The following article emphases on determining the effects of Management Accounting Practices on Small and Medium sized Enterprises (SME). The SMEs studied in the research belong to the southern part of Bangladesh including Faridpur, Madaripur, Bagherhat, Khulna and Gopalganj. Quantitate research approach has been used and data was collected from 252 SME managers by using a well-structured questionnaire. The sample was selected through random sampling methods. SPSS (Statistical Package for the Social Science), update version was used to analysis the data. The article has introduced multiple regression analysis to identify the relationship between management accounting practices and business performances of an organization. Multiple regressions analysis has been used to measure the impact of the relationship in the research model. The results of regression analysis showed that a positive relationship was exited between management accounting practices and SMEs business performance.

## I. INTRODUCTION

Development of small and medium enterprises (SMEs) is envisaged as a key element in this development strategy. For achieving double digit growth in manufacturing, matching development of SMEs is considered critical. Enhanced micro, small and medium enterprise activities in the rural and backward regions constitute a key component of the strategy for rural development and reduction of poverty and regional disparity (Bakht & Basher, 2015)

Small and Medium Enterprises (SMEs) are treated as the engines of growth and drivers of innovation worldwide. They play a significant role in driving economic growth and generating jobs. In Bangladesh, the sector is actually changing the face of the economy. SMEs are playing a vital role for the country's accelerated industrialization and economic growth, employment generation and reducing poverty. SMEs now occupy an important position in the national economy. They account for about 45 percent of manufacturing value addition, about 80 percent of industrial employment, about 90 percent of total industrial units and about 25 percent of the labor force. Their total contribution to export earnings varies from 75 percent to 80 percent. The industrial sector makes up 31 percent of the country's gross domestic product (GDP), most of which is coming from SMEs (Muhammad & AlAmin, 2022).

SMEs play an important role for the national economy and world economy by creating employment opportunity and value added backing to innovation. SMEs are dominant to the efforts to attain environmental sustainably and more comprehensive growth (Eniola & Ektebang, 2014). Small and Medium Enterprise (SMEs) play an important role in any economy through generation of employments contributing to growth of GDP, embarking on innovations and stimulating of other economic activities (Gamage, 2003).

Small and medium business in Bangladesh has a resilient position which is treated as the backbone of the national economy. The role of SMEs is immense to alleviate poverty from the country. By extending SME with a lower investment can provide huge employment opportunity for the densely populated countries like Bangladesh. SME are expected to create jobs, reduce poverty and drive robust national economy (Alauddin & Chowdhury, 2015).

Small and Medium Enterprise (SME) are treated as the engines of growth and drivers of innovation worldwide. SME play a vital role in driving economic growth and generating jobs. In Bangladesh, the sector is truly shifting the face of the economy. SMEs have an impact for country's accelerated industrialization and economic growth, employment generation and reducing poverty. SMEs now occupy an important position in the national economy, they account for about 45 percent of manufacturing value addition, about 80 percent of industrial employment, about 90 percent of total industrial units and about 25 percent of the labor force.

Their total contribution to export earnings varies from 75 percent to 80 percent. The industrial sector makes up 31 percent of the country's gross domestic product (GDP), most of which is coming from SMEs (Bakht, 1998).

## II. LITERATURE REVIEW

Mbogo (2011) conduct a study on the impact of managerial accounting skill on the success and growth of SMEs & Medium enterprises in Kenya. The paper use census research design and collect 31 responses by giving a self-administered questionnaire to all participants. The result of the research concluded that manager's capabilities in management accounting and training level have a significant strong positive relation with the SMEs performance and decision making therefore influence the success and growth of SMEs.

Another study conducted by Ahmad (2012) on the role and use of management accounting practices in Malaysian SMEs. The study utilized primary data, 160 respondent's responses within 1000 questionnaires distributed in manufacturing sector to Malaysian SMEs. The findings of the study is that the use of budgeting system, costing system and performance evaluation system are significantly higher effect than the decision support system and strategic management accounting. The study conclude that MAPs playing effective roles in the management of Malaysian SMEs and poor management accounting practices is the main cause of failure of SMEs.

