The Great Depression was a worldwide economic downturn that began in 1929 and lasted until about 1939. It was the longest and most severe financial crisis ever experienced by the Western World, sparking fundamental changes in economic institutions, macroeconomic policy, and economic theory. Although it originated in the United States, the Great Depression caused drastic declines in output, severe unemployment, and acute deflation in almost every country of the world. The timing and severity of the Great Depression varied substantially across countries. The Depression was particularly long and severe in the United States and Europe however, it was milder in Japan and Latin America. The Great Depression caused enormous hardship for tens of millions of people and the failure of a large fraction of the nation’s banks, businesses, and farms.

## I. INTRODUCTION

The Great Depression, originating from the Wall Street Crash of 1929, cast a profound shadow over the world economy, triggering a cascade of effects and adverse conditions that reverberated across nations.

The interconnectedness of global economies meant that the economic downturn in one region swiftly translated into widespread suffering and instability.

One of the immediate effects was the contraction of international trade. The Smoot-Hawley Tariff Act of 1930, was initially designed to protect American industries by imposing higher tariffs on imported goods backfired spectacularly. Other nations responded with retaliatory tariffs, leading to a sharp decline in global trade. Protectionist measures, instead of shielding economies, intensified the economic downturn by stifling international commerce.

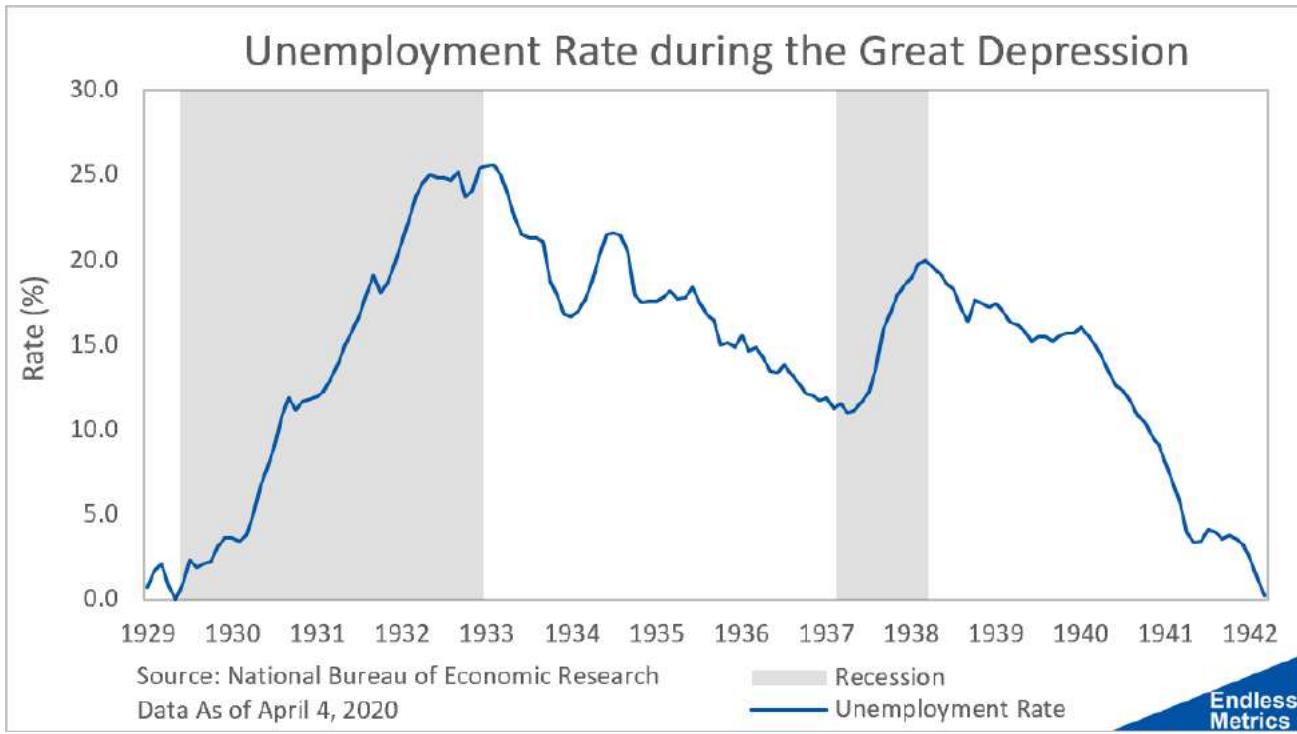

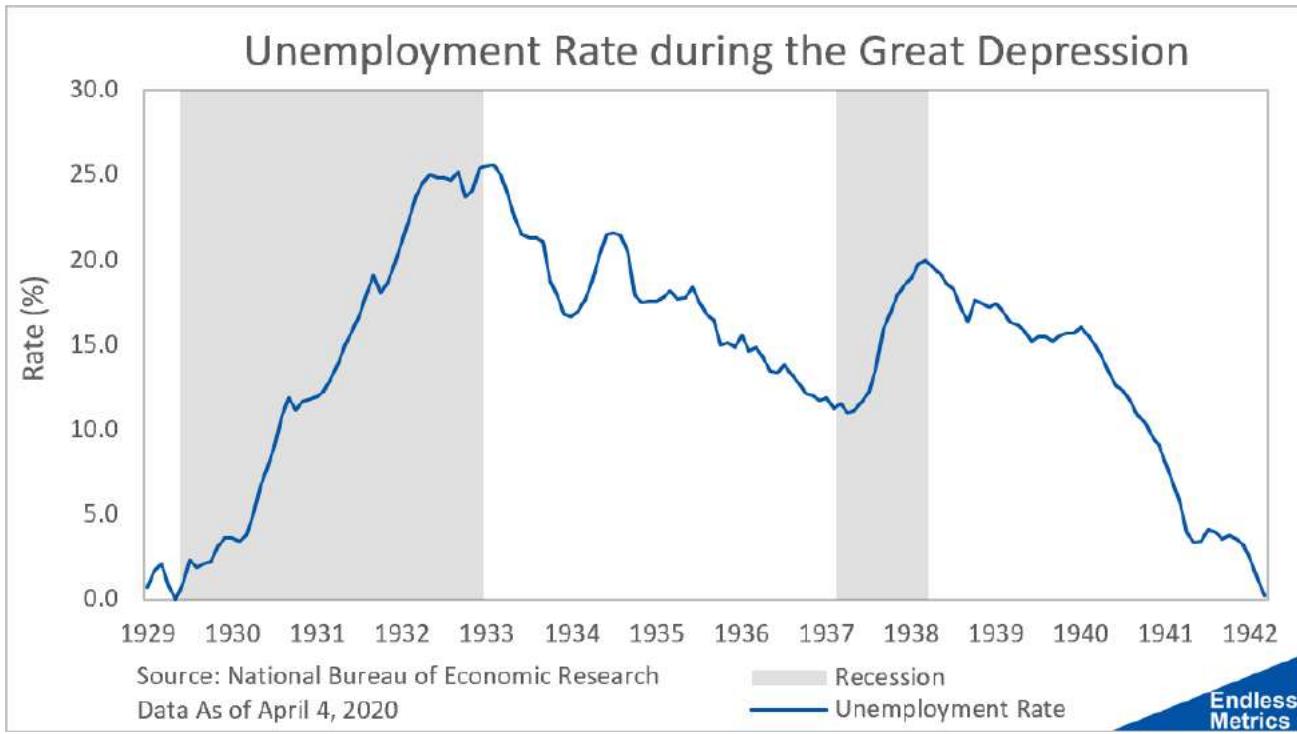

Unemployment soared to unprecedented levels in many nations. In the United States, the epicenter of the crisis, millions of individuals found themselves without jobs in industrial production plummeted. This spike in unemployment had a domino effect, impacting consumer spending and exacerbating the economic downturn. Similar patterns emerged in European countries, with Germany experiencing severe unemployment rates and economic hardships that contributed to social and political unrest.

The banking sector faced a perilous situation, with numerous financial institutions collapsing under the weight of the economic crisis. Bank failures led to a contraction of credit, making it challenging for businesses to secure loans and hinder economic recovery. The financial panic instilled a pervasive sense of uncertainty, further dampening economic activities globally.

