The sovereign debt crisis has severely affected countries within the Eurozone. The widespread consequences of the crisis include economic recession and financial markets downturn. The following essay provides a detailed overview of the debt crisis and its major impacts on financial markets and institutions, and presents lessons learned following the crisis. The results presented by this essay comprise the strong interconnection within the Eurozone and the lack of efficient regulations.

## I. INTRODUCTION

A sovereign default is defined as the failure of a government to meet payments on its debt obligations to domestic and external creditors (Nelson, 2013). The default risk of several European countries increased excessively after the 2007/2008 financial crisis, when indebted nations extended their borrowings to recover from recession. Consequently, by 2010 they were facing severe budget deficits. The European sovereign debt crisis evolved into the biggest challenge of the Eurozone as it threatened the stability of the Economic and Monetary Union, financial markets and banking systems.

The purpose of this essay is to provide an in-depth analysis of the causes and effects of the European sovereign debt crisis as well as the measures taken to respond to the crisis.

The essay is organised in six parts. It will first explain the main causes of the crisis. Secondly, it will present the consequences on financial markets and institutions. Thirdly, the effectiveness of the measures implemented to solve the crisis will be evaluated. Finally, the essay discusses the aftermaths of the crisis, including its effects on the financial landscape, the new trends emerging, and the lessons to be learned.

## II. MAIN CAUSES OF THE EUROPEAN SOVEREIGN DEBT CRISIS

The European debt crisis was triggered in 2009 by negative macroeconomic and financial shocks involving governments, banks, and inefficient regulations. Firstly, it is essential to recount the Eurozone's establishment to understand the debt crisis. The European Economic and Monetary Union (EMU) is an agreement between the European Union's member states, to establish a common monetary policy and a single currency, the euro (Eurozone Portal, 2014). The EMU is described in the Maastricht Treaty of 1992, and pursued to facilitate capital and commercial flows and enhance economic growth. To be part of the Eurozone, the member states have to meet strict requirements in terms of price stability, public finance, interest rates and currency exchange rates. As an integral part of the EMU, the European Central Bank was established in 1998 to regulate the monetary policy in the Eurozone. In January 1st 1999, the euro was officially instituted as the common currency of eleven members of the EU. As of today, the Eurozone consists of eighteen countries (Eurozone Portal, 2014).

Even though the Stability and Growth Pact (SGP) was established in 1997 to control EMU members' budget balances (limiting budget deficit at $3\%$ of GDP and total debt at $60\%$ of GDP), a fiscal union and a banking union were missing in the euro area. When they joined the Eurozone, governments were now able to access credit markets easily and benefit from low interest rates without being monitored (Lane, 2012, pp. 49-67). Portugal, Ireland, Italy, Greece, and Spain, commonly referred to as the PIIGS, are at the centre of the sovereign debt crisis. Indeed, the favourable access to capital markets resulted in excessive borrowing and government spending by the PIIGS. Figure 1 emphasises the fact that the PIIGS' budget deficit was higher than the $3\%$ allowed by SGP when they joined the Eurozone.

Figure 1: Budget Deficit 1991-2014

Source: Bloomberg, 2014

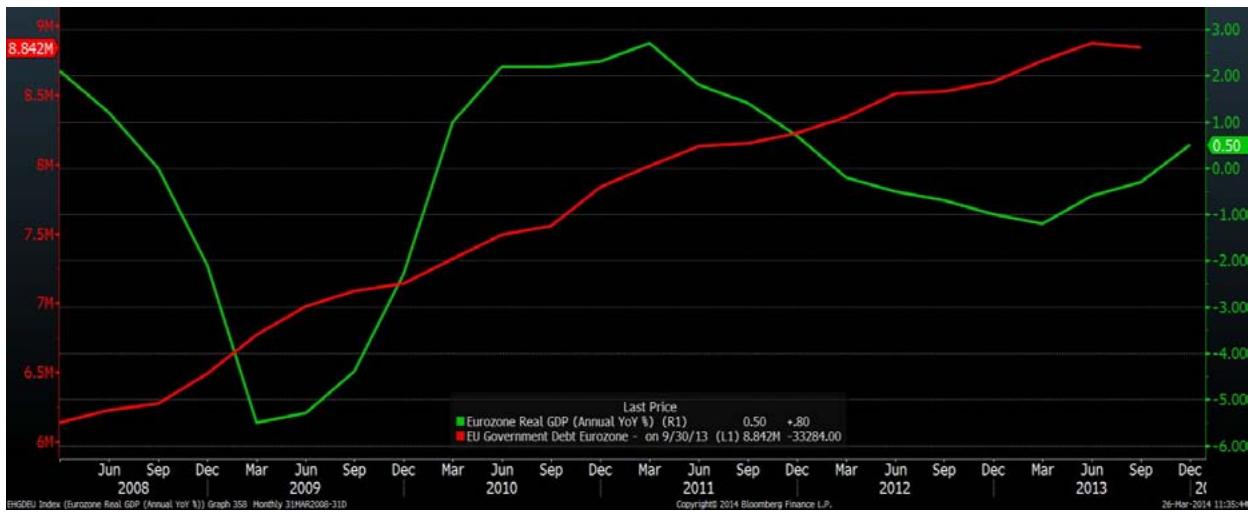

Beside the macroeconomic challenges within the Eurozone, the financial crisis which started in the US in 2007 had significant impacts on Europe. The bankruptcy of Lehman Brothers, the biggest securitisation provider in the US, led to soaring investor' uncertainty and difficult cross-border access to liquidity between banks. Likewise, due to high exposure of European financial institutions to losses in the US, EMU countries' banking system faced serious problems. Hence, governments had to support domestic financial institutions. For instance, Ireland's banks were destructed so the government provided two-year liability guarantee to banks in Ireland. Additionally, governments set up subsidies, such as the "Abwrackpraemie" in Germany for the automotive sector, to boost growth and prevent economic recession (BAFA, Bundesamt für Wirtschaft und Ausfuhrkontrolle, 2014). However, as the Eurozone's economy slowed down (GDP fell to $-5.5\%$ in the first quarter of 2009) and countries continued their intensive borrowing, their total debt increased even more as shown in Figure 2.