Lavia Lopez and Hiebl (2014) mentioned that as SMEs faced challenges for more managerial skill and capital than large organizations, so they need special treatment when the care is about management accounting practices, in the research which is conducted on the use management accounting in small and medium enterprises. The researcher also mentioned that management accounting practices is very inadequate in SMEs and different from large companies.

The first empirical insights on the impact of using a package of traditional and a package of contemporary management accounting practices in the public sector was given by Nuhu (2016) in the study investigated on the relation between organizational change and performance with the use of MAPs. This study covers 740 public sector organizations for data collection based on a distributed mail survey. The paper suggests that the contemporary MAPs plays an effective role rather than traditional MAPs for the increasing performance and staring organizational change.

The effect of using MAPs on the Business performance of SMEs within the Gauteng Province of South Africa was studied by Maziriri and Mapuranga (2017) by using quantitative research design and utilizing primary data collected from 380 SME managers. The paper resulted that MAPs has a positive relation with business performance of SMEs. As per the research though information for decision making has no significant effect on business performance but costing system, budgeting system, performance evaluation system and strategic analysis has a positive effect on business performance.

Alkhajeh & khalid (2018) also studied on the impact of MAPs on SMEs business performance within the Gauteng region of South Africa. The researcher used both primary and secondary data to meet the objectives of the study. This paper concluded that there is a positive relation with MAPs & business performance and it highlighted that with the increased implications of managerial accounting practices Manager can able to confirm a enhanced performance and growth.

To manage and handle the highly competitive business environment organizations need to adopt many changes which is required for meeting the ever changing demand of customers (Ahmad et al., 2013). To manage such environment organizations need to be informed time to time; MAPs provide necessary information and helps to be flexible for adopting changes by motivating behavior and guiding the proper action of the managers (Mitchell & Reid 2000).

Maziriri and Chinomona, (2016) mentioned that for stimulating business performance MAPs has a greater influence because it helps to improve organizations managerial efficiency consequently business performance.

## III. PROBLEM STATEMENT

A significant transformation of the SME sector has taken place in Bangladesh over time with various public and private initiatives. It is estimated that 7.5 million MSMEs (including cottage) constitute a significant component of economic enterprises accounting over $97\%$ of all enterprises in Bangladesh, and the share of SMEs in GDP is estimated at about $25\%$ in an ADB study of 2015 and it may be even more if properly estimated. The government of Bangladesh has taken some initiative towards enhancing and flourishes the SMEs banks disbursed huge loan for the SMEs (Alam, & Ullah, 2006).

In Bangladesh the most of the owners of SMEs are not aware or lack of knowledge to use relevant management accounting tool that will help by providing information. The SMEs are plagued by a lack of business management skills which were hampering the overall activities of SMEs including their operation and making them more competitive in global world. Various study and research article mentioned that these factors are the result of lack of management accounting practices in SMEs. Various literatures focus on the economic importance of SMEs, their techniques for survival, management accounting practices like costing system, budgeting, performance evaluation, and information for decision making, strategic analysis, and business performance (Yeshmin & Hossan, 2011).

SMEs as a failure with low profitability and high risk of default for the inappropriate use of management strategy. This study focuses on the impact of SMEs business performances of MAPs in Bangladesh. It is obligatory that this gap need to be overcome to avoid the failure of SME (Jahur, & Quadir, 2012).

## IV. THEORETICAL FRAMEWORK

Grant & Osanloo (2014) described theoretical framework as one of the most important aspects in the research process though often misunderstood by doctoral candidates. It explains the application of a theory in a dissertation providing also a strong evidence of academic standards and scholastic functions.

