## I. INTRODUCTION

The recovery of the Deposit Money Banks (DMBs) loaned funds in Nigeria has remained a challenge. This is evident in the CBN report, which confirms that DMBs NPL stood at a threshold contrary to the statutory acceptable minimum (National Bureau of Statistics (NBS), 2021). This development has a negative ripple effect on the efficiency of operation and real profitability of the banking industry in Nigeria. According to a Moody report in 2019, when bank debtors fail to honour credit agreements, it has serious attendant consequences for the creditor (DMBs) and the economy as a whole. The fallout on this issue of NPL is that DMBs have become risk-averse and are against actively providing funds to businesses; they have concentrated on loans recovery.

While Nigerian banks appear to be posting profit growth year on year, this is primarily due to the exchange rate of the Nigerian Naira. Banks' real profitability has been declining in absolute terms and dollar terms. In addition, the recent CBN stress test revealed that banks are carrying a lot of bad restructured loans, which will further erode profitability and capital if the prudential guideline is not strictly applied. Statistics Africa in its 2019 ranking of banks in Africa further lent credence to the weak profitability of Nigerian Deposit Money Banks. Nigeria's most profitable bank, Zenith Bank, was ranked eighth in profitability in the report. The $532m recorded by Zenith bank was 23 of South Africa's Standard Bank Group's profit for the period, despite Nigeria being the largest economy in Africa. This indicates a potential problem of how strategies execution influences Nigerian banks. This development raises the question, what is the effect of strategy execution on firm profitability of DMBs in Lagos State, Nigeria?

Achieving significant financial performance for organisations in an environment characterized by uncertainties and intense competition warrants those organisations to formulate and execute strategies to contend with these business realities. Despite the relevance of strategy execution, a well-thought-out plan without the framework for execution is another failed strategy. The field of strategic management has recorded only a handful of studies (Adetayo, 2018; Auka & Langat, 2016; Bhimavarapu, Kim & Xiong, 2019; De Oliveira, Carneiro & Esteves, 2019; George, Monster, & Walker, 2019; Gumel, 2019; Korkmaz, 2020; Srivastava & Sushil, 2017; Waititu, 2016), applying majorly systematic reviews and cross-sectional survey research approach. Their findings suggested that the interaction between strategy execution factors such as unfolding, communication, structure, control, and high-performance working system on firm profitability remain unclear. Hence, this limits the understanding of the strategy execution-firm profitability link within the context

of empiricism. This gap in the literature is therefore worthy of investigation.

Research in leadership literature has stressed the need to set in motion a definitive leadership philosophy to drive the organization's affairs (Onamusi, 2020). Such a leader defines the work system, defines authority, spells out responsibility, and enhances strategies' development and successful implementation through the established internal organisational frameworks. Given that businesses operate within a constantly changing environment, such unplanned and unanticipated dynamism may create challenges for strategy execution given the time difference between strategy unfolding and execution; as such, it becomes imperative that organisational leadership becomes agile. An agile leader can operate as a contingent internal organisational factor that enhances the organisational capability to thrive under intense and complex market environment and achieve effective strategy unfolding outcomes. Evidence of empirical studies have been written on leadership (Azim, Fan, Uddin, Jilani, & Begum, 2019; Ibrahim & Daniel, 2019; Khattak, Zolin, & Muhammad, 2020; Mahmood, Uddin, & Fan, 2019; Weller, Sus, Evanschitzky, & Wangenheim, 2020; Yue, Men, & Ferguson, 2019; Zuraik & Kelly, 2018), and with a few focusing on the relevance of agile leadership (Akkaya & Tabak, 2020; Joiner, 2019).

Also, scholarly works have addressed the relevance of strategy execution to the organisation (Adetayo, 2018; Agyapong, Zamore, & Mensah, 2019; Auka & Langat, 2016; Bhimavarapu et al., 2019; De Oliveira et al., 2019; George et al., 2019; Gumel, 2019; Korkmaz, 2020; Mailu, Ntale, & Ngui, 2018; Srivastava & Sushil, 2017; Yang, 2019; Zaidi, Zawawi, & Nordin, & Ahnuar, 2018). However, one missing issue from all these studies is how agile leadership enhances the interaction between strategy execution and performance? This creates another gap that necessitates the conduct of this study. Hence, the study raises the question can agile leadership moderate the interaction between strategy execution and firm profitability of selected Deposit Money Banks in Lagos State, Nigeria?

## II. LITERATURE REVIEW

### a) Theoretical basis for the Study

The ADKAR model is considered a widely used goal-oriented change management approach that facilitates the organisational change from the individual perspective. The ADKAR model offers explanations of how successful change can be achieved by enhancing employees within an organisation (Shah, 2014). The central premise upon which the ADKAR theory is built is on the assumption that organisational change is a function of people-change (Adhikari, 2007). Organisations do not change; instead, the people within

The organisation change. When successful change occurs, the individual change matches the stage of organisational change. The ADKAR theory has been a change management model that explains the interactions between strategy execution and performance. It presented the framework to guarantee successful change given that strategy execution is a management change activity.

However, despite the support found in literature about the significance of the ADKAR model to enhance the organisational change process, which enhances organisational performance, the ADKAR model shares its limitation. Shah (2014) stressed that the model missed out on leadership and program management principles to create clarity and provide direction to change. Moreover, it emphasizes internal organisational factors and does not consider external variables that could disrupt the internal organisational change process. Businesses operate not in isolation but with a dynamic, complex, and far-reaching external environment. According to Teece (2014a), dynamic capability represents an "entity's ability to integrate, build, and reconfigure internal and external competencies to address the fast-changing environment." Consequently, the Dynamic capability theory was considered to complement the ADKAR theory in explaining the process of achieving successful strategy execution in a dynamic environment. Overall, given how static the ADKAR theory is, the DCT provided complimentary support and theoretical explanation for the interaction between strategy execution and firm profitability.

### b) Strategy Execution and Firm Profitability

It is imperative that banks consistently achieve significant year-on-year profit to be considered a profitable going concern. While several factors have been considered in the extant literature as enablers of firm profitability, this study considers strategy execution a plausible determinant. It is important to stress that literature on strategy execution or implementation is surprisingly scanty. What is alarming is that despite the attention given to the significance of strategic management in ensuring strategy formulated gets implemented, only a few empirical studies have considered the strategy execution with respect to factors responsible for its success and scanty empirical evidence of the effect of strategy execution on firm profitability let alone on firm profitable. Amongst the few that considered the above objective, Waititu (2016) established that commercial banks listed on Kenya's stock exchange that had significant investment in strategy execution success factors (leadership, structure-role fix, communication-system, & work-specific culture) achieved a substantial increase in profitability on year on year from 2011 to 2016.

In a similar study, Gomera, Chinyamurindi, and Mishi (2018) found a positive and significant relationship between strategy implementation and firm profitability among SMMEs in Buffalo City Municipality. While Gomera et al.'s (2018) finding differs from Waititu's (2016) because the former focused on the financial performance effect of strategy execution, the latter examined the relationship between strategy execution and financial performance. Despite this dissimilarity, and underlining relevance of strategic execution for firm performance can be deduced. In addition, the findings of Gomera et al. (2018) align with related studies (Monday et al., 2015; Siam & Hilman, 2014). Langat and Auka's (2015) and Serra and Kunc (2015) posited that strategy implementation and corporate performance are positive correlates. Also, Siam and Hilman (2014) found that strategic goals achievement and firm profitability are strong correlates; and this suggests why the strategic goals are considered one of the organisational performance measures. Furthermore, some streams of scholars discussed strategy execution with strategy unfolding. For example, Auka and Langat (2016) posited that "strategy unfolding is a management tool used to help the organization to focus its energy, to ensure that the members of the organization are working towards the same goals, to assess and adjust the organization's direction in response to a changing environment." Auka and Langat (2016) corroborated earlier scholars like Siam and Hilman (2014) to position the positive interaction between strategy unfolding processes and financial performance. The findings provide an additional basis for Krisada and Kittisak's (2019) studies.