Figure 2: Eurozone: Real GDP vs. Government Debt

Source: Bloomberg, 2014

The culminating event of the sovereign debt crisis happened in October 2009 when Greece announced a much higher than expected annual deficit to GDP forecast (Lane, 2012, pp. 49-67). The country had changed political legislation, and revised its forecast from $6\%$ to $12.7\%$. Although in the past

European economies' high budget deficits did not result in negative reaction from the markets, Greece's official announcement increased concerns about the fiscal irresponsibility of peripheral countries (Bernoth and Von Hagen et al., 2012, pp. 975-995).

## III. IMPACT ON THE BOND MARKET AND ITS IMPLICATIONS ON OTHER MARKETS

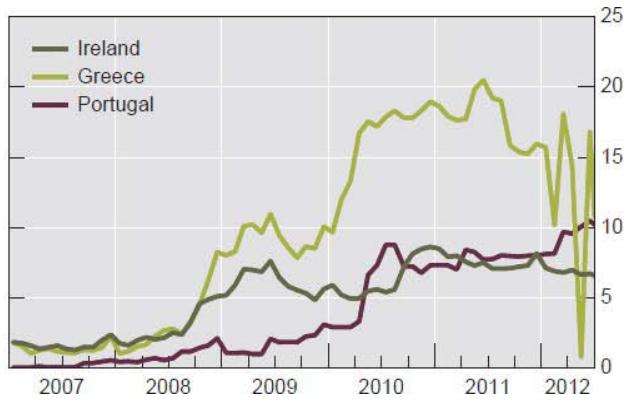

The European debt crisis reached its first peak in the first half of 2011 after Greece, Ireland and Portugal officially requested financial assistance. According to Bernoth and Von Hagen (2012), "government bond yields include risk premiums; increasing indebtedness may cause bond yields to go up, thus raising the cost of borrowing and imposing discipline on governments." Governments issue debt almost every week to roll their outstanding bonds. Therefore, the risk of not being able to borrow rose (Bernoth and Von Hagen et al., 2012, pp. 975-995).

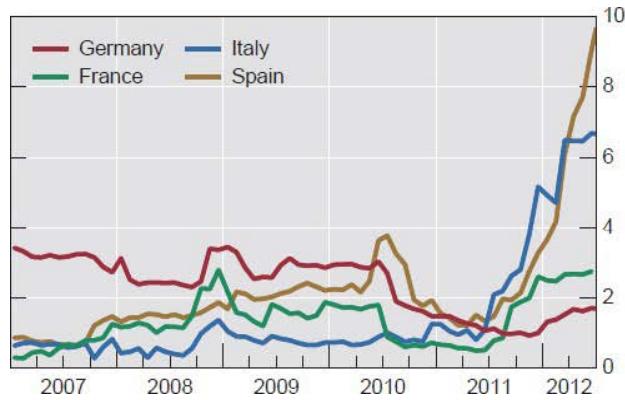

Figure 3: PIIGS 10-year Government Spread to Germany

Source: Bloomberg, 2014

Figure 3 emphasises the deteriorating situation of bond markets by observing the widening spreads of ten-year bond yields of the PIIGS countries. The second peak of the yield can be examined in May 2012 when Greece faced default risk once again. However this time, the second rescue package of €130 billion from the IMF and the EU was granted under the condition that a debt swap be concluded. Private investors such as banks, insurance companies and investment funds had to accept a haircut on their Greek bonds' face value. Due to the financial restructuring of Greece, the fear about contagion effect on other Eurozone countries increased (DW.de, 2014). Consequently, credit rating agencies had to adjust their ratings of the PIIGS' sovereign debt (Table 1).

Table 1: Sovereign Debt Ratings

<table><tr><td></td><td>Germany</td><td>Italy</td><td>Spain</td><td>Ireland</td><td>Greece</td><td>Portugal</td></tr><tr><td>Moody's</td><td>Aaa</td><td>Baa2</td><td>Baa2</td><td>Baa3</td><td>Caa3</td><td>Ba3</td></tr><tr><td>S&P</td><td>AAAu</td><td>BBBu</td><td>BBB-</td><td>BBB+</td><td>B-</td><td>BBu</td></tr><tr><td>Fitch</td><td>AAA</td><td>BBB+</td><td>BBB</td><td>BBB+</td><td>B-</td><td>BB+</td></tr></table>