Social conditions deteriorated as a result of the economic hardships. Homelessness, poverty, and destitution became widespread, particularly in industrialized nations. The plight of the unemployed and disenfranchised fueled social unrest, contributing to political upheavals and the rise of extremist ideologies. In Germany, the economic turmoil facilitated the ascent of Adolf Hitler and the Nazi Party, capitalizing on widespread discontent.

Internationally, the Great Depression catalyzed geopolitical tensions. Economic hardships fueled nationalistic sentiments and isolationist policies as nations sought to prioritize their own interests. This inward turn contributed to strained diplomatic relations, hindering international cooperation and exacerbating global political instability.

The conditions sparked by the Great Depression set the stage for a revaluation of economic and political systems. In response to the crisis, nations began to reassess the role of government intervention in the economy. Keynesian economic theory gained prominence, advocating for government spending to stimulate demand and alleviate economic downturns. Social safety nets and labor regulations were also instituted to mitigate the impact of economic shocks on vulnerable populations.

The Great Depression, with its far-reaching consequences, underscored the imperative for collaborative international efforts to address economic challenges. It laid the groundwork for the establishment of institutions like the International Monetary Fund (IMF) and the World Bank, aimed at fostering economic stability and preventing a recurrence of such widespread financial crises in the future. The lessons learned during this tumultuous period significantly influenced the development of economic policies and international relations in the subsequent decades.

## II. EVENTS WHICH LEAD TO THE SITUATION AT HAND/PAST ECONOMIC POLICY

- Post-World War I Economic Turmoil

- After the conclusion of World War I in 1918, nations faced the challenges of reconstruction and economic recovery. The war had left Europe economically devastated, with many nations burdened by war debts and reparations.

- Rise of Protectionist Policies

In the aftermath of World War I, some nations, including the United States, adopted protectionist trade policies to shield domestic industries from foreign competition. The desire to protect local economies contributed to the emergence of tariffs and trade restrictions.

The Roaring Twenties

The 1920s, known as the "Roaring Twenties" in the United States, were characterized by economic prosperity, technological advancements, and increased consumer spending. However, this period of apparent affluence masked underlying economic imbalances and unsustainable practices.

Stock Market Boom

The U.S. stock market experienced a period of exuberant growth during the 1920s. Investors, fueled by optimism and speculative fever, engaged in rampant buying, driving stock prices to unprecedented highs.

- Wall Street Crash - October 29, 1929

The culmination of speculative excesses and economic imbalances came to a head with the Wall Street Crash of 1929. On "Black Tuesday," October 29, 1929, the U.S. stock market collapsed, wiping out billions of dollars in wealth. The crash marked the beginning of the Great Depression.

Bank Failures and Financial Panic

The stock market crash triggered a wave of bank failures and a financial panic. The loss of confidence in the banking system led to mass withdrawals, causing banks to collapse. The ensuing contraction of credit further deepened the economic crisis.

Global Economic Impact

The economic repercussions of the U.S. stock market crash reverberated worldwide. International trade declined, and economies across the globe entered into a synchronized contraction. Nations that were heavily dependent on exports suffered immensely.

Dust Bowl - Early 1930s

Concurrently, a severe environmental disaster known as the Dust Bowl struck the American Midwest. Prolonged drought, combined with poor agricultural practices, led to massive dust storms, damaging crops and exacerbating economic distress in the region.

- Smoot-Hawley Tariff Act - June 1930

- In an attempt to protect American farmers and industries, the U.S. Congress passed the Smoot-Hawley Tariff Act in June 1930. The act significantly raised tariffs on imported goods, contributing to a global increase in protectionist measures.

- Rise of Protectionism and Political Extremism

- The adoption of protectionist policies, including the Smoot-Hawley Act, had unintended consequences. It not only hindered international trade but also contributed to the rise of political extremism, particularly in Germany with the ascent of Adolf Hitler.

- Impact on the Weimar Republic and the rise of Adolf Hitler

The economic hardships and protectionist policies, coupled with the lingering effects of World War I, contributed to the rise of political extremism, exemplified by the ascent of Adolf Hitler in Germany. The economic repercussions, including the political and economic instability in Germany, paved the way for the rise of Hitler, as the Weimar Republic struggled to recover.

