I. INTRODUCTION

One of the most important phases in every nation's development is the formalization of the informal economy. A crucial enabler in this regard has been highlighted as financial inclusion.

To promote equitable economic growth and end poverty in the nation, access to financing for the poor is crucial. Offering financial services is the method by which money is raised and put to use in the economy. In addition to accelerating the process of resource mobilization and usage, a developed inclusive financial system also offers financial services to everyone who needs them. (NFIS, 2021). The issue of financial inclusion is a development policy in many countries (Sarma and Pais 2013). Financial inclusion refers to bringing the unbanked populace within the formal financial net. A comprehensive financial system facilitates enormous contributions to economic development by finding pioneering ways to empower the unbanked, under-banked, or the like. Making banking and payment services accessible to the entire populace without discrimination is the key purpose of Financial Inclusion. To get all the affiliates of the economy under the umbrella of financial inclusion, the provision of financial services from banks evolving day by day. As the Fourth Industrial Revolution was just beginning, Bangladesh's first National Financial Inclusion Strategy (NFIS) has been developed.

A variety of remote access financial services are in an extensive form from the last decade provided through different channels like cell phones, ATMs, POS, and banking correspondents (also known as agent banking or agency banking) made an important contribution to enhancing financial inclusion by reaching people that traditional, branch-based structure would have been unable to reach (EFInA, October 2011).

Nowadays banking plays, a pivotal role in our society that has never been more important earlier. The way Bill Gates (2008) announced that "banking is essential, banks are not" (as cited in Baten & Kamil 2010). This quotation means that the traditional bank branch is going to be replaced by new ideas and technologies which continue to attract new users. The banks will be able to improve customer service levels and tie their customers closer to the bank by adopting fresh innovations in the banking sector, new technology for establishing maiden ideas, and a new sense of satisfaction to customer end view in line with the banks aim to expand its customer base and to counteract the aggressive marketing effort. According to Quarterly Financial Stability Assessment Report (2018) by Bangladesh Bank, the most recent development in financial technology, or Fintech, through which banks can perform financial intermediation is agent banking. Fintech is defined by the Financial Stability Board (FSB) as "Technology-enabled advancement in financial services that could lead to additional business models, applications, processes, or products with an emphasis on the concept effect on the provision of financial services. Agent banking has been a proven tool and an effective way to reduce costs of operation for financial institutions. For instance, agent banking services will allow banks to lower expenditures on physical structures. It is believed that agent banking will help banks to cut costs, increase revenue, and become more convenient for customers. In a nutshell, the development of agent banking has encouraged the adoption of a decentralized approach to give banks more needed flexibility to distribute financial products and convenient access to a formal financial net of a wide range of unbanked and under-banked populace and also reach potential customers which ensure the effective financial inclusion, a major phenomenon to economic integrity and economic uplift of poorer segment people of rural and remote areas of a country.

II. OBJECTIVES

The present study is an attempt to obtain the following objectives:

To shed light on the concept of agent banking and financial inclusion;

To explore agent banking as an agent to financial inclusion in Bangladesh;

To quest the significance of agent banking in the Bangladesh context;

To provide some recommendations.

III. METHODOLOGY

The study was carried out using secondary data sources. This is an exploratory study based on secondary data collected from websites of the Bangladesh Bank, central banks of various countries, books, related journals, World Bank reports, working papers, agent banking guidelines from various countries, conference and seminar reports, annual reports of Bangladesh bank and other online sources.

IV. LITERATURE REVIEW

This topic has attracted growing interest from the academic community. Pervin and Sarker's research indicates (2021) agent banking is one of the important and ground-breaking techniques that has always brought rural people under one roof of banking services. The study also focuses on Bangladesh's agent banking market's recent expansion and its prospects for the future. In their study, Nisha et al. (2020) seeks to represent the overall aspect of agent banking and its relationship to financial inclusion in the context of Bangladesh, emphasizing it as a reliable and effective method of establishing financial deepening throughout the country's unbanked areas. The study also underlines that agent banking may ensure the impoverished in rural areas have access to financial services and lead to Bangladesh's overall growth.

