The goal of this paper was to produce predictions regarding the future stock price of the massive corporation Apple Inc. The Information Technology (IT) sector comprises six distinct industries, among which Apple Inc., which is a large-cap company, has been the mainstay of my research. Apple Inc. is one of the most valuable companies in the world, with a market capitalization of over $2 trillion. In the study, a predictive model has been devised to estimate the equity price of the Apple Inc. company, employing diverse statistical techniques. A variety of statistical methods to examine 23 observations using time series data from FactSet-2022 has been used in this study. Graphical techniques including histograms, dissipate plots, and line plots were used to outwardly investigate the dataset, while elucidating insights were utilized to sum up the attributes of versatile factors like Value, EPS, BVPS, CR, DTA, EBIT, and SPS.

## I. INTRODUCTION

The goal of this paper was to produce predictions regarding the future stock price of the massive corporation Apple Inc. by using statistical models.

models. The Information Technology (IT) sector comprises six distinct industries, among which Apple Inc., which is a large-cap company has been the mainstay of my research. Apple Inc. is one of the most valuable companies in the world, with a market capitalization of over $2 trillion. In the study, a predictive model has been devised to estimate the equity price of the Apple Inc. company, employing diverse statistical techniques.

The model can be used by investors and analysts to make informed decisions about investing in Apple Inc. and to predict its future performance.

## II. PREVIOUS RESEARCH

Predicting equity prices is a significant issue in financial research, especially in the Information Technology (IT) sector, where businesses such as Apple Inc. hold significant influence. This literature study evaluates current research on constructing statistical models for predicting Apple Inc.'s share price using regression analysis in the IT industry.

The impact of market opinion on the stock returns of Apple Inc., providing an understanding of issues affecting its equity price has been considered in this study [1]. For developing statistical models, especially in financial forecasting, [2] this original textbook offers foundational knowledge on econometrics, including regression analysis. The association between Apple Inc.'s financial performance and its stock price movements, providing perceptions to prospective forecasters for regression analysis has been demonstrated in this study [3]. This study [4] combined regression modeling to forecast changes in the company's stock price based on company performance metrics and its financial data. Regression analysis has been applied in this empirical study [5] to explore the relationship between several financial variables and Apple Inc. stock returns. By concentrating on challenges associated with regression analysis, such as multicollinearity and model overfitting a comprehensive guide has been provided this paper [6]. This review [7] explores the use of sentiment analysis of social platforms like Twitter data to predict stock prices, offering potential further predictors for regression analysis. This study [8] provides on the parameters that

affect volatility and stock returns, which may assist in determining which variables should be considered in a regression analysis. Tsay's book [9] provides sophisticated approaches for evaluating financial time series data, including methods relevant to regression analysis for predicting equities prices. Not only emphasizing Apple Inc., but this research paper also predicted the trend pattern by using machine learning techniques such as Support Vector Machine (SVM) that could be perfect for regression analysis in forecasting equity prices [10].

## III. METHODOLOGY

The data has been taken from FactSet-2022 and it is time series data. The data is secondary data and

there were 23 observations in the dataset. Generally, several statistical techniques have been used in this research project. For graphical techniques, histograms, scatter plots, line plots, and as analytical methods, three types of statistical tools have been used. I have used descriptive statistics for scalable variables (Price, EPS, BVPS, CR, DTA, EBIT, SPS) and to measure the linear association, I have used correlation, and finally to predict the model regression analysis. I have stated R as the scripting language.

