The back bone of every economy is the private informal sector (SMEs) and most employment opportunities in Zambia largely focus on small and medium scale enterprises. Hence the contributions the sector makes to economic growth and development through job creation and can’t be overemphasized. However, SMEs were almost dismissed form the formal financial sector in Zambia. The small and medium scale enterprises face difficulties in accessing the financial opportunities, enterprise development skills, face unfavourable regulatory bottlenecks and inappropriate market structures and these therefore, poses serious restriction to their growth and development in the economy. When microfinance was properly harnessed, could make significant contributions to the economic growth and development because it promotes higher investments leading to economic empowerment which in turn promotes confidence, self-esteem, and build capabilities, particularly for the vulnerable majority. In other words, it creates access to productive capital for the poor and subsequently reduces poverty.

## I. INTRODUCTION

Microfinancing has becomes a credible and effective instrument for poverty alleviation and as such, its contributions to economic growth cannot be overemphasized. (Akinyemi, cited in Onuba 2008) The financing of small and medium scale enterprises are vital instruments for poverty alleviation in society. Therefore, SMEs play a crucial role in national building, and providing them with needed facilities would assist in bridging the gap between the rich and the poor. (Onuba 2008). The available information from the Registrar of patent and Companies department indicates that about \(40\%\) of the companies registered are micro, small and medium enterprises (SMEs). This target group has been identified as the catalyst for economic growth of the country as they are the major sources income and employment. The Ministry of Small and Medium Enterprises had in 2022 estimated that the Zambian private sector consists of approximately 70,000 registered Limited companies and 10,000 registered partnerships. Therefore, the need to provide secure source of financing for the sector can't be overstressed. Since Zambia attained a mickle income status with per capita of at least US\(1,000 by the year 2019, led by the vibrant private sector, within a decentralized democratic environment in which the country's was growing the economy or increasing the market value of all the final goods and services produced in the country in (GDP) by \(6 - 8\%\) every year. The main goal of Zambia's Growth and Poverty Reduction Strategy (ZGPRS) was to "sustainable economic growth, accelerated poverty reduction and the protection of the vulnerable and excluded within a decentralized, democratic environment. The intention was to eliminate the widespread poverty and growing income inequality, especially among the productive poor who constitute the majority of the working population".

The microfinance is that part of the financial sector which comprises of formal and informal financial institutions, small and large, that provide small sized financial services to all segments of the population, in rural and urban areas. These institutions cover a array ranging from indigenous rotating savings and credit associations, self-help groups, financial cooperatives, rural banks and commercial banks. The Zambian government supported these institutions in order to create the much needed jobs for the youths and improve their integration in the developing financial sector. The 2006 Nobel peace prize for Muhammed Yunus and the Grameen bank, stood as the proof that microfinance had become the hottest idea for solving the problem of poverty.

According to king and Levine (1993), there seemed to be a positive relationship between the size of the financial sector and economic growth. Access to credit by both individuals and business houses, have been positively associated with asset growth, investment and overall economic growth. Microfinance offered the following services basic financial services such as loans, savings, money transfer services, micro insurance etc. The products help the people to run their businesses, build assets, smooth consumption and manage risks. The poor people in the communities address their financial needs through variety of informal relationships. The credit is always available from informal money lenders at a higher cost to borrowers (CGAP, 2006) The savings services available through a variety of informal relationships like savings clubs, rotating savings and credit associations and other mutual savings societies in local language called village banking. Although these clubs tend to be erratic and somewhat insecure. Traditionally, banks have not considered poor people to be viable market, rendering the SME sector to continue experiencing difficulties in accessing financial services. The SMEs don't have adequate know how information and research and development to innovate and remain competitive. Their limited international market exposure, low product quality, default in compliance with standards, and little access to international partnerships impede SMEs participation into global markets (BDSF, 2008). In addition, insufficient distribution channels often dominated by large firms also make difficult for SMEs to access financial markets. For now, there is an established, yet growing recognition of the importance of micro, small and medium scale enterprise (MSMEs) in sustained national economic growth, therefore little attention has been given to that sector of the economy.

## II. BENEFITS MICROFINANCEPRODUCTS AND SERVICES TO CHAZANGA COMPOUND

### a) Employment

When the entrepreneurs borrow, they create employment or opportunities for others. An increase in the employment benefits the local economy as the money circulates through local businesses and services in Chazanga compound.

