Nigeria’s balance of payment crisis has been at the heart of its frequent recession and incessant currency devaluation. Hence it is imperative that major economic policies and strategies address this issue. As this paper as showed, if Nigeria could consistently attain overall balance of payment surplus, the naira will be strengthened, and the economy will flourish. Therefore, this paper attempts to demystify Nigeria’s balance of payment deficit while offering recommendations to improve the weak balance of payment. While the structural approach to adjusting balance of payment crisis seems to be the method with lasting economic change, it appears the most difficult to execute.

## I. INTRODUCTION

Balance of payment is a statement of a country's transactions with the rest of the world over a particular period (Lagoarde-Segot, 2023). It has the current account which shows goods and services transaction and the capital account which shows capital movement. Balance of payment is said to be at deficit if import is more than export and if capital outflow is bigger than capital inflow. While it is at surplus if the reverse is the case. Nigeria has often have daunting balance of payment deficit due to its over-reliance on crude oil (Knoema, 2020). According to the World Bank, Nigeria has a negative (15.4 billion and a negative 16.9 billion in current account balance of payment in 2015 and 2020 respectively (The World Bank, n. d.). While balance of payment deficit shows high consumption and perhaps high quality of life, it tells a different story when it becomes unsustainable. Nigeria has dealt with unsustainable balance of payment deficit for a long time. This is evidenced in the frequent IMF loans, frequent naira devaluation, and frequent contractionary monetary policy (Oladipupo, 2011).

In this paper, we shall espouse Nigeria's balance of payment crisis within the framework of the three balance of payment approaches and recommend how Nigeria can better address its balance of payment deficit.

## II. ASSESSING BALANCE OF PAYMENT WITH THE MUNDELL-FLEMING MODEL

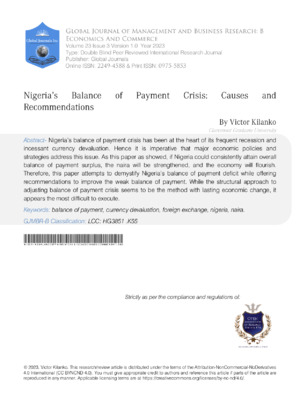

The Mundell-Fleming model also known as the IS/LM/BP model provides economists with a framework to understand and explain the causes of balance of payment problems (Bird, 2014). Let us start with a basic introduction of the model as showed in Figure 1.

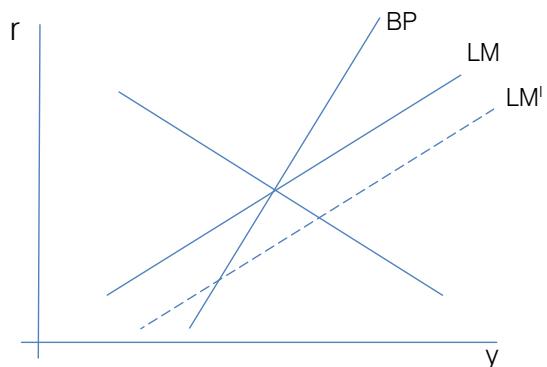

Figure 1: A basic Mundell-Fleming Model

The IS schedule (real economy) shows the combination of the interest rate and income level where planned investment is equal to planned savings (Bird, 2006). It shows real sector equilibrium. It is downward sloping because when interest rate falls, investment increases based on the elasticity of investment to interest rate (Fan & Fan, 2002). Also, when income rises, savings rise based on marginal propensity to save (MPS). It is quite flat because we are assuming that Nigeria's MPS is small, and investment is very elastic to interest rate.

The LM schedule (monetary economy) represents the values of interest rate and income level where the demand for money equals the supply of money. This shows monetary sector equilibrium (Pilbeam, 2013). It is upward sloping because at a certain level of money supply, when income increases, the demand for money as a means of transaction increases and the interest rate also increases as money demand increases (Fan & Fan, 2002). It is steep because we assume that as income rises, the transactional demand for money rises and that there is a steep money supply schedule as money supply is not very elastic to interest rate (at full capacity). Also, we assume Nigeria's money demand isn't very sensitive to interest rate.

From the above set up, there is a huge transactional demand for money and an insensitive money supply. Money supply doesn't necessarily increase with increased interest rates.

Moreover, the BP schedule (balance of payment) represents the export and import. We assume the export as given because it depends on other nations' income level which is beyond Nigeria's control. But import is based on Nigeria's income level. When income increases, import increases based on Nigeria's marginal propensity to import (as an import dependent nation)(Riti, Gubak, & DA Madina, 2016). Hence the BP schedule is upward sloping (Fan & Fan, 2002). If we consider the capital account as well, the capital flow will depend on the elasticity of capital flow to interest rate. We assume that capital flow is insensitive to interest rate as political instability and security threats deter investors, so the BP schedule is quite steep. And if there will be a capital surge at all, the interest rate needs to be very high.