In a different study, Ahmed & Ahmed (2018) found that agent banking serves as a bridge between the rural unbanked majority and financial services that they would otherwise not have access to in developing countries like Bangladesh. The study explains how agent banking innovation in the banking industry might assist the financial inclusion of the underprivileged. Agent banking has made several financial services available in rural areas, allowing people to utilize them there rather than go to cities (Afzal, 2017). The results of an empirical investigation by Idoko and Chukwu (2022) into the impact of agency banking on financial inclusion among adult rural residents in rural communities show that agency banking has a positive influence. According to Barasa and Mwirigi (2013), agency banking has been crucial in boosting the use of financial services in underserved markets. The involvement and efforts of the agent bankers, particularly in rural and semi-urban regions, are bringing financial literacy to the common people on the streets through agency communications about how agency banking functions. While highlighting the significance of financial inclusion, Thapar (2013) noted in a study the necessity of creating a system that meets peoples' needs to assure that the economy as a whole is expanding. The study also shows that while banks are adding new branches, there is still much work to be done to improve financial inclusion. Business correspondents should be hired in communities and given training ahead of time to promote financial inclusion programs. People who have access to a functional financial system, especially the impoverished, can become more economically and socially empowered, improving their ability to integrate into society and actively participate in progress; A key factor in improving financial access is the spread of financial services aimed towards the underprivileged and low-income population (Mujeri, 2015).

Siddiquie (2014) reveals in a study that most of the services of a bank can be provided through agents, thus people in the remotest area of a country can be brought under proper financial structure by the virtue of agent banking. Veniard (2010) found that when financial service providers do not have branches that are close to the customer, the customer is less likely to use and transact with their service, and subsequently emerges the new delivery models as a way to drastically change the economics of banking the poor. The author also suggested that by using retail points as cash merchants (defined here as agent banking), banks, telecom companies, and other providers can offer saving services in a commercially viable way by reducing fixed costs and encouraging customers to use the service more often, thereby providing access to additional revenue sources.

Islam & Mamun (2011) indicates that Bangladesh Bank has been pursuing financial inclusion as a policy priority for accelerated economic growth while maintaining monetary and financial stability. They also suggest that access to financial services will open up entrepreneurship opportunities, receiving benefits from government programs, therefore, contributing to financial deepening. It is an additional delivery channel that can enhance the convenience, the outreach of quality and affordable financial services, particularly to the underserved, in a more cost-efficient manner, such an arrangement is a cheaper way for financial institutions to reach out to the underserved population (Siddiqui, 2013).InfosysFinacle thought paper (2012) reveals multifold advantages of agency banking for accessing into financial inclusion system like cost-effective model, channel innovation for improving banking penetration in underserved areas, and new distribution strategy to extend banks reach to the poor or who are reluctant to make a trip to the nearest branch. Lyman, Ivatury & Staschen (2006) mentioned in the CGAP paper that branchless banking through retail agents appeals to policymakers and regulators because it has the potential to extend financial services to unbanked and marginalized communities.

In a study, Ullah & Haque (2014) examined that agent banking has worked wonders in several developing countries in different parts of the world like Brazil, Columbia, Peru, Malaysia, Kenya, etc. Agent banking has been a revolutionary inclusion in the financial system of Brazil as the agents deal with almost everything like bills and pension payments, cash deposits, withdrawals, and money transfers. In their study, they also revealed that 'As reported by the Banco Central do Brasil, the central bank of Brazil, since the introduction of agent banking, 12 million current accounts were opened across the agency banking network within only three years and the total amount of transactions reached 2.6 billion reflecting the necessity of such a service. Columbia and Peru also turned to the mechanism. Although in Columbia the bank branches covered 73 percent of the municipality, the agent banking helped raise the coverage to nearly 100 percent. In 2009 the total numbers of transactions in Peru and Columbia were 67 million and 29 million respectively which were quite big compared to the size of their respective economy.'

Quarterly Report (2022) of Bangladesh Bank states that the implementation of the government's Vision 2041 and the sustainable development goal set by the United Nations (UN), as well as the national financial inclusion policy, depends heavily on the general populace's financial literacy. The goal of financial inclusion will be easier to reach if the general public is well-informed about financial services and products. In that light, Bangladesh Bank has released guidelines for banks and financial institutions on how to broaden their financial inclusion sphere by educating the general public sufficiently about their goods and services. Agent banking can be quite helpful in this context since it can regionally extend formal financial services to a larger portion of Bangladesh's economically excluded population and therefore enhance financial inclusion.

V. DEFINITION OF CONCEPT

a) Financial Inclusion

Following NFIS (2021) Bangladesh, Financial inclusion has no unified definition worldwide. Financial inclusion in Bangladesh is not just about increasing the availability of credit and other financial services rather it entails access to and use of a variety of quality financial goods and services offered by regulated service providers to all demographic groups. This strategy defines financial inclusion as:

"Access of individuals and businesses including unserved and underserved to the full range of financial services facilitated with technology provided at affordable cost with quality, ease of access and scope of risk mitigation responsibly and sustainably through a regulated, transparent, efficient and competitive financial marketplace." This will be regarded as Bangladesh's national definition of financial inclusion.