### b) Improvement of Businesses

The provision of microfinance products and services in the compound has greatly helped the businesses to upscale their business operations by offering immediate financial resources and capital accumulation.

### c) Reduction of Early Marriages in the Compound

When the economically weaker families have access to credit at an affordable rate, the girl children in the community will be able to receive formal education and reduce the chances of early marriages and teen pregnancies in the compound, thereby increase their chances of completing school would increase and hence more likely to obtain a fair paying job or higher education.

### d) An Opportunity to Receive Education

The children of the economically weaker families' miss education days due to agricultural activities and selling at the market so that they can earn help the family financially. Therefore, microfinance product and services aid such children by providing the funds to meet the financial needs of the families. That would give the opportunity to the children to complete their education.

### e) Help in Reducing High Rate of Alcohol Consumption and Abuse

Most compounds in Lusaka are densely populated, lack social amenities, clean drinking water and don't have enough entertainment ventures, so the source of entertainment for the youths is engaging in illicit activities like beer drinking, prostitution, criminal activities and smoking dagga. The microfinance companies provide the small loans to businesses in such localities, most of the youths will have something to do or will be employed by most of the entrepreneurs enabling them to stay away from illicit activities and alcohol consumption.

# f) The Possibility of Future Investments Increase

Poverty is a perpetual cycle. The scarcity of money results in lack of food and water, leading to lack of sanitary living conditions and malnutrition and illness. The microfinance products and services break this cycle by making more money available. Once the basic needs are met in the compounds, the people would think of the possibility of future investments because the people meet their basic needs.

## III. FINDINGS

This part of the article presents the actual findings from the field work, analysis and discussion of data presented in both qualitative and quantitative status. The results were based on the study which was conducted in Chazanga compound of Lusaka urban district.

During the research expedition, the main aim was to establish the benefits the SMEs derive from microfinancing on small businesses, growth, expansion and survival in Chazanga compound of Lusaka urban District. In the findings, it was learnt that the survival of the SMEs depended largely on whether the enterprises were able to generate the profits from the use of micro funds and easy access to micro credit. That was evidenced by all the SMEs who obtained microloans doing well and expanding their businesses.