The economic downturn, coupled with the impact of protectionist measures, undermined the fragile stability of the Weimar Republic in Germany. Economic hardships paved the way for the rise of extremist ideologies.

Global Economic Decline Continues - 1931 As the economic downturn persisted, nations struggled to find effective solutions. By the freeze date of 27th January 1931, the world was mired in a deepening economic crisis, marked by deflation, unemployment, and social upheaval.

### Timeline

1. Stock Market Crash (Wall Street Crash - 1929): October 29, 1929: The Wall Street Crash, a catastrophic stock market collapse, triggered the the onset of the Great Depression. Stock values plummeted, leading to a severe economic downturn.

2. Dust Bowl Crisis (1930-1936): Concurrently, the Dust Bowl crisis emerged in the U.S., causing widespread agricultural devastation due to severe drought and poor land management practices.

3. Smoot-Hawley Tariff Act (June 17, 1930): The Smoot-Hawley Tariff Act was signed into law, raising tariffs on imported goods by $40 - 60\%$. Intended to protect domestic industries, it inadvertently worsened the global economic situation.

4. Impact on Protectionism and Rise of Isolationism (1930s): The protectionist measures of the Smoot-Hawley Act contributed to a rise in protectionism globally, hindering international trade and fostering isolationist tendencies, particularly in the USA.

## III. KEYNESIAN ECONOMICS

Keynesian economics, developed by British economist John Maynard Keynes during the 20th century, is a macroeconomic theory that significantly influenced economic policies worldwide. Keynes challenged classical economic thought, which emphasized the self-regulating nature of markets and minimal government intervention.

Keynesian economics revolves around the idea that during economic downturns, governments should actively intervene to stimulate demand and promote economic recovery. Keynes argued that when private-sector spending is insufficient to maintain full employment, government spending and policies could fill the gap. This perspective gained prominence during the Great Depression of the 1930s. Central to Keynesian theory is the concept of aggregate demand, representing the total spending on goods and services in an economy. Keynes asserted that fluctuations in aggregate demand, particularly inadequate demand during recessions could lead to unemployment and economic stagnation. In response, he proposed counter-cyclical policies to manage demand.

Keynesian economics advocates for expansionary fiscal policy during economic slumps, involving increased government spending or tax cuts to boost demand. This counters the downturn and supports job creation. Conversely, during periods of high inflation or economic overheating, Keynesians recommend contractionary fiscal policies, such as reducing government spending or increasing taxes, to cool the economy.

Monetary policy also plays a role in Keynesian economics. By adjusting interest rates and influencing the money supply, central banks aim to stabilize the economy. Lowering interest rates encourages borrowing and spending, while higher rates can curb inflation.

Keynesian ideas found widespread application after World War II, shaping the economic policies of many developed nations. However, the rise of monetarism and supply-side economics in the late $20^{\text{th}}$ century led to challenges to Keynesian orthodoxy. Despite debates over policy effectiveness, Keynesian economics remains influential, especially during periods of economic crises when governments often adopt stimulus measures to revive growth and employment. The 2008 global financial crisis and the COVID-19 pandemic prompted renewed interest in Keynesian-style interventions to address economic challenges.

## IV. CLASSICAL ECONOMICS

Classical economics, dominant before the 20th century, laid the groundwork for economic thought, emphasizing laissez-faire principles and the belief in self-regulating markets. Its relevance extended into the years leading up to the freeze date of 1931, impacting economic policies and shaping the global financial landscape.

At its core, classical economics asserted that markets naturally reach equilibrium, ensuring full employment and optimal resource allocation without government interference. It was rooted in the ideas of influential economists like Adam Smith and David Ricardo.

Laissez-Faire Ideology: Classical economists advocated for minimal government intervention, arguing that markets if left unhindered, would efficiently allocate resources. The "invisible hand" concept, introduced by Adam Smith, suggested that individuals pursuing self-interest unintentionally contribute to the collective good.

Gold Standard and Free Trade: During this period, the gold standard was a key feature of classical economic policies. Currencies were backed by gold, giving a currency both stability and legitimacy. Additionally, classical economists supported free trade, believing it maximized global efficiency and prosperity.