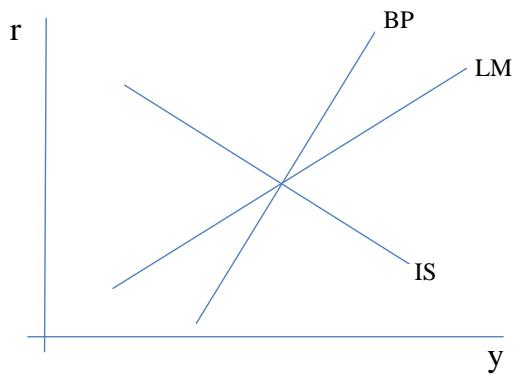

Let us consider how a shift in these schedules will affect balance of payment. If there's an expansionary fiscal policy, IS shifts to $\mathsf{IS}^1$ as showed in figure 2.

Figure 2: A Mundell-Fleming Model Showing a Shift in IS.

The national income increases, and interest rates are pushed up. But as interest rate is still below BP, the economy lacks the required interest rate to bring in enough capital. There will be an overall balance of payment deficit. Also, the steep BP means low capital mobility as many investors do not consider investing in assets in developing economies. However, if Nigeria can fix its capital mobility issues and make the BP schedule to be more flat-like, a surge of capital into the economy will cause balance of payment surplus to compensate for any current account balance of payment deficit (Ezu & Oranefo, 2023). We will discuss how Nigeria can fix its capital mobility issues under the structural approach.

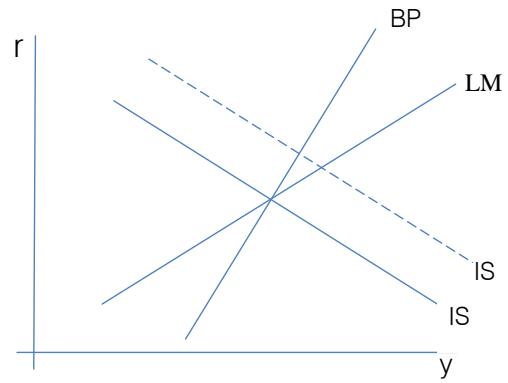

If there was a monetary expansion as showed in figure 3 due to an increase in money supply, interest rates will be pushed down below the BP schedule further than the push of the IS shift. Even though there is higher national income, the economy lacks enough interest rate to attract capital inflow, so there will be an overall balance of payment deficit. Hence, Nigeria really must investigate solving its capital mobility issues.

Figure 3: A Mundell-Fleming Model Showing a Shift in LM

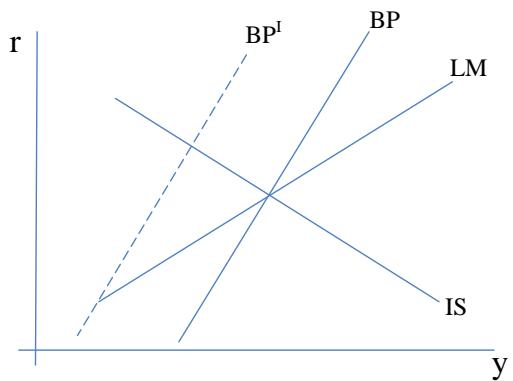

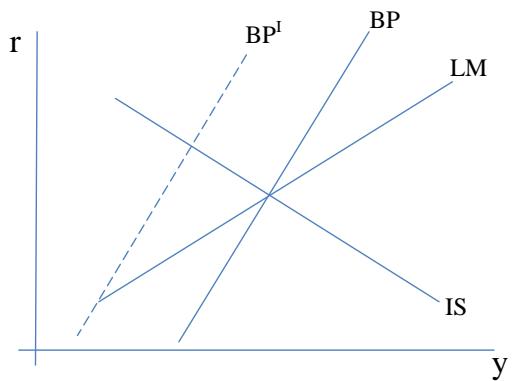

Assuming Nigeria shifts its BP schedule to the right due to increase in political stability or credit worthiness or change in exchange rate as showed in figure 4. The interest rate is above the BP which means that there will be a surge in capital inflow which can compensate for any balance of payment current account deficit and create an overall balance of payment surplus.

Figure 4: A Mundell-Fleming Model Showing a Shift in BP

## III. BALANCE OF PAYMENT THEORIES

There are three balance of payment theories that examine balance of payment problems. They are the absorption approach, the monetary approach, and the structural approach.