To buttress the relevance of strategy execution to organization performance, Barrick, Thurgood, Smith, and Courtright (2015) and Gakenia, Katuse, and Kiriri (2017) aver that critical to the achievement of continuous firm performance is the consciousness to execute strategies. Another related study that corroborated the finding of Auka and Langat (2016) and Monday et al. (2015) is Krisada and Kittisak (2019). The pharmaceutical industry in Thailand showed that strategy unfolding and implementation is a critical element that explains significant variation in organisational performance (Krisada & Kittisak, 2019). The strategy execution factors considered in this study such as strategic unfolding (Auka & Langat, 2016), high-performance work system (Chahal, Jyoti, & Rani, 2016; Jeong & Choi, 2016; Zhu, Liu, & Chen, 2018), management communication (Nebo, Nwankwo, & Okonkwo, 2015)), monitoring and evaluation (Sihag & Rijsdijk, 2019), and organisational structure (Dischner, 2015; Onono, 2018) had all been documented to have a significant effect on organisational performance. Consequent to this discussion, this study hypothesizes that: H01: Strategy execution has a significant effect on the firm profitability of quoted DMBs in Lagos State, Nigeria.

### c) The moderating role of Agile Leadership

Leadership permeates the entire organisation's architecture and possesses the capability to enshrine policies and formulate and drive organisational strategies to optimum performance (Onamusi, 2020). The significance of leadership to organisational performance has been investigated in existing literature in different research contexts; small and micro businesses (Dunne, Aaron, McDowell, Urban, & Geho, 2016; Lawal, Ajonbadi, & Otokiti, 2014), software development team (Garcia & Macri, 2020), health science library (Uzohue, Yaya, & Akintayo, 2016), public schools (Anyieni & Areri, 2016; Erniwati, Ramly, & Alam, 2020), and paint manufacturing companies (Onamusi, 2020).

Managing a profitable organization, especially in tough situations, necessitates an agile leadership (Hao & Yazdanifard, 2015), which has a favorable impact on the climate and structure of the organization (Al Bourini et al., 2015; Flanigan et al., 2017; Hao & Yazdanifard, 2015; Obeidat & Tarhini (2016).One leadership mindset considered appropriate for changing environments is agile leadership, which is curved from the agility literature. McPherson (2016) stressed that as individuals progress up the organisational ladder and become leaders, they must develop the capacity to manage changes and uncertainties; this capacity warrants being agile in orientation and acts. Moreover, extant literature buttressed the servant leader attribute of an agile leader by stressing that such leaders work in the interest of the employees, develop their capacity and provide the opportunity to share responsibility and authority. These attributes make agile leadership a suitable approach to handle complexities and the unknown. More so, delivering value, complexity and planning, self-organization, cross-functionality of teams, and fostering collaboration are all regarded essential for an agile leadership attitude.

Hence on the strength of the relevance of agile leadership to organisation progress, this study argues that strategy execution is a challenging management activity that requires an agility leader to succeed. Given the time lag between strategy unfolding and execution and the uncertainties within the firm macro environment, the agile leader will navigate the external organisation challenges and achieve significant strategy execution performance. Besides, Kinyanjui (2015) established that strategic leadership (an attribute of agile leadership) influences strategy execution. To provide additional support for this narrative within the theoretical discussion, the contingency theory of fit-as moderator considers agile leadership a contingent factor to enhance firm profitability. More so, where the effect of the independent variable (strategy execution) on the dependent variable (firm profitability) is influenced by the introduction of a third variable (agile leadership), then a moderation-effect is theoretically established (Onamusi,

Asikhia, & Makinde, 2019). Hence this study hypothesizes that: H02: Agile leadership has a significant moderating effect on the interaction between strategy execution and firm profitability of quoted DMBs in Lagos State, Nigeria.

## III. METHODOLOGY

This study adopted a quantitative method using the survey research design to obtain data and establish the interaction between strategy execution, agile leadership, and firm profitability on DMBs in an emerging economy.

# a) The Study Context, Sampling, and Data

Via a structured questionnaire, this study collected data from the employee at the management level in the DMBs in Lagos State. A total of 69,793 management staff of eleven (11) publicly quoted DMBs in Lagos State, Nigeria (Access Bank Plc, Fidelity Bank, FCMB, Ecobank, Guaranty Trust Bank, United Bank for Africa, Unity, Sterling, Union Bank, WEMA, and Zenith bank) constitute the population of this study. The number was obtained from the bank's human resource office in March 2021. The bank selected are all quoted banks, and they account for more than 72 of the market shares of the banking industry in Nigeria. The appropriate sample size for the above population is 379, based on Krejcie and Morgan's (1970) sample size determination formula.

### b) Measurement of Variables and Data Estimation Technique

The dependent variable in this study is firm profitability, and it reflects DMB's ability to generate earnings over time (Muya & Gathogo, 2016). Firm profitability is measured using a six-point Likert scale, consistent with (Bendig et al., 2019; Asikhia, Makinde, & Onamusi, 2020).

In this study, the independent variable is strategy execution. Extant literature considers strategy execution as an organisation's internal activity that guarantees the actualization of strategic intent (Abdullah, Hamad, Romano, & Faisal, 2017; Ngui & Maina, 2019). In concomitance with the problem discussed in the introduction, this study investigates strategy execution success factors: strategic unfolding, management communication, Organisational structure, monitoring and evaluation (strategic control), and work system. These elements are measured using a Likert-type scale following the procedures of earlier scholars Elbanna, Andrews, and Pollanen (2016). Management communication reflects how management can communicate with employees to enhance employee participation and commitment to work. These elements are measured using a Likert-type scale following the procedures of earlier scholars (Indrasari, Syamsudin, Purnomo, & Yunus, 2019).

Existing literature considers organisational structure a contextual moderator that can determine how the interaction between two variables can be influenced. Using a six-point Likert scale, it is measured as an organismic structure (Wilden et al., 2013; Onamusi, Makinde, & Akinlabi, 2021). Extant literature measures work system as the combination of human resource practices directed at attaining higher organisational performance. The measurement scale was adopted from previously validated measures by Nadeem, Riaz, & Danish (2019). These elements are measured using a Likert-type scale following the procedures of earlier scholars Nadeem, Riaz, & Danish (2019).

Prior studies consider monitoring and evaluation as strategic control activities to actualize strategic plans. These elements are measured using a Likert-type scale following the procedures of earlier scholars (Weibel, Den Hartog, Gillespie, Searle, Six, & Skinner, 2016). Prior empirical studies measure business continuity to reflect the extent to which an organisation can operate on a going concern (Ngo & O'Cass, 2013). These elements are measured using a Likert-type scale following the procedures of earlier scholars Busaibe et al. (2017) and Obikwe (2018)

The moderating variable in this study is agile leadership. It is measured based on leadership's ability to cope with complex environmental issues quickly, cope with being uncomfortable, can ask the right questions, apply values and experience to a range of apparently different business areas. These elements are measured (using a 6-point Likert scale) following the procedures of earlier scholars (McPherson, 2016). This study followed similar measures used by earlier scholars as discussed above.

