This project evaluates the Brownian Motion model’s effectiveness compared to historical stock market data. This paper analyzes its potential reasons for inaccuracies across time spans, specifically delving into its inability to incorporate major events such as the COVID-19 pandemic and the 2008 stock market crash. The paper uses the 2008 stock market crash and the Great Depression example instead of the COVID-19 pandemic to allow long-term accuracy to be tested. A prominent element of this model is the stochastic differential equation, which represents the randomness and uniqueness that the price of a derivative depends on. Stochastic elements reflect factors that influence the value of a derivative, like time, volatility of the underlying asset, interest rates, and other market conditions. The Markov property simplifies this complicated figure, meaning that the future value is independent of past prices. The Markov property is a “memoryless” feature; the current price is the only factor in future pricing, aligning with the effective market hypothesis. Finally, the paper offers insights on enhancements to the model, adjusting it to be a more efficient tool for economic forecasting.

## I. INTRODUCTION

Stochastic calculus allows the modeling of random systems such as financial markets. "Stochastic components" in such models are randomly determined, with a random probability distribution that may be statistically analyzed but is impossible to predict precisely. The basis of this area of mathematics lies in continuous but not differentiable functions, requiring a theory of integration where integral equations do not need defined derivative terms. Brownian Motion is often a component in the stochastic differential equations of stochastic calculus, representing the unpredictable aspect.[^8] Named for Robert Brown, the botanist who observed the motion of pollen particles in water in 1827, the Brownian motion model imitates prices in a continuous-time setting and is independent of past movements. It can be considered a limit of a symmetric random walk (a sequence of vertices and edges of a graph) with small steps in short time intervals. In each time unit $\Delta t$, a step of size $\Delta x$ is taken to the left or right with equal probability. Each step is an independent event with a value of either 1 or -1. The step size $\Delta x$ is related to the time interval $\Delta t$ by $\Delta x = \sigma \sqrt{(\Delta t)}$ where $\sigma$ represents the standard deviation and the position at time $t$, denoted by $X(t)$, is the sum of all steps taken up to time $t$.[3]

The history of stochastic calculus begins with Brownian motion, and its origin can be traced back to two men who developed their models independently: L. Bachelier, who created a model while deriving the dynamics of the Paris stock market, and A. Einstein, who created a model of small particles suspended in a liquid. In an attempt to model the Paris Bourse market, Bachelier used the Central Limit Theorem, which states that the sampling distribution of a variable approximates a normal distribution as long as it is large enough. He concluded that increments in stock prices should be independent (future movements are independent of past movements), stationary (statistical properties are constant over time), and normally distributed (as $\Delta t$ approaches 0, $X(t)$ becomes a continuous process with mean 0 and variance $\sigma^2 t$ ). He was able to define processes related to Brownian motion, such as finding the maximum change during a time interval. Bachelier was the first to suggest using Brownian motion to model stock prices. In creating his model, Einstein assumed Bachelier's finding that Brownian motion was a stochastic process with independent increments, continuous paths, and stationary Gaussian increments. He concluded that the visible random movement of particles in water that Robert Brown observed was due to water molecules' invisible and random motion. In a statistical mechanics approach, he modeled these molecules as randomly moving particles that collide with suspended particles to cause erratic movements. Most importantly, he derived the diffusion equation, which relates the mean square displacement of a particle to the time interval of observation, which is given by: $(x^2) = 2Dt$ where $(x^2)$ is the mean square displacement of the particle, $D$ is the diffusion coefficient, and $t$ is the time interval. If the kinetic energy of fluids was right, the molecules of water moved at random, and a small particle would receive a random number of impacts of random strength from random directions in any period of time, which would cause the particle to move in the same way that Brown first observed.[5]

Economist Paul Samuelson found Bachelier's thesis in the MIT library and argued that prices must have fluctuated randomly in 1965, 65 years after Bachelier assumed it. His papers became the basis of the efficient market hypothesis and the foundation of option pricing theory.[^10] Samuelson proposed that changes in future prices were uncorrelated across time, a generalization of Bachelier's random walk model, and claimed that this postulate could be extended to an immediate application to options.[6] As for Einstein's contribution to financial modeling, the stock price can be envisioned as a particle undergoing Brownian motion. Just as in Einstein's model driven by molecular collisions, a stock price moves randomly, caused by various unpredictable market factors. Based on his derived diffusion equation, the analogous function for stock prices would be $\square S^2) = \sigma^2 t$ where $(S^2)$ is the variation in stock price, $\sigma^2$ quantifies the degree of risk associated with the price, and $t$ is the time interval. This equation implies that the uncertainty or random movement in stock price increases with time.