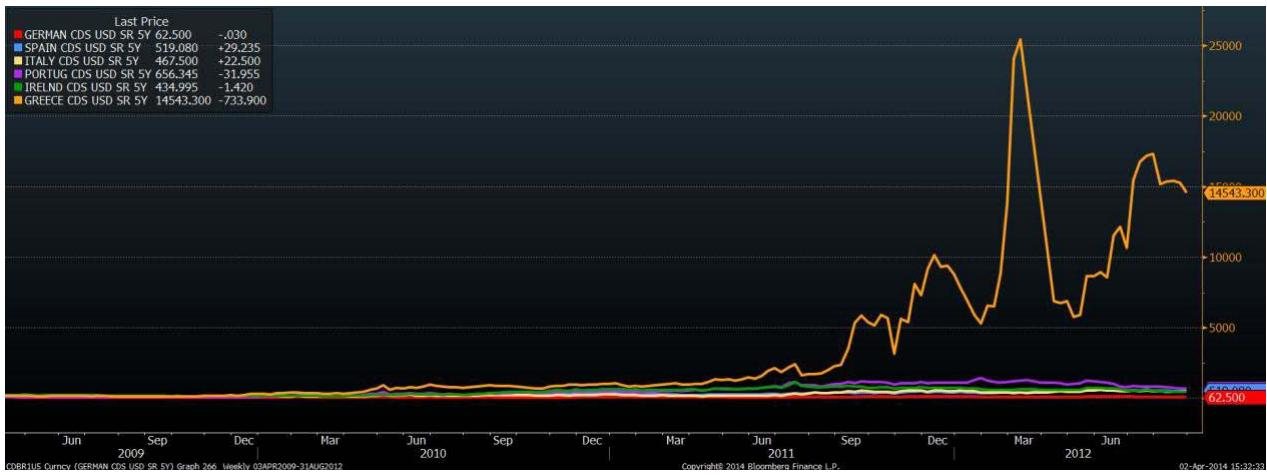

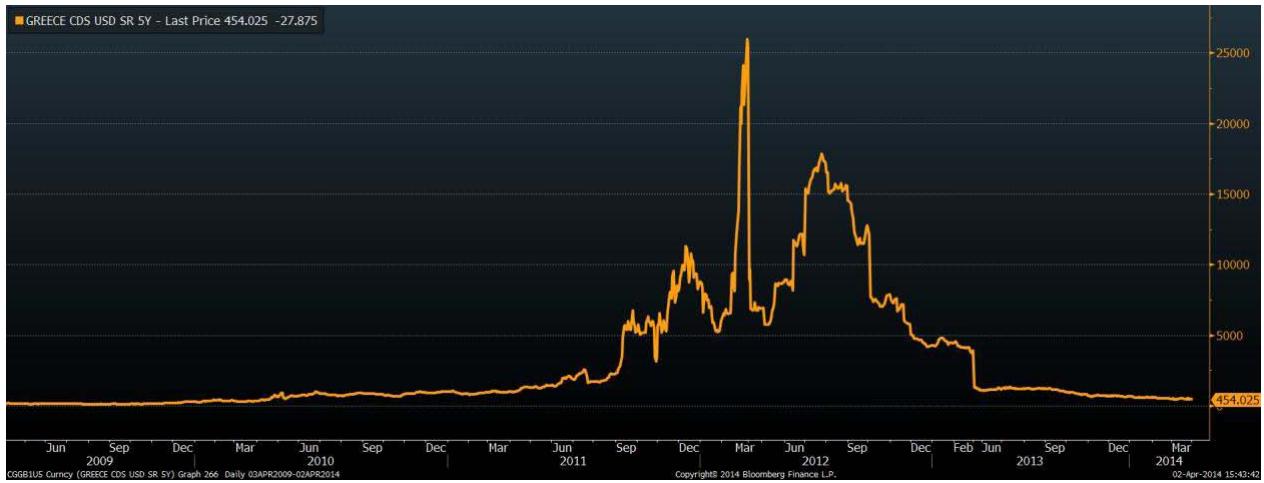

In parallel, prices for derivative instruments used by financial institutions to hedge against sovereign default risk soared. Credit default swap (CDS) spreads are valuable indicators to measure sovereign risk as they are usually traded as an insurance against sovereign bond default (Alloway, 2013). Hence, tighter spreads represent lower risk and wider spreads such as shown by Figure 4 suggest a higher event-risk. Figure 4 depicts a dramatic increase in March 2012 which indicates a high default probability of Greece. Additionally, at a spread of 2500 bps, Greece's CDS contracts were too expensive to be traded (Arghyrou,

Kontonikas et al., 2012, pp. 658-677; Lucas and Schwaab et al., 2013). Figure 5 emphasises the uncertainty and the contagion risk to other peripheral countries.

Source: Bloomberg, 2014

Figure 4: 5y-Credit Default Swap Greece

Figure 5: 5y-Credit Default Swap PIIS compared to Germany

Source: Bloomberg, 2014

Beside the bond market, these circumstances weakened the Eurozone and its common currency the euro. The whole system of the EMU was questioned and as a sign of increased concerns about the future instability of the Eurozone, the Euro to US-Dollar exchange rate depreciated massively (Figure 6).

