, experience, and voluntariness of use are posited to mediate the impact of the four key constructs on usage intention and behavior (Venkatesh et al., 2003).

Based on the TAM theory, and combined with the features of mobile services, CAM (Compass Acceptance Model for the analysis and evaluation of mobile service) is especially designed for the analysis and evaluation of the user acceptance for mobile services. The model determines four influence factors on the acceptance of mobile service according to four aspects of income, pay, service and service situation. The four factor is Perceived Usefulness, Perceived Ease of Use, Perceived Mobility and Perceived Cost (Amberg et al, 2004).

## III. RESEARCH MODEL AND HYPOTHESES

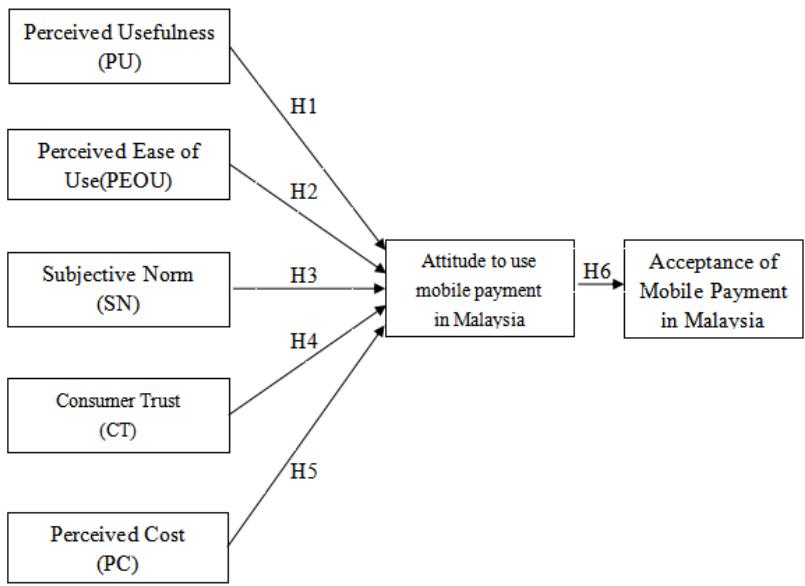

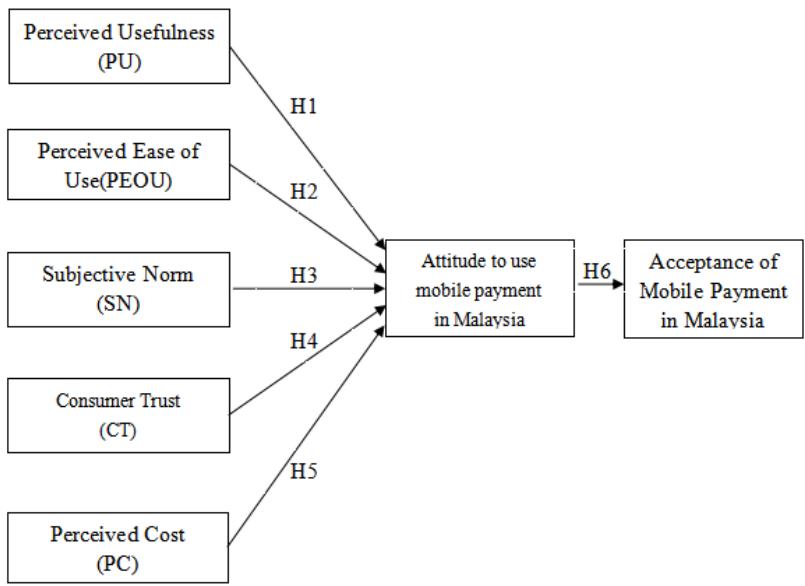

Based on these theories, the hypotheses are developed and then the research model is proposed. The independent variables are PU, PEOU, SN, CT, PC. Attitude is the mediate variable, and Acceptance is the dependent variable.

### a) Perceived Usefulness (PU)

Perceived Usefulness can be interpreted as being the way a system could enhance a consumer's job performance. In the context of mobile payment services adoption, PU is defined as the extent to which an individual believes that using mobile payment services will enhance his or her productivity and performance in conducting payment transactions. If consumers gain a more positive view of mobile payment services, they will have a positive attitude and intention toward the services. Some empirical studies on mobile payment adoption (Kim et al., 2016, Mun, 2017), have also noted PU as an important factor influencing consumer intention to adopt m-payment services. Therefore, the following hypothesis is proposed:

H1: Perceived Usefulness of mobile payment services has a positive effect upon customers' attitude toward using mobile payment services.