Stock markets, foreign exchange markets, commodity markets, and bond markets are all assumed to follow Brownian motion, where random amounts alter the change of state on the assets. The models used to describe this motion are fundamental tools on which financial asset pricing and derivatives pricing models are based. The assumption that asset prices follow Brownian motion is essential to options pricing models. Options, which give its holder the right but not the obligation to buy or sell a certain amount of a financial asset by a certain date for a certain strike price, are determined by derivative pricing. Using Brownian motion to determine the fair price of an option, these models can more accurately describe how prices change over time. $^{8}$

In this paper, the Dow Jones Industrial Average (DJIA) will be used to discuss Brownian Motion's accuracy in predicting stocks. The DJIA is a stock market index measuring the performance of 30 large and publicly owned companies. The index is price-weighted: the components are weighted based on their stock prices rather than their market capitalization. The DJIA index is relatively measured; its value represents the aggregate stock prices of its component companies. The units of the index are not specified in terms of a specific unit, currency, or percentage. The DJIA values indicate the index level at a point in time. The index value refers to the combined stock prices of the 30 companies in the index, weighted by their prices, equated to that numerical value. Changes in the DJIA over time reflect the overall performance of the stock market as represented by these 30 companies. The DJIA can be used to track the overall health and trends in the stock market as the companies within it span many important industries and commodities.

## II. OPTIONS PRICING AND GEOMETRIC BROWNIAN MOTION

Because Brownian motion can take on negative values, it is not always suitable for modeling stock prices. As a result, we use a non-negative variation called Geometric Brownian motion. A stochastic process $S_{t}$ is said to follow a Geometric Brownian motion if it can be defined by $S(t) = S_{o}e^{X(t)}$, where $X(t) = \sigma B(t) + \mu t$ is Brownian motion with drift and $S(0) = S_{0} > 0$ is the initial value. After taking the natural logarithm, the equation becomes $X(t) = \ln(S(t)/S_{0}) = \ln(S(t)) - \ln(S_{0})$. $\ln(S(t)) = \ln(S_{0}) + X(t)$ is normal with mean $\mu t + \ln(S_{0})$, and variance $\sigma^{2}t$. The idea of using this model is to create a "level playing field" where the activity of buying or selling stock offers no arbitrage or simultaneously buying and selling the same asset in different markets to try to profit off of the tiny differences in price between markets, so no one should be able to make a profit with certainty.[9]

It also must satisfy the following stochastic differential equation $\mathrm{dS}_{\mathrm{t}} = S_{\mathrm{t}}(\mu \mathrm{dt} + \sigma \mathrm{dB}_{\mathrm{t}})$ where $\mathrm{dS}_{\mathrm{t}}$ is the change in the stock price, $S_{\mathrm{t}}$ is the stock price at time $t$, $\mu$ is the percentage drift representing the expected return of the stock per unit of time, $\sigma$ is the percentage volatility measuring the standard deviation of the stock's returns, and $\mathrm{dB}_{t}$ represents a Brownian motion process. Higher volatility increases the option's value since there is a greater chance that the stock price will move significantly by the expiration date. This equation has an analytic solution: $S_{t} = S_{0}e^{(\mu -\sigma 2 / 2)t + \sigma dBt}$ for an arbitrary initial value $S_0$. The expected price grows like a fixed-income security with a continuously compounded interest rate. In practice, the compounded interest rate is much greater than the real fixed-income interest rate so that one would invest in stocks. This model is used in options pricing. $^{10}$

The rights without obligations that options provide have financial value, so option holders must purchase them and make them assets. They are called derivative assets because they derive their value from other assets. For an exercise price $K$ and an exercise date $T$, one has the right to buy stocks with price $K$ and sell them with $S_T$ in the market if $S_T > K$. If not, one has no obligation to purchase. This option is called a European call option, and we define claim $C$ (payoff at time $T$ ) by $C = (S_T - K)_+ = \max(S_T - K, 0)$. So, if $S_T > K$, then the option owner will obtain the payoff $C$ at time $T$, while if $S_T \leq K$, then the owner will not exercise their option, and the payoff is 0. At the time of writing the option, $S_T$ is unknown and therefore raises the problem of pricing the option, or how should one price at time $t = 0$ an asset worth $(S_T - K)_+$ at time $T$? The primary goal is to determine the fair price at $t = 0$ for a European call option, which is only one example of financial derive. The oldest derivative and most natural claim on a stock is the forward. If two parties enter into a forward contract, the seller agrees to give the other party the stock at some set time for some set price. If $T$ denotes the expiry date, $F$ denotes the strike price, and the value of the stock at time $t > 0$ is $S_t$. The stock must be exchanged at time $T$ for $\$F$, so to determine the fair value of this contract means to determine the value of $F$.[11]