Figure 6: Euro/Dollar Fluctuation

Source: Bloomberg, 2014

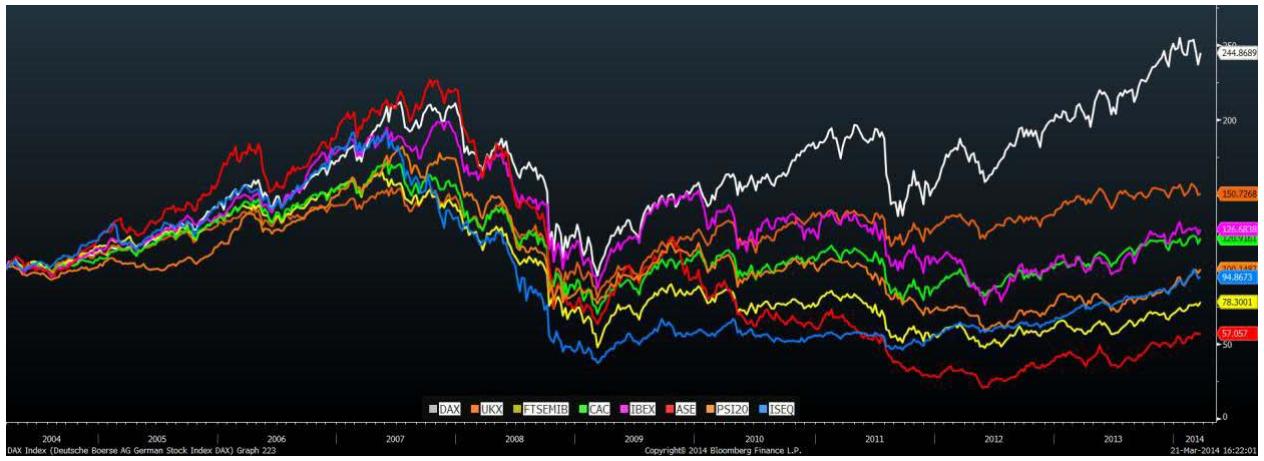

The European stock markets also experienced a downward trend as a result of the financial crisis. According to Figure 7, stock markets remained volatile between 2008 and the beginning of 2012 because of the political and economic uncertainty. However, when the newly appointed ECB President, Mario Draghi, pledged "to do whatever it takes to preserve the euro" in July 2012, the German and British equity markets improved (Random, 2012). In addition, as the federal funds rate was kept at the historical low of $0.25\%$, investors shifted to equities as they were more lucrative investments.

Figure 7: Most liquid European Stock Markets

Source: Bloomberg, 2014

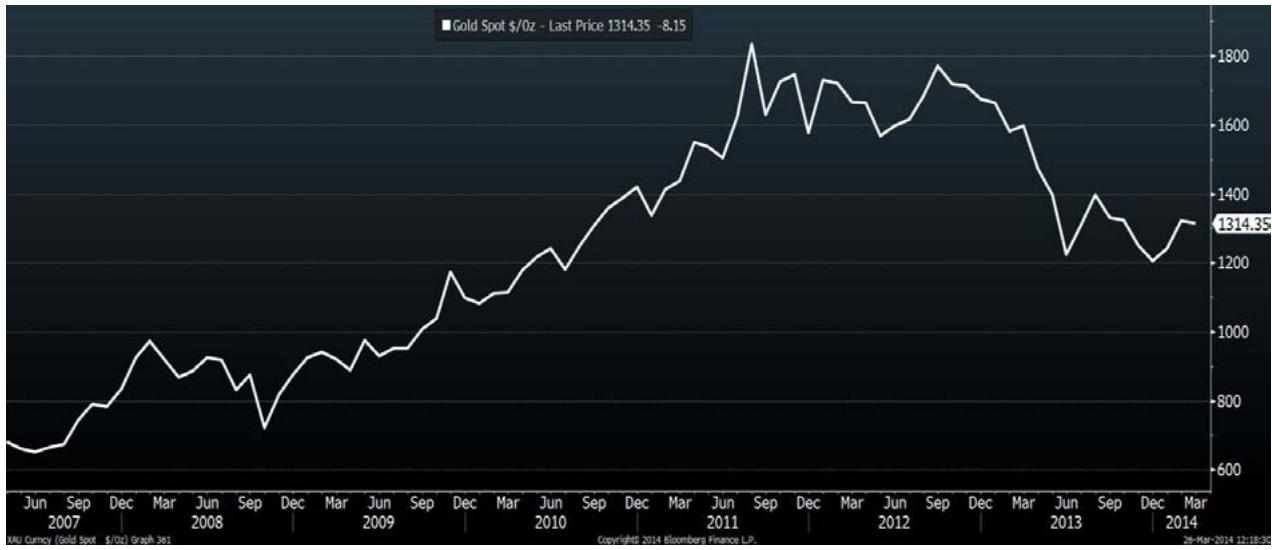

Consequently, risk averse investors sought safer asset classes such as gold. Figure 8 depicts the upward trend of gold price since 2009. Gold price started to decrease in September 2012 when the European economy seemed to recover.

Figure 8: Gold Price Increases in Uncertain Time Periods, 2007-2014

Source: Bloomberg, 2014

## IV. IMPACT ON FINANCIAL INSTITUTIONS

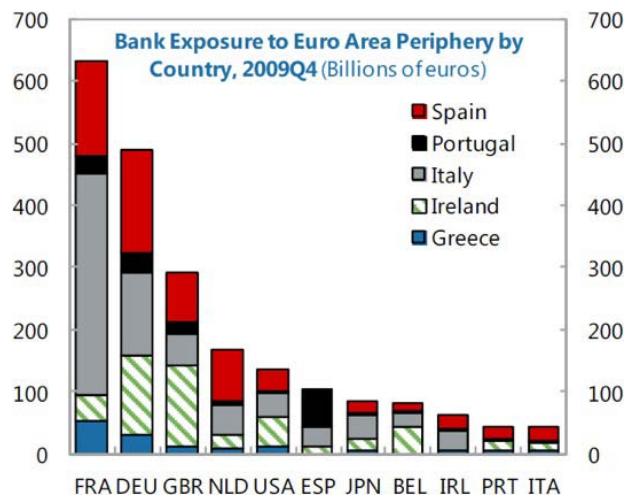

The main effects of the debt crisis on financial institutions, such as commercial banks, investment banks and insurance companies were lower profitability and rising insolvency risk. In the last quarter of 2009, foreign and European banks had a debt exposure of € 560 Billion to the PIIGS's debts. Figure 9 illustrates banks' exposure to PIIGS' debts. Europe financing systems are interconnected so even though the PIIGS are relatively small countries their risk of default caused a threat to the whole banking system (Bloomberg, 2013).

Source: Bank for International Settlement, 2010 Figure 9: European and Foreign Banks Debt Exposure to PIIGS

Therefore, as commercial banks worried about each other's solvency and exposure level to sovereign debt default, counterparty risk increased. Interbank lending slowed down following a dramatic increase of the interbank interest rates within the Eurozone from March 2010 as shown in Figure 10.