### b) Perceived Ease of Use (PEOU)

Although individuals believe that using a particular application could improve their performance, they might find that the application is difficult to master. In TAM and CAM, Perceived Ease of Use is an important element and is concerned with the extent of users' belief that a system is easy to use, to set up, or to learn. PEOU has also been found to have a direct impact on individuals' intentions to adopt m-payment services (Kim et al., 2016; Lesa & Tembo, 2016). Perceived ease of use may have a positive upon the attitude towards mobile payment services, and have a positive effect upon the perceived usefulness. This leads to the following hypothesis.

H2: Perceived Ease of Use of mobile payment services has a positive effect upon customers' attitude to use mobile payment services.

### c) Subjective Norm (SN)

Subjective Norm refers to the degree to which an individual pays attention to and is influenced by the opinions of people who are important to him/her while considering a particular activity (Fishbein & Ajzen, 1975). Subjective norms have been found to be more important prior to, or in the early stages of innovation implementation when users have limited direct experience from which to develop attitudes (Hartwick & Barki, 1994; Taylor & Todd, 1995). Empirical researches show that have positive effect on intention to use mobile payment system (Ting et al., 2016; Teng et al., 2018). Therefore, the hypothesis for this study with regard to SN is proposed as:

H3: Subjective Norm has a positive effect upon customers' attitude to use mobile payment services.

### d) Consumer Trust (CT)

Trust is seen as an expression of security when making an exchange, or in another type of relationship

(Garbarino & Johnson, 1999). Empirically, researches showed that consumer trust and perceived risk have a greater impact on network services. Some researchers believe that Consumer Trust is positively related to consumers' electronic commerce behavior(Jarvenpaa, 2000; Gefen, 2000; Heijden et al., 2003; Pavlou, 2003; Donna, 2006; Qiu et al., 2008; Chong et al., 2012; Phonthanukitithaworn, 2016). In the context of mobile payment services, some scholars proposed that consumer trust must be for both the mobile service provider and the mobile technology (Chandra et al., 2010; Zhou, 2013). In Malaysia, it is found that Trust is an important factor positively related to acceptance of mobile banking (Tham, 2018). Therefore, the hypothesis for this study with regard to Consumer Trust is proposed as:

H4: Consumer Trust has a positive effect upon customers' attitude toward using mobile payment services.

### e) Perceived Cost (PC)

Perceived Cost (PC) refers to the sum of the expenditures felt by the customer during the actual consumption process. It is the time, money, physical strength and energy involved in the customer's entire process of consuming the product or service. Many empirical research have discussed how perceived cost affect acceptance of network products (Soane et al., 2010; Benazić et al., 2015).

Empirical researches show that individual believes using mobile payment services will cost them extra money (Luarn & Lin, 2005). Several studies suggest that Perceived Cost could be a major barrier to the adoption of new technologies in mobile phone services in Taiwan, Malaysia, Thailand and so on

(Cheong & Park, 2005, Wei et al., 2009, Zhou, 2013; Phonthanukitithaworn, 2015). Given this importance of PC, it has been suggested that PC could be incorporated as an extended construct in TAM when investigating mobile payment (Cheong & Park, 2005). Therefore, the hypothesis for this study with regard to PC is proposed as:

H5: Perceived Cost of mobile payment services has a positive effect upon customers' attitude toward using mobile payment services.

### f) Attitude (Att)

Attitude has a significant impact on consumers' behavioural intentions (Fishbein & Ajzen, 1975). Attitude is one of the most important concepts in social psychology (Manstead & Hewstone, 1995). Attitude is viewed as an evaluative judgment of an object in terms of its degree of goodness or badness. Ajzen's (2005) definition of attitude as a "disposition to respond favorably or unfavorably to an object, institution or event", represents this view. Attitude has been frequently used to explain human behaviors (Zimbardo et al., 1977). Previous research has suggested that, when conducting research into usage intentions, attitude will be accepted as a moreaccurate predictor in research, especially in studies on electronic, digital, and wireless channels (Bobitt & Dabholkar, 2001). These assumptions lead to the following hypothesis:

H6: Attitude toward using mobile payment services has a positive effect upon consumers' acceptance to use mobile payment services (Acc).