## III. MARKOV PROPERTY

Geometric Brownian Motion follows the Markov property, a memoryless feature that allows the future price to be independent of the past prices, given the present price. This feature aligns with the efficient market hypothesis that all past information is already reflected in current prices. In the context of Brownian Motion, the Markov property simplifies the process's modeling. The property allows for the future movements of a particle in Brownian motion to rely only on its current position, disregarding the path the particle took to get there. This simplifies the analysis and modeling of Brownian motion because once the current state of a particle is known, its history of motion can be ignored, as its past does not influence its future.

The Markov property is defined by the equation $\mathbb{P}(55 + 5\in 5|\mathcal{F}) = \mathbb{P}(55 + 5\in 5|55\phi \circ \alpha \lambda \lambda 5,5\in 5$ and $5\in 5$. The starting point is a probability space $(\Omega,\mathcal{F},\mathbb{P})$, so that $\Omega$ is the set of outcomes, $\mathcal{F}$ the 5-algebra (a subset of the set algebras) of events, and $\mathbb{P}$ the probability measure on $(\Omega,\mathcal{F})$. The time set 5 is either N (discrete time) or $[0,\infty)$ (continuous time).

The defining condition states that the conditional distribution of $55 + 5$ given $\mathcal{F}5$ is the same as the conditional distribution of $55 + 5$ just given 55. Conditional distribution is the probability distribution of a random variable. $^{14}$ It is calculated according to the rules of conditional probability after observing another random variable. In the equation, s can be thought of as present time, so that $5 + 5$ is a time in the future. The present state, 55 is known, so the events in the past are irrelevant for predicting the future state, $55 + 5$.

## IV. COMPARING BROWNIAN MOTION STOCK INDEX MODELS

Python and Sublime Text were used to simulate Brownian Motion. $^{15,16}$ A random seed value, 42, was generated. The specific value doesn't matter; what's important is that using the same seed value will produce the same sequence of random numbers, making your code more predictable and reproducible. When prompted with "code for Brownian motion with the value of Dow Jones stocks as y-axis and from 2000 to 2015 in Python," and "code for Brownian motion with the value of Dow Jones stocks as y-axis and from 1900 to 2000 in Python," ChatGPT-generated code for the simulated graphs. $^{17}$ These codes were edited slightly to produce better results and to fix minor errors.

To create the Brownian Motion function, the line def brownian_motion(dt, n_steps) was used to define a function named brownian_motion that takes two parameters, (1) dt (time step) and (2) n_steps (number of steps). $t = \text{np.linspace}$ (1900, 2000, n_steps + 1) creates an array $t$ representing time from 1900 to 2000 with $n_steps + 1$ points. Increments = np.random.normal (0, np.sqrt(dt), n_steps) generates random increments from a normal distribution with mean 0 and standard deviation V/dt. Bm = np Cumsum (increments) calculates the cumulative sum of the increments to obtain the Brownian motion values. return t, bm: Returns the time array $t$ and the corresponding Brownian motion array bm. To set the function's parameters, dt=1/252.0 was used to set the days per year in which stocks are traded (252 trading days in a year). n Years = 2015 - 2000 or n Years = 2000 - 1900 was used to calculate the number of years. In Figure 1, n Years = 2015 - 2000 was used. In Figure 3, n years = 2000 - 1900 was used. Lastly, to generate Brownian Motion t, bm = brownian_motion(dt, n_steps)was used to call the brownian_motion function to generate time (t) and corresponding Brownian motion values (bm) based on the specified time step and number of steps. To simulate Dow Jones Stock Values, initial_price = 10000 was used to set the initial index value to 10,000. Then, dow_jones = initial_price * np. exp(0.02 * t + 0.1 * bm) simulates Dow Jones stock values using the geometric Brownian motion equation. To plot geometric Brownian Motion plt. figure(figsize=(10,6)): Creates a new figure with a specified sizeplt.plot(t, dow_jones, label='Dow Jones Index'): Plots the Dow Jones stock values against time. plt.title('Brownian Motion with Dow Jones Stock Values (1900-2000)')sets the plot's title, plt. label ('Time (Years)')sets the label for the x-axis, plt. label ('Dow Jones Index')sets the label for the y-axis, pltlegend(), adds a legend to the plot, plt.grid(True), adds a grid to the plot, and plt.show(), displays the plot.