To test the null hypothesis one, PLS-SEM was adopted using the Smart PLS statistical platform version 3.3.6. The study used the PLS algorithm's command, which is appropriate for predicting effect-relationship, ran the bootstrapping to ascertain the level of significance of the prediction, and ran blindfolding to determine the predictive relevance of the structural model specified. Hence, the issue of 'Goodness of model fit' or lack of model fit does not invalidate the result (predictive power) of the PLS algorithm (Hair et al., 2013; Hair et al., 2017; Henseler & Sarstedt, 2013). The choice of PLS-SEM (via Smart PLS) is because it is a more advanced multivariate analytical technique that performs multiple regression factor analysis and provides a pictorial model of the interactions in a study with the push of one command as against running an isolated analysis using SPSS (Hair, Black, Babin, & Anderson, 2018). In addition, the SmartPLS statistical platform offers a more strict and robust analysis compared with the outcomes of SPSS (Onamusi & Adenekan, 2021).

## IV. RESULT

Validity, Reliability, and Hypotheses Testing

Table 1: Validity and Reliability test for measurement items.

<table><tr><td>Latent Variables</td><td>CA</td><td>CR</td><td>AVE</td></tr><tr><td>Agile Leadership</td><td>0.810</td><td>0.872</td><td>0.583</td></tr><tr><td>Strategy execution</td><td>0.794</td><td>0.836</td><td>0526</td></tr><tr><td>Firm profitability</td><td>0.798</td><td>0.867</td><td>0.620</td></tr></table>

Table 2: Discriminant Validity using Heterotrait-Monotrait Ratio (HTMT)

<table><tr><td>Latent Variables</td><td>ALL</td><td>FPT</td><td>SEN</td></tr><tr><td>Agile Leadership (AOL)</td><td>0.763</td><td></td><td></td></tr><tr><td>Firm profitability (FPT)</td><td>0.660</td><td>0.573</td><td></td></tr><tr><td>Strategy execution (SEN)</td><td>0.366</td><td>0.692</td><td>0.631</td></tr></table>

Table 1 and 2 provide statistical evidence that the research instrument was valid after it meet the threshold of 0.05 for AVE (convergent validity). Likewise, within the acceptable threshold of below 0.9 using the HTMT criterion for discriminant validity. Further analysis revealed that Cronbach Alpha's coefficient are above the 0.70 threshold. Hence, the research instrument used for data collection was certified valid and reliable.

$H_{0}1$: The effect of strategy execution on the firm profitability of selected deposit money banks in Lagos State, Nigeria, is insignificant.

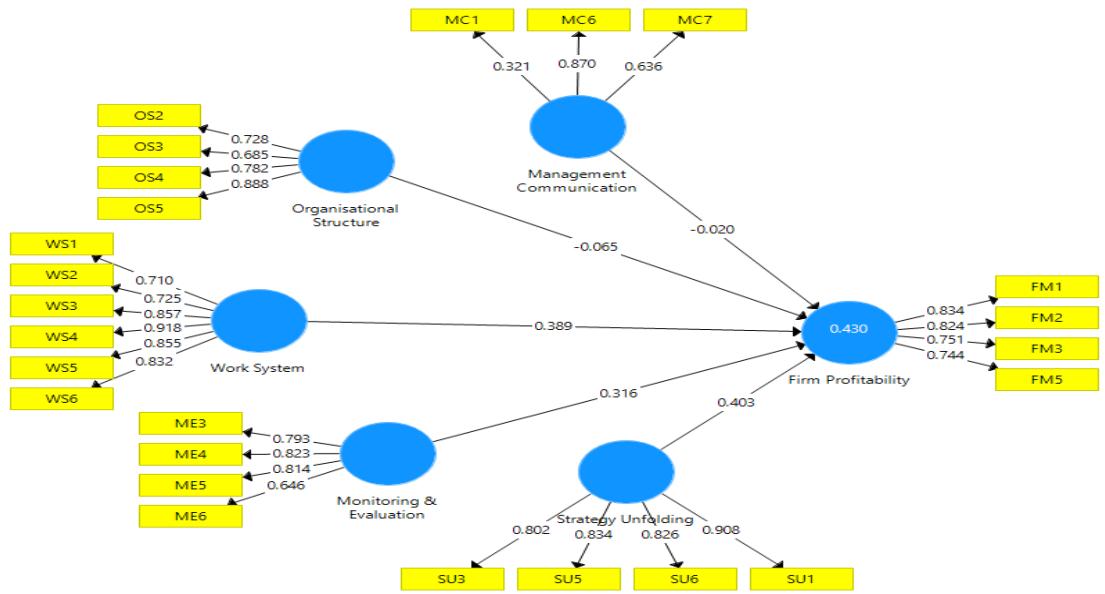

The independent variable strategy execution includes sub-measures such as strategy unfolding, management communication, organisational structure, work system, and monitoring and evaluation, while firm profitability constitutes the dependent variable. Data from four hundred and fifty-two (452) respondents were