A theoretical framework is a foundational review of existing theories that serves as a roadmap for developing the arguments you will use in your own work. Theories are developed by researchers to explain phenomena, draw connections, and make predictions.

developing the arguments you will use in your own work.(October 14, 2015 by Sarah Vinz and Revised on September 14, 2022 by Tegan George)

Most of the research on the need, application and practice of management accounting conducted on the basis of contingency theory, this study is done based on the framework of contingency theory.

## V. CONCEPTUAL MODEL AND HYPOTHESIS DEVELOPMENT

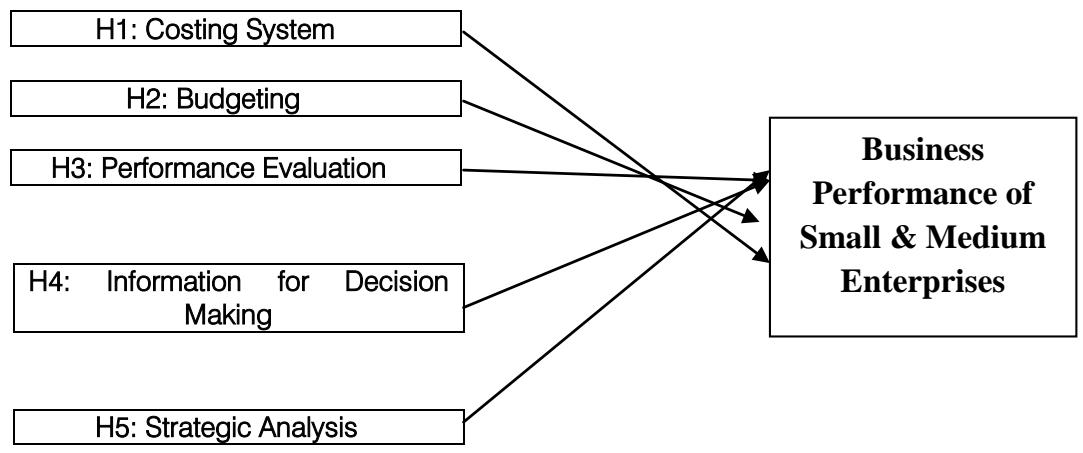

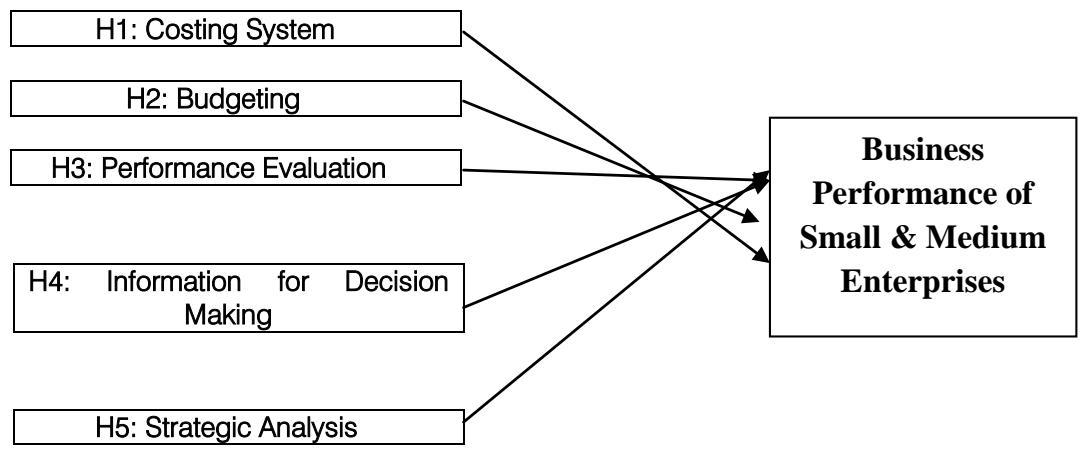

To evaluate how management accounting practice keep impact on business performance of small & medium enterprise, a conceptual model is developed on the basis of reviewed literature on management accounting and business performance. Costing system, budgeting, performance evaluation, information for decision making and strategic analysis are independent variables while business performance of small and medium enterprises is a dependent variable. The hypothesized correlation between independent variables and dependent variable is represented in this conceptualized research model.

