Different perceptions shape different banking choices. This study investigates women’s perceptions of banking channels in Bangladesh. It also explores the diverse catalysts influencing banking choices and women’s challenges in shaping their preferences. We used a qualitative interview method to understand female perceptions of banking channels. We did a thematic analysis of interviews with thirty female banking system users as the sample. Using the purposive sampling method, we selected the respondents for the interviews. To analyze the coded interviews, we employed an atlas. ti 2023, a qualitative data analysis software. The study found that quick and convenient access, efficient financial management, cost-effectiveness and high security play a significant role in shaping women’s banking behaviours. The study also found that women encounter challenges related to digital literacy, security and complex banking systems. Moreover, the study found that the benefits of time-saving mechanisms are replaced by the burden of high transaction costs, challenging low-income thresholds. Therefore, the authors of this article recommend digital literacy initiatives, security enhancements, and cost mitigation strategies. The study emphasized the need for policy interventions to promote women’s financial inclusion.

## I. INTRODUCTION

The role played by the financial system in Bangladesh is significant for the country's development and the achievement of its goals. The government has executed various measures to improve public finance management, such as using New Public Management principles and innovative tools for financial management in the public sector (Das et al., 2023). Furthermore, the banking institutions and financial entities in Bangladesh actively contribute to promoting sustainable economic growth and environmental preservation through green financing, as per the guidelines set by the Bangladesh Bank (BB)(Shil & Chowdhury, 2021). Additionally, there is a growing interest in implementing Financial Supply Chain Management (FSCM) practices in Bangladesh, with specific banks and financial institutions already embracing these concepts to benefit buyers, suppliers, and the overall financial supply chain (Moon & Hasan, 2022).

Banking alternatives accessible for financial services in Bangladesh encompass mobile banking, short messaging service (SMS) banking, agent banking, internet banking, and mobile money accounts (Akash et al., 2022). Mobile banking refers to engaging in finance-related activities on a mobile device such as a smartphone or tablet (Kabir et al., 2021). It represents a straightforward and cost-effective choice for customers, having experienced a surge in popularity within Bangladesh due to the inadequacy of conventional banking facilities (Bhowmik et al., 2023). Conversely, agent banking has emerged as a robust mechanism for facilitating financial inclusion, predominantly in rural regions (M. T. Hasan, 2020). The purpose of these banking options is to enhance financial inclusion and furnish convenient services to the populace of Bangladesh.

Microelectronic payment systems, mobile banking, and trade receivable exchange (TRX) represent a selection of transaction options found within Bangladesh's financial systems (Akash et al., 2022; Moniruzzaman et al., 2023). In Bangladesh, mobile financial services (MFS) have played a significant role in serving online business activities and other financial services (Rohanifar et al., 2022). Clients can opt for mobile banking as a convenient and cost-effective method using smartphones or tablets (Islam et al., 2022). TRX, on the other hand, presents a financing solution that unlocks the funds tied up in trade receivables, benefiting small and medium enterprises operating in Bangladesh. These various transaction choices have been developed to enhance service delivery, increase consumer awareness, and address working capital challenges within the country. However, the widespread adoption of cashless transaction services in Bangladesh faces obstacles such as intermediaries, the potential for terrorist activities, and the need to re-skill existing employees. Consequently, concerted efforts are being made to integrate cashless systems into the societal context of Bangladesh and the wider Global South.

In recent years, considerable growth in digital financial services in Bangladesh has been witnessed. The banking sector has fully embraced digital technologies, transforming government practices and banking models (Hoque, 2023). Mobile financial services (MFS) have seen tremendous growth, with a significant increase in the number of mobile accounts and a rise in the frequency of transactions conducted through the mobile network (Uddin & Begum, 2023). The healthcare sector has also observed an increase in the adoption of FinTech services, influenced by factors such as perceived ease of use, social influence, and trust (Moudud-Ul-Huq & Perhiar, 2023). The outbreak of the COVID-19 pandemic is one of the reasons for the increase in the adoption of MFS, with social influence, trust, perceived benefit, and facilitating conditions playing a significant role in the intention to adopt (Hassan et al., 2023). Overall, the growth of digital financial services in Bangladesh has provided opportunities for the government, businesses, and financial institutions to offer various payment options and has the potential to contribute to financial inclusion. The participation rate of women and men in Bangladesh's financial system varies across different sectors. In the agricultural industry, the female workforce comprises $18.3\%$, while the male workforce comprises $22.3\%$ (Biswas et al., 2022). In the banking industry, there is a higher representation of male employees, with males accounting for $85\%$ and females accounting for $15\%$ (Rahman & Khan, 2020). Moreover, women's empowerment and economic engagement in Bangladesh have improved by increasing female labour force participation and reducing the gender wage gap. Gender diversity and inclusion should be promoted by addressing the societal and maker barriers, as women still face challenges regarding their economic preferences and control (Solotaroff et al., 2019).

Although digital banking services are becoming increasingly popular globally, there still needs to be more knowledge regarding the specific reasons, challenges, and expectations related to female clients in Bangladesh. Many studies (Babbar et al., 2023; Bhuiyan et al., 2022; Chakraborty & Abraham, 2023; Hayat & Hossain, n.d.; Kumari, 2023; Lee et al., 2022; Siek & Rukma, 2022; Singh & Singh, 2023; Toyon, 2023) have examined the adoption of digital banking services, but they typically fail to consider the specific gender-related factors that can impact women's choices, experiences, and expectations in this area. Addressing the vacuum, this study aims to fill the gap three-fold. First, it will investigate the catalysts of females' use of banking systems, namely mobile banking, app or internet-based banking, branch banking, and agent banking for their transactions. Second, it also finds out the challenges faced by the females while completing the transactions using these systems. Third, it will gather the participants' recommendations for improving the banking systems. To facilitate the study, the paper interviews 30 female users of banking systems and uses thematic analysis to understand the perception of females towards all banking systems. We use purposive sampling in this regard and adopt atlas.ti 2023 to analyze the coded interviews. This paper contributes to existing literature by emphasizing the status quo and challenges of different banking systems and investigating the expectations of females for the regulators and policymakers.