Figure 10: EURIBOR vs. EONIA, 2009-2014

Source: Bloomberg, 2014 In addition, consumers' concerns about insolvency increased, thus deposits were withdrawn from banks from countries where the banking system was perceived as risky (Allen and Moessner, 2012, pp. 1-26). As shown in Table 2, the growth of deposits from clients and banks slowed down within the euro area

(Allen and Moessner, 2012, pp. 1-26). The table also depicts a downward trend in inter- commercial banks loans. Between July 2008 and June 2011, it decreased by €593 billion which highlights the serious loss of confidence among euro area commercial banks.

Table 2: Combined Balance Sheet of Euro Area Commercial Banks, 2007-2012

<table><tr><td></td><td colspan="2">ASSETS

(€Billion)</td><td colspan="2">LIABILITIES

(€Billion)</td></tr><tr><td>Changes</td><td>Loans to domestic households and businesses</td><td>Loans to commercial banks</td><td>Deposits from households and businesses</td><td>Deposits from commercial banks</td></tr><tr><td>Jul 07–Jun 08</td><td>961</td><td>713</td><td>1,009</td><td>717</td></tr><tr><td>Jul 08–Jun 10</td><td>339</td><td>-106</td><td>969</td><td>275</td></tr><tr><td>Jul 10–Jun 11</td><td>235</td><td>-487</td><td>362</td><td>-851</td></tr><tr><td>Jul–Dec 11</td><td>-62</td><td>294</td><td>92</td><td>665</td></tr><tr><td>Jan–Jun 12</td><td>27</td><td>-276</td><td>86</td><td>252</td></tr></table>

Central banks became the lender of last resort for commercial banks. The Eurosystem, an institution comprised of the national central banks of Eurozone members, played a key role in the banking system crisis. Central banks from countries with surplus deposited their funds in the Eurosystem, and central banks from countries with deficit borrowed from the Eurosystem, to provide their commercial banks with funds (Allen and Moessner, 2012, pp. 1-26). As shown in Figure, from 2009 the PIIGS' commercial banks significantly increased their borrowings from the Eurosystem.

Source: Datastream; national data

Figure 11: Commercial Banks Loans through the Eurosystem

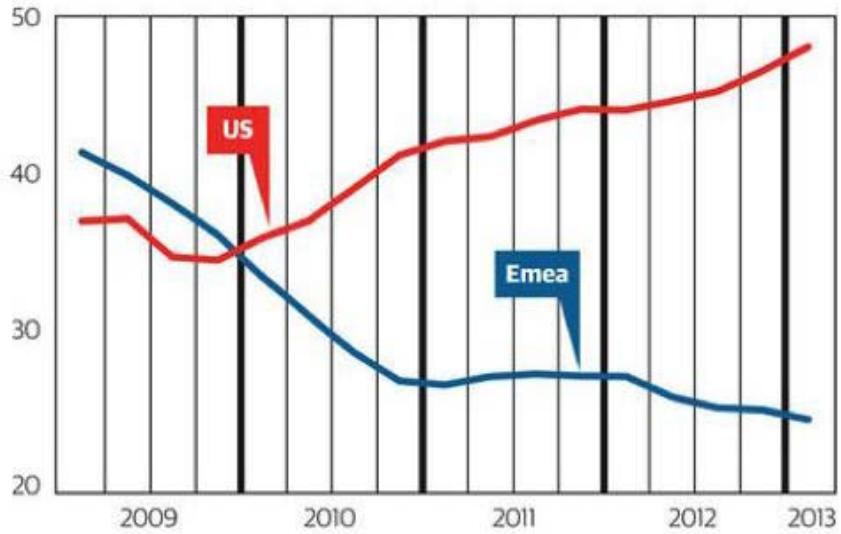

The weaker economic environment in Europe also impacted on investment banks. As the sovereign-debt crisis weighed on stock markets and investors lost confidence, initial public offerings, trading and merger and acquisitions activities were severely affected.

Europe was hit hard by the slowdown in financial markets, with investment banking fees in the region so far falling to the lowest level in ten years in 2012, according to Thomas Reuters (Sakoui, 2012).

Figure 12: US vs. EMEA Global Share of Investment Banking Fees (%)

Source: Dealogic In addition, fixed-income revenue for the 10 largest global investment banks, which include European banks, Barclays, Deutsche Bank, Credit Suisse and UBS, dropped at least $25\%$ between 2009 and 2012 (Ewing, 2012). This downturn in the investment banking industry resulted in more than 120,000 job cuts between 2011 and 2012 (Ewing, 2012). Banks scaled down their investment banking division to

concentrate on expanding services to consumers and businesses to improve their profitability and sustainability.