Management Accounting Practices Figure 1: Proposed Research Framework

a) Based on the Literature Espoused, the Following Hypothesis has been Formulated

- H1: The costing system positively related with the business performance;

- H2: Budgeting has a positive relation with business performance;

- H3: Performance evaluation positively related with the business performance;

- H4: Information for decision making has a positive relation with the business performance;

- H5: Strategic analysis positive influence the business performance.

## VI. RESEARCH DESIGN AND METHODOLOGY

This paper targeted to conduct survey on trading and manufacturing SMEs (where the service related SMEs was excluded) that were operating in the southern part of Bangladesh. To get a proper response, stratified sampling technique is selected so that the response could ensure an appropriate illustration of every sub sample.

The survey was conducted in SMEs functioning within the Gopalganj region.

After considering sampling cost, dynamism of population, sample group, relevance, accuracy as well as obligatory information for the study, a sample size of 250 was selected for the study.

A well-thought-out and consistent questionnaire was distributed via mail to the owners or the managers or the accountants of each SMEs. The demanded details of the research questionnaire were about business and participants related in the first section. The last section was asking about the dependent variable- business performance and the other remaining section desired details regarding the independent variable- MAPs which include costing system, budgeting, performance evaluation, information for decision making and strategic analysis.

Like art scale was utilized for desiring response where strongly Agree $= 5$ and Strongly Disagree $= 1$.

## VII. RESULTS RELATING TO THE SAMPLE COMPOSITION

To conduct the study a set of questionnaire has been distributed to different retail SME managers and owners in southern part of Bangladesh including Faridpur, Madaripur, Bagherhat, Khulna and Gopalganj five districts. Only 252 questionnaires are usable out of 310 questionnaires distributed. The valid response rate is approximately $81\%$. Table1 show the demographic information of participants of questionnaires.

Table 1: Demographic Information of Participants

<table><tr><td>Gender</td><td>N</td><td>%</td></tr><tr><td>Male</td><td>98</td><td>39</td></tr><tr><td>Female</td><td>154</td><td>61</td></tr><tr><td>Total</td><td>252</td><td>100</td></tr><tr><td>Age Group</td><td>N</td><td>%</td></tr><tr><td>25-35 years</td><td>161</td><td>64</td></tr><tr><td>36-45 years</td><td>66</td><td>26</td></tr><tr><td>46 + years</td><td>25</td><td>10</td></tr><tr><td>Total</td><td>252</td><td>100</td></tr></table>

## VIII. MULTIPLE REGRESSION ANALYSIS

### a) Regression Analysis Results

The table shows that BP has a strong positive correlation with the costing system (0.064), Budgeting

(0.184), performance evaluation (0.337), and strategic analysis (0.424), where it has an weak negative correlation with information for decision making (-0.163)

Table 2: Multiple Regression Analysis: Management Accounting Practices and Business Performance

<table><tr><td>Independent Variable

Management accounting practices</td><td>Standardized Beta</td><td>T (t)</td><td>Sig (p)</td></tr><tr><td>Costing system</td><td>0.064</td><td>1.722</td><td>0.048</td></tr><tr><td>Budgeting</td><td>0.184</td><td>2.235</td><td>0.002</td></tr><tr><td>Performance evaluation</td><td>0.337</td><td>5.412</td><td>0.000</td></tr><tr><td>Information for decision making</td><td>-0.163</td><td>-1.139</td><td>0.001</td></tr><tr><td>Strategic analysis</td><td>0.424</td><td>3.421</td><td>0.011</td></tr><tr><td>R=0.412 Adjusted R2 = 0.424 Significant at the 0.05 level</td><td></td><td></td><td></td></tr></table>

## IX. DISCUSSION

The following analysis determining the effects of management accounting practices on performance of small and medium sized enterprises (SME).