This paper is organized as follows: Chapter 2 reviews the relevant literature of the study. Chapter 3 entails the data and methodology followed throughout the study. Chapter 3 facilitates the findings and discussion, which includes the catalysts for adopting digital banking services, challenges faced by females, and recommendations by the participants for banking services in Bangladesh. Finally, chapter 4 concludes with recommendations for stakeholders and concluding remarks.

## II. LITERATURE REVIEW

### a) Digital Dividends and Financial Inclusion

The concept of digital dividend arising from financial inclusion denotes the advantageous economic outcomes and prospects that ensue from the expansion of digital financial services and the enhanced availability of formal financial services for populations that have been excluded or underserved (Shen, 2022). This phenomenon is improbable to result in economic growth, improved living conditions, and poverty alleviation (Buteau et al., 2021). In addition, the incorporation of digital financial services plays an essential role in the achievement of financial inclusion and the stimulation of economic development. Moreover, digital inclusive finance, which amalgamates digital technology and inclusive finance, holds the capacity to mitigate credit constraints, diminish information uncertainty, and enhance agricultural productivity. By reducing the costs associated with financial institutions and the expenses incurred by utilizing financial services, digital inclusive finance can contribute to the process of alleviating multidimensional poverty. Furthermore, it demonstrates the potential for susceptible and disadvantaged groups, like females, small-business owners, and internal migrants, to enhance their access to various financial services.

### b) Gender Inclusive Financial Services

Financial inclusion has been observed to exert a favourable influence on women's empowerment at a global level, including within the context of Bangladesh. Research studies (Chakraborty & Abraham, 2023; Kumari, 2023; Singh & Singh, 2023) have indicated that the notion of financial inclusion, which involves offering savings accounts to individuals who lack access to traditional banking services, leads to greater involvement of women in making financial decisions within households, as well as elevated levels of savings and income. In Bangladesh, women's financial inclusion obstructions have been attributed to religious limitations and gender-based discrepancies within the labour market (Chakraborty & Abraham, 2023; Uddin & Begum,

2023). Nevertheless, it has been found that nations that possess legislation and regulations aimed at promoting gender equality, along with adequate mechanisms for regulation, tend to exhibit a more fabulous presence of financially active women (M. Z. Hoque et al., 2024). However, it is vital to recognize that although financial technology (FinTech) can enhance financial inclusion, it may not be adequate to eliminate the gender gap in financial inclusion (Moghadam & Karami, 2023). Additional policy initiatives may thus be necessary to address gender inequality and foster the financial empowerment of women (Aziz et al., 2022; Chakraborty & Abraham, 2023; Moghadam & Karami, 2023).

### c) Banking: What Shapes our Choices?

Mobile banking, agent banking, branch banking, and app-based banking are all choices available to consumers. Meanwhile, the determinants of these options differ depending on factors like perceived usefulness, ease of use, technology readiness, customer loyalty, and consumer preferences (Uddin & Begum, 2023). Research studies (Akash et al., 2022; Kabir et al., 2021) have indicated that implementing mobile banking necessitates a substantial investment; however, more is needed to guarantee success (Fitriati et al., 2022). The publication of reports on digital transformation and artificial intelligence in the financial sector has resulted in changes in the competitive dynamics and operating models of banking sectors, creating opportunities for app-based banking and cross-selling strategies (Shrivastava & Shah, 2021). Various factors impact the acceptance of mobile banking, such as client loyalty, alternate channels, and the efficient coordination of diverse technologies and business processes (Alonso-Dos-Santos et al., 2020). Consumer preferences for mobile banking apps are shaped by the banking services' compatibility, lenience, and utility (Giovanis et al., 2019).

### d) Landscape of Different Banking Systems

## i. Agent Banking

Agent banking is a financial service that facilitates banking services through alternative means, such as retail outlets, utilizing technology (Chakrobortty & Sultana, 2023). It acts as a mechanism for financial inclusion by incorporating the unbanked population into the formal financial system (Khanam, 2022). The adoption of agent banking has proven successful in regions facing challenges related to geographic accessibility, such as Latin America and Africa (Siddiquie, 2014). Moreover, developed nations like the United Kingdom and Australia have gradually begun implementing agent banking due to its ability to reduce financial institution costs (Ahmed & Ahmed, 2018). In Bangladesh, it has emerged as the most influential avenue for financial inclusion, offering financial transactions to rural individuals without access to banking services through conveniently located agents (Nawrin et al., 2020). By bringing the banking channel closer to clients, agent banking presents flexibility and convenient access to a wide range of individuals who are currently unbanked or have limited access to banking services, facilitating effective financial inclusion.

## ii. Branch Banking

Branch banking refers to the traditional banking model in which customers interact with bank branches for financial transactions and services. It encompasses physical establishments where customers can avail themselves of services such as deposits, withdrawals, loans, and customer support. The existence of tangible branches, direct interactions with bank personnel, and using physical currency for transactions distinguish branch banking. Nonetheless, there is an emerging tendency towards branchless banking, particularly in nations like Bangladesh, where the economy is experiencing rapid growth (Akoil, 2022). Nevertheless, there is an acknowledgement of the imperative to enhance rural branch penetration, financial literacy, confidence in the banking industry, and digital financial services to augment financial inclusion (Ashraf, 2023).