The functional specification, population regression equation, and sample regression equation have been shown in the following Eqns. 1, 2 and 3.

$$

+ \quad + \quad +

$$

Eqn. 1 Price $= \mathrm{f}$ (BVPS, EBIT, SPS)

Eqn. 2 $\mathrm{Price} = \alpha +\beta_{\mathrm{BVPS}}^{*}\mathrm{BVPS} + \beta_{\mathrm{EBIT}}^{*}\mathrm{EBIT} + \beta_{\mathrm{CR}}^{*}\mathrm{SPS} + \varepsilon$

Eqn. 3 $\mathrm{Price} = \mathrm{a}\mathrm{b}_{\mathrm{BVPS}}^{*}\mathrm{BVPS} + \beta_{\mathrm{EBIT}}^{*}\mathrm{EBIT} + \beta_{\mathrm{CR}}^{*}\mathrm{SPS} + \mathrm{e}$

In the above multiple regression equations, price is the dependent variable which was hypothesized to be a positive function on independent variables respectively book value per share (BVPS), earnings before interest and taxes (EBIT) and sell per share(SPS).

## IV. RESULTS

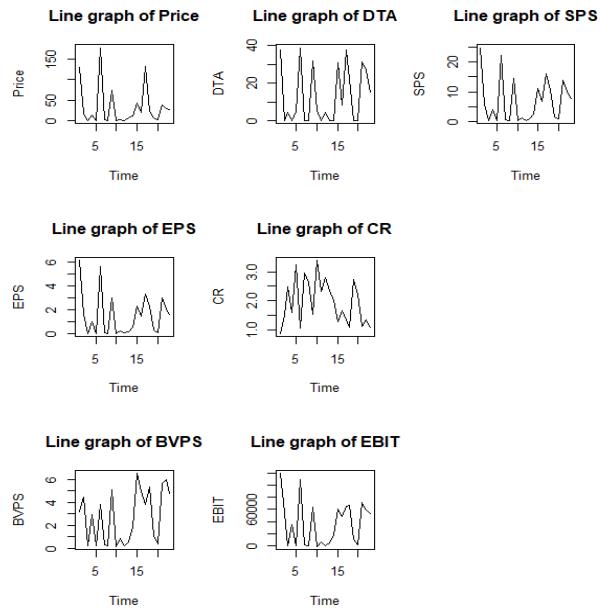

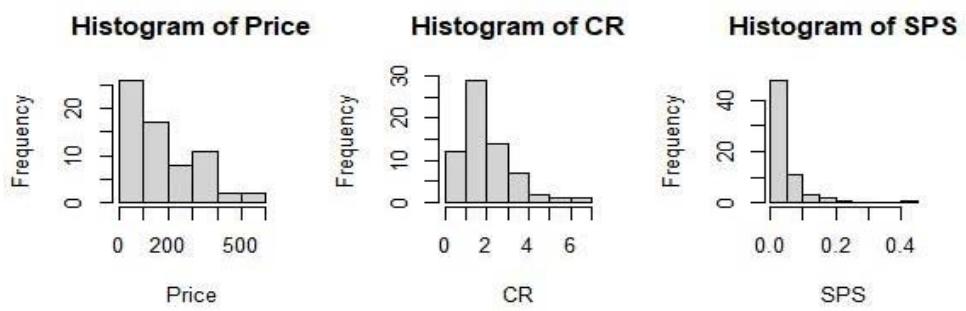

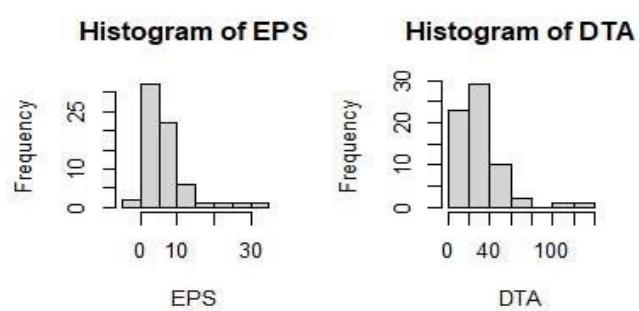

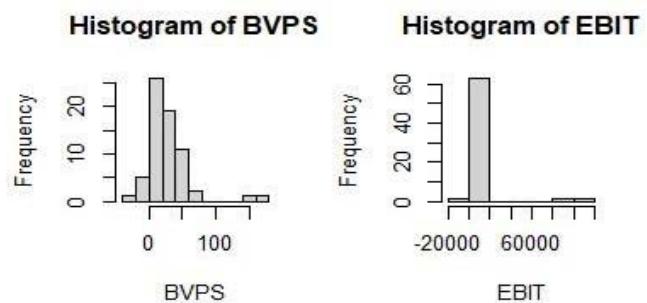

For graphical analysis, a histogram (fig.1), scatter plot (fig.2), and line-plot (fig.3) have been developed for all dependent and independent variables.