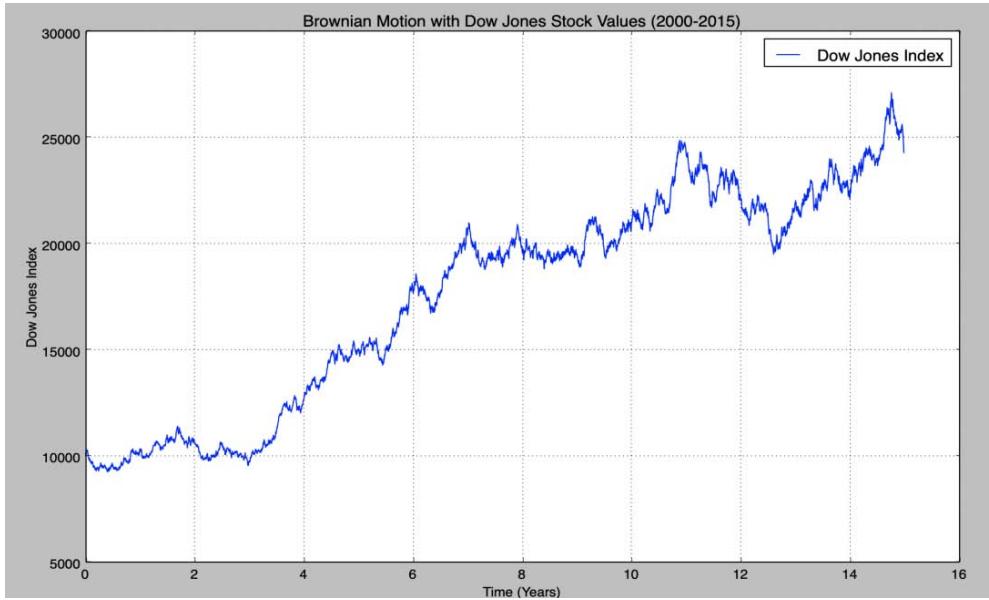

Figure 1: Simulated Brownian Motion From 2000-2015 Measuring Dow Jones Industrial Average Index. $^{18}$