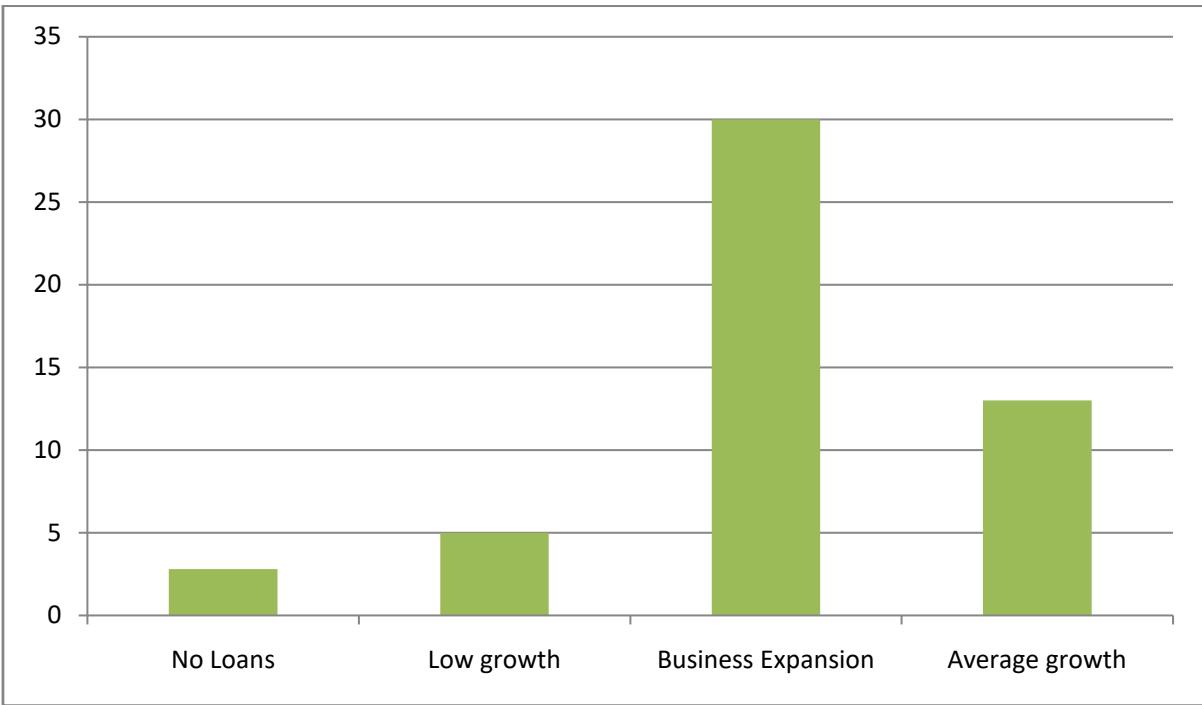

Figure 1.0: Bar Graph Showing SMEs Level of Satisfaction on the Benefits of Microfinancing

Source: Field Study 2022, Business Performance After Acquiring the Loan

The bar graph above, showed 30 entrepreneurs expressed satisfaction with the performance of the loans and that their businesses grew, expanded and were sustainable translating to $60\%$. The entrepreneurs extolled and commended the microfinance institutions as the tool which helped government to reduce poverty levels in the compound. 20 entrepreneurs stated that their businesses experienced average growth and were able to reach the break even point after getting the loans form the microfinance companies, this number translated to $20\%$. 15 entrepreneurs experienced low growth rate translating to $15\%$ but were still optimistic that their businesses would be pick one day while 5 entrepreneurs who never obtained any loans were still struggling with the business representing $5\%$. The majority of the people who had the opportunity to access the financial support implemented it in the businesses which pushed them out of the dependence syndrome and were then living far above the poverty datum line in the compound. They further listed the other benefits as development of skills, improvements in the customer services, high sales growth and expansion of customer base which in turn improved the income flow of the businesses.

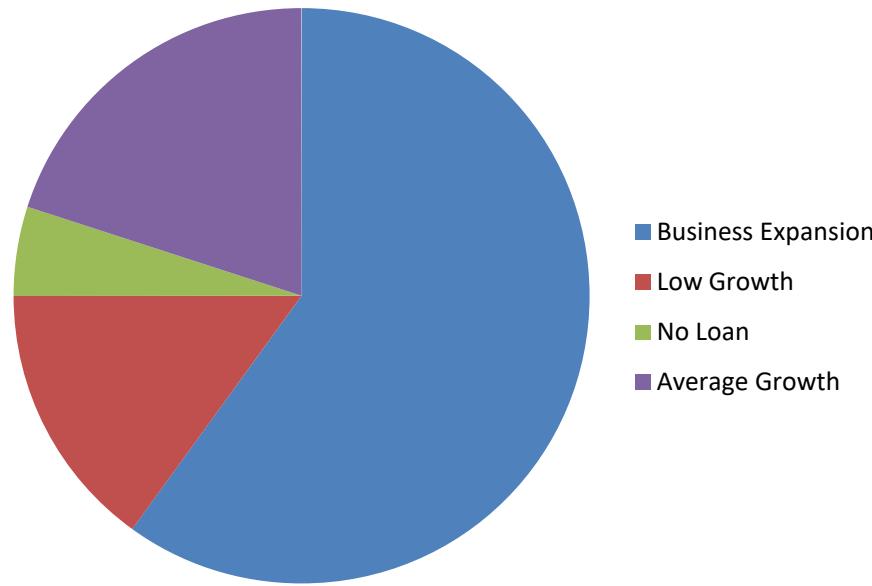

Level of Satisfaction

Figure 1.1: Pie Chart Showing Level of Satisfaction Derived from the Microloans from Mfis

Source:Author 2022

According to the above pie chart 1.0, showed that $60\%$ of the total number of the small and medium scale entrepreneurs interviewed their businesses picked up, grew and expanded when they received the capital injection in form of loans which were obtained from the existing microfinance institutions in Lusaka. The loans enabled their businesses to grow, expand and remained stable to date. The businessmen and women gave testimonies on drastic reduction of poverty in their families when they obtained the funding from the microfinance companies and that their business productivity was real. $20\%$ of the group which obtained the loans recorded average growth which represented a breakeven point where the business neither made loss nor profit but maintained the working capital. $15\%$ of the entrepreneurs' businesses recorded low growth although the businesses were still running smoothly. According to researcher's observations the businesses had low sales because of the high competition in the market and that their locations were still being developed. The final $5\%$ of the entrepreneurs recorded very low growth because these people feared to get the loans due to loans conditions and requirements of providing the assets as collateral and also feared that they might be arrested if they had failed to pay back the loans.