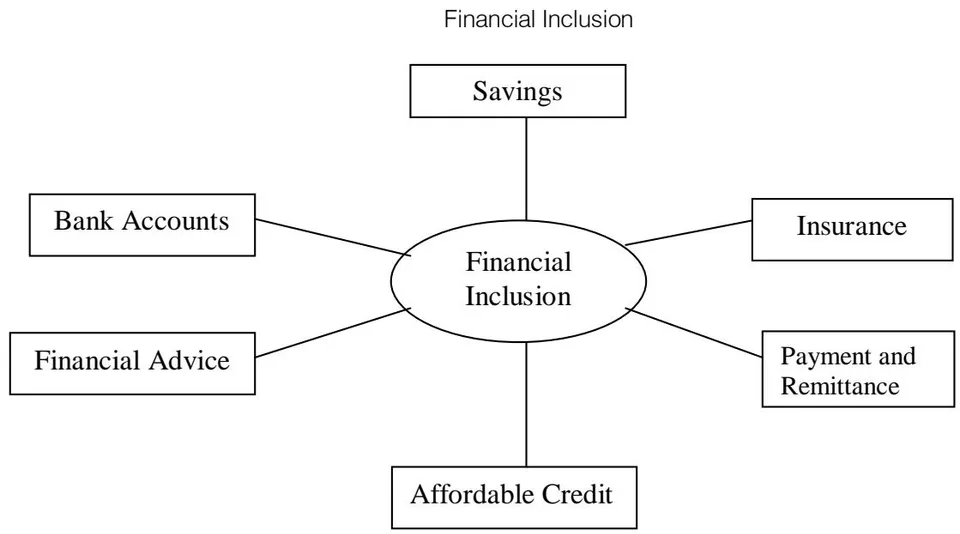

Financial inclusion refers to a process that ensures the ease of access, availability, and usage of the formal financial system for all members of an economy (Sarma and Pais, 2013). A Government Committee on financial inclusion in India defines financial inclusion as 'the process of ensuring access to financial services and timely and adequate credit where needed by vulnerable groups such as the weaker sections and low-income groups at an affordable cost (Rangarajan Committee, 2008). The committee also mentioned that the various financial services include savings, loans, insurance, payments, remittance facilities, and financial counseling/advisory services by the formal financial system.

Choudhury (2010) observed that the "Extent of financial inclusion can be assessed in some ways. The most commonly used indicator has been the number of bank accounts (per 1000 people). However, financial inclusion does not end with the opening of bank accounts. What matters ultimately is the availability of banking services and access to finance by mass people. Some other indicators have also been developed to capture the financial inclusion like the number of bank branches, number of ATMs, bank credit as a percentage of GDP, bank deposit as a percentage of GDP, etc."

Thapar (2013) points out that "financial inclusion is delivery of banking services at an affordable cost to the vast sections of disadvantaged and low-income group. The various financial services include savings, loans, insurance, payments, remittance facilities, and financial counseling/ advisory services by the formal financial system."

Centerfor Financial Inclusion's Vision (2015) for Financial Inclusion includes:

- Access to a full suite of financial services: Including credit, savings, insurance, and payments

- Provided with quality: Convenient, affordable, suitable, provided with dignity and client protection

- To everyone who can use financial services: Excluded and under-served people. Special attention to rural, people with disabilities, women, and other often-excluded groups

- With financial capability: Clients are informed and able to make good money management decisions

- Through a diverse and competitive marketplace: A range of providers, robust financial infrastructure, and a clear regulatory framework

United Nations (2006), in its blue book titled "Building Inclusive Financial Sectors for Development", defines financial inclusion as "access to the range of financial services at a reasonable cost for the bankable people and farms".

According to the House of Commons Treasury Committee (2006), financial inclusion also refers to the ability of individuals to access appropriate financial products and services. An understanding of appropriate financial products and services includes financial awareness, knowledge about banks and banking channels, facilities provided by the banks, and advantages of using the banking channel (Islam & Mamun 2011).

In the National Strategy for Financial Inclusion in Indonesia, financial inclusion is defined as: The right of every individual to have access to a full range of quality financial services in a timely, convenient, informed manner, and at affordable cost in full respect of his/her personal dignity. Financial services are provided to all segments of society, with a particular attention to low-income poor, productive poor, migrant workers, and people living in a remote area (Booklet Financial Inclusion, 2014).