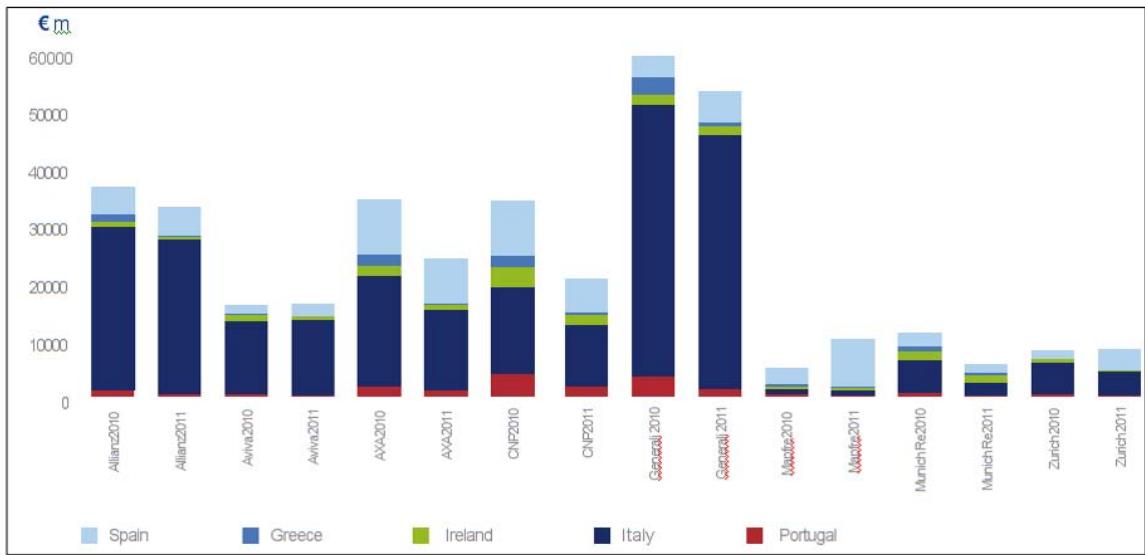

The European debt crisis impact on insurance companies was due to their debt exposure to European sovereign bonds. Indeed, insurers invest heavily in financial markets and primarily allocate their assets in bonds; therefore they are highly sensitive to interest rates fluctuations. Declining interest rates on the PIIGS sovereign debts resulted in lower investment returns and impacted insurers' profitability (Willis Market Security, 2011, pp. 2-7). As shown in Figure 13, the major companies' debt exposure to Italy sovereign debt was the highest, approximately € 200 billion in 2010 and 2011.

Figure 13: Main Insurance Companies Exposure to Sovereign Debt, 2010 and 2011

Source: KPMG

## V. EFFECTIVENESS OF POLICIES AND MEASURES

Several measures have been implemented by financial institutions and European policy makers to respond to the ongoing crisis. The first set of measures relates to government bailouts. Greece was the first country to seek official financial assistance. During 2010 and 2012, emergency loans of over €240 billion were provided to Greece by the EU, the IMF and the ECB. The bailout's objectives were to enable Greece to restructure its debt and meet its budget targets. Subsequently, two temporary facilities were established in 2010 to provide financial assistance to distressed economies through loans and bond purchases: The European Financial Stabilisation Mechanism (EFSM) and European Financial Stability Facility (EFSF) (Papadimas, 2010). Portugal and Ireland were respectively granted loans of €67.5 billion and €78 billion through the EFSM and the EFSF. The European Stability Mechanism (ESM) was set up in 2012 as a permanent replacement for the EFSF and EFSM (ECB wp, M. D. Paries, R. Santis, 2013).

In parallel, the ECB set up conventional and unconventional measures to increase the liquidity, reduce credit risk and restore confidence on financial markets. The ECB first decreased the key interest rate in April 2010 from $1\%$ to $0.25\%$ to lower borrowing costs and boost investments. The unconventional measure was to intervene in the financial markets by launching the Securities Market Programme (SMP). The SMP enabled the ECB to purchase securities and aimed at stabilizing the transmission mechanism of monetary policy.

As a result of the measures implemented by the European policymakers and financial institutions, Figure 14 shows the bond market regained ground starting from 2013, as the borrowing costs of the PIIGS have fallen to pre-crisis levels (Alderman, 2014).

Figure 14: PIIGS 10-year Bond Yields, 2009-2014

Source: Bloomberg, 2014

Greece 10-year bond yield IS currently trading at $6.84\%$, down $50\%$ from last year, and Ireland trading at $3\%$ compared to $14\%$ at the peak of the crisis (Alderman, 2014). Furthermore, Figures 15 and 16 emphasise the decrease in CDS trading as financial assistance provided by the bailout programmes reduced the PLIGS' default risk.

Source: Bloomberg, 2014

Figure 15: Stabilised 5year-CDS Greece

Figure 16: Current 5year-CDS PIISS compared to Germany, 2014

Source: Bloomberg, 2014

Ireland and Spain become the first countries to exit the bailout program respectively in 2013 and 2014 (McDonald, 2013). They will no longer have access to bailout loans, but can issue bonds again.

Despite the positive effects on the financial markets, providing financial assistance did not address the budget deficit issue effectively. The bailouts were granted under the condition that the countries implement tough austerity measures to achieve budget stability; however policymakers underestimated the effects of these measures as the countries' economic growth remain slow (Spiegel Online, 2013).