Figure1

From fig.1 we can see that the histogram of is skewed to the right BVPS, and EBIT's histogram is Price, EPS, CR, SPS, DTA are positively skewed which relatively symmetric.

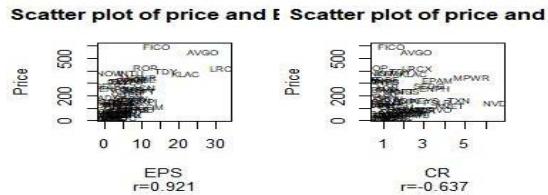

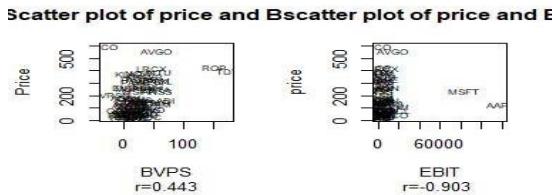

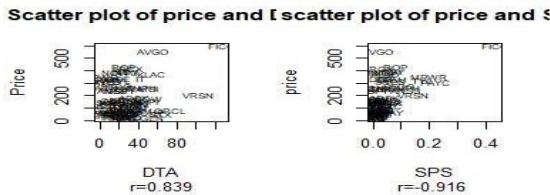

Figure 2

The scatter plot of dependent and independent variables is shown in fig. 2. Price and EPS are positively correlated ( $r = 0.692$ ) with very strong linear association. Whereas price and CR ( $r = -0.637$ ) show a negative but moderate linear relation. The Price-BVPS scatterplot

suggests a positive correlation $(r = 0.443)$. While price and EBIT $(r = -0.903)$ shows a negative but strong linear relation. Price-DTA scatterplot $(r = 0.839)$ and Price-SPS scatterplot $(r = 0.916)$ show strong positive linear associations.

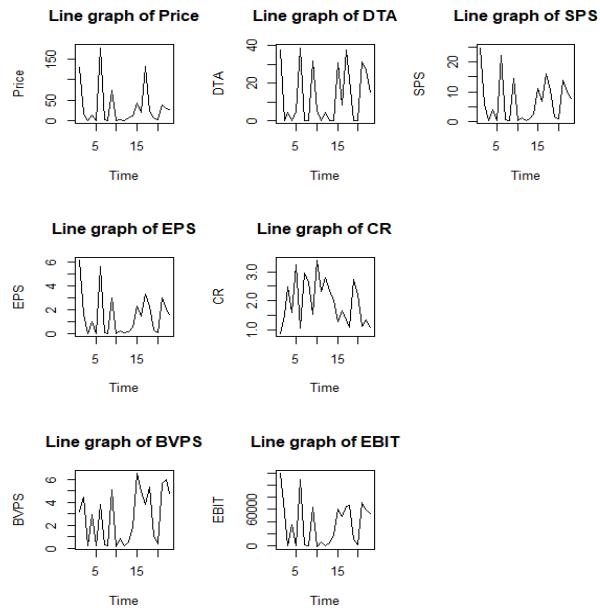

Figure 3

The line graph in fig. 3 shows the trend of Price, EPS, BVPS, DTA, CR, EBIT and SPS with respect to month. Cyclical positive trend has been seen from the

line graph of Price, EPS, BVPS, DTA, CR, EBIT and SPS. Whereas relatively secular trend with seasonality has been from DTA line graph.