Rahman (2009) defines financial inclusion in Bangladesh as access to financial services from officially regulated and supervised entities in which banks and financial institutions are licensed by the Bangladesh Bank, MFIs by the Microcredit Regulatory Authority (MRA), registered cooperatives by the Department of Cooperatives; and official entities themselves including post offices and National Savings Directorate.

As stated by Alliance for Financial Inclusion (2012) the term financial inclusion refers to a broad financial system that provides access to financing, mobilization of savings, credit allocation, risk management, as well as payment services. Financial inclusion states both the acceptable provision of services by the financial institutions as well as the suitable uptake or use of these services by all segments of the population. According toInfosysFinacle thought paper (2012) benefitting from the entry of new entities as agents and the emergence of modern technology agency banking has expanded the definition of financial inclusion, which refers to the unification of a variety of bank and non-bank players to offer financial services at lower cost, wider reach and in a simpler way to all end customers of financial services, unbanked or otherwise.

b) Agent Banking

Agent banking can ensure the access of marginalized people to several financial services, especially in remote areas. It can work wonders in financial inclusion and enhancing financial activity in remote areas (Ullah & Haque, 2014).

On the word of Alliance for Financial Inclusion (2012) "The agent banking model is one in which banks provide financial services through nonbank agents, such as grocery stores, retail outlets, post offices, pharmacies, or lottery outlets. This model allows banks to expand services into areas where they do not have sufficient incentive or capacity to establish a formal branch, which is particularly true in rural and poor areas where as a result a high percentage of people are unbanked."

Agent banking means the provision of banking services by a third-party agent to customers on behalf of a licensed, prudentially-regulated financial institution, such as a bank or other deposit-taking institution (EFInA, October 2011). In the agency banking model financial institutions work with networks of existing nonbank retail outlets—such as convenience stores, gas stations, and post offices—to deliver financial services (Chaia, Scifff& Silva, 2010).

Guidelines on agent banking (Bangladesh Bank, 2013) for the banks, Bangladesh Bank points out that agent banking means providing banking services to the bank customers through the engaged agents under a valid agency agreement, rather than a teller/cashier. It is the owner of an outlet that conducts banking transactions on behalf of the concerned bank.

The following services will be covered under Agent Banking:

Collection of small value cash deposits and cash withdrawals (ceiling should be determined by BB from time to time);

Inward foreign remittance disbursement;

Facilitating small value loan disbursement and recovery of loans, and installments;

Facilitating utility bill payment;

Cash payment under the social safety net programme of the Government;

Facilitating fund transfer (ceiling should be determined by BB from time to time);

Balance inquiry;

Collection and processing of forms/documents concerning account opening, loan application, and credit and debit card application from the public;

Post-sanction monitoring of loans and advances and follow-up of loan recovery.

Receiving of clearing cheque.

Other functions like a collection of insurance premiums including micro- insurance etc.

In Colombia, agents are called 'non-bank correspondents. These are commercial businesses that can provide financial services on behalf of formal financial institutions (EFInA, October 2011). Chude & Chude (2014) experienced that agent banking has become an essential practice of financial institutions in bringing their services closer to the people on the grass root. The study revealed that agent banking has proved to have an essential role to play in improving customer satisfaction and bank profitability and it was recommended that agent banking should be adopted in Nigeria.

Siddiqui (2013) stated that the use of the term 'agent' is not necessarily a reference to an agent in the traditional legal sense of a party authorized by a principal to act on the principal's behalf and for whom the principal is liable concerning activities taken by the agent within the scope of its agency relationship or contract. He also notified that an agent is any third party acting on behalf of a bank, whether under an agency agreement, service agreement, or other similar arrangements. In this study, Siddiqui (2013) observed that

Many countries permit a wide range of individuals and legal entities to be agents for banks. Other countries limit the list of eligible agents based on a legal form. For example, India permits a wide variety of eligible agents, such as certain nonprofits, post offices, some shop owners, retired teachers, and most recently, profit companies including mobile network operators (MNOs). Kenya takes a different approach, requiring agents to be for-profit actors and disallowing non-profit entities (like non-governmental Organizations (NGOs), educational institutions, and faith-based organizations). In another example, Brazil permits any legal entity to act as an agent but prevents individuals from doing so.

An agent is an entity engaged by a financial institution to make available certain services on its behalf utilizing the agent's grounds. That means extending the banking habits among the less privileged both in urban and rural areas. It encompasses the delivery of financial services outside conventional bank branches, via non-bank retail outlets that rely on technologies such as point-of-sale (POS) devices or cell phones for concurrent business processing.