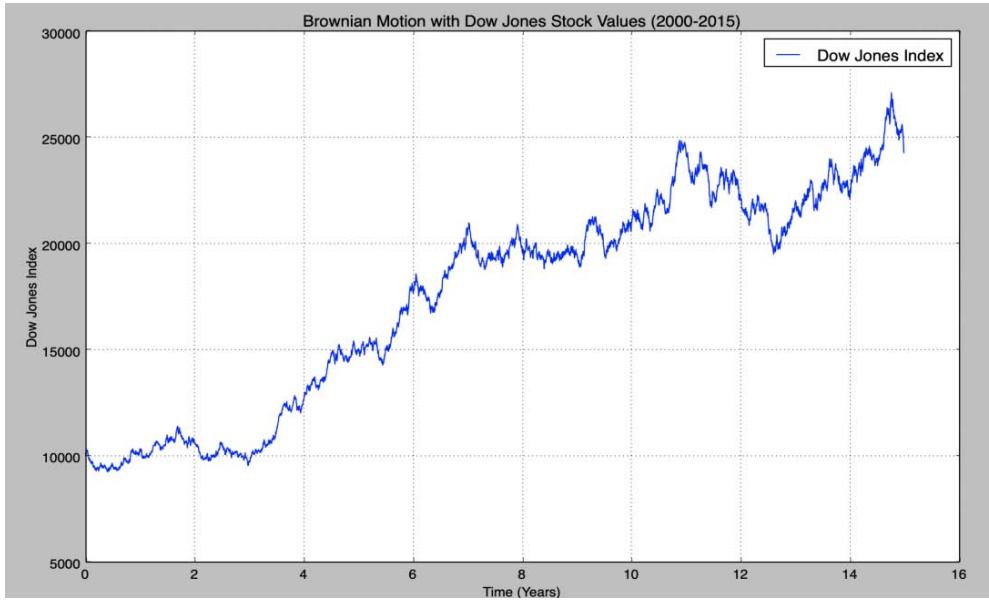

Figure 2: Real-life Dow Jones Industrial Average Index From 2000-1015.19

In comparing the simulated Dow Jones Industrial Average (DJIA) index to the real-life index over fifteen years, from 2000 to 2015, the overall trends of the simulated graph are accurate, but the changes in the index from year to year are not. In the simulated chart, the index starts at around 10,000, whereas the index in 2000 was about 20,000. The start value of the simulated graph is set to 10,000 as that value cannot be predicted or changed by Brownian Motion. Over time, the predicted values become more closely related to the real-life values without considering any events that significantly affect the economy and stock market. In the time period from 2000 to 2015, the DJIA index lost nearly half its value because of the stock market crash of 2008 but then made a complete recovery. However, because this decrease in the index happened so suddenly and the economy was able to recover quickly and completely, the trend of the simulated graph is still closely related to the actual health of the stock market. The simulated value of the DJIA steadily rose, with minor depressions, from 2000 to 2015, which aligns with the real-life stock market trends, except for the 2008 crash. In both the real-life and simulated graphs, during 2015, the index was about 25,000, with the simulated value slightly higher than the actual index. Overall, Brownian Motion on a small time interval is semi-accurate compared to the true DJIA index but is not precise enough for any factual claims to be made. The trends of the graphs mirror each other well, but when observing shorter time periods or a specific year, the values differ greatly.

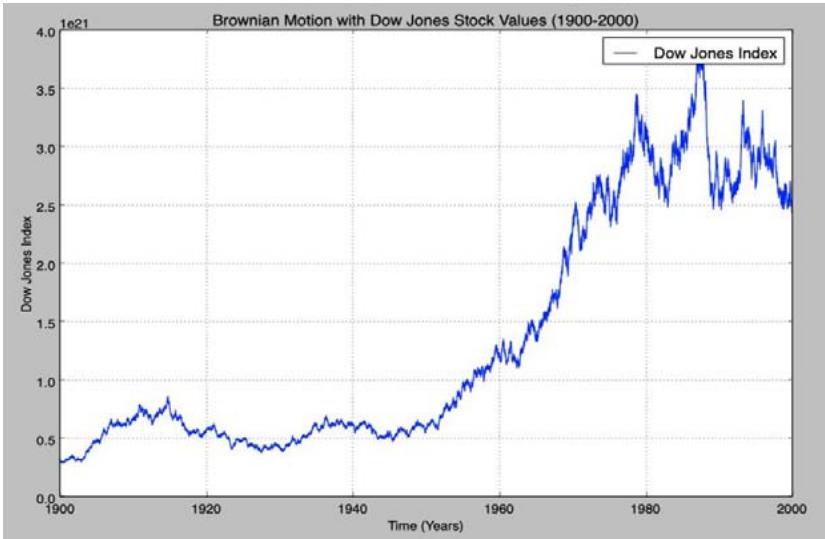

Figure 3: Simulated Brownian Motion from 1900-2000 measuring Dow Jones Industrial Average Index with the y-axis being in the thousands.[20]

Figure 4: Real-life Dow Jones Industrial Average Index From 1900-2000.21

In comparing the simulated Dow Jones Industrial Average (DJIA) index to the real-life index over one hundred years, from 1900 to 2000, the overall trends of the graphs are very similar. The start value—randomly generated in the simulated graph—is inaccurate, but the simulation quickly balances out as time progresses. When analyzing large periods of time, especially in the last century, where significant advances have been made (including the inception of the internet), it makes sense that the simulated graph would be inaccurate. While the real-life diagram depicts sharp declines and increases, the geometric Brownian Motion steadily rises with time, providing incorrect results. Due to the nature of Brownian Motion and its properties of randomness, sharp peaks and valleys like those depicted in the real-life graph are unlikely to be represented. Overall, the long-term estimate of the DJIA is almost entirely different from the actual graph, primarily due to the many events occurring in the 20th century. Although this depiction is inaccurate, Brownian Motion's uses are still helpful as a baseline for predicting future stock values. In the shorter time period of fifteen years, while disregarding the stock market crash, the simulated graph is closely related to the actual stock values.