### a) The Absorption Approach

The absorption approach focuses mainly on the current account side of the balance of payment- the real sector (IS)(Pilbeam, 2013). If IS shifts to the right due to improved business outlook or increase in the average propensity to consume, or fiscal expansion, national income will increase. This will lead to an increase in import as the aggregate domestic demand is bigger than the aggregate domestic supply or as higher income induces inflation which makes local goods more expensive than imported ones (Lagoarde-Segot, 2023). This will cause a problem in Nigeria's balance of payment because the current account weakens and there is a current account balance of payment deficit.

To view this in Mathematical Expressions:

$Y = C + I + G + X - M$ Equation 1 Where $Y$ = national income

$C =$ consumption

$I =$ investment

$G =$ government spending

$X =$ export

M = import

$S =$ savings

$C + I + G =$ domestic demand

$X - M = Y - (C + I + G)$ Equation 2 And Income (Y) = Consumption (C) + Savings (S). Equation 3

$X - M = (S - I) + (T - G)$ Equation 4 From the above equation 4, a balance of payment current account problem can be due to a public sector or a private sector problem. We have seen above how a shift in the private sector (S - I) due to fiscal changes (shift in T-G) can cause a current account problem.

However, this approach does not recognize the capital/ financial account(Bird, 2006). The model is silent on the effect of interest rate on BP nor on how change in interest rate can induce capital inflow to attain an overall balance of payment equilibrium. As seen in figure 2, a shift in IS will of course create a ripple effect that the model ignores because it didn't talk about capital flow or money. Well, the balance of payment account is beyond the current account. Many scholars have attributed this shortcoming to the era the theory was postulated as there was limited capital mobility, pegged exchange rate, and little monetary independence(Bird, 2014). This is often called the trilemma and countries must meet two of the three conditions (pegged exchange rate, capital mobility, and monetary independence) (Popper, Mandilaras, & Bird, 2013).

This also explains the reason the theory doesn't mention exchange rate. Exchange rate differentials will affect import and export. A devaluation of naira will make export cheaper and import more expensive. For a country largely dependent on import, this will lead to current account balance of payment deficit which this theory ignores.

The key takeaway is that whenever Nigeria's aggregate demand is greater than its aggregate supply, it leads to balance of payment current account deficit.

Normally in a Domestic Monetary Sector Equilibrium:

Money demand (Md) = (Ms) Money supply.

Where $Md = kPY$

$k =$ nominal income coefficient

$P = \text{price level}$

Y = real income And $Ms = D + R$

$D =$ net domestic assets of the banking system

$R =$ international reserves

Let us assume that there is a domestic monetary sector disequilibrium and money supply is higher than money demand. It is also right to assume that there will be higher spending. As this approach integrates both the real sector and monetary sector, we can safely assume that people can spend the excess money in the domestic real sector. When full capacity is reached, price level will go up and our exports will become more expensive. Many people will shift to imported goods because they are cheaper, and this weakens the balance of payment current account and causes a balance of payment deficit problem. This same outcome will result from direct spending in foreign real sector as import quantity goes up than export and the balance of payment current account weakens.

If people chose to spend the excess money supply in the domestic financial market, they can buy government bonds and cause the price to rise with increased demand. This will make the interest rate fall.

$R = Md - D$

Change in $R =$ Change in Md-Change in D.

In real life though, these causes are not always clearly delineated. Expansionary fiscal measures may raise income, cause inflation, increase import, cause balance of payment current account deficit. With the attendant interest rate increase may come high capital inflow. Disequilibrium in the capital account is due to disequilibrium in the current account.

With Nigeria's flexible exchange rate, balance of payment deficit leads to exchange rate devaluation and the fall in the value of Naira as the government tries to discourage import consumption and encourage more export and made-in-Nigeria products' consumption (Ukangwa, Onyenze, & Uke-ejibe, n. d.). Nigeria's To reduce the deficit, the government either dampens demand or raise national aggregate supply. Oftentimes, the government reduces demand which tends to lead to recession.

### b) The Monetary Approach

The monetary approach simply says that any disequilibrium in the balance of payment is due to disequilibrium in the domestic monetary sector (Pilbeam, 2013).