Now, a model for acceptance of mobile payment is established. It can be illustrated by the figure 1.

Source: developed for this research Figure 1: The conceptual framework for Acceptance of Mobile Payment in Malaysia

## IV. RESEARCH METHODOLOGY

### a) Measure development

Survey has been selected as the central research methodology in this research. The multi-item scales measure was applied to this research in order to test the proposed research model. The statements are written for each item, and the participants were required to indicate whether they agreed or disagreed with the statements on a Likert scale. Some of the items in the survey were taken from previously published scales with appropriate psychometric properties research. The items were adopted or adapted to fit the context of mobile payments. After an extensive literature review on the topic, new items were also developed by this research.

### b) Data Collection

Mobile payment users are the target participants for this survey, which does not necessarily suggest that the participants have adopted the services. Basically, this research will select the people in the economically developed Klang Valley, Kuala Lumpur area as the research object. Respondents were invited to participate in the survey by answering papery questionnaire.

The questionnaire collects two major types of information. One part concerns participants' demographic information, and the other part is about participants' perceptions of each of the constructs in the proposed model. The demographic information includes gender, age, level of education, and occupation. The rest of the questionnaire asks for participants' the opinions of each item.

The sample size depends on several important criteria including statistical, managerial issues and budget. Statistics show that the number of mobile payment user in Malaysia is about 3.2 million. According to Sekaran & Bouge (2010), it is adequate for this study with the sample size 384. A total of about 500 questionnaires were distributed to mobile payment users in Klang Valley, Malaysia and 392 valid were collected.

## V. DATA ANALYSIS

Following the response from survey, the proposed hypotheses will be tested. SEM based analysis techniques will be used to analysis the data. First, the Confirmatory Factor Analysis (CFA) will be employed to assess the validity of the measurement for the model, then the proposed model will be tested using the Structural Equation Modeling (SEM), so that the causal structure of the model can be evaluated. The research will use AMOS to analyse the measurement model and the structural model.

The proposed research model was evaluated using structural equation modelling and employed a two-step modelling approach, including the assessment of the measurement model and the assessment of the structural model (Byrne,2010). The assessment of the measurement model ensures that observed variables are appropriately loaded with regards to the factors they belonged to, with no significant cross-loading to an item of another factor. The assessment of the structural model determines the relationship between independent and dependent variables.

### a) Assessment of measurement model

A confirmatory factor analysis using AMOS (v20) was conducted on all the items simultaneously to evaluate the validity of the items and the seven underlying constructs in the measurement model. The overall fit of the hypothesised model was assessed using eight common model-fit measures: goodness-of-fit (GFI), standardised root mean-square residual (SRMR), root mean-square error of approximation (RMSEA), comparative fit index(CFI), tuckerlewis index(TLI), normalised fit index(NFI), adjusted goodness-of-fit (AGFI), and normed $\chi^2$ /df.

Table I summarises the results for the model-fit indices, which show that the measurement model exhibits a good fit with the data collected. And the evaluation of the psychometric properties of the measurement model in terms of reliability and construct validity can be processed.

Table 1: Results of the measurement model across model-fit indices

<table><tr><td>Fitness Indexes</td><td>Critical Values</td><td>Results</td><td>Fitting Judgment</td></tr><tr><td>X2</td><td></td><td>838.990</td><td></td></tr><tr><td>df</td><td></td><td>618</td><td></td></tr><tr><td>X2/df</td><td>1-3</td><td>1.358</td><td>Y</td></tr><tr><td>SRMR</td><td><0.1</td><td>0.027</td><td>Y</td></tr><tr><td>GFI</td><td>>0.9</td><td>0.902</td><td>Y</td></tr><tr><td>AGFI</td><td>>0.9</td><td>0.882</td><td>Close to 0.9</td></tr><tr><td>NFI</td><td>>0.9</td><td>0.924</td><td>Y</td></tr><tr><td>TLI</td><td>>0.9</td><td>0.976</td><td>Y</td></tr><tr><td>CFI</td><td>>0.9</td><td>0.978</td><td>Y</td></tr><tr><td>RMSEA</td><td><0.08</td><td>0.030</td><td>Y</td></tr></table>

Construct validity was examined through the test for convergent and discriminant validity. Convergent validity was evaluated using the attributes of factor loading, average variance extracted (AVE), and construct reliability (CR). The values are provided in Table II. It shows that all the scale items are highly loaded with respect to their constructs as all factor loadings are above the threshold value of 0.50, and item reliability of each indicator, including CR, had scores above 0.70, suggesting good reliability as well as good convergent validity. Notably, the CR values of the five constructs in the model are all above 0.85 which provides evidence that these measures consistently represent the same latent construct.