However, the perception of classical economics changed tack at the time of the great depression. The classical insistence on market self-regulation faced scrutiny as the Great Depression unfolded.

Governments, constrained by classical ideologies, found it challenging to address the economic crisis effectively. The gold standard, once a symbol of stability, became a constraint in responding to the turmoil.

<table><tr><td></td><td>Keynesian view</td><td>Monetarist view</td></tr><tr><td>Fiscal policy</td><td>In recession, expansionary fiscal policy can stimulate economic activity</td><td>Fiscal policy causes no long-term increase in real output</td></tr><tr><td>Wage rigidity</td><td>Wages can be sticky downwards causing unemployment</td><td>In absence of min wages/ trade unions wages flexible.</td></tr><tr><td>Unemployment</td><td>Demand-deficient unemployment big causes</td><td>Tend to emphasis supply-side unemployment (natural rate)</td></tr><tr><td>Phillips Curve</td><td>There is a trade off between unemployment and inflation</td><td>Only a trade-off in the short-term.</td></tr><tr><td>Government borrowing</td><td>In recession, governments should borrow more to offset fall in private spending</td><td>Government should seek to run balanced budget</td></tr><tr><td>Crowding out</td><td>No crowding out in recession</td><td>Government borrowing causes more crowding out</td></tr></table>

To conclude, the Great Depression is considered a turning point in world history that altered social, political, and economic spheres for many years to come. Its roots can be traced back to the 1929 Wall Street Crash, which caused immense instability to spread throughout many countries. Because the world's economies are intertwined, a decline in one area's economy can have immediate effects on other parts of the world. The Smoot-Hawley Tariff Act is a prime example of protectionist policies that were intended to protect home industries, but they made matters worse by restricting international trade. Geopolitical tensions and political extremism were fostered by the collapse of banks, a sharp increase in unemployment, and worsening social conditions. Political and economic systems were reevaluated as a result of the Great Depression. In response, the theory of Keynesian economics developed, urging government action to boost demand and lessen economic downturns. With its focus on laissez-faire principles, classical economics came under fire as governments tried to handle the crisis within its bounds. In addition, the Great Depression highlighted the necessity of cooperative global endeavors to tackle economic obstacles. In the aftermath of it, organizations like the World Bank and the International Monetary Fund (IMF) were founded to promote economic stability and avert further financial crises. Ultimately, the lessons learned from the Great Depression significantly influenced the development of economic policies and international relations in the subsequent decades. Thinking back on this turbulent time, we are reminded of how crucial cooperation, alertness, and flexible policymaking are when negotiating unpredictable economic conditions.

Generating HTML Viewer...

Funding

No external funding was declared for this work.

Conflict of Interest

The authors declare no conflict of interest.

Ethical Approval

No ethics committee approval was required for this article type.

Data Availability

Not applicable for this article.

How to Cite This Article

Tanish Singh. 2026. \u201cA detailed analysis of The Great Depression\u201d. Global Journal of Human-Social Science - E: Economics GJHSS-E Volume 24 (GJHSS Volume 24 Issue E3): .

Explore published articles in an immersive Augmented Reality environment. Our platform converts research papers into interactive 3D books, allowing readers to view and interact with content using AR and VR compatible devices.

Your published article is automatically converted into a realistic 3D book. Flip through pages and read research papers in a more engaging and interactive format.

The Great Depression was a worldwide economic downturn that began in 1929 and lasted until about 1939. It was the longest and most severe financial crisis ever experienced by the Western World, sparking fundamental changes in economic institutions, macroeconomic policy, and economic theory. Although it originated in the United States, the Great Depression caused drastic declines in output, severe unemployment, and acute deflation in almost every country of the world. The timing and severity of the Great Depression varied substantially across countries. The Depression was particularly long and severe in the United States and Europe however, it was milder in Japan and Latin America. The Great Depression caused enormous hardship for tens of millions of people and the failure of a large fraction of the nation’s banks, businesses, and farms.

Our website is actively being updated, and changes may occur frequently. Please clear your browser cache if needed. For feedback or error reporting, please email [email protected]

Thank you for connecting with us. We will respond to you shortly.