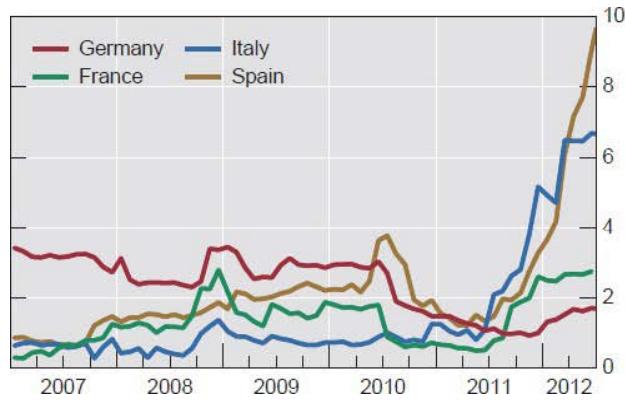

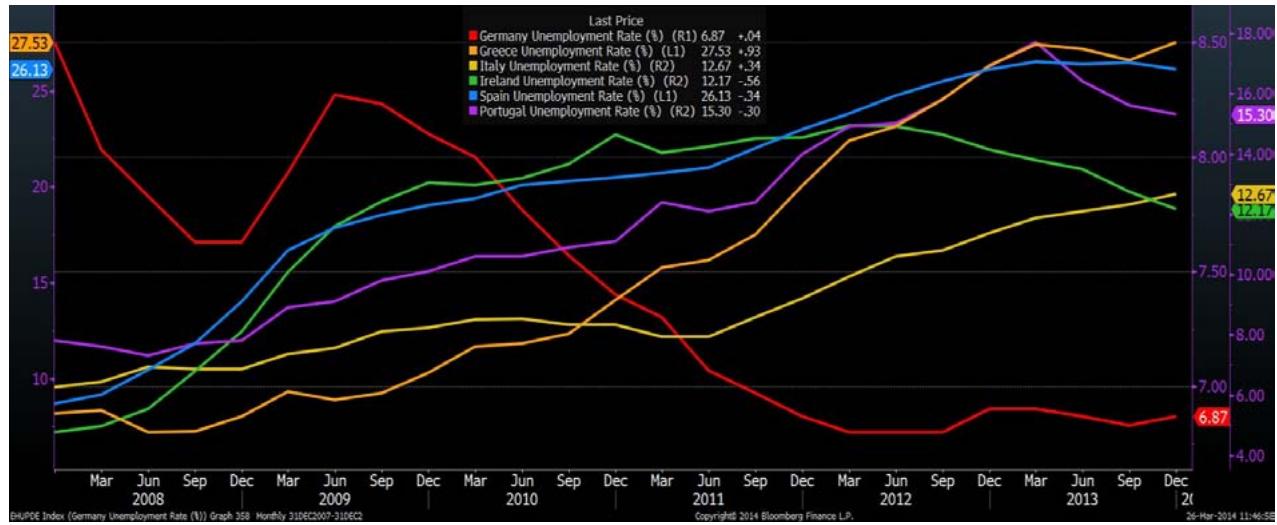

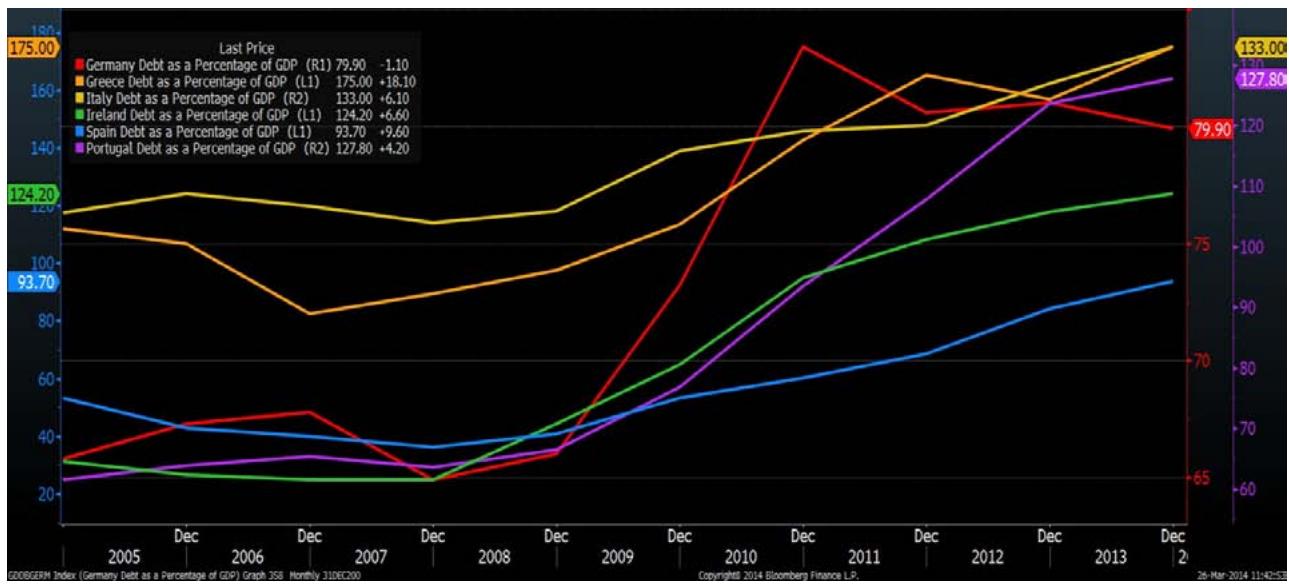

Unemployment in the Eurozone has reached record highs; Greece and Spain are the most severely hit countries with rates currently above $26\%$ as shown in Figure 17. In addition, as shown in Figure 18, the countries' debts as a percentage of GDP are currently higher than ever.

Source: Bloomberg, 2014

Figure 17: Germany and PIIGS Unemployment Rate

Figure 18: PIIGS Debt as a Percentage of GDP

Source: Bloomberg, 2014

Another critical aspect is the unconventional intervention of the ECB in the European sovereign bond market. Firstly, by buying government securities, the ECB is impacting the valuation of sovereign debt which is inconsistent with the main goals of monetary policy. ECB's high level of influence in operational financial market activities could lead to the deformation of the markets over a medium or long period of time.

Furthermore, the ECB is expanding the size of its balance sheet which endangers its independency (Procedia Economics and Finance 3 (2012) 763 - 768, A. Romana, I. Bilana).

## VI. EFFECTS ON THE FINANCIAL LANDSCAPE, LESSONS LEARNED AND NEW TRENDS

The debt crisis revealed several structural problems within the EU framework and within European economies. An important lesson to be taken from these recent events is that a currency union should also result in a fiscal union (Dombret, 2013). This understanding has led to the revisions of several EMU policies: Policymakers have introduced new packages of legislation, such as the "two-pack" for Eurozone members in 2013 to prevent excessive levels of debt and ensure fiscal stability (Eurozone Portal, 2014). The "two-pack" strengthens the existing SGP by imposing a budgetary coordination, and stricter economic and financial surveillance in the euro area. The member states budgetary plans will be assessed by the European Commission prior to their adoption and members experiencing financial instabilities will be monitored closely (Eurozone Portal, 2014).