Equation 5

Equation 6

Equation 7 With lower relative interest rate, there will be capital outflow. This weakens the balance of payment capital account. On the other hand, with the fall in interest rate, investment and consumption may increase as business owners and consumers take advantage of lower interest rate to spend more. As aggregate demand rises, inflation sets in when we reach full capacity, and we are back to weak balance of payment current account. Elsewhere, people could have spent their money in the foreign financial market assuming exchange rate doesn't change, and assuming no default or political risks and there's perfect competition. They take advantage of interest rate differentials and capital flows out of the Nigerian economy. Hence, we have balance of payment capital account deficit. The above shows diverse ways the Nigerian balance of payment can have problems and the underlying cause is the shift in the LM schedule due to disequilibrium in money supply or money demand as shown in figure 3.

Equation 8

Equation 9 balance of payment deficit problem, hence, touches every fabric of the economy. A balance of payment surplus would however strengthen the naira. But if we had pegged exchange rate, surplus balance of payment adds to our reserves and deficit balance of payment depletes our reserves. And whenever we can't meet our money demand, we use reserve as shown in equation 9 (Bird, 1981).

There are legitimate criticisms of the monetary approach as it has no mention of the exchange rate. Exchange rate plays a huge role in capital flow and this approach despite its reference to money didn't include the influence of the exchange rate (lyoboyi & Muftau,

2014). Based on the above explanation about excess money demand and a surge in capital inflow, an unstable exchange rate will discourage foreign direct investment and keep the overall balance of payment weakened. Likewise, Nigeria's default risk and high political instability may restrict capital inflow which the model fails to address. Also, disequilibrium in the balance of payment may be the cause of domestic monetary sector disequilibrium. Balance of payment current account deficit may cause higher money supply to try and handle the deficit.

Like monetarists, the monetary approach assumes that money demand is stable (Bird, 2007). The demand for money is unstable. So, expecting to find a domestic monetary sector equilibrium ( $\text{Md} = \text{Ms}$ ) may be challenging.

### c) The Structural Approach: The Houthakker-Magee Effect

The Houthakker-Magee effect points to the fact that countries might just be producing the wrong goods (Bird, 2006). That is, the balance of payment problem is down to not producing the right goods. Wrong goods are classified as goods with low-income elasticity of demand. That is, as income increases the demand for these goods remains low. If a country is producing this kind of goods, its export doesn't increase with income. So, its export remains low, and it is forced to import goods with high income elasticity of demand so the import keeps getting higher. As Nigeria only produces raw materials like agricultural products and crude oil, as the income of her trading partners increases, they don't have a proportionate increase in demand for these goods. Hence, Nigeria's export does not proportionately increase with income over time. On the other side, Nigeria must import goods with high income elasticity of demand as she does not produce them. Goods like technology often have high income elasticity of demand. This makes import higher than export and weakens the balance of payment account.

This phenomenon came because of an experiment by Houthakker and Magee where they realized that countries trading goods with low-income elasticity of demand often have balance of payment current account deficit (Houthakker & Magee, 1969). And it is often suggested that these countries ensure that their growth rate isn't as high as their trading partners'. This helps manage aggregate demand relative to other countries.

Another cause of problem to the balance of payment under the structural approach is when a country has the right goods, but it is in the wrong markets. The wrong market being that it sells in a country with little/no income growth. So, if Nigerian goods have high income elasticity of demand but the income of our trading partners (countries) is somewhat stagnant, Nigeria's export would be somewhat stagnant also while her import increases because she must meet her increased aggregate demand. As import is greater than export, balance of payment current account weakens.

Moreover, another element of the structural approach is when we have the right goods and the right markets, but our production is inefficient. If our competition is advanced countries with better production and more productivity (lower unit cost of production), they can charge lower prices, reinvest their profits into research and development, and lower prices even more while they raise quality. We (with our inefficient production and higher unit cost of production) can't compete with this. If we choose to match their prices, our profits will be too low that we can't reinvest profit to make improvements on our products and production. If we choose to charge higher prices, we will be priced out of the market. Either way, our balance of payment is weakened as our export is pushed low and import remains high. This is the conundrum most underdeveloped countries find themselves. The inefficiency might be perpetuated by poor infrastructure (education, health, human capital, physical infrastructure), little access to capital or just political reasons. In all of these, our investment in productivity is greatly affected and our international competitiveness is hindered. As imports remain higher than exports, balance of payment current account is weakened.

## IV. DISCUSSION AND RECOMMENDATION

The structural approach makes the case for a diversified Nigerian economy focused on manufactured goods with high income elasticity of demand. The more reason why Nigerian creative sector and technology sector should be supported as they tend to produce goods whose demands increase with income (Bird, 1983). When done well, the structural approach will shift the BP schedule below the interest rate to create an insurge flow of capital into Nigeria due to political stability, credit worthiness, or the view that Nigerian investments are perfect substitute to investments anywhere in the world as explained above. With increased export, increased capital inflow, and decreased import, Nigeria will be on the way to economic prosperity.