## iii. Mobile Banking

Mobile banking is a technological application that allows clientele to carry out financial transactions using their portable devices. It is a widely embraced method of service provision within the banking sector, offering convenience and accessibility to patrons (Budiarti et al., 2023). The present inclination indicates a burgeoning predilection for mobile banking among the millennial cohort, enticed by its contemporary and instantaneous attributes (Hasan & Habib, 2022). Mobile banking facilitates non-monetary or cashless dealings, empowering customers to effectuate smartphone payments and transfers (A. & Subramanian, 2022). A network of interconnected computers buttresses it and can be availed around the clock, allowing clients to carry out financial transactions at any time and from any location (Herawati et al., 2021). Mobile banking also proffers advantages such as decreased cash management, heightened effectiveness, and fiscal savings for enterprises. Nonetheless, obstacles still exist that necessitate surmounting, encompassing restricted functionalities, disturbances in network connectivity, and the imperative to ensure the security and privacy of mobile banking transactions.

## iv. App-based Banking

The term "app-based banking" pertains to the utilization of mobile banking applications for the execution of financial transactions. It is a technological application devised to furnish convenience and immediate accessibility to banking services, mainly catering to the preferences of the millennial generation, who favour contemporary and digital solutions (Budiarti et al., 2023). App-based banking falls within the broader digital banking domain, encompassing many electronic payment systems, including online credit card payments, electronic cash, electronic checks, and minor payments (Sharma et al., 2022). The employment of app-based banking has experienced a gradual upsurge owing to its advantageous characteristics such as convenience, timeliness, and efficiency, thus rendering it a promising means of payment today (Prasetyaningrum et al., 2022). Gamification, which is the application of game elements within a non-game context, has also been embraced by numerous app-based banking companies to augment user engagement and loyalty (Siek & Rukma, 2022). Overall, app-based banking signifies a disruptive innovation that has profoundly revolutionized the conventional banking industry, presenting personalized and commercialized banking transactions through innovative digital applications.

## III. DATA AND METHODOLOGY

### a) Approach

The interview method is applied in this study as it is qualitative. It allows us to comprehensively understand the underlying issues in the research and elucidate novel theoretical aspects (Adeoye-Olatunde & Olenik, 2021; Edwards & Holland, 2020). The study's main objective is to understand the perception of females towards different banking channels for making transactions, which still needs to be explored by the existing studies. This kind of research gap can be effectively addressed through a qualitative approach (Thakkar et al., 2022). All interviews are conducted skillfully by the authors to delve into the rationales behind the selection of various banking options, the challenges faced by the women, and the proposed recommendations for enhancing the status quo for them in Bangladesh.

### b) Interview

In-depth qualitative interviews can yield profound insights into a particular matter while mitigating the risk of researchers imposing their perspectives and limiting the scope of discussion (Edwards & Holland, 2020). To conduct these interviews, the authors adhered to a predefined protocol. A semistructured interview format allowed flexibility in exploring participants' experiences, perceptions, and suggestions regarding banking channels. The interviews covered reasons for choosing a specific banking channel, challenges encountered during banking transactions, and recommendations for enhancing banking services in Bangladesh. It was ensured that the interviewees willingly disengaged from answering the questions at any point. The questions ranged from straightforward to crucial. Each interview lasted 5 to 10 minutes, minimizing the time and inconvenience for the respondents. This investigation has concentrated explicitly on females who demonstrated sufficient seriousness and enthusiasm towards providing their responses.

### c) Data Collection

We conducted a qualitative research study to understand the banking channel preferences, challenges faced, and recommendations for improvement among female users in Bangladesh. The study involved interviews with 30 female participants selected through purposive sampling. The participants were chosen based on their uses of banking channels, including branch banking, agent banking, mobile banking, and Internet or app-based banking services. The participants represented diverse ages and socioeconomic backgrounds within Bangladesh.

### d) Data Analysis

We employed atlas.ti 2023, a qualitative data analysis software, to analyze the interview transcripts. Before the analysis, all interview sessions were coded to ensure accuracy and consistency in data representation. Then, the transcripts were coded systematically to identify recurring themes, patterns, and categories related to banking channel preferences, challenges, and recommendations. Through iterative coding and analysis, emergent themes and sub-themes were identified based on the content of the interviews. The coded data were interpreted to extract meaningful insights, understand participant perspectives, and identify commonalities and differences among responses.

### e) Ethical Considerations

Participants' identities and personal information were kept confidential throughout the study. In addition, participant identifiers were removed from transcripts to maintain anonymity during that analysis and reporting. Adequate measures were taken to ensure the secure storage and handling of interview recordings and transcripts in compliance with ethical guidelines and data protection regulations.

## IV. FINDINGS AND DISCUSSIONS

In Bangladesh, people can transact through branch banking, mobile banking (i.e., bKash, Nagad, Tap), internet or app-based banking backed by formal banks (i.e., Trust Money, Cell fin, etc.), and agent banking. To understand the catalysts influencing their choices, the challenges they face, and the things they seek from those options are presented and discussed. The data is organized based on preferences for agent banking, branch banking, mobile banking, and app-based banking systems.