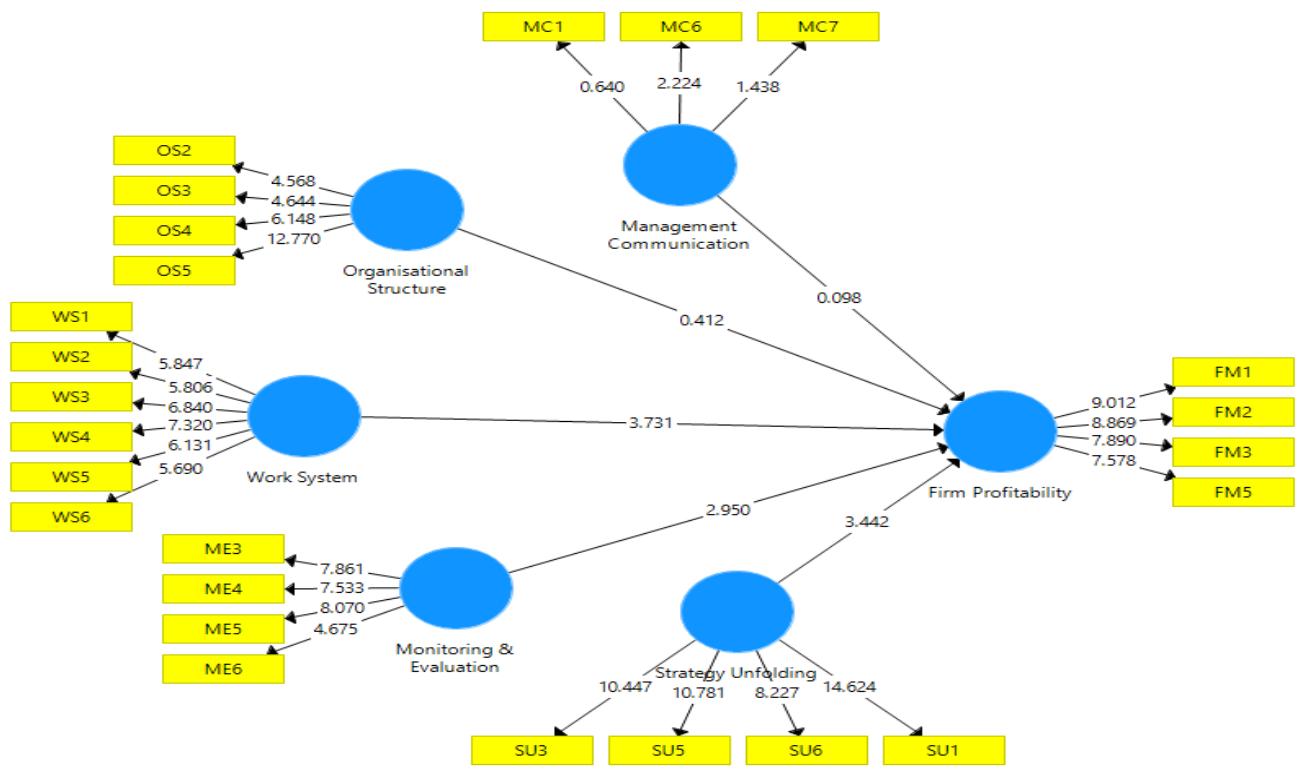

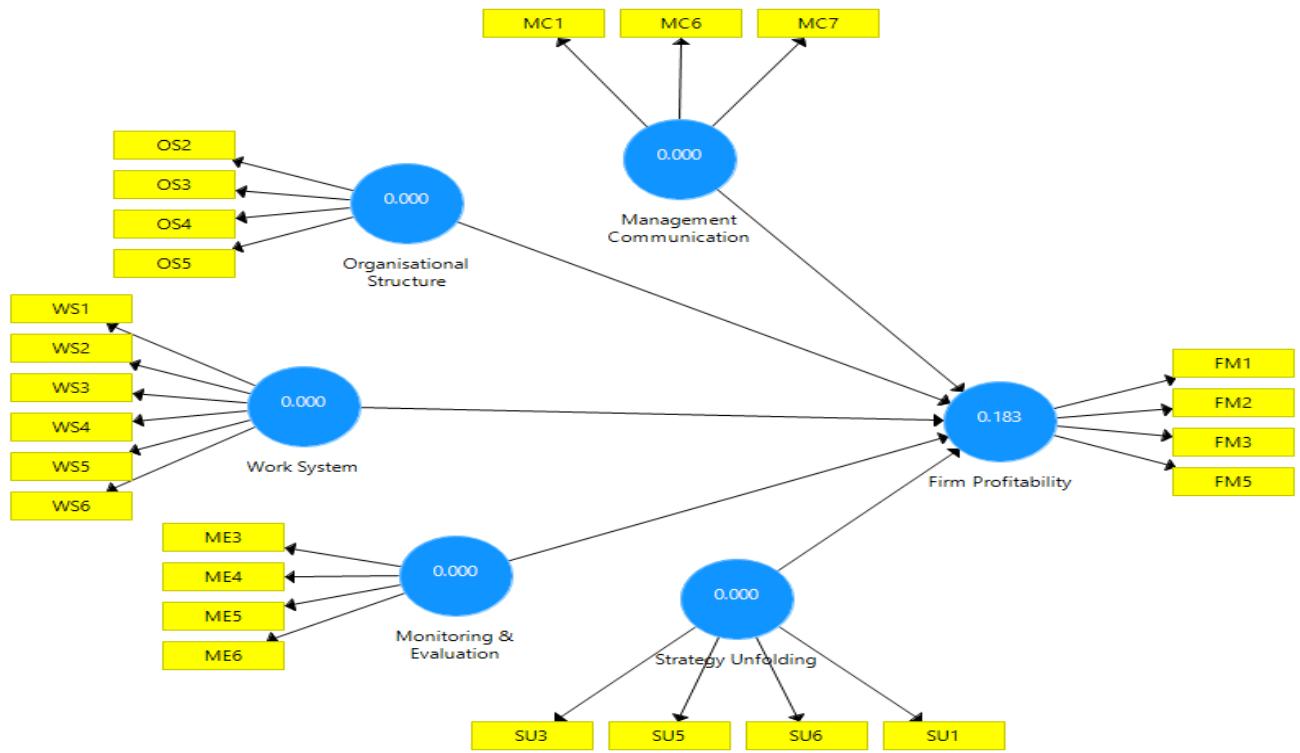

collated for the analysis. The result of the PLS-SEM is presented in three models (see Figures 1, 2 & 3) and a table (see table 3). Figure one shows the path analysis; figure two shows the t values, which confirm the significance of the path analysis and figure three shows $Q^2$, which confirms the predictive relevance of the structural model (t value above 1.96 and $Q^2$ above zero confirm a statistically significant effect and that the structural model specified is relevance). Each model comprised of the outer model, which shows the factor loadings (correlation) of each item in relation to the latent variable, and the inner model termed the structural model (predictive model), which explains the interactions between the independent (strategy execution) variable(s) and the dependent (firm profitability) variable in a study. Table 3 provides a tabular representation of Figures I, 2, and 3.

Figure 1: Path Analysis for Hypothesis One

Figure 2: T-Statistics for Hypothesis One Source: Researcher's Computation via SmartPLS V3.3.6

Table 3: Summary of the PLS-SEM for the effect of Strategy Execution on firm profitability of Quoted DMBs in Lagos State, Nigeria

<table><tr><td>Path Description</td><td>Original sample (o) Unstandardized Beta</td><td>t</td><td>Sig.</td><td>f2</td><td>R2</td><td>Adj.R2</td><td>Sig.</td><td>Q2</td></tr><tr><td>Management communication → Firm profitability</td><td>-0.020</td><td>0.098</td><td>0.922</td><td>0.001</td><td></td><td></td><td></td><td></td></tr><tr><td>Monitoring & Evaluation → Firm profitability</td><td>0.316</td><td>2.950</td><td>0.003</td><td>0.142</td><td>0.430</td><td>0.373</td><td>0.000</td><td>0.183</td></tr><tr><td>Organisational Structure → Firm profitability</td><td>-0.065</td><td>0.412</td><td>0.681</td><td>0.003</td><td></td><td></td><td></td><td></td></tr><tr><td>Strategy Unfolding → Firm profitability</td><td>0.403</td><td>3.442</td><td>0.001</td><td>0.136</td><td></td><td></td><td></td><td></td></tr><tr><td>Work System → Firm profitability</td><td>0.389</td><td>3.731</td><td>0.000</td><td>0.244</td><td></td><td></td><td></td><td></td></tr></table>

Figure 1 presents the results of PLS-SEM analysis for the effect of strategy execution dimensions on firm profitability selected deposit money banks in Lagos State, Nigeria. The Adjusted $R^2$ was used to establish the predictive power of the study's model. From the results, the adjusted coefficient of determination (Adj $R^2$ ) of 0.373 showed that strategy execution dimensions explained $37.3\%$ of the variation in firm profitability DMBs understudy, and the remaining $72.7\%$ variation in firm profitability is explained by other exogenous variables different from strategy execution dimensions considered in this study. The effect is statistically significant at a $95\%$ confidence interval with a p-value less than 0.05. This result suggests that strategy execution influences $37.3\%$ of the firm profitability selected deposit money banks in Lagos State, Nigeria.