## IV. CONCLUSION

This study was focused on the benefits the small and medium scale entrepreneurs get from microfinance companies in Chazanga compound. Fifty (50) entrepreneurs were picked randomly in the compound to take part in the research so as to enable the researcher establish the real benefits accrued to their businesses after obtaining the loans in relation to business profitability, poverty alleviation in their families, growth and expansion.

### a) Practical Implications

This study showed that $95\%$ of the small and medium scale entrepreneurs who obtained the loans from microfinance companies their businesses grew and expanded when they received additional capital which was injected in the business in form of loans. The loans enabled their businesses to grow, expand and remained stable. The businessmen and women gave testimonies on drastic reduction of poverty in their families as well when they obtained the funding from the microfinance companies and that their business productivity was real.

The research results also showed a clear picture of the $5\%$ who never obtained the loans from MFIs for fear of losing their assets if they had failed to pay back the loans that their businesses remained stunted because they lacked additional capital to boost their operations.

In summary therefore, access to financial services from microfinance companies in Chazanga compound of Lusaka urban district, helped business growth, expansion, employment creation and reduced poverty for those entrepreneurs who obtained loan products and other services from MFIs. That further enhanced the income of the people and mandated the affordability of some basic necessities of life namely education, shelter, health, good nutrition, clothing and clean piped water reticulation.

### b) Limitations of the Research

This work has some limitations as follows:

1. The research should have been extended to other compounds in Lusaka urban district but was restricted to one (1) compound only due to financial constraints.

2. Some of the SMEs were not so open to share business information for fear of being attacked by the thieves and robbers.

3. The researcher took into consideration the tribal, religious, ethical, traditional and cultural beliefs of the respondents.

4. Some of the entrepreneurs never wanted to share both business and family information until after being paid.

5. The other entrepreneurs were not able to read and write; therefore they had difficulties to answer questions in the questionnaires.

## V. RECOMMENDATIONS FOR FURTHER

### RESEARCH

Recommended further researches should be done on the following areas:

1. The Post Office Microfinance Company which was introduced by the Zambian government in 2012 must be reintroduced to cater for both civil servants and business organizations.

2. Government credit unions should be introduced to enable entrepreneurs embark on the other financial products and services to ease the difficulties in the system and help serve the needs of the poor.

3. Reduction of interest rates; this proved as a deterrent to micro loans acquisition because most of the interest rates were quite high for business organizations.

4. The policies, rules, permits and other regulations on taxes and business registration should be relaxed to make it conducive to foster development of more businesses in Lusaka urban district.

Generating HTML Viewer...

References

7 Cites in Article

H Abraham,I Balogun (2012). Performance of Microfinance Institutions in Nigeria: an appraisal of self-reporting institutions to Mix Market.

Tony Ndakoh (2010). Culture and the performance of Microfinance Institutions (MFIs).

Anne Nørgaard,Jørgensen (2011). the profitability of microfinance institutions and the connection to the yield on the gross portfolio-an empirical analysis.

Anne-Lucie Lafourcade,Jennifer Isern,Patricia Mwangi,Matthew Brown,Mix (2005). Brown, Jennifer Anne, (born 17 Aug. 1969), Headmistress, St Albans High School for Girls, since 2014.

B Anaro (2006). CBN Microfinance will empower the poor and create jobs.

V Bogan,W Johnson,N Mhlanga (2007). Does Capital Structure Affect the Financial Sustainability of Microfinance Institutions?" 7. CGAP Brief.

Christian Kitenge,Moembo Kingdome (2004). Financial and Social Performance of Microfinance Institutions.

No ethics committee approval was required for this article type.

Data Availability

Not applicable for this article.

How to Cite This Article

Francis Daka. 2026. \u201cBenefits SMEs derive from MFIs\u201d. Global Journal of Management and Business Research - B: Economic & Commerce GJMBR-B Volume 23 (GJMBR Volume 23 Issue B1).

Explore published articles in an immersive Augmented Reality environment. Our platform converts research papers into interactive 3D books, allowing readers to view and interact with content using AR and VR compatible devices.

Your published article is automatically converted into a realistic 3D book. Flip through pages and read research papers in a more engaging and interactive format.

Our website is actively being updated, and changes may occur frequently. Please clear your browser cache if needed. For feedback or error reporting, please email [email protected]

Thank you for connecting with us. We will respond to you shortly.