Table 1: Descriptive Statistics Table 1 Shows the descriptive statistics of the variables. From the table.1, the value of skewness indicates that the distribution of Price, EPS, BVPS, CR, DTA, EBIT, and

<table><tr><td>Name</td><td>n</td><td>Mean</td><td>Median</td><td>Std.Dev</td><td>Skewness</td><td>Kurtosis</td></tr><tr><td>Price</td><td>23</td><td>33.43</td><td>14.46</td><td>48.89</td><td>1.72</td><td>5.22</td></tr><tr><td>EPS</td><td>23</td><td>1.51</td><td>0.99</td><td>1.77</td><td>1.18</td><td>3.90</td></tr><tr><td>BVPS</td><td>23</td><td>2.73</td><td>2.94</td><td>2.29</td><td>0.16</td><td>1.44</td></tr><tr><td>CR</td><td>23</td><td>1.95</td><td>1.68</td><td>0.77</td><td>0.32</td><td>1.81</td></tr><tr><td>DTA</td><td>23</td><td>13.05</td><td>5.02</td><td>15.07</td><td>0.59</td><td>1.70</td></tr><tr><td>EBIT</td><td>23</td><td>36886.22</td><td>34494.00</td><td>36577.37</td><td>0.59</td><td>2.44</td></tr><tr><td>SPS</td><td>23</td><td>6.85</td><td>4.17</td><td>7.40</td><td>0.94</td><td>2.99</td></tr></table>

SPS are positively skewed to the right and Price, EPS, and SPS have extreme values with high kurtosis, whereas others are significantly more peaked than symmetric leptokurtic distributions.

Table 2: Correlation Matrix

<table><tr><td></td><td>Price</td><td>EPS</td><td>BVPS</td><td>CR</td><td>DTA</td><td>EBIT</td><td>SPS</td></tr><tr><td>Price</td><td>1.000</td><td>0.921</td><td>0.443</td><td>0.637</td><td>0.839</td><td>0.837</td><td>0.916</td></tr><tr><td>EPS</td><td>0.921</td><td>1.000</td><td>0.643</td><td>-0.801</td><td>0.832</td><td>0.971</td><td>0.993</td></tr><tr><td>BVPS</td><td>0.443</td><td>0.643</td><td>1.000</td><td>-0.866</td><td>0.703</td><td>0.786</td><td>0.689</td></tr><tr><td>CR</td><td>-0.637</td><td>-0.801</td><td>-0.866</td><td>1.000</td><td>-0.725</td><td>-0.893</td><td>-0.820</td></tr><tr><td>DTA</td><td>0.839</td><td>0.892</td><td>0.703</td><td>-0.725</td><td>1.000</td><td>0.864</td><td>0.929</td></tr><tr><td>EBIT</td><td>0.837</td><td>0.971</td><td>0.786</td><td>-0.893</td><td>0.864</td><td>1.000</td><td>0.970</td></tr><tr><td>SPS</td><td>0.916</td><td>0.993</td><td>0.689</td><td>-0.820</td><td>0.929</td><td>0.970</td><td>1.000</td></tr></table>

Table 2:

Shows the correlation matrix among the variables. Almost all variables showed a positive and strong correlation. Price and SPS show the highest with

$(r = 0.921)$ while Price and CR indicate the lowest correlation $(r = -0.637)$. The correlation coefficients of all variables agreed with the original hypothesis.

Table 3: Regression Results Eqn. 4 Price = 1.433-6.15*BVPS+9.34*SPS-0.001\*EBIT

<table><tr><td></td><td>Price</td><td>BVPS</td><td>SPS</td><td>EBIT</td></tr><tr><td>t-stat</td><td>0.272</td><td>-2.234*</td><td>4.281***</td><td>-0.798</td></tr><tr><td>p-value</td><td>0.788</td><td>0.038</td><td>0.000</td><td>0.435</td></tr><tr><td>r(corr.)</td><td></td><td>0.443</td><td>0.916</td><td>0.837</td></tr></table>