VI. PRESENT SCENARIO OF AGENT BANKING AND FINANCIAL INCLUSION INITIATIVE IN BANGLADESH

Financial inclusion is the gateway to achieving inclusive growth and for this reason, Bangladesh Bank (BB) plans to permit agent banking to gear up its strength aspiring to help the government attain sustainable economic development. The BB has already laid the necessary foundation for agent banking by introducing mobile banking which has already got a good response, especially from rural people (Siddiqui, 2013). The Bangladesh Bank has decided to promote agent banking to reach out to the poor segment of society with a range of financial services, especially at geographically dispersed locations (Haque, 2013). Financial inclusion denotes the ability of individuals to access appropriate financial products and services and it is inevitable for a country like Bangladesh to provide financial opportunities to financially-excluded people as they are almost half the country's total population; development cannot be possible excluding half the total population (Faruk, 2015).

In December 2013, Bangladesh Bank issued licenses for conducting agent banking services, particularly in rural areas where conventional bank services were not widely accessible. Agent banking will be used more frequently as a crucial distribution channel for financial inclusion, under its BB standards. According to Bangladesh Bank's Quarterly Report on Agent Banking (2022), 30 banks were offering agent banking as of June 2022 through 19,737 outlets run by 14,299 agents. Over the preceding quarter, the number of outlets increased by while the number of agents increased by . A total of 16,074,378 accounts have been opened through agent banking, of which 7,937,867 (or ) belong to female customers and 13,890,321 (or ) to people in rural areas.

| Urban | Rural | Total | |

| Number of Accounts | 2184057 | 13890321 | 16,074,378 |

| Number of Agents | 2185 | 12114 | 14,299 |

| Number of Outlets | 2730 | 17007 | 19,737 |

| Amount of Deposits (in BDT million) | 60412.87 | 220440.31 | 280853.18 |

| Amount of Lending (in BDT million) | 26385.98 | 50070.35 | 76456.33 |

| June '21 | Mar '22 | June 2022 | Change | ||

| Y-to-Y | Q-to-Q | ||||

| No. of Banks with License | 28 | 29 | 30 | 2 | 1 |

| No. of Banks in Agent Banking Operation | 28 | 29 | 30 | 2 | 1 |

| No. of Agents | 12,912 | 14,166 | 14,299 | 1,387 | 133 |

| No. of Outlets | 17,147 | 19,530 | 19,737 | 2590 | 207 |

| No. of Accounts | 12,205,358 | 15,193,146 | 16,074,378 | 3869020 | 881232 |

| No. of Female Accounts | 5,675,329 | 7,445,291 | 7,937,867 | 2262538 | 492576 |

| Number of Rural Accounts | 10,539,163 | 13,036,428 | 13,890,321 | 3351158 | 853893 |

| Amount of Deposits (in BDT million) | 203,792.83 | 251,649.63 | 280,853.18 | 77060.35 | 29203.55 |

| Amount of Loan Disbursed (in BDT million) | 31,862.86 | 64,214.57 | 76,456.33 | 44593.47 | 12241.76 |

| Amount of Inward Remittance(in BDT million) | 679,540.45 | 847,150.68 | 970,481.82 | 290,941.37 | 123,331.14 |

As per Bangladesh Bank Guidelines (2013), a good number of retail services will be brought under agent banking which includes a collection of small value cash deposits and cash withdrawals, inward foreign remittance disbursement; small value loan disbursement, and recovery of loan installments; utility bills payment, cash payment under social safety net programs, fund transfer, balance inquiry; issuance of mini bank statements, collection, and processing of documents about account opening, loan application, credit, and debit card application; monitoring loans and advances and following up loan recovery. Other functions like deposit collection, payment of insurance premiums, and sale of crops and other insurances will also be allowed under agent banking.

It is believed that about 75 percent of the adult population, mainly living in rural areas in Bangladesh, does not have bank accounts. These unbanked people are expected to benefit from agent banking (Haque, 2013). Haque (2013) states that after mobile financial services, the introduction of agent banking will contribute further to enhancing access to finance, licensed banks in collaboration with mobile phone operators started mobile financial services in 2011 and now they have over 3.00 million customers, mostly middle- and low-income people. He also reveals that the volume of transactions per day is between TK. 300 million and Tk. 350 million and it is increasing every day; the number of agents and sub-agents of mobile financial service operators is also increasing rapidly.