The path coefficient of each strategy execution dimension (strategy unfolding, management communication, organisational structure, work system, and monitoring and evaluation) represents the coefficient of determination $(\beta)$ which shows the relative effect of each strategy execution dimensions on firm profitability selected deposit money banks in Lagos State, Nigeria. PLS-SEM results in fig. 1 and 2 revealed that all strategy execution dimensions have positive and significant effects except for management communication and organisational structure with insignificant relative effects. Specifically, the results revealed that at $95\%$ confidence level, monitoring and evaluation $(\beta = 0.320, t = 2.291)$, strategy unfolding $(\beta = 0.403, t = 3.344)$, and work system $(\beta = 0.389, t = 3.731)$ of the quoted DMBs in Lagos State, Nigeria were statistically significant as their p-values were less than 0.05 and their t-values greater than 1.96. However, the relative effect of management communication $(\beta = -0.020, t = 0.098)$ and organisational structure $(\beta = -0.065, t = 0.412)$ has at-value below the acceptable threshold of 1.96 to suggest that the relative effect is

statistically insignificant. Based on the path coefficient, the regression model is restated as follows:

$$

F P = 0. 0 0 + 0. 4 0 3 S U + 0. 3 8 9 W S + 0. 3 2 0 M E - - - - - - (i)

$$

$$

FP = Firm profitability

$$

$$

\mathrm{S U} = \text{Strategyunfolding}

$$

$$

WS = Work system

$$

$$

M E = \text{Montirong and Evaluation}

$$

Further analysis indicates that taking all other independent variables at zero, a unit change in Strategy unfolding holds a potential increase of 0.403 in firm profitability for the quoted DMBs in Lagos State, Nigeria, given that all other factors are held constant. Similarly, the result shows that a unit change in the Work system will lead to a 0.389 increase in firm profitability for the quoted DMBs in Lagos State, Nigeria, given that all other factors are held constant. Lastly, the result shows that a unit change in Work sys Monitoring and Evaluation will lead to a 0.320 increase in firm profitability for the quoted DMBs in Lagos State, Nigeria, given that all other factors are held constant. Overall, from the results, Strategy unfolding had the highest relative effect on firm profitability for the quoted DMBs in Lagos State, Nigeria, with a coefficient of 0.403 and t value of $t = 3.344$. In second place is the Work system with a coefficient of 0.389 and t value of $t = 3.731$. Lastly, monitoring and evaluation with a coefficient of 0.308 and t value of 2.950.

The PLS-SEM offers the opportunity to detect the effect size of the predictor variables (strategy execution dimension) on the outcome variable (firm profitability) using the F-Square $(f^2)$ statistic. Scholars provided thresholds for $f^2$ Values of 0.02, 0.15, and 0.35, representing small, medium, and large effects, respectively (Cohen, 1988, Fasola, Asikhia, Akinlabi, & Makinde, 2020). Table 3 represents the effect size of all strategy execution dimensions on firm profitability of the quoted DMBs in Lagos State, Nigeria. The effect size of strategy unfolding, work system, and monitoring and

evaluation was 0.136, 0.244, and 0.142. Concerning Cohen's $f^2$ criterion, it is safe to say that strategy unfolding and work system have medium effect size while monitoring and evaluation has above medium effect size on firm profitability of the quoted DMBs in Lagos State, Nigeria.

Further analysis was conducted to establish the predictive relevance of the model using the Stone-Gleissner$Q^2$value. Scholars posit that$Q^2$values of 0.02, 0.15, and 0.35 represent small, medium, and large predictive relevance. Hair et al.(2013)suggested that$Q^2$above zero confirms that the structural model specified is relevant. According to Table 3, the$Q^2$value of firm profitability of DMBs in Lagos State, Nigeria, is 0.183. Hence, strategy execution has an above medium degree of predictive relevance regarding firm profitability of DMBs in Lagos State, Nigeria.

Moreover, for this reason, the structural model specified is relevant and has sufficient predictive quality. Based on the strength of the PLS-SEM summarized results in table 3 ( $Adj R^2 = 0.373$, $p = 0.000$, $Q^2 = 0.183$ ), this study can conclude that strategy execution significantly affects the firm profitability of quoted DMBs in Lagos State, Nigeria. Hence, the study accepts the hypothesis one ( $H_{01}$ ), which states that the effect of strategy execution on firm profitability of selected deposit money banks in Lagos State, Nigeria, is significant.