### a) Catalysts of Adopting Banking Systems

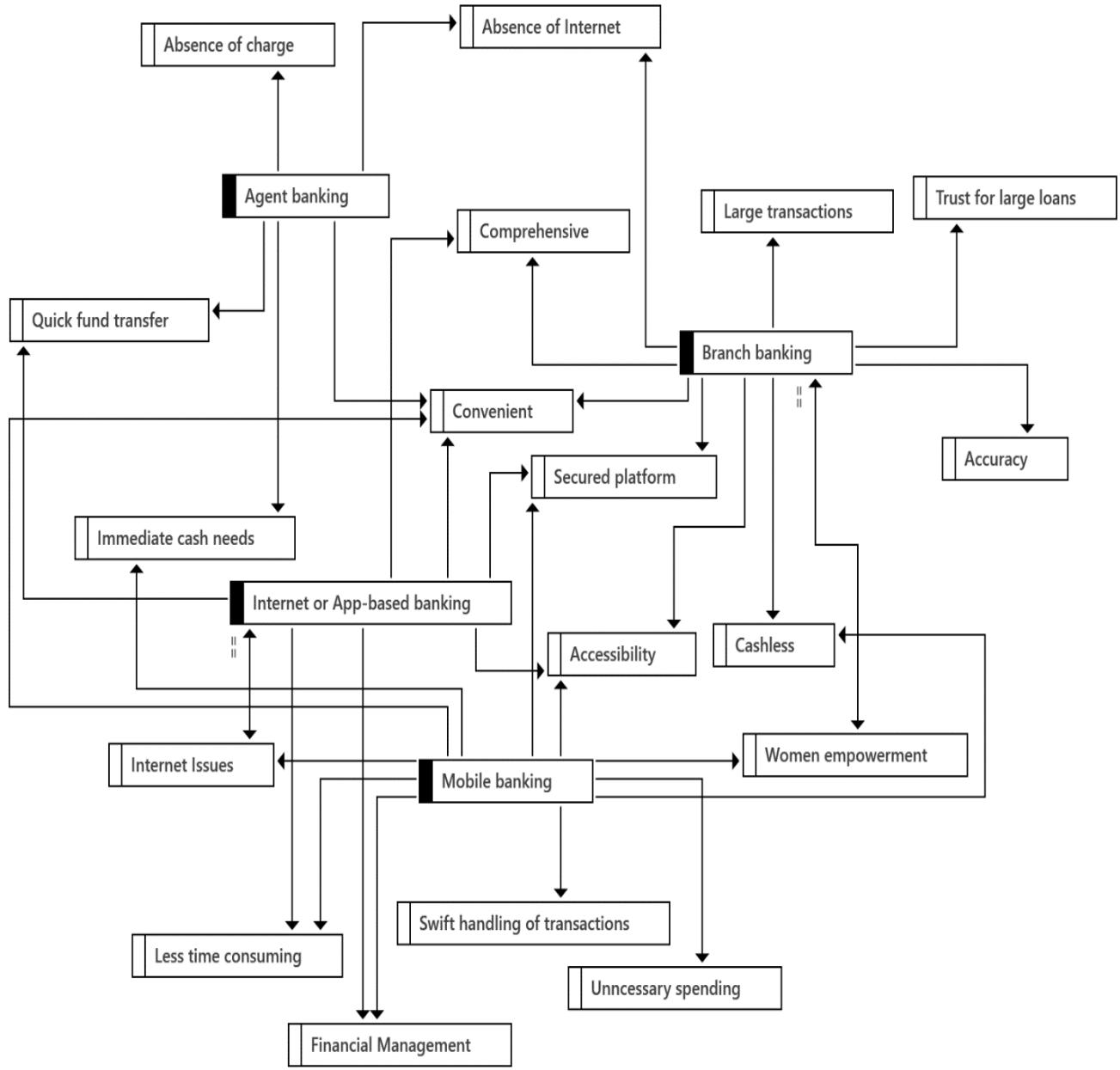

In this dynamic financial landscape, women increasingly attach thinking systems to commenter needs and preferences. Each avenue of banking systems, including agent banking, Internet or app-based banking, mobile banking, and traditional branch banking, presents distinct prospects and factors for the users, especially females. Figure 1 shows the catalysts, summarized through the following themes, for women's choice of banking systems.

## i. Convenience and Accessibility

Women's banking preferences show a strong inclination towards convenient and accessible services. Agent banking, Internet or app-based banking, mobile banking, and branch banking all allow females to efficiently conduct financial transactions and manage their accounts. The ability to quickly and conveniently access banking services plays a significant role in shaping their banking behaviours. Alongside, women prefer banking services that utilize technology to provide convenient connectivity and advanced features, such as Internet or app-based and mobile banking platforms that allow them to manage their finances on their smartphones or computers. Both systems offer data tracking, auto-statement generation, and enhanced security measures for a secure and user-friendly experience.

## ii. Financial Management and Insights

The quest for efficient financial management and insights propels women towards banking services that provide tools and resources for monitoring and analyzing their finances. Internet or app-based banking and mobile banking platforms equip women with comprehensive insights into their expenditure patterns, budgeting tools, and tailored financial guidance, enabling them to make well-informed decisions regarding their monetary affairs. In addition, when making choices, females meticulously assess their expenses and fees linked to the banking services. While opting for banking systems, most participants prefer app-based banking and agent banking more because of the cost-effectiveness and absence of additional charges, such as transportation costs, transaction charges, and the costs incurred due to inconveniences. However, some women feel mobile banking can be feasible, although it has some transaction costs.

## iii. Transaction Efficiency and Comprehensive Services

Efficiency in making transactions is one of the significant considerations when choosing banking services. The ability to transfer funds swiftly and securely, regardless of the platform used, is highly valued. From this perspective, females use mobile banking and app or internet-based banking due to the advantages of immediate fund transfer and swift transaction handling. In addition, they use mobile banking for its diversified range of services. Internet or app-based banking is preferred for transferring money from one account to another bank account within the shortest possible time.

## iv. Security and Empowerment

Although all banking systems are highly secured, mobile banking and app-based banking systems are affected by hackers. From this viewpoint, agent banking and branch banking serve as fully secured and more accurate platforms. However, things are improving as they offer updated security systems to users, thus instilling confidence in female users against the odds. Moreover, these services contribute to women's empowerment by giving them greater control over their finances and access to essential banking services.

Figure 1: Catalysts for choosing different systems.