Bangladesh Bank already initiated the following steps for enhancing financial inclusion in Bangladesh:

Mobile financial services guideline with provision to appoint an agent for providing the service and to fetch unbanked people into the financial net

Agent Banking guideline with an aim to financial inclusion of rural people

Bank account for farmers with a balance of TK. 10 only and instruct the commercial banks for ensuring the service at all branches including urban and rural areas

Account for students with special features like no account maintenance charge, Free ATM card, etc.

BB ensures the proper allocation of bank branches between urban and rural areas with an instruction to commercial banks to open a branch at a 1:1 ratio of rural and urban.

| July'22 | July'21 | July'20 | July'19 | ||

| Total number of bank branches | 10,982 | 10,796 | 10,606 | 10,320 | |

| a) | Urban | 5738 | 5657 | 5573 | 5397 |

| b) | Rural | 5244 | 5139 | 5033 | 4923 |

VII. SIGNIFICANCE OF AGENT BANKING

In Bangladesh, the central bank, Bangladesh Bank (BB), has historically been in charge of promoting financial inclusion. The BB has been doing this by implementing a "Three-Dimensional Action" of financial inclusion, which is interconnected. One of these actions is Diversifying Service Delivery Channel, which entails using diverse service delivery channels through various initiatives, such as agent banking, which was started in 2013.

Difficult-to-access localities, such as remote, hilly, sparsely populated places; haor, char, and other comparable areas with challenging terrain; and relatively underdeveloped areas with subpar infrastructure, are some of the main contributing causes to financial exclusion in Bangladesh. In this context, the significance of agent banking is paramount. The high operational costs of financial services, such as branch opening, employee training, technical costs, etc., are further factors contributing to financial exclusion in Bangladesh, a developing country, according to Nisha and Rifat (2017). Additionally, it has been observed that the urban poor does not use financial services because they cannot afford the high cost of banking transactions. (Nisha et al., 2015).

According to Bangladesh Bank's Annual Report (2020-21), scheduled banks are permitted to expand banking services through agents, who can provide limited banking and financial services on behalf of a bank per an authorized agency contract. With the use of this platform, banks can offer their services in remote places without having to open a branch or send staff members there. Agent banking in rural areas has accelerated financial inclusion and opened up countless opportunities for banks and their clients. Agent banking assists banks with deposit mobilization, credit allocation, and—most importantly—distribution of incoming foreign remittances. Agent banking continued to advance significantly even during the COVID-19 outbreak when all other commercial and financial activity experienced a decline. To give remote rural consumers a viable alternative to traditional banking, agent banking has been developing. The Agent networks give the chance to expand the financial system efficiently, and they are also one of the most significant drivers of financial inclusion in Bangladesh because they deliver financial services to the underserved and unbanked all over the nation through agent outlets.

Huda et al. (2020), who claim that agents are used as prospective distribution channels for financial inclusion, endorse this point of view in their study. They emphasize the fact that Bangladesh Bank is promoting agent banking to reach the untapped market and existing customers who live in geographically dispersed areas so that they can benefit from real-time banking services from the agent. An agent banking branch can be thought of as a mini branch of a bank that has all the contemporary amenities that a full branch of a bank has.

The significance of a wide-ranging financial system is extensively acknowledged and financial inclusion is evolving as the main concern in many countries lately. The country's development strategy recognizes that socioeconomic opportunities and development in Bangladesh will be undermined if expanded financial services are not available, especially to the poor and other disadvantaged groups who are deprived of access to these services and who need these services (Mujeri, 2015).

Branchless banking through retail agents appeals to policymakers and regulators because it has the potential to extend financial services to unbanked and marginalized communities (Lyman et. al., 2006). The financial tools available to the poor to manage their money are often costly, unsafe, and inefficient. Money kept at home may be subject to theft, temptation, and family demands, while money lenders and other intermediaries charge high fees and prohibitive interest rates. Formal financial institutions are largely inaccessible to the poor as they are often costly, hard to reach, and offer products that seldom suit their needs (Thapar, 2013).

A research team from BIBM (2015) pointed out that i.n a growing number of countries, banks, and other commercial financial service providers are finding new ways to make money delivering financial services to unbanked people. Rather than using bank branches and their officers, they offer banking and payment services through postal and retail outlets, including grocery stores, pharmacies, seed and fertilizer retailers, and gas stations, among others. For poor people, "branchless banking" through retail agents may be far more convenient and efficient than going to a bank branch. For many poor customers, it will be the first time they have access to any formal financial services- and formal services are usually significantly safer and cheaper than informal alternatives (Lyman et. al., 2006).