Table 2: Factor loadings, AVE, item reliability, and construct reliability of the five-factor CFA model

<table><tr><td>Construct</td><td>Item</td><td>Factor Loading</td><td>SMC</td><td>CR</td><td>AVE</td></tr><tr><td rowspan="5">PU</td><td>PU1</td><td>0.821</td><td>0.674</td><td rowspan="5">0.865</td><td rowspan="5">0.570</td></tr><tr><td>PU2</td><td>0.576</td><td>0.332</td></tr><tr><td>PU3</td><td>0.603</td><td>0.364</td></tr><tr><td>PU4</td><td>0.911</td><td>0.830</td></tr><tr><td>PU5</td><td>0.807</td><td>0.651</td></tr><tr><td rowspan="5">PEOU</td><td>PEOU1</td><td>0.696</td><td>0.484</td><td rowspan="5">0.851</td><td rowspan="5">0.553</td></tr><tr><td>PEOU2</td><td>0.723</td><td>0.523</td></tr><tr><td>PEOU3</td><td>0.744</td><td>0.554</td></tr><tr><td>PEOU4</td><td>0.747</td><td>0.558</td></tr><tr><td>PEOU5</td><td>0.738</td><td>0.545</td></tr><tr><td rowspan="6">SN</td><td>SN1</td><td>0.642</td><td>0.412</td><td rowspan="6">0.865</td><td rowspan="6">0.520</td></tr><tr><td>SN2</td><td>0.649</td><td>0.421</td></tr><tr><td>SN3</td><td>0.621</td><td>0.386</td></tr><tr><td>SN4</td><td>0.805</td><td>0.648</td></tr><tr><td>SN5</td><td>0.827</td><td>0.684</td></tr><tr><td>SN6</td><td>0.753</td><td>0.567</td></tr><tr><td rowspan="7">CT</td><td>CT1</td><td>0.838</td><td>0.702</td><td rowspan="7">0.914</td><td rowspan="7">0.604</td></tr><tr><td>CT2</td><td>0.842</td><td>0.709</td></tr><tr><td>CT3</td><td>0.627</td><td>0.393</td></tr><tr><td>CT4</td><td>0.866</td><td>0.750</td></tr><tr><td>CT5</td><td>0.758</td><td>0.575</td></tr><tr><td>CT6</td><td>0.705</td><td>0.497</td></tr><tr><td>CT7</td><td>0.777</td><td>0.604</td></tr><tr><td rowspan="5">PC</td><td>PC1</td><td>0.856</td><td>0.733</td><td rowspan="5">0.927</td><td rowspan="5">0.719</td></tr><tr><td>PC2</td><td>0.850</td><td>0.723</td></tr><tr><td>PC3</td><td>0.736</td><td>0.542</td></tr><tr><td>PC4</td><td>0.895</td><td>0.801</td></tr><tr><td>PC5</td><td>0.894</td><td>0.799</td></tr></table>

The square root of AVE values were compared with the correlation estimates for assessing discriminant validity. The correlation matrix in Table III shows that the square root of AVE values are all larger than the correlation estimates, confirming that a satisfactory level of discriminant validity has been achieved. This evidence indicates that the measured variables have more in common with the construct they are associated with rather than other constructs in the model. Further, it indicates that all the constructs in the measurement model are significantly different from each other.

Table 3: Matrix of correlation constructs and the square root of AVE for the examination of discriminant validity

<table><tr><td></td><td>PU</td><td>PEOU</td><td>SN</td><td>CT</td><td>PC</td><td>Att</td><td>Acc</td></tr><tr><td>PU</td><td>0.755</td><td></td><td></td><td></td><td></td><td></td><td></td></tr><tr><td>PEOU</td><td>0.564</td><td>0.744</td><td></td><td></td><td></td><td></td><td></td></tr><tr><td>SN</td><td>0.540</td><td>0.558</td><td>0.721</td><td></td><td></td><td></td><td></td></tr><tr><td>CT</td><td>0.379</td><td>0.511</td><td>0.553</td><td>0.777</td><td></td><td></td><td></td></tr><tr><td>PC</td><td>0.152</td><td>0.210</td><td>0.170</td><td>0.210</td><td>0.848</td><td></td><td></td></tr><tr><td>Att</td><td>0.547</td><td>0.561</td><td>0.556</td><td>0.552</td><td>0.230</td><td>0.831</td><td></td></tr><tr><td>Acc</td><td>0.634</td><td>0.624</td><td>0.630</td><td>0.603</td><td>0.282</td><td>0.711</td><td>0.813</td></tr></table>