### a) Costing System and Business Performance

The costing system has a result of $\beta = 0.064$, $t = 1.722$ and $p = 0.048$ in the regression analysis. This indicates that the costing system is a statistically significant predictor of business performance. And business performance is positively affected by the costing system. So, the result reveals that an improved costing system emerged as a positive contributor to business performance of SMEs. This statement is justified by Elhamma and Zhang (2013) that revels the performance of SMEs are highly influenced by costing system.

### b) Budgeting and Business Performance

The table shows that Budgeting has a positive impact on business performance with a result of $\beta = 0.184$, $t = 2.235$ and $p = 0.002$ in the regression analysis. This indicates that budgeting is a statistically significant predictor of business performance. The performance of business can be improved through the sound utilization of budgeting. This result was obtained and conducted by Qi (2010) which show the impact of budgeting MAP on SMEs in China.

### c) Performance Evaluation and Business Performance

Performance evaluation appeared as a statistically insignificant predictor of SMEs business

- performance with sig (p) 0.000. Besides It has a result of $\beta = 0.337$ & t= 5.412. This indicates that performance evaluation has significantly influence on business performance. This result is contradicting and acknowledged by Joseph (2015), and Quresh & Hasan (2013).

d) Information for Decision Making and Business Performance

The sig (p) result value depicts that information for decision making is not the statistically most significant predictor of SMEs business performance. It has a result of $\beta = -0.163$, $t = -1.139$ & sig (p) = 0.001. This result shows that business performance of SMEs is not highly influenced by information for decision making. The information for decision making has an impact on business performance. It is more relevant that the decision-making process of small business entrepreneurs is different in decision making, which proves that many current models of strategic decision-making are not suitable for explaining decision-making in small firms (Gilmore and Carson, 2000).

### e) Strategic Analysis and Business Performance

The result of $\beta = 0.424$, $t = 3.421$ and sig (p) $= 0.044$ indicates that an improved strategic analysis system and environment can keep positive contribution to business performance. It's proved that strategic analysis was solidest conjecturer and it has a great impact on business performance. The results of the analysis are supported by Parnell (2013), which showed the strong relationship between MAP and business performance.

## X. CONCLUSION AND IMPLICATIONS OF THE STUDY

This research provides information that influences future research methods and literature by providing information on management accounting. Researchers can use this paper as a reference for future research on this topic. Also this study greatly affects SME business in southern part of Bangladesh by validating management accounting practices costing system, budgeting, performance evaluation, information for decision making, strategic analysis. This study also demonstrates that SMEs that are directly involved in business management accounting practices are growing at a faster pace and have increased business performance. There are theoretical and practical implications of this study. Performance evaluations indicate that there is a strong underlying relationship between the use of management accounting and increased business performance. Just as this study will be useful in the literature of current researchers, it will influence the development of SME business in a developing country like Bangladesh by providing different directions for the practice of management accounting in the future, especially in the southern part of Bangladesh.

Generating HTML Viewer...

References

30 Cites in Article

Zaid Bakht,Debapriya Bhattacharya (2015). Investment, Employment and Value Added in Bangladesh Manufacturing Sector in 1980s: Evidence and Estimate.

M Muhammad,S Al-Amin (2022). Green Management in SMEs of Bangladesh: Present Scenario, Implementation Obstacles and Policy Options.

N Nath (2021). Manufacturing sector of Bangladesh-growth, structure and strategies for future development.

G Myslimi,K Kaçani (2016). Impact of SMEs in economic growth in Albania.

M Alauddin,M Chowdhury (2015). Small and medium enterprise in Bangladesh-Prospects and challenges.

Z Bakht (1998). Growth Potentials of Small and Medium Enterprises: A Review of Eight Sub-sectors in Bangladesh.

Anthony Eniola,Harry Ektebang (2014). SME firms performance in Nigeria: Competitive advantage and its impact.

A Gamage (2003). Small and medium enterprise development in Sri Lanka: a review.