## V. LIMITATIONS

Although geometric Brownian motion has widespread uses, it has many limitations and faces criticism for its oversimplification and the many assumptions it makes. For instance, GBM assumes constant volatility over time, which isn't true in the real market.[22] Additionally, actual financial returns often exhibit fat tails—greater-than-expected probabilities of extreme values—and are not normally distributed. Geometric Brownian Motion also does not account for market crashes or price jumps. While the model provides a framework for understanding stock pricing, real-world financial markets are influenced by factors that are not entirely random, like global pandemics and depressions, and can exhibit trends and cycles. Therefore, while the Brownian motion model is useful, it oversimplifies the complexities of financial markets.

## VI. DISCUSSION

The primary motivation behind these models comes from the nature of the stochastic processes. In practice, the price changes in the stock market are so frequent that a discrete-time model can hardly follow its movement. On the other hand, continuous-time models such as the ones used in Brownian motion lead to more explicit computations, even if they require code for simulation. While the Brownian motion model effectively captures the randomness of market movements through its stochastic components, it also reveals the challenges of predicting large-scale economic events.

This analysis emphasizes the need for continuous refinement of financial models to better understand and predict market behaviors. Incorporating elements into the algorithm that account for sudden, significant economic events could greatly enhance the model's accuracy in real-world scenarios, leading to more informed investment strategies and better financial planning. The balance between mathematical modeling and practical economic realities underscores the importance of considering both random and systematic factors in economic forecasting. As the global economy continues to evolve in complexity, the adaptation and improvement of models such as Brownian motion become imperative. The ability of models like Brownian motion to provide insight into market dynamics directly impacts financial decision-making, risk management, and policy formation. With the world still grappling with the effects of the COVID-19 pandemic, understanding how major events disrupt the economy is pivotal in navigating current and future economic crises. By striving to refine and improve these models, one can hope to achieve a more stable and predictable financial future.

Generating HTML Viewer...

References

18 Cites in Article

Daniel Mcgrath (2006). Behavioral Code Team.

James Chen (2021). Central Limit Theorem.

(2023). Chapter 10: Introduction to Stochastic Processes.

Elena Picech (2006). https://digitalcommons.georgiasouthern.edu/cgi/viewcontent.cgi?article=1182&context=thecoastalreview.

Imad Al-Qadi,Yanfeng Ouyang,Eleftheria Kontou,Angeli Jayme,Noah Isserman,Lewis Lehe,Ghassan Chehab,Asad Khan,Denissa Purba,Watheq Sayeh,Haolin Yang,Gabriel Price,Zhoutong Jiang (2023). Planning for Emerging Mobility: Testing and Deployment in Illinois.

(2020). Dow Jones Industrial Average Index (DJIA).

John Hunter (2007). Matplotlib: A 2D Graphics Environment.

Robert Jarrow,Philip Protter (2023). A short history of stochastic integration and mathematical finance: the early years, 1880–1970.

J Skinner (2008). LAS VEGAS SANDS CORP., a Nevada corporation, Plaintiff, v. UKNOWN REGISTRANTS OF www.wn0000.com, www.wn1111.com, www.wn2222.com, www.wn3333.com, www.wn4444.com, www.wn5555.com, www.wn6666.com, www.wn7777.com, www.wn8888.com, www.wn9999.com, www.112211.com, www.4456888.com, www.4489888.com, www.001148.com, and www.2289888.com, Defendants..

Michael Kozdron (2023). Appendix B: Probability, Stochastic Processes and Stochastic Calculus.

K Kuter (2019). Saint Mary’s College, Cushwa-Leighton Library.

No ethics committee approval was required for this article type.

Data Availability

Not applicable for this article.

How to Cite This Article

Chelsea Peng. 2026. \u201cFinancial Modeling with Geometric Brownian Motion\u201d. Global Journal of Management and Business Research - C: Finance GJMBR-C Volume 23 (GJMBR Volume 23 Issue C4).

Explore published articles in an immersive Augmented Reality environment. Our platform converts research papers into interactive 3D books, allowing readers to view and interact with content using AR and VR compatible devices.

Your published article is automatically converted into a realistic 3D book. Flip through pages and read research papers in a more engaging and interactive format.

Our website is actively being updated, and changes may occur frequently. Please clear your browser cache if needed. For feedback or error reporting, please email [email protected]

Thank you for connecting with us. We will respond to you shortly.