### b) Assessment of structural model and hypotheses testing

Structural model analysis was undertaken to determine the relationships among the constructs in the proposed model, and subsequently determine the direction of significant paths between the constructs. The overall fit of the structural model was shown satisfactory, which was indicative of good model performance.

Table IV shows that almost all the indexes of the structural equation basically reach the ideal value, which shows that the structural equation model is acceptable. The path parameters are shown in table IV which provide a basis for the following hypothesis verification.

Table 4: The path parameters

<table><tr><td colspan="3">Constructs Path</td><td>S.E.</td><td>C.R.

(T-value)</td><td>P</td><td>Standardized Estimate

(Beta)</td></tr><tr><td>Att</td><td>←</td><td>PU</td><td>0.195</td><td>0.051</td><td>***</td><td>0.220</td></tr><tr><td>Att</td><td>←</td><td>PEOU</td><td>0.218</td><td>0.069</td><td>0.002</td><td>0.201</td></tr><tr><td>Att</td><td>←</td><td>SN</td><td>0.188</td><td>0.058</td><td>0.001</td><td>0.193</td></tr><tr><td>Att</td><td>←</td><td>CT</td><td>0.260</td><td>0.058</td><td>***</td><td>0.245</td></tr><tr><td>Att</td><td>←</td><td>PC</td><td>0.055</td><td>0.03</td><td>0.07</td><td>0.064</td></tr><tr><td>Acc</td><td>←</td><td>Att</td><td>0.319</td><td>0.061</td><td>***</td><td>0.269</td></tr></table>

The results for the structural path analysis indicate the model's structural paths. Four of the model's five paths are statistically significant at the 0.05 level of significance. After cross-matching the results of structural path analysis with the hypotheses, five hypotheses(H1, H2, H3, H4 and H6) were supported and one(H5) were rejected.

Of these five influencing factors, Consumer Trust was the factor with the most influence, having the highest weight of 0.245, followed by PU(0.220), PEOU(0.201), and SN(0.193).

## VI. RESEARCH FINDINGS AND THEIR IMPLICATIONS

The results from the testing of the hypotheses derived from the research model reveals that Malaysian consumers' Perceptions of Cost has no statistically significant relationship with attitude to adopt mobile payment. On the other hand, the factor of Consumer Trust plays the most important role, followed by Perceived Usefulness, Perceived Ease of Use, and Subjective Norm.

Consumer Trust has proved to be the first factor affecting users' attitude to mobile payment services. This finding suggests that consumers will not use mobile payment if they feel that they lack trust in entities associated with the provision of mobile payment services. This lack of trust may be a fundamental problem for consumers to refuse to provide personal information to mobile payment providers. It is important to build trust among potential users of mobile payment services because individuals who have no experience with mobile payment may be insecure in wireless transactions that are invisible to them.

The significant positive correlation between Consumer Trust and adoption attitude indicates that personal trust in mobile payment entities plays an important role in influencing personal use of mobile payment services. Therefore, it implies in practice that entities involved in the mobile payment process, such as financial institutions, businesses and third parties, need to pay attention to security issues. An important step will be to promote and strengthen information that mobile payment services are modern, safe and secure, thereby enhancing Malaysian consumers' trust in mobile payment services.

Secondly, it is proved in this study that Perceived Usefulness is important to users' attitude. The convenience of mobile payments is very attractive to consumers, which is the biggest competitive advantage of mobile payments compared to other payment instruments such as cash and credit cards. In order to further promote mobile payment, mobile payment operators need to continuously improve the consumer experience and provide consumers with better services. The user's usage habits can be gradually cultivated if the Perceived Usefulness is Improved. And the development of mobile payment can come true.