M Alam,M Ullah (2006). SMEs in Bangladesh and their financing: An analysis and some recommendations.

F Yeshmin,M Hossan (2011). Significance of management accounting techniques in decisionmaking: an empirical study on manufacturing organizations in Bangladesh.

M Jahur,S Quadir (2012). Financial distress in small and medium enterprises (SMES) of Bangladesh: Determinants and remedial measures.

Hussain Ahmad,Sayyed Shah,Fatmawati Latada,Muhammad Wahab (2019). Teacher Identity Development in Professional Learning: An Overview of Theoretical Frameworks.

S Vinz (2022). Example Theoretical Synthesis Investigation Outline of.

(2015). Handbook of Urban Educational Leadership.

E Maziriri (2017). The impact of management accounting practices (Maps) on the business performance of small and medium enterprises within the gauteng province of South Africa.

Mahdi Alkhajeh,Azam Abdelhakeem Khalid (2018). Management Accounting Practices (MAPs) Impact on Small and Medium Enterprise Business Performance within the Gauteng Province of South Africa.

Marion Mbogo (2011). Influence of Managerial Accounting Skills on SME’s on the Success and Growth of Small and Medium Enterprises in Kenya..

E Maziriri (2017). The impact of management accounting practices (Maps) on the business performance of small and medium enterprises within the gauteng province of South Africa.

E Maziriri,E Chinomona (2016). Modeling the influence of relationship marketing, green marketing and innovative marketing on the business performance of small, medium and micro enterprises (SMMES).

Kamilah Ahmad,Shafie Mohamed Zabri (2012). Factors explaining the use of management accounting practices in Malaysian medium-sized firms.

N Nuhu,K Baird,R Appuhami (2016). The association between the use of management accounting practices with organizational change and organizational performance.

Oro Lavia López,Martin Hiebl (2015). Management Accounting in Small and Medium-Sized Enterprises: Current Knowledge and Avenues for Further Research.

Mahdi Alkhajeh,Abdelhakeem Azam (2018). The Relationship of Implementing Management Accounting Practices (MAPs) with Performance in Small and Medium Size Enterprises.

Falconer Mitchell,Gavin Reid (2000). Editorial. Problems, challenges and opportunities: the small business as a setting for management accounting research.

John Parnell (2013). Uncertainty, Generic Strategy, Strategic Clarity, and Performance of Retail SMEs in Peru, Argentina, and the United States.

Audrey Gilmore,David Carson (2000). The Demonstration of a Methodology for Assessing SME Decision Making.

Amber Qureshi,Mubashir Hassan (2013). Impact of performance management on the organisational performance: An analytical investigation of the business model of McDonalds.

O Joseph (2015). Effectiveness of performance appraisal as a tool to measure employee productivity in organizations.

Y Qi (2010). The Impact of the Budgetting Process on Performance in Small and Medium-sized Firms in China.

Azzouz Elhamma,Y Zhang (2013). The Impact of Business Strategy on Budgetary Evaluation in Moroccan Firms : An Emprical Study.

No ethics committee approval was required for this article type.

Data Availability

Not applicable for this article.

How to Cite This Article

Md. Faykuzzaman Mia. 2026. \u201cEffects of Management Accounting Practices on SME Performance in Bangladesh: A Study of Southern Region of Bangladesh\u201d. Global Journal of Management and Business Research - D: Accounting & Auditing GJMBR-D Volume 23 (GJMBR Volume 23 Issue D1).

Explore published articles in an immersive Augmented Reality environment. Our platform converts research papers into interactive 3D books, allowing readers to view and interact with content using AR and VR compatible devices.

Your published article is automatically converted into a realistic 3D book. Flip through pages and read research papers in a more engaging and interactive format.

Our website is actively being updated, and changes may occur frequently. Please clear your browser cache if needed. For feedback or error reporting, please email [email protected]

Thank you for connecting with us. We will respond to you shortly.