Our hypothesis is, Ho: $\beta \mathrm{BVPS} = \beta \mathrm{SPS} = \beta \mathrm{EBIT} = 0$

$$

\mathrm{H_a}: \beta_i \neq 0.

$$

The overall equation is significant at $5\%$ level of significance as F statistics is $(62.93 > 3.00)$, so we can conclude that, null hypothesis (H0) is rejected. Since the coefficient of determination is $r^2 = 0.91$, so $91\%$ variation in price is explained by BVPS, SPS and EBIT. For significant test of the regression coefficient individually t-test has been done. SPS $(4.281 > 2.99)$ and BVPS $(-2.234 > 1.28)$ statistically significant at $1\%$ and $10\%$ levels respectively. Whereas EBIT $(-0.798 < 1.28)$ is not statistically significant.

## V. CONCLUSION

The study presents a statistical model for predicting the equity price of Apple Inc. in the Information Technology sector. The Research was successful, and the explanatory power was high. Price has been considered as the response variable concerning explanatory variables BVPS SPS and EBIT. All explanatory variables were significant except DTA. Price was a successful function of the explanatory variables, and all agreed with the hypothesis. The model can be used by investors and analysts to make informed decisions about investing in Apple Inc. and to predict its future performance. The research might be improved by considering adding more variables.

Generating HTML Viewer...

References

10 Cites in Article

W Chen,Y Lai,C Su (2018). The impact of market sentiment on stock returns: A case study of Apple Inc.

D Gujarati,D Porter (2009). Basic econometrics.

P Chandra,S Kumar (2020). Financial performance and stock price movements: A study of Apple Inc.

H Lee,J Lee (2017). Predicting stock price movements: A study of Apple Inc.

C Li,Y Tseng (2016). An empirical study of Apple Inc.'s stock returns: A regression analysis approach.

P Kennedy (2008). Ross A. Kennedy (Ed.), A Companion to Woodrow Wilson. (Wiley-Blackwell Companions to American History.) Malden, MA/Oxford, Wiley-Blackwell 2013.

J Kim,T Kim (2019). Predicting stock prices using sentiment analysis of Twitter data: An empirical analysis of the IT sector.

K West (2003). Stock returns and volatility: A firm-level analysis.

R Tsay (2010). Analysis of financial time series.

J Chen,Z Jiang,H Wu (2015). Stock trend prediction with technical indicators using SVM.

No ethics committee approval was required for this article type.

Data Availability

Not applicable for this article.

How to Cite This Article

Most Tajmary Mahfuz. 2026. \u201cA Statistical Model for Predict Equity Price of the Apple Inc. company in the Information Technology Sector\u201d. Global Journal of Computer Science and Technology - C: Software & Data Engineering GJCST-C Volume 24 (GJCST Volume 24 Issue C1): .

Explore published articles in an immersive Augmented Reality environment. Our platform converts research papers into interactive 3D books, allowing readers to view and interact with content using AR and VR compatible devices.

Your published article is automatically converted into a realistic 3D book. Flip through pages and read research papers in a more engaging and interactive format.

The goal of this paper was to produce predictions regarding the future stock price of the massive corporation Apple Inc. The Information Technology (IT) sector comprises six distinct industries, among which Apple Inc., which is a large-cap company, has been the mainstay of my research. Apple Inc. is one of the most valuable companies in the world, with a market capitalization of over $2 trillion. In the study, a predictive model has been devised to estimate the equity price of the Apple Inc. company, employing diverse statistical techniques. A variety of statistical methods to examine 23 observations using time series data from FactSet-2022 has been used in this study. Graphical techniques including histograms, dissipate plots, and line plots were used to outwardly investigate the dataset, while elucidating insights were utilized to sum up the attributes of versatile factors like Value, EPS, BVPS, CR, DTA, EBIT, and SPS.

Our website is actively being updated, and changes may occur frequently. Please clear your browser cache if needed. For feedback or error reporting, please email [email protected]

Thank you for connecting with us. We will respond to you shortly.