Source:Authors'analysis

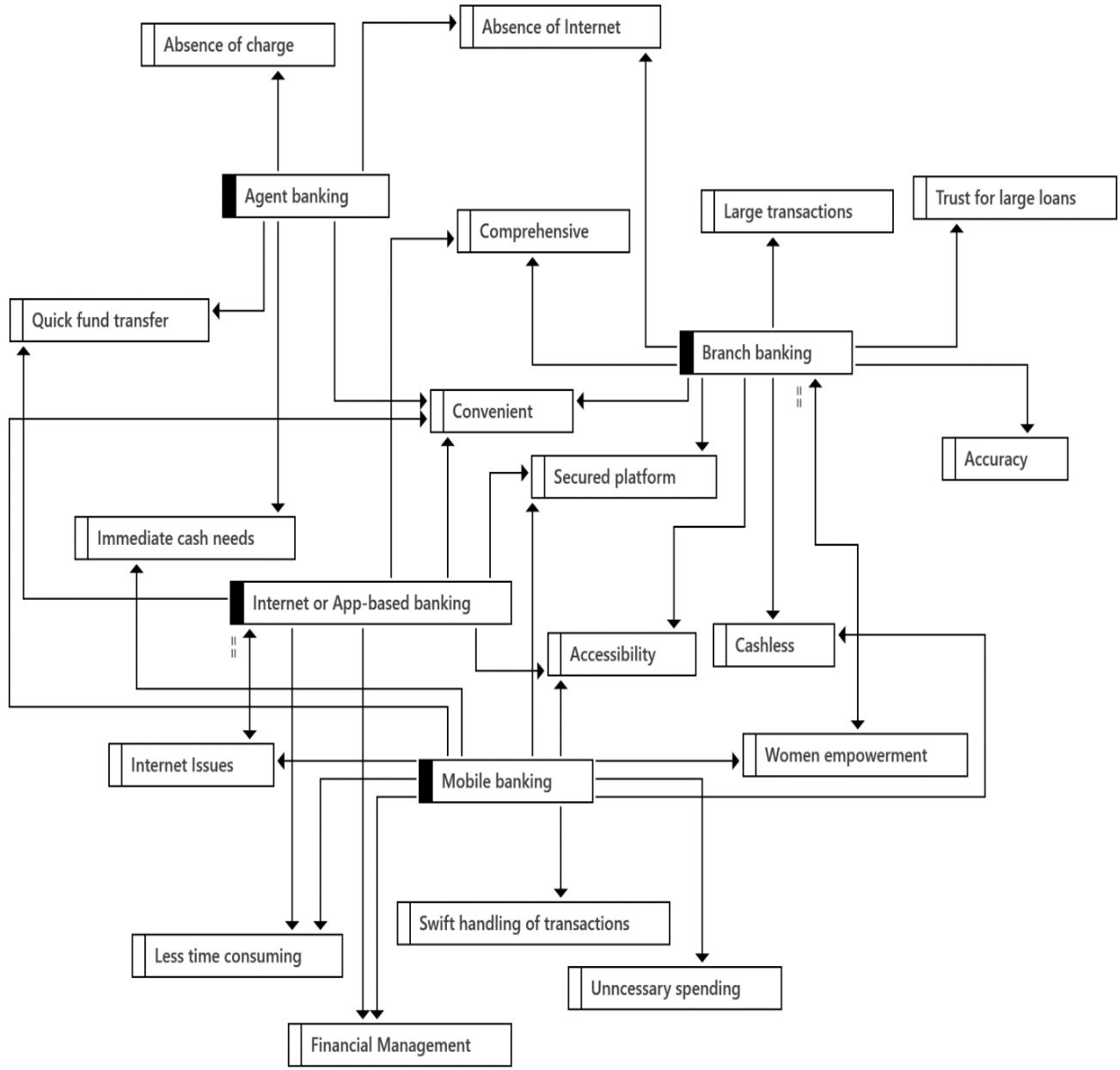

### b) Challenges faced by the females

This paper delves into women's challenges in accessing banking services across systems. We explore the following five key themes, which encapsulate the multiple barriers shown in figure 2.

## i. Digital Literacy and Accessibility

Navigating the Internet or app-based banking systems can be confusing, unfamiliar, and complex for women. Issues such as Internet errors, technical errors, and security problems add to this complexity. The absence of the Internet in certain areas further limits accessibility to digital banking services, impacting women disproportionately.

Figure 2: Challenges encountered by female users

Source:Authors'analysis

## ii. Security and Trust

Security concerns, including password issues and potential security breaches, are significant barriers to women's adoption of Internet or app-based and mobile banking. Women may be more cautious about engaging in digital transactions due to concerns about data privacy and online security.

## iii. Service Coverage and Features

Across various banking systems, women encounter challenges related to limited service coverage, especially in rural or underprivileged areas. The absence of essential features like medical facilities in mobile banking apps highlights a gap in addressing women's specific needs. The lack of foreign transactions and extensive loan facilities further restricts the utility of banking services for women, limiting their financial empowerment and mobility.

## iv. Cost and Time Constraints

High transaction costs associated with mobile banking services and the opportunity cost of time spent in branch banking pose significant challenges for women, particularly those from low-income thresholds. Time-consuming processes and limited service availability in agent banking further compound women's financial burdens, constraining their ability to access and utilize banking services effectively.

## v. Adaptation and Support

Women encounter difficulties adapting to digital technologies and navigating complex banking systems, reflecting broader socio-cultural barriers and systemic inequalities. Insufficient support mechanisms and a lack of trained service agents exacerbate these challenges, hindering women's capacity to engage in formal financial transactions and decision-making processes. Enhancing financial literacy programs and providing targeted support services are essential to fostering women's financial autonomy and promoting inclusive banking practices.

Through this analysis, this paper underscores the need for comprehensive policy interventions and institutional reforms to address systemic barriers and promote women's financial inclusion. By introducing digital literacy initiatives, enhancing security protocols, expanding service coverage, and mitigating cost constraints, policymakers and financial institutions can create more inclusive and equitable banking environments that empower women and advance socioeconomic development globally.