Severe weaknesses in the banking sector were also revealed by the debt crisis, reminding that banking crises have the strong potential of slowing down the global economy(Nowotny, 2012). European governments are working towards setting up supervisory authorities in the banking sector to enhance financial stability. A key pillar of the future banking union, the Capital Requirements Directive, which sets stronger capital requirements for banks, was adopted in January 2014, in addition to Basel III. The Single Supervisory Mechanism should enter into force in autumn 2014, creating a supervision system for banks within the EU(ECB, 2014). A banking union should lead to better supervision of the sector and ensure that immediate action is taken when weaknesses are detected. It should also reduce the interdependence of financial institutions and governments(Dombret, 2013).

Following the crisis, the financial landscape was transformed and new trends have emerged. European central banks and governments have become more involved in the financial markets to reduce the probability of longer recessions (El-Rian, 2011). The sovereign debt crisis has clearly revealed banks' inefficiency to identify and measure the various types of risk they face. Therefore, the financial institutions have been working on strengthening their risk management divisions to respond appropriately to future crises (Dombret, 2013). Moreover, several banks have downsized their investment banking divisions to concentrate on their core operations. Their lending standards have increased to comply with the new regulations, making it more difficult for individuals and companies to access credit. Consequently, private equity firms, which comply with softer regulatory requirements, have been entering the lending market (Tett, 2014).

## VII. CONCLUSION

This essay identified inefficient regulations, budget deficits, and vulnerable banking systems as the main causes of the European sovereign debt crisis, which initially erupted when it became public knowledge that Greece faced default. The crisis led to soaring volatility within the financial markets and contributed to the revaluation of risks. Moreover, financial institutions faced liquidity issues and the need of financial restructuring. In response to the crisis, several measures were implemented to stabilize the weakening Eurozone economy. As a result, confidence could be restored; however there are still some economic and fiscal challenges. EU member states have increased their policy coordination after understanding that tougher preventive measures to control budget deficit and bank failures are essential to avoid a repetition of the debt crisis. Furthermore, alternative financial institutions have emerged.

Generating HTML Viewer...

References

26 Cites in Article

L Alderman (2014). Banks Take On European Debt, Despite Underlying Problems.

W Allen,R Moessner (2012). The liquidity consequences of the euro area sovereign crisis.

T Alloway (2013). Credit default swaps run out of road.

Michael Arghyrou,Alexandros Kontonikas (2012). The EMU sovereign-debt crisis: Fundamentals, expectations and contagion.

B Bafa (2014). Bundesamt für Wirtschaft und Ausfuhrkontrolle: Umweltprämie.

(2011). Gowing, Nicholas Keith, (Nik), (born 13 Jan. 1951), Main Presenter, BBC World News, BBC News, 2000–14 (Presenter, 1996–2000); Visiting Professor, King’s College London, since 2014.

Kerstin Bernoth,Jürgen Von Hagen,Ludger Schuknecht (2012). Sovereign risk premiums in the European government bond market.

A Choudhury,E Logutenkova,A Kirchfeld (2012). Investment Bankers Face Termination as Europe Fees Fall.

(2013). Financial Sector Assessment Program : Nigeria - Crisis Management and Crisis Preparedness Frameworks.

Dw,De (2012). Greek creditors receive official 'haircut' notification.

Ecb (2014). ECB: Banking Supervision.

(2011). Financial Inclusion Data: Assessing the Landscape and Country-level Target Approaches.

Giorgio Basevi,Carlo D’adda (2014). Overview: Analytics of the Euro Area Crisis.

J Ewing (2012). African Financial Sectors and the European Debt Crisis : Will Trouble Blow across the Sahara?.

(2007). 3 The International Monetary Fund (IMF).

Philip Lane (2012). The European Sovereign Debt Crisis.

André Lucas,Bernd Schwaab,Xin Zhang (2013). Conditional Euro Area Sovereign Default Risk.

H Mcdonald (2013). Ireland becomes first country to exit Eurozone bailout programme.

R Nelson (2013). Sovereign Debt in Advanced Economies: Overview and Issues for Congress.

E Nowotny (2012). Designing a Central Bank.

L Papadimas (2010). The following Biological Psychiatry article in press are now available online in full text at http://www.sobp.org/journal.

Spiegel Online (2013). IMF may stop contributing to Greek bailout.

J Randow (2012). Draghi Says ECB Will Do What's Needed to Preserve Euro: Economy.

G Tett (2014). The real titans of finance are no longer in the banks.

Roberto Frenkel (2014). What Have the Crises in Emerging Markets and the Euro Zone in Common and What Differentiates Them?.

Vighneswara Swamy (2011). EUROZONE SOVEREIGN DEBT CRISIS AND ITS IMPACT ON INDIA'S CROSS-BORDER CREDIT MARKET.

No ethics committee approval was required for this article type.

Data Availability

Not applicable for this article.

How to Cite This Article

afzal ahmad. 2026. \u201cLessons Learned from European Sovereign Debt Crisis\u201d. Global Journal of Management and Business Research - D: Accounting & Auditing GJMBR-D Volume 22 (GJMBR Volume 22 Issue D2).

Explore published articles in an immersive Augmented Reality environment. Our platform converts research papers into interactive 3D books, allowing readers to view and interact with content using AR and VR compatible devices.

Your published article is automatically converted into a realistic 3D book. Flip through pages and read research papers in a more engaging and interactive format.

Our website is actively being updated, and changes may occur frequently. Please clear your browser cache if needed. For feedback or error reporting, please email [email protected]

Thank you for connecting with us. We will respond to you shortly.