Thirdly, from the results of empirical analysis of this study, it is known that Perceived Ease of Use will positively affect consumer attitude and acceptance to mobile payments. It will enhance users' acceptance if mobile payment is easy to learn and can quickly find the required functions. Practically, mobile payment software should be designed with a simpler interface, designed to be a smoother payment process, to provide consumers with a better user experience, and to make users think that mobile payment is easier to use, so users are more willing to use mobile payment. For mobile payment operator, a simple interface and a simplified payment process is necessary.

Lastly, Subjective Norm was found to have a significant influence on Malaysian consumers' intention to adopt m-payment services. The influence of friends, parents, colleagues and even media can become a critical determinant in the decision-making process of potential users in adopting mobile payment.

In the early stage of using mobile payment, potential users have limited information about mobile payment. Therefore, people who have not used such services before may rely heavily on the opinions of others to help them make decisions. That is to say, consumers will consider the opinions and suggestions of people in their social circles before making mobile payments.

The results of this study confirm the impact of Subjective Norm on Malaysian users. This study demonstrates the role of social impact in people's intention to adopt and use mobile payment. The practical implication of this discovery is that service providers need to improve consumers' acceptance of mobile payment services by considering social and community networks. This may involve developing a marketing strategy that uses a thoughtful approach to advertising by embedding it in informal social channels such as online social networking sites and promoting the spread of mobile payments through word-of-mouth transmission.

The results of this study show that there is no statistical correlation between PC and attitude. The reason is probably that the cost of mobile payment is relatively low at present, which basically involves only a small amount of mobile data and low cost to transfer money from mobile payment platform to bank. Most people think that these costs are reasonable.

## VII. CONCLUSION

This paper studies the attitude and acceptance of mobile payment in Malaysia. This paper proposes a theoretical model which includes the relevant psychological measurement factors that influence consumers' attitude towards mobile payment, and carries out empirical verification. The study found that the acceptance of mobile payment was influenced by the factors of Consumer Trust, Perceived Usefulness, Perceived Ease of Use and Subjective Norm.

The findings of this study have some implications for mobile payment service agents in Malaysia, because they can understand users' attitudes and satisfaction towards mobile payment, and even consumer behavior in decision-making process, and propose areas they can focus on in order to encourage people to adopt this service.

### Conflict of Interest Statement

The authors declare no conflicts of interests.

About the Authors

Cao Yong, PhD, visiting scholar at Management and Science University, Malaysia.

Li Qiang, senior lecturer at Yichun Technical College.

#### APPENDIX

Measurement items

#### Perceived Usefulness

PU1 I believe that using Mobile Payment will enable me to pay more quickly and it can save time for me.

PU2 I believe that using Mobile Payment will enable me to conduct a payment transaction whenever I want, thus it can enhance my payment efficiency.

PU3 I believe that using Mobile Payment will enable me to conduct a payment transaction wherever I am, thus it can enhance my payment efficiency.

PU4 I believe Mobile Payment provides convenience because there is no need to carry cash or credit card.

PU5 Mobile payment can bind multiple cards from different banks, enabling users to complete cross-bank financial transactions.

#### Perceived Ease of use

PEOU1 I think the mobile payment interface is designed to be friendly and easy to understand.

PEOU2 I believe mobile payment easy to learn.

PEOU3 I believe that it is easy to open a Mobile Payment account.

PEOU4 I believe that it is easy to complete transaction by Mobile Payment

PEOU5 For me, using Mobile Payment do not require much mental effort.

#### Subject Norm

SN1 If people who are important to me (For example, my family) use mobile payment, I will consider to use it.

SN2 If people whose opinions I value (For example, my close friends and my relatives) use mobile payment, I will consider to use it.

SN3 If people who are vital to my work (For example, my leaders) use mobile payment, I will consider to use it.

SN4 If many colleagues of mine use m-payment, I will consider using it.

SN5 If the frequency of appearance on the media is high, I will consider using mobile payments.

SN6 If most vendors or merchants accept consumers to use mobile payments, then I will also consider using mobile payments.

#### Consumer Trust

CT1 I believe Mobile Payment is a mature technology

CT2 I believe that my account money is safe (for instance, no loss of my financial details to thieves).

CT3 I believe that my personal information is safe (for instance, it may not be exposed to others).

CT4 I believe that my money transfer process is secure and safe (for instance, no overcharge from merchants or credit card providers)

CT5 I believe that when the payment security problem arise, the mobile payment service provider and bank are able to solve these problems in time.

CT6 I believe there is no financial loss in my mobile payment account even if the smart phone is lost.