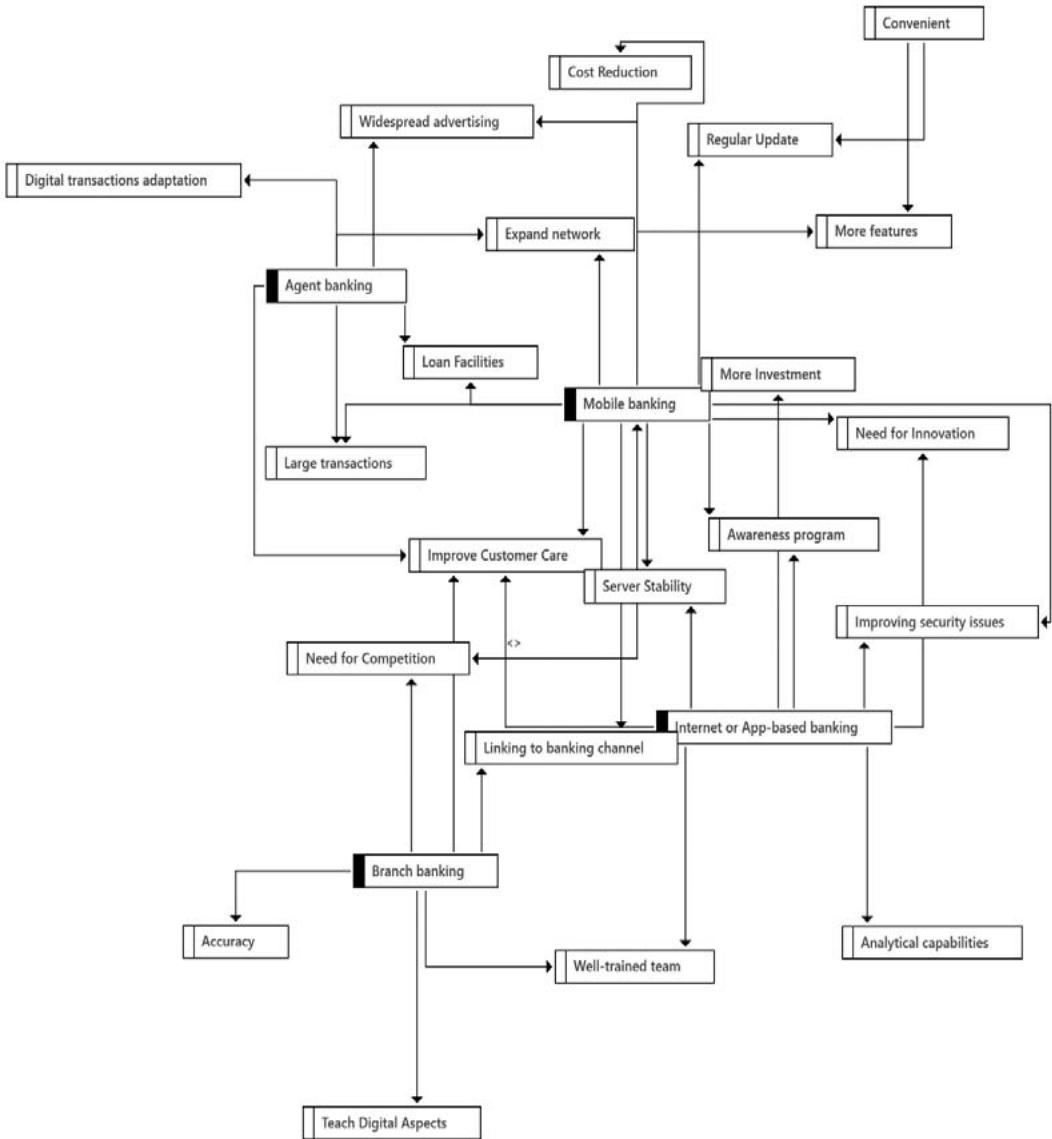

### c) Expectations of Females

The agent banking system needs to adapt to digital transactions by implementing user-friendly methods, such as mobile wallets, QR code payments, etc. They may also offer incentives for customers and agents to promote digital transactions. They must also expand the network by identifying underserved areas and incentivising agents to establish in rural areas. Moreover, they may adopt multiple channels for widespread advertisement of the benefits of agent banking. As women nowadays get used to doing business, they need large transactions and loan facilities from the banks. Therefore, this system is expected to offer these facilities by implementing a robust verification process, clear guidelines, collaboration with financial institutions, and streamlining loan application and approval processes.

Source:Authors'analysis Figure 3: Expectations of females

Branch banking encompasses a wide range of aspects within its operational framework. It requires an inclusive effort to educate the stakeholders on digital components to ensure the seamless integration of digital services alongside conventional banking activities. Moreover, the agents need to be well-informed about the policies and guidelines of the banks. Meanwhile, it is seen that male agents dominate this system, although a proficient female team has the potential to make a significant contribution to a diverse and inclusive work environment. The escalating competition stimulates innovation, urging branches to enhance their services and offerings continuously. Branches must prioritize improved customer care, foster robust relationships, and address concerns promptly.

Internet or app-based banking systems need more analytical capabilities to provide insights into customer behaviour and preferences. A well-trained and technologically proficient team is required to ensure seamless online operation and protect customer information. Investment in infrastructure and technology is crucial for keeping servers stable and optimizing user experience, especially for banks that have yet to introduce their software for banking from home. Like other banking systems, an awareness program is required to inform customers about the existence of this banking system, the benefits of digital banking, and data protection. In addition, continuous innovation is vital to develop new features and functionalities to make this banking system modern and popular.

Mobile banking allows users to engage in a multitude of financial transactions on the go, facilitating convenience and accessibility. Although several mobile banking companies offer diversified features throughout the country, they are expected to enable extensive transaction facilities, expand their network, and reduce costs while sending money and cashing out digital money. In addition, more investment in innovation and security grounds is necessary as the likelihood of fraud and scams exists. Further, as mobile banking users are from diverse backgrounds and areas, educating all users about the proper use of services and ways of avoiding scams is essential. The emphasis on server stability, improved customer care, and healthy competition is indispensable to deliver a seamless and secure banking experience for modern financial management.