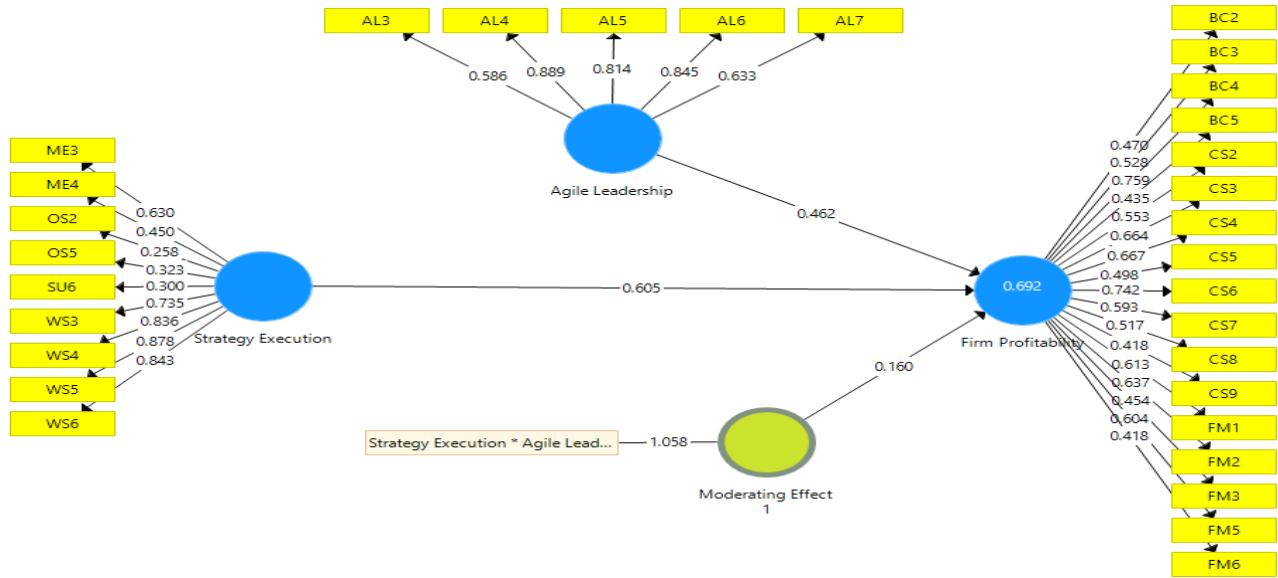

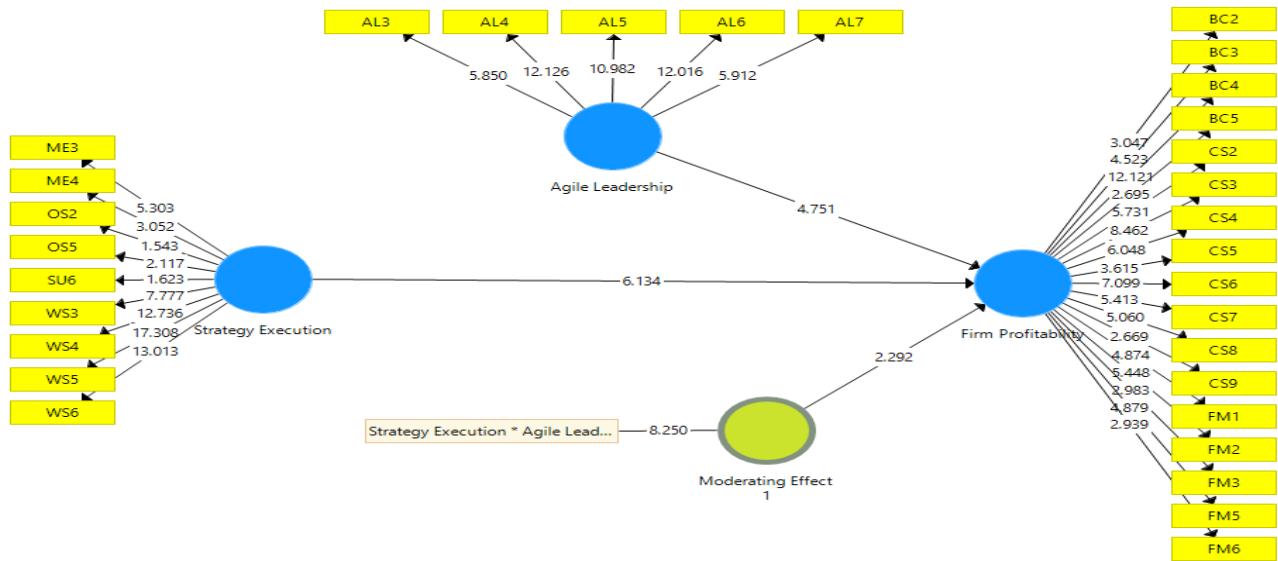

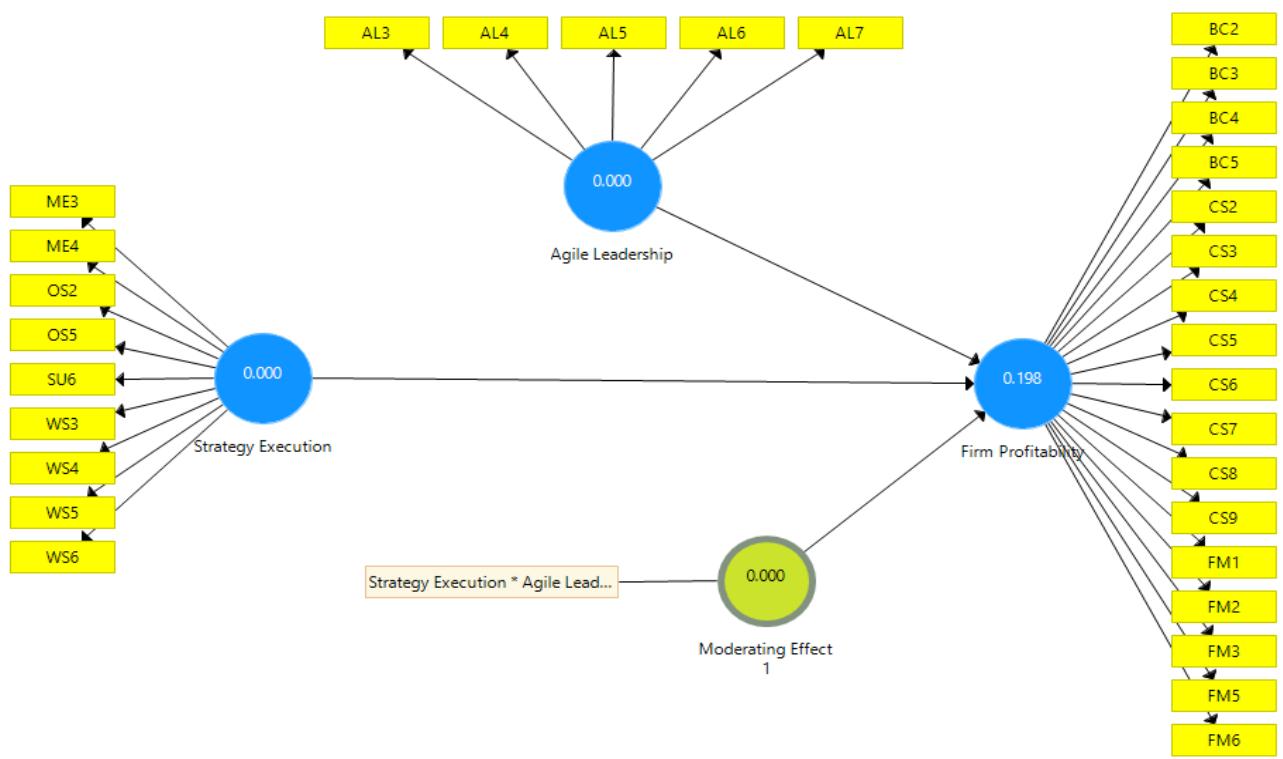

$H_{0}2$: Agile leadership significantly affects the interaction between strategy execution and firm profitability of quoted DMBs in Lagos State, Nigeria.

Figure 3: $\mathbf{Q}^2$ Statistics for Hypothesis One

Figure 1: Path Analysis for Hypothesis Two

Figure 2: T-Statistics for Hypothesis Two

Figure 3: $\mathbf{Q}^2$ Statistics for Hypothesis Two

Tables 4: Summary of moderated analysis for moderating effect of agile leadership on the interaction between strategy execution and firm profitability in Southwest Nigeria using PLS-SEM

<table><tr><td>Path Description</td><td>Original sample (o) Unstandardized Beta</td><td>Sample Mean</td><td>Standard Deviation</td><td>t</td><td>Sig.</td><td>Q2</td></tr><tr><td>Agile Leadership →Firm profitability</td><td>0.464</td><td>0.467</td><td>0.088</td><td>5.242</td><td>0.000</td><td></td></tr><tr><td>Strategy Execution →Firm profitability</td><td>0.604</td><td>0.600</td><td>0.094</td><td>6.442</td><td>0.000</td><td>0.198</td></tr><tr><td>Moderating Effect →Firm profitability</td><td>0.160</td><td>0.152</td><td>0.074</td><td>2.172</td><td>0.030</td><td></td></tr></table>

Figures 4, 5, and 6 present the results of PLS-SEM analysis for the moderating effect of agile leadership on the interaction between strategy execution and firm profitability of quoted DMBs in Lagos State, Nigeria. To establish the moderating effect in a PLS-SEM warrants the creation of a new variable termed strategy execution\*agile leadership. This interaction term's influence is examined on the dependent variable (firm profitability), and a significant moderating effect is established if the coefficient of the interaction term has a p-value less than 0.05. It is noteworthy that in moderation PLS-SEM analysis, emphasis is on the moderating path result and with less attention to Adj $R^2$ or the $R^2$ coefficient found in SPSS output for moderation analysis.

The result in Figures 4, 5, and 6 shows that the interaction term of strategy execution\*agile leadership has a path coefficient of determination value of 0.160. This suggests that the introduction of agile leadership has enhanced the effect strategy execution has on firm profitability by 0.160, and this moderating effect is positive and statistically significant at p-value = 0.030. In addition, the SmartPLS provided the Simple Slope Analysis (SSA), which provides additional evidence to reinforce the presence or absence of a moderating effect.