Kenya's banking sector has witnessed an increase in financial inclusion following the introduction of agent banking, according to a new report from the Central Bank of Kenya (CBK, 2014). This new model has ensured more people have increased contact with banking facilities since its roll out in May 2010, the report says. In June 2014, 15 commercial banks had contracted 26,750 active agents facilitating more than 106 million transactions valued at Sh571,5 billion (€4.8 billion). This was up from 14 commercial banks in March 2014 with 24,645 agents facilitating about 92.6 million transactions valued at Sh499 billion (Making Finance Work for Africa, 2014).

For banks, branchless banking through retail agents is used to reduce the cost of delivering financial services, relieve crowds in bank branches, and establish a presence in new areas (World Bank, 2006).

The amount of money expended by financial service providers to serve a poor customer with a small balance and conducting small transactions is simply too great to make such accounts viable, according to a report from the Bill and Melinda Gates Foundation (Making Finance Work for Africa, 2014).

To provide financial services to the poor through bank-based delivery channels in traditional banking methods is a matter of high cost. The sum of money spent by financial service providers to attend to a poor customer with a small balance and accompanying small transactions is simply too excessive to make such accounts feasible. Furthermore, the customer is less likely to use and transact with any bank branches not close to him or her.

Nonetheless, we see the emergence of new delivery models as a way to drastically change the economics of banking for the poor. By using retail points as cash merchants (defined here as agent banking), banks, telecom companies, and other providers can offer saving services in a commercially viable way by reducing fixed costs and encouraging customers to use the service more often, thereby providing access to additional revenue sources (Veniard, 2010).

Agent banking systems are up to three times cheaper to operate than branches for two reasons. First, agent banking minimizes fixed costs by leveraging existing retail outlets and reducing the need for financial service providers to invest in their infrastructure. Although agent banking incurs higher variable costs from commissions to agents and communications, fixed costs per transaction for branches are significantly higher. Second, acquisition costs are lower for mobile-enabled agents and mobile wallets.... mobile wallets may also benefit from lower-cost Know Your Customer requirements, such as the elimination of requirements to provide photographs and photocopies of documents (Veniard, 2010).

By bringing the channel closer to the client, the agent banking structure can also benefit from additional revenue associated with transactions acquired by the agent, such as person-to-person transactions and bill payments. Because of lesser transaction charges and a transaction-driven returns model agent banking systems are cost-effective for transactional accounts with low balances.

Agency banking rationalized banks' operational expenditure and reduced the cost to customers while enabling wider reach. In time, agents also took up the responsibility of on boarding, managing, and servicing customers, making agency banking a lucrative option for banking institutions (InfosysFinacle thought paper, 2012).

Financial services actively contribute to the humane & economic development of society. These lead to social safety net & protect the people from economic shocks. Hence, each & every individual should be provided with affordable institutional financial products/services (Thapar, 2013).

VIII. CHALLENGES OF AGENT BANKING IN BANGLADESH

Banks cannot rely on agents to cross-sell financial products. As a result, to increase overall customer profitability, banks may need to incur additional costs in marketing and deploying sales forces, including branch employees, to cross-sell additional financial products to agent customers (Veniard, 2010).

Most of those lacking a bank account believe they can do without one. Therefore, the challenge facing banks is to convince and incentive these people to adopt their services (Kiran, 2009). Thus, positioning banking services is an important aspect to face while executing agent banking.

In the Bangladesh context, trust-building on agents is a considerable challenge, as sometimes banks are termed 'Problem Bank', and thus customers' rely upon them is in poor status. Besides this, depending on the delivery channel and nature of the product technology costs may vary due to the bank's high-cost maintenance costs of core banking systems and complex procedures due to regulatory bindings. It's still a reality in Bangladesh that technological advancement is far behind and remote area of the countryside is out of the reach of internet service providers due to non-use or underuse of availing internet facility of the target locality. GoB's (Government of Bangladesh) step towards minimizing the gap is not significant in nature. Computer literacy is not available even in High School and there is a provision for appointing a minimum lone teacher at each High School to teach the students and aware of information technology. So an adaptation of technology-based financial services in a remote area is tough and sometimes unfeasible in the Bangladesh context. It also will be difficult for a bank to identify locations and clusters where an agent is required to operate on behalf of the bank or might be a commercial bank appoint agent only in the area which has the potential to maximize profit ignoring the underneath concept of financial inclusion of underserved segment of the population in a remote area. The central bank should take the initiatives to identify the locations where the appointment of an agent is required and which bank will come up with the appointment of agents.