## V. CONCLUSIONS

In conclusion, this study sheds light on Bangladesh's financial and banking systems, which have been influenced by different factors that shape the choices of its users. Through this study, we have examined women's perceptions of defining their banking choices. We have investigated and found different significant factors that catalyze their banking preferences. It was discovered in this research that both the benefits and challenges of financial systems work behind shaping the banking behaviours of women. The study identifies that quick and easy accessibility was one of the most significant factors besides efficient economic management, transaction efficiency, security and empowerment.

Additionally, the challenges faced by women in using banking systems were highlighted here as lack of digital literacy, time and cost constraints, limited service coverage, adaptation complexity and support. The study uncovered women's expectations of their preferred banking choices through the qualitative interview method, such as enhancing widespread advertisement, improving security issues, establishing server stability, reducing cost, expanding networks, adding more features, etc. For a more inclusive financial landscape, this study emphasizes the need for an accelerated effort to redesign a banking system that will work for all women of Bangladesh and will be a catalyst for worthwhile financial inclusion.

Our findings suggest that regulators must encourage using agent banking systems for digital transactions by providing user-friendly incentives such as mobile wallets and QR code payments. Additionally, expanding the networks to reach underserved areas and motivating agents to operate in rural locations is paramount. Well-defined protocols and close cooperation with financial institutions are essential to streamline significant transactions and loan provisions, especially for female entrepreneurs. Alongside, banking professionals should prioritise teaching stakeholders about digital components, guaranteeing adherence to regulations and procedures. Besides, they need to promote diversity by actively supporting female involvement.

Moreover, sustained innovation is crucial for improving services and maintaining competitiveness. Internet and app-based banking systems necessitate investment in analytical skills, infrastructure, and technology to enhance user experience and safeguard client information. Customer education programs are crucial for raising awareness about the advantages and safety measures of digital banking. Mobile banking service providers need to prioritize the facilitation of substantial transactions, the expansion of their networks, the reduction of costs, and the investment in innovation and security measures to limit the dangers of fraud. It is crucial to provide education on correct usage and avoidance of scams, as well as to ensure the reliability of servers, enhance customer support, and foster healthy competition to create a banking experience that is smooth and secure for all users. While this study aimed to investigate the banking choices of females based on the status quo and challenges, it is essential to acknowledge the limitation regarding the sample's representativeness. The sample consisted of purposively selecting 30 females from diversified backgrounds, which might result in inadequate expression of banking experience of women. Future research could address this limitation by employing more diversified sampling to ensure higher representativeness.

### Appendix 2: Questions

1. What is your name and profession?

2. Do you use digital banking services?

3. Which service you usually use for transactions among branch banking, mobile banking, agent banking, app or internet-based banking?

4. What are the catalysts behind adopting this service?

5. What kind of challenges you usually face while using this service?

6. What is your expectation from the service providers?

Generating HTML Viewer...

References

52 Cites in Article

A,A Subramanian,R (2022). Current Status of Research on Mobile Banking: An Analysis of Literature.

Omolola Adeoye‐olatunde,Nicole Olenik (2021). Research and scholarly methods: Semi‐structured interviews.

Jashim Ahmed,Asma Ahmed (2018). Agrani Doer Banking: Agent Banking Business in Bangladesh.

M Akash,Md. Jahid,Md Habib (2022). An overview of Study on Mobile Banking in Bangladesh: Area of Rangpur Division.

S Akoil (2022). Branchless Banking: Opportunities and implementation Challenges in Bangladesh Context.

M Alonso-Dos-Santos,Y Soto-Fuentes,V Valderrama-Palma (2020). Determinants of Mobile Banking Users’ Loyalty.

M Ashraf (2023). Comprehending rural people's intention of rural people to use branchless banking during the corona pandemic: Evidence from Bangladesh.

Faisal Aziz,Salman Sheikh,Ijaz Shah (2022). Financial inclusion for women empowerment in South Asian countries.

M Babbar,S Agrawal,D Hossain,M Husain (2023). Adoption of digital technologies amidst COVID-19 and privacy breach in India and Bangladesh.

Moumita Bhowmik,Fardeen Ashraf,Tashfia Fatema,Faria Habib,Md Kabir,Iyolita Islam,Muhammad Islam (2023). Evaluating Usability of Mobile Financial Applications Used in Bangladesh.

M Bhuiyan,M Imran,A Rahid (2022). DIGITAL COMPETITIVENESS IN THE BANKING SECTOR OF BANGLADESH.

Rumana Biswas,Anika Mou,Afsana Yasmin,Md. Zonayet,Nahid Hossain (2022). WOMEN PARTICIPATION IN AGRICULTURE OF BANGLADESH.

Ayu Budiarti,Eriska Wulandari,Rita Rodiah,Uli Anjani,Rama Rozak,Heni Mulyani (2023). Perspektif Mahasiswa Terhadap Transaksi Digital dalam Penggunaan Mobile Banking.

Sharon Buteau,Preethi Rao,Fabrizio Valenti (2021). Emerging insights from digital solutions in financial inclusion.

R Chakraborty,R Abraham (2023). THE INFLUENCE OF FINANCIAL INCLUSION ON DIMENSIONS OF WOMEN'S EMPOWERMENT: EVIDENCE FROM KERALA STATE, INDIA, AND CHITTAGONG DIVISION, BANGLADESH.

T Chakrobortty,M Sultana (2023). Financial Inclusion for Rural Community in Bangladesh through Agent Banking.

A Das,L Brown,A Mcfarlane (2023). Asymmetric Effects of Financial Development on CO2 Emissions in Bangladesh.

Rosalind Edwards,Janet Holland (2020). Reviewing challenges and the future for qualitative interviewing.