CT7 I believe that mobile payment provider are trustworthy and honest.

#### Perceived cost

PC1 I'm worried the cost of opening a mobile account will be high.

PC2 I'm worried the transaction fees for using m-payment will be high

PC3 I'm worried the cost of transferring money from a mobile account to a bank account will be high.

PC4 I am worried that using mobile payments will consume a lot of mobile phone data and increase my spending.

PC5 I am worried that it will cost a lot of money to replace a device that can use mobile payments.

Attitude to use mobile payment

Att1 The performance of Mobile Payment meets my expectation.

Att2 I think the positive effect of mobile payments is greater than negative.

Att3 When I don't have time to visit the site (such as working or studying) and need to spend at the same time (such as online shopping or buying tickets), I am happy to use mobile payment.

Att4 I am happy to use mobile payments when the mall needs to line up.

Acceptance of mobile payment

Acc1 For me, using mobile payment is a good idea.

Acc2 Mobile payment brings me a pleasant experience, I am willing to use it.

Acc3 I will use mobile payment as a primary payment method.

Acc4 I like using mobile payment and I will recommend it to my friends.

<table><tr><td>Categories</td><td>Demographic frequency</td><td>Percentage</td></tr><tr><td>Gender</td><td></td><td></td></tr><tr><td>Male</td><td>187</td><td>47.70%</td></tr><tr><td>Female</td><td>205</td><td>52.30%</td></tr><tr><td>Age</td><td></td><td></td></tr><tr><td>Below 20</td><td>51</td><td>13.01%</td></tr><tr><td>20-35</td><td>133</td><td>33.93%</td></tr><tr><td>36-50</td><td>94</td><td>23.98%</td></tr><tr><td>51-60</td><td>74</td><td>18.88%</td></tr><tr><td>Above 60</td><td>40</td><td>10.20%</td></tr><tr><td>Education level</td><td></td><td></td></tr><tr><td>High school or lower</td><td>134</td><td>34.18%</td></tr><tr><td>Bachelor</td><td>208</td><td>53.06%</td></tr><tr><td>Master</td><td>41</td><td>10.46%</td></tr><tr><td>Doctor</td><td>9</td><td>2.30%</td></tr><tr><td>Monthly income</td><td></td><td></td></tr><tr><td>1500 or less</td><td>115</td><td>29.34%</td></tr><tr><td>1500-3000</td><td>125</td><td>31.89%</td></tr><tr><td>3001-5000</td><td>89</td><td>22.70%</td></tr><tr><td>5001-8000</td><td>41</td><td>10.46%</td></tr><tr><td>Above 8000</td><td>22</td><td>5.61%</td></tr><tr><td>Occupation</td><td></td><td></td></tr><tr><td>Government servant</td><td>70</td><td>17.86%</td></tr><tr><td>Business owner</td><td>16</td><td>4.08%</td></tr><tr><td>Staff in private company</td><td>105</td><td>26.79%</td></tr><tr><td>Student</td><td>123</td><td>31.38%</td></tr><tr><td>Others</td><td>68</td><td>17.35%</td></tr></table>

Generating HTML Viewer...

References

38 Cites in Article

I Ajzen (2005). Attitudes, personality and behaviour.

Michael Amberg,Markus Hirschmeier,Jens Wehrmann (2004). The Compass Acceptance Model for the analysis and evaluation of mobile services.

D Benazić,A Tanković (2015). Impact of Perceived Risk and Perceived Cost on Trust in the Online Shopping Websites and Customer Repurchase Intention, 24th CROMAR congress: Marketing Theory and Practice -Building Bridges and Fostering Collaboration.

L Bobbitt,P Dabholkar (2001). Integrating attitudinal theories to understand and predict use of technology-based self-service: The Internet as an illustration.

B Bryne (2010). The AMOS Program.

Shalini Chandra,Shirish Srivastava,Yin-Leng Theng (2010). Evaluating the Role of Trust in Consumer Adoption of Mobile Payment Systems: An Empirical Analysis.

Je Ho Cheong,Myeong‐cheol Park (2005). Mobile internet acceptance in Korea.

Alain Yee-Loong Chong,Felix Chan,Keng-Boon Ooi (2012). Predicting consumer decisions to adopt mobile commerce: Cross country empirical examination between China and Malaysia.

F Davis (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology.

W Donna (2006). The importance of ease of use, usefulness, and trust to online consumers: An examination of the technology acceptance model with older consumers.