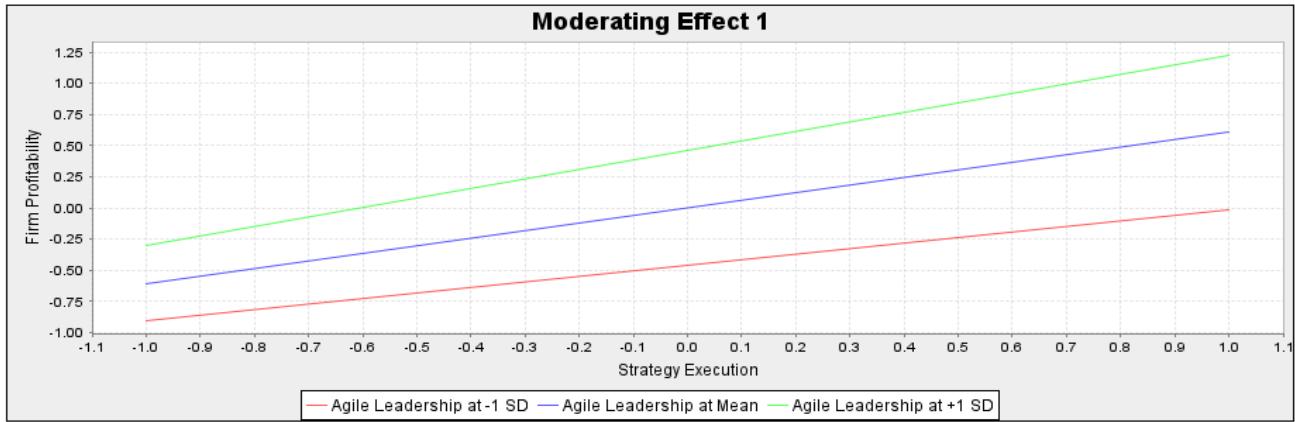

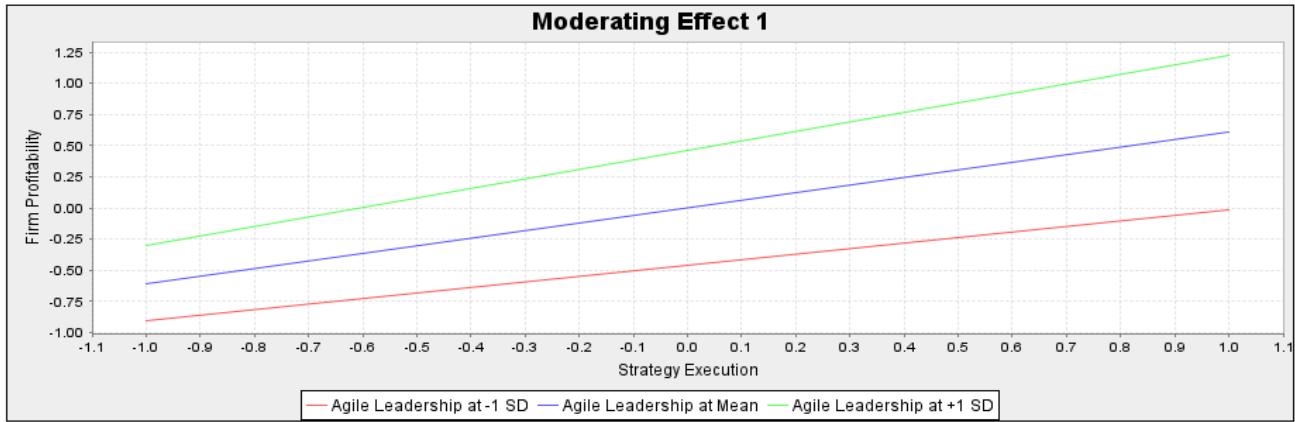

Figure 7: Simple Slope Analysis for the moderating effect of agile leadership

From figure 7, the red line shows low agile leadership at one standard deviation below the mean; the blue line shows agile leadership at mean, which indicates common effect without the moderation effect, and the green shows high agile leadership at one standard deviation above the mean, and it reflects the moderation effect. Hence, the green line above the blue line suggests that DMBs involved in making a high level of agile leadership enhance the strategy execution-performance linkage. It is on the strength of the moderated analysis result $(\beta = 0.160; p < 0.050, Q^2 = 0.198)$ and the Simple Slope Analysis obtained that this study concludes that agile leadership has a positive and significant moderating effect on the interaction between strategy execution and DMBs performance in Lagos State, Nigeria. Hence, the study rejects the null hypothesis two $(H_02)$, which states that agile leadership has no significant moderating effect on the interaction between strategy execution and firm profitability of DMBs in Lagos State, Nigeria.

## V. DISCUSSION AND CONCLUSION

This study reveals that strategy execution holds potential for affecting DMBs profitability. This finding found support in prior studies. Waititu (2016), within Kenya's commercial banks' context, posited that investment in strategy execution success achieved a substantial increase in profitability on a year-on-year basis. In the small business community in Buffalo City Municipality in South Africa, Gomera et al. (2018) revealed that the relationship between strategy implementation and firm profitability is positive and significant. While Gomera et al.'s (2018) finding differs from Waititu's (2016) because the former focused on the financial performance effect of strategy execution, the latter examined the relationship between strategy execution and financial performance. To buttress the relevance of strategy execution to organization performance, Barrick et al. (2015) and Gakenia et al. (2017) aver that strategy execution is a critical influencer of performance in any organization. Another related study that corroborated the finding of Auka and Langat (2016) and Monday et al. (2015) is Krisada and Kittisak (2019).

Supplementary analysis revealed that agile leadership acted as a significant moderating variable because its introduction enhances strategy execution's capacity to influence firm profitability. According to Onamusi (2021), leadership permeates the entire organisation's architecture and possesses the capability to enshrine policies and formulate and drive organisational strategies to optimum performance. The significance of leadership to organisational success has been positioned by prior scholars (Garcia & Macri, 2020; Erniwati, Ramly, & Alam, 2020; Anning-Dorson, 2018) and substantiated by this study.

Hence on the strength of the relevance of agile leadership to organisation progress, this study concludes that strategy execution is a challenging management activity that requires an agile leader to succeed. Given the time lag between strategy unfolding and execution and the uncertainties within the firm macro environment, the agile leader will navigate the external organisation challenges and achieve significant strategy execution performance. To provide additional support for this narrative within the theoretical discussion, the contingency theory of fit-as moderator considers agile leadership a contingent factor to enhance firm profitability. More so, where the effect of the independent variable (strategy execution) on the dependent variable (firm profitability) is influenced by the introduction of a third variable (agile leadership), then a moderation-effect is theoretically established (Onamusi, Asikhia, & Makinde, 2019). It is imperative for the DMBs investigated to ensure that they look into formulating strategies and identify critical factors that can aid its successful implementation. It is equally critical for the management of the DMBs examined to imbibe the agile leadership orientation because such a leadership attribute potentially aid firm profitability.

Generating HTML Viewer...

References

55 Cites in Article

H Abdullah,R Hamad,P Romano,K Faisal (2017). Factors Influencing Implementation of Performance Management Programmes in South African Universities.

A Adetayo (2018). Impact of strategic planning on organisational performance: a study of Unilever Nigeria plc and may & baker Nigeria plc.

H Adhikari (2007). Organisational change models: A comparison.

Ahmed Agyapong,Stephen Zamore,Henry Mensah (2020). Strategy and Performance: Does Environmental Dynamism Matter?.