When looking at accessing the unbanked as a potential new market, banks generally have to reach outside their traditional paradigms, as it is not a viable option for a widely dispersed rural population who find it prohibitively expensive and time-consuming to travel to the nearest bank branch. Conversely, it is not practical or cost-effective for the bank to set up full branches in rural areas with low population density (iVeri Whitepaper, 2014).

Another issue to be considered in the implementation of an agent banking scheme is related to the technological and logistic capability and willingness of the banks.

The Bangladesh Bank guideline on Agent Banking lacks a strategic plan and specific timeframe for implementation of the scheme so commercial banks show reluctance and consider only commercially viable locations and clusters which may endanger the BB's aim of financial inclusion through the scheme and reach the marginalized people of the country. The distribution strategy of the banks to implement agent banking consistent with changing customer demographics and other economic factors is also important for effective and efficient financial inclusion of unbanked people. Agents may fail to provide quality service and maintain the secrecy of customer data which can adversely affect the overall credibility of banks, an alarming matter for both banking institutions and the regulators. Usually, agents don't have operational expertise, even though getting well instructions or trained; on banking products and other technological appliances thus need online help and real-time solutions to agent problems. Bangladesh Bank set a broader range of rules for agent banking but it's the individual bank's responsibility to ensure the clarity of agents' responsibility, access to information of banks data center, the exercise of authority, and segregation of execution of operations.

IX. RECOMMENDATIONS

Draft guideline on Agent Banking of BB has a significant limiting factor that will impede the spread of agent banking rapidly. Our recommendation is to learn from successfully implemented agent banking programs from different countries and allow non-bank financial institutions and other corporations to perform agent banking so that within a shorter period major portion of the populace incorporates the formal financial net.

To achieve comprehensive financial inclusion in Bangladesh several non-banking institutions from unrelated verticals like telecom and retail should be stepping into this space under the umbrella of agent banking by offering financial products and services like mobile wallets and white-labeled loan products and Govt. policy should encourage the same for the greater interest of economic growth and justifiable distribution of wealth.

Agents might lack behind to ensure the service quality compare to banks and thus spoil the image of the bank significantly. To get rid of the instance's banks must take care of appointing right and

competent agents and regularly monitor their performance and evaluate periodically.

There should have a uniform schedule of charges related to agent banking that check the banks' lust for profit maximization or Bangladesh Bank should quest for developing a mechanism to create market competition that ensures the lower service charge and thus accelerate financial inclusion.

Banks should ensure real-time support and on-time solutions to agents' problems through the agent banking support team round the clock with availability to physical attendance, when & where required.

Regulators should issue detailed strategic plans and guidelines for financial inclusion to commercial banks to open branches in allhabitants of five thousand or more population in under-banked areas and ten thousand or more population in other areas.

Commercial banks of Bangladesh should advise ensuring serve rural areas with assigned responsibility to ensure that every household has at least one bank account whether or not through the branch or agent banking.

For true financial inclusion, the bank should develop and offer financial products which are the best suited to low-income groups both in urban and rural areas such as no minimum balance account/zero balance account, services free from procedural hassle, simplification of KYC procedure, reasonable bank charges or cost-free services for small amount processing, etc.

Regulators should allow and suggest commercial banks to operate small-scale branches with limited financial services in all villages for close supervision and mentoring of agents for ensuring that a range of banking services are available to the residents of each village aiming for financial inclusion effectively.

X. CONCLUSION

Financial inclusion is not only a societal obligation of governments but an evolving primacy for banks that have nowhere else to go to achieve business growth. It is high time that banks took a comprehensive outlook of inclusion policy and all its fundamentals from customers to products to technology, and attain the finest mix to drive their strategy in the future. A rightly implemented financial inclusion program through agent banking might offer banks an advanced means of market expansion and customer variety management. The intentions of financial inclusion through the agent banking model can reach more rural communities, as many of the rural users are formally unbanked. The expanding trend of agent banking suggests that there is a notable change to include rural residents who do not have access to traditional financial services. The provision of basic financial services, particularly for rural women, small company owners, and recipients of remittances, is being greatly aided by agent banking. It is imperative that agent banking become more widely accepted to advance financial inclusion initiatives and achieve Bangladesh's goal of sustained economic growth. Although agent banking is new to the nation and is still in its developing phases, to significantly contribute to financial inclusion, agents need to offer a broad range of financial services suitable for the populace and new inventions galore, and fresh improvements are emerging.