M Fishbein,I Ajzen (1975). Belief, Attitude, Intention, and Behavior: An Introduction to Theory and Research.

Ellen Garbarino,Mark Johnson (1999). The Different Roles of Satisfaction, Trust, and Commitment in Customer Relationships.

David Gefen (2000). E-commerce: the role of familiarity and trust.

E Ghazali (2018). Do consumers want mobile commerce? A closer look at M-shopping and technology adoption in Malaysia.

Jon Hartwick,Henri Barki (1994). Explaining the Role of User Participation in Information System Use.

H Heijden,T Verhagen,M Creemers (2003). Understanding online purchase intentions: Contributions from technology and trust perpectives.

Sirkka Jarvenpaa,Noam Tractinsky,Michael Vitale (2000). Consumer trust in an Internet store.

Yonghee Kim,Young-Ju Park,Jeongil Choi,Jiyoung Yeon (2016). An Empirical Study on the Adoption of “Fintech” Service: Focused on Mobile Payment Services.

E Lesa,S Tembo (2016). Study on Factors Affecting Mobile Payment Systems Diffusion in Zambia.

Pin Luarn,Hsin-Hui Lin (2005). Toward an understanding of the behavioral intention to use mobile banking.

A Manstead,M Hewstone (1995). The Blackwell Encyclopedia of Social Psychology.

Yeow Mun,Haliyana Khalid,Devika Nadarajah (2017). Millennials’ Perception on Mobile Payment Services in Malaysia.

P Pavlou (2003). Consumer Acceptance of Electronic Commerce: Integrating Trust and Risk with the Technology Acceptance Model.

C Phonthanukitithaworn,C Sellitto,M Fong (2015). User intentions to adopt mobile payment services: a study of early adopters in Thailand.

Chanchai Phonthanukitithaworn,Carmine Sellitto,Michelle Fong (2016). An investigation of mobile payment (m-payment) services in Thailand.

Ajao Qasim,Emad Abu-Shanab (2016). Drivers of mobile payment acceptance: The impact of network externalities.

Lingyun Qiu,Dong Li (2008). Applying TAM in B2C E-commerce research: An extended model.

U Sekaran,R Bougie (2010). Research methods for business: A skill-building approach.

Emma Soane,Chris Dewberry,Sunitha Narendran (2010). The role of perceived costs and perceived benefits in the relationship between personality and risk‐related choices.

Shirley Taylor,Peter Todd (1995). Understanding Information Technology Usage: A Test of Competing Models.

P Teng,T Ling,K Seng (2018). Understanding Customer Intention to Use Mobile Payment Services in Nanjing, China.

Seyed Nikou,Harihodin Selamat,Rasimah Yusoff,Mohsen Khiabani (2018). Electronic Customer Relationship Management, Customer Satisfaction, and Customer Loyalty: A Comprehensive Review Study.

Hiram Ting,Yusman Yacob,Lona Liew,Wee Lau (2016). Intention to Use Mobile Payment System: A Case of Developing Market by Ethnicity.

V Venkatesh,M Morris,G Davis,F Davis (2003). User acceptance of information technology: Toward a unified view.

Viswanath Venkatesh,V Ramesh,Anne Massey (2003). Understanding usability in mobile commerce.

T Wei,G Marthandan,A Chong,K Ooi,S Arumugam (2009). What drives Malaysian mcommerce adoption? An empirical analysis.

P Zimbardo,E Ebbesen,C Maslach (1977). Influencing attitudes and changing behaviour.

T Zhou (2013). An empirical examination of continuance intention of mobile payment services.

No ethics committee approval was required for this article type.

Data Availability

Not applicable for this article.

How to Cite This Article

Cao Yong. 2026. \u201cAn Empirical Model of Acceptance of Mobile Payment in Malaysia\u201d. Global Journal of Management and Business Research - E: Marketing GJMBR-E Volume 22 (GJMBR Volume 22 Issue E1).

Explore published articles in an immersive Augmented Reality environment. Our platform converts research papers into interactive 3D books, allowing readers to view and interact with content using AR and VR compatible devices.

Your published article is automatically converted into a realistic 3D book. Flip through pages and read research papers in a more engaging and interactive format.

Our website is actively being updated, and changes may occur frequently. Please clear your browser cache if needed. For feedback or error reporting, please email [email protected]

Thank you for connecting with us. We will respond to you shortly.