There are also some criticisms for this structural approach. One, it focuses on current account alone. In trying to explain the cause of balance of payment problems and making a huge point about the structure of the economy (which is often overlooked), it is unfortunate that the capital account is ignored. The author believes that the role of the financial market of a country in re-structuring of the economy can't be ignored. The monetary sector often determines what investments go into the real sector. If a country has subpar productivity relative to her competitors, the monetary policies can often be used to incentivize investment. This will be a worthy addition to the structural approach for Nigeria.

This paper also espouses a problem that is often challenging to address. As we have said that many developing countries suffer from this "structural syndrome". Nigeria has long highlighted this problem and sought to diversify away from crude oil. However, this has proven difficult. Nigeria, and maybe most developing countries, often don't have the political will or time to make this structural change. Building the manufacturing/technology sector (which is efficient and has products with high income elasticity of demand) is huge investment of time and resources in education, infrastructure, policies etc. A term or two in office is not enough to do this. Political unrest and ethnic agitations often make fundamental changes challenging. A tribe or group of people who have always benefitted from existing structures will feel threatened.

Also, if developing countries are ready to put their acts together and produce goods with high income elasticity of demand, would advanced countries be ready to reduce their export and surplus so that developing countries (new market entrants) can raise their exports (Bird, 2001)? Will they be international coordination? This might be a worthy question for the World Trade Organization.

## V. CONCLUSION

Dampening aggregate demand may seem like a quick fix to Nigeria's balance of payment deficit problem, however, this paper has showed that this measure creates recession. A more sustainable, and maybe difficult, approach is raising Nigeria's output through a structural focus on efficient production of goods with high income elasticity of demand. This approach will raise wages, raise quality of life (if inflation can be managed), and strengthen the naira. A surplus balance of payment looks like the linchpin to Nigeria's economic buoyancy. Hopefully Nigeria has the political will and patience to execute this approach.

Generating HTML Viewer...

References

18 Cites in Article

Graham Bird (1981). Financing balance of payments deficits in developing countries: The roles of official and private sectors and the scope for cooperation between them.

Graham Bird (1983). Should developing countries use currency depreciation as a tool of balance of payments adjustment? A review of the theory and evidence, and a guide for the policy maker.

Graham Bird (2001). Conducting macroeconomic policy in developing countries: Piece of cake or mission impossible?.

Graham Bird (2006). Introduction.

Graham Bird (2007). Macroeconomic Policy and the International Monetary Fund.

G Bird (2014). Macroeconomic Policy in Open Economies.

G Ezu,P Oranefo (2023). Effect of Capital Flight on Foreign Investment in Nigeria.

Liang-Shing Fan,Chuen-Mei Fan (2002). The Mundell-Fleming Model Revisited.

H Houthakker,Stephen Magee (1969). Income and Price Elasticities in World Trade.

Martins Iyoboyi,Olarinde Muftau (2014). Impact of exchange rate depreciation on the balance of payments: Empirical evidence from Nigeria.

Knoema (2020). Figure 3. High net lending of non-financial corporations is driving the current account surplus.

Thomas Lagoarde-Segot (2023). Trade, Capital Flows and the Balance of Payments.

A Oladipupo (2011). Impact of Exchange Rate on Balance of Payment in Nigeria.

K Pilbeam (2013). International Finance.

H Popper,A Mandilaras,G Bird (2013). Trilemma stability and international macroeconomic archetypes.

J Riti,H Gubak,Da Madina (2016). Growth of non-oil sectors: A key to diversification and economic performance in Nigeria.

(2021). Current account balance, billions of US dollars.

J Ukangwa,N Onyenze,K Uke-Ejibe Analysis of the Impact of Exchange Rate on Balance Of Payments in Nigeria.

No ethics committee approval was required for this article type.

Data Availability

Not applicable for this article.

How to Cite This Article

Victor Kilanko. 2026. \u201cNigeria’s Balance of Payment Crisis: Causes and Recommendations\u201d. Global Journal of Management and Business Research - B: Economic & Commerce GJMBR-B Volume 23 (GJMBR Volume 23 Issue B3).

Explore published articles in an immersive Augmented Reality environment. Our platform converts research papers into interactive 3D books, allowing readers to view and interact with content using AR and VR compatible devices.

Your published article is automatically converted into a realistic 3D book. Flip through pages and read research papers in a more engaging and interactive format.

Our website is actively being updated, and changes may occur frequently. Please clear your browser cache if needed. For feedback or error reporting, please email [email protected]

Thank you for connecting with us. We will respond to you shortly.