Bulent Akkaya,A Tabak (2020). Leadership Styles and Organizational Agility Relationship in Science Parks: An Industry 4.0 Perspective.

Al Bourini,F Abu-Rumman,A Alhadid,A (2015). The Impact of Leadership style as a Moderator Variable on the Relationship between Leadership practices and Organisational Performance Analytical Study on Jordanian Commercial Banks.

Thomas Anning-Dorson (2018). Customer involvement capability and service firm performance: The mediating role of innovation.

A Anyieni,D Areri (2016). Assessment of the Factors Influencing the Implementation of Strategic Plans in Secondary Schools in Kenya.

O Asikhia,O Makinde,A Onamusi (2020). Marketing capability and firm performance: Mediating role of new product development and management innovation.

D Auka,J Langat (2016). Effects of strategic planning on performance of medium sized enterprises in Nakuru Town.

M Azim,L Fan,M Uddin,M Jilani,S Begum (2019). Linking transformational leadership with employees' engagement in the creative process.

D Bendig,S Enke,N Thieme,M Brettel (2018). Performance implications of cross-functional coopetition in new product development: The mediating role of organisational learning.

Sasidhar Bhimavarapu,Seong-Young Kim,Jie Xiong (2019). Strategy execution in public sectors: empirical evidence from Belgium.

Leena Busaibe,Sanjay Singh,Syed Ahmad,Sanjaya Gaur (2017). Determinants of organizational innovation: a framework.

H Chahal,J Jyoti,A Rani (2016). The effect of perceived high-performance human resource practices on business performance: Role of organisational learning.

Carla De Oliveira,Jorge Carneiro,Felipe Esteves (2019). Conceptualizing and measuring the “strategy execution” construct.

Simon Dischner (2015). Organizational structure, organizational form, and counterproductive work behavior: A competitive test of the bureaucratic and post-bureaucratic views.

Timothy Dunne,Joshua Aaron,William Mcdowell,David Urban,Patrick Geho (2016). The impact of leadership on small business innovativeness.

Said Elbanna,Rhys Andrews,Raili Pollanen (2016). Strategic Planning and Implementation Success in Public Service Organizations: Evidence from Canada.

S Erniwati,M Ramly,R Alam (2020). Leadership style, organisational culture and job satisfaction at employee performance.

Rod Flanigan,Jacob Bishop,Ben Brachle,Bradley Winn (2017). Leadership and Small Firm Financial Performance: The Moderating Effects of Demographic Characteristics.

C Gakenia,P Katuse,P Kiriri (2017). Influence of Strategy Execution on Academic Performance of National Schools in Kenya.

Fernando Garcia,Rosária Russo (2020). Leadership and Performance of the Software Development Team: Influence of the Type of Project Management.

Bert George,Richard Walker,Joost Monster (2019). Does Strategic Planning Improve Organizational Performance? A Meta‐Analysis.

Shingirai Gomera,Willie Chinyamurindi,Syden Mishi (2018). Relationship between strategic planning and financial performance: The case of small, micro- and medium-scale businesses in the Buffalo City Metropolitan.

Babandi Gumel (2019). The Impact of Strategic Planning on Growth of Small Businesses in Nigeria..

J Hair,G Hult,C Ringle,M Sarstedt (2013). A primer on partial least squares structural equation modeling (PLS-SEM).

J Hair,G Hult,C Ringle,M Sarstedt (2017). A primer on partial least squares structural equation modeling.

J Hair,W Black,B Babin,R Anderson (2018). Multivariate data analysis.

M Hao,R Yazdanifard (2015). How effective leadership can facilitate change in organisations through improvement and innovation.

Jörg Henseler,Christian Ringle,Marko Sarstedt (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling.

A ibrahim,C Daniel (2019). Impact of leadership on organisational performance.

M Indrasari,N Syamsudin,R Purnomo,E Yunus (2019). Compensation, organisational communication, and career path as determinants of employee performance improvement.

D Jeong,M Choi (2016). The impact of highperformance work systems on rm performance: The moderating effects of the human resource function's influence.

B Joiner (2019). Leadership agility for organisational agility.

Mohammad Khattak,Roxanne Zolin,Noor Muhammad (2020). Linking transformational leadership and continuous improvement.

Joan Oracha,Martin Ogutu,Peter K’obonyo,Medina Twalib (2015). Effect of Competitive Advantage on the Relationship between Strategic Leadership and Performance of International Non-Governmental Organizations in Kenya.

Göksel Korkmaz (2020). The Moderating Effect of Internal Audit in Strategic Planning Implementation Success.

R Krejcie,D Morgan (1970). Determining sample size for research activities.

C Krisada,J Kittisak (2019). Effect of strategic planning process on performance of pharmaceutical manufacturing SMEs in Thailand with moderating role of competitive intensity.

Karel Skokan,Adam Pawliczek,Radomir Piszczur (2015). Strategic Planning and Business Performance of Micro, Small and Medium-Sized Enterprises.

A Lawal,H Ajonbadi,B Otokiti (2014). Leadership and organisational performance in the Nigeria small and medium enterprises (SMEs).

M Mahmood,M Uddin,L Fan (2019). The influence of transformational leadership on employees' creative process engagement: A multilevel analysis.

R Mailu,J Ntale,T Ngui (2018). Strategy implementation and organisational performance in the pharmaceutical industry in Kenya.

Blair Mcpherson (2016). Agile, adaptive leaders.

J Monday,G Akinola,P Ologbenla,O Aladeraji (2015). Entrepreneurial Orientation, Economic Factors and Performance of Selected Quoted Consumer Goods Manufacturing Companies in Nigeria: A Combined Effect.

Moody (2019). Nigeria banking performance.

T Muya,G Gathogo (2016). Effect of working capital management on the profitability of manufacturing firms in Nakuru town, Kenya.

Kashif Nadeem,Amir Riaz,Rizwan Danish (2019). Influence of high-performance work system on employee service performance and OCB: the mediating role of resilience.

(2019). Nigeria banking performance.

C Nebo,P Nwankwo,R Okonkwo,F Zaidi,E Zawawi,R Nordin,E Ahnuar (2015). An empirical analysis of strategy implementation process and performance of construction companies.

Chunling Zhu,Anqi Liu,Guoling Chen (2018). High performance work systems and corporate performance: the influence of entrepreneurial orientation and organizational learning.

A Zuraik,L Kelly (2018). The role of CEO transformational leadership and innovation climate in exploration and exploitation.

The Affinity to Execute Strategy could Drive Firm Profitability. Is this True? What Role Does Anagile Leader Play?.

No ethics committee approval was required for this article type.

Data Availability

Not applicable for this article.

How to Cite This Article

Onamusi Abiodun. 2026. \u201cThe Affinity to Execute Strategy Could Drive Firm Profitability. Is This True? What Role Does an Agile Leader Play?\u201d. Global Journal of Management and Business Research - A: Administration & Management GJMBR-A Volume 22 (GJMBR Volume 22 Issue A5).

Explore published articles in an immersive Augmented Reality environment. Our platform converts research papers into interactive 3D books, allowing readers to view and interact with content using AR and VR compatible devices.

Your published article is automatically converted into a realistic 3D book. Flip through pages and read research papers in a more engaging and interactive format.

Our website is actively being updated, and changes may occur frequently. Please clear your browser cache if needed. For feedback or error reporting, please email [email protected]

Thank you for connecting with us. We will respond to you shortly.