A Fitriati,C Ardiani,H Pramono,B Pratama,R Mudjiyanti (2022). Investigating The Determinants of Mobile Banking Usage.

Apostolos Giovanis,Pinelopi Athanasopoulou,Costas Assimakopoulos,Christos Sarmaniotis (2019). Adoption of mobile banking services.

I Hasan,Md Habib (2022). Mobile Banking Financial Solution for Blockchain-Powered Agri-Food Supply Chain (ASC).

M Hasan (2020). M-Banking: The Transaction Revolution in Bangladesh.

Md Hassan,Md Islam,M Yusof,H Nasir,N Huda (2023). Investigating the Determinants of Islamic Mobile FinTech Service Acceptance: A Modified UTAUT2 Approach.

M Hayat,M Hossain,(n.D A Case Study On Customer Satisfaction Towards Online Banking In Bangladesh.

A Herawati,Sarwani,I Gustaman (2021). Sikap Nasabah dan Kinerja Atribut Produk Mobile Banking.

Mohammed Hoque,Nazneen Chowdhury,Al Hossain,Tanjim Tabassum (2024). Social and facilitating influences in fintech user intention and the fintech gender gap.

Md. Hoque (2023). Fintech’s game-changing opportunities for SMEs: A study on selected SMEs in Bangladesh.

Mohammad Islam,Prince Das,Mahbub Alam,Md. Hanif (2022). Financial Supply Chain & its Implementation in the Banking Sectors of Bangladesh.

Md. Kabir,S Huda,Omar Faruq (2021). MOBILE FINANCIAL SERVICES IN THE CONTEXT OF BANGLADESH.

Ummay Khanam (2022). Agent Banking: An Agent of Financial Inclusion in Bangladesh.

Manisha Kumari (2023). Fostering Women Empowerment through Financial Inclusion in India.

Jean Lee,Jonathan Morduch,Saravana Ravindran,Abu Shonchoy (2022). Narrowing the gender gap in mobile banking.

H Moghadam,A Karami (2023). Financial inclusion through FinTech and women's financial empowerment.

Md. Moniruzzaman,Dr. Sha’ari Abd Hamid,Dr. Abu Sofian Yaacob,Dato’ Dr. Mohd Padzil Hashim (2023). Financing by the Encashment of Trade Receivables through Trade Receivable Exchange in Bangladesh.

Zarin Moon,Md. Hasan (2022). Impact of COVID-19 on Green Financial Practices of Banks and Financial Institutions in Bangladesh.

Syed Moudud-Ul-Huq,Shumaila Perhiar (2023). What Factors Need to Be Considered for Adopting M-Banking Services in a Developing Economy?.

K Nawrin,A Bushra,N Nisha (2020). Agent Banking and Financial Inclusion: The Case of Bangladesh.

Putri Prasetyaningrum,Purwanto Purwanto,Adian Rochim (2022). Gamification On Mobile Banking Application: A Literature Review.

M Rahman,M Khan (2020). Investigating the Effect of Women's Position on Advancement in the Banking Sector of Bangladesh.

Y Rohanifar,S Sultana,S Nandy,P Saha,Md Chowdhury,M Al-Ameen,S Ahmed (2022). ACM SIGCAS/SIGCHI Conference on Computing and Sustainable Societies (COMPASS).

Soma Dey,Sacchidanand Majumder (2024). Determinants influencing the adoption of mobile banking by women in Bangladesh.

R Sharma,A Deo,A Awasthi (2022). PAYMENT APPLICATIONS AND CHANGING TRENDS OF BANKING.

Y Shen (2022). Comment on "Measuring Digital Financial Inclusion in Emerging Market and Developing Economies: A New Index.

Nikhil Shil,Anup Chowdhury (2021). Public Financial Management Systems in Bangladesh: An Ideological Review.

Dr. Shrivastava,Dr. Shah (2021). Determinants of cross selling through mobile apps in Indian Banks – A Factor Analysis Approach.

Md. Siddiquie (2014). Agent banking, the revolution in financial service sector of Bangladesh.

Michael Siek,Luin Rukma (2022). Impact Analysis of Digital Banking Applications on Disrupting Traditional Banking Industry.

P Singh,K Singh (2023). FINANCIAL INCLUSION-A FRONT WHEEL FOR WOMENS EMPOWERMENT.

J Solotaroff,A Kotikula,T Lonnberg,S Ali,R Pande,F Jahan (2019). Voices to choices: Bangladesh's journey in women's economic empowerment.

Jinal Thakkar,Pooja Rao,Kumar Shubham,Vaibhav Jain,Dinesh Jayagopi (2022). Understanding Interviewees’ Perceptions and Behaviour towards Verbally and Non-verbally Expressive Virtual Interviewing Agents.

M Toyon (2023). Navigating Digital Inequality: Examining Factors Affecting Rural Customers' Internet Banking Adoption in Post-COVID Bangladesh.

K Uddin,T Begum (2023). Financial Inclusion: Factors Influencing on Customer Adoption of Mobile Banking Services in Bangladesh.

No ethics committee approval was required for this article type.

Data Availability

Not applicable for this article.

How to Cite This Article

Fatema Tuz Zuhora. 2026. \u201cDigital Dividends: Redefining Banking Choices of Women in Bangladesh\u201d. Global Journal of Management and Business Research - C: Finance GJMBR-C Volume 24 (GJMBR Volume 24 Issue C1).

Explore published articles in an immersive Augmented Reality environment. Our platform converts research papers into interactive 3D books, allowing readers to view and interact with content using AR and VR compatible devices.

Your published article is automatically converted into a realistic 3D book. Flip through pages and read research papers in a more engaging and interactive format.

Our website is actively being updated, and changes may occur frequently. Please clear your browser cache if needed. For feedback or error reporting, please email [email protected]

Thank you for connecting with us. We will respond to you shortly.