This paper aims to assess the service quality of Sonali Bank Limited using the SERVQUAL framework to measure Tangibility, Reliability, Responsiveness, Assurance, Empathy and Overall Service Quality. A well-structured questionnaire was developed, and 200 respondents’ data were analysed with SPSS 20. Data analysis showed that Tangibility, Reliability, and Empathy positively affect Overall Service Quality, and Responsiveness and Assurance negatively impact Service Quality. Customer perception reveals that Tangibility, Reliability, and Responsiveness of Sonali Bank Limited are not satisfactory, while Assurance and Empathy are founded as moderate and satisfactory, respectively. Finally, we found that overall service quality depends on at least one of the following variables: Tangibility, Reliability, Responsiveness, Assurance, and Empathy.

## I. INTRODUCTION

If we observe the service quality of banks and financial institutions, especially the service of state-owned banking Bangladesh, we perceive that it has been struggling very hard for the last couple of years to compete in the market to delight the customers. The country's financial viability depends on banks and financial institutions' performance, and for this reason, to espouse the economic system of Bangladesh, the service quality of banks and financial institutions must be sturdy solid and effectual.

Bangladeshi Banking diligence is trying to integrate its service sector when it gained independence after 1971. Banks have witnessed a significant rumble after the hasty technological encroachment and superior relations structure. Markets are intensively bloodthirsty in terms of giving both number and superior services. Command of customers is more challenging to fulfill than before, pushing firms to give service quality today. Giving customers contentment and making the relationship with customers to gain loyalty is the main focus of banking sectors to deal with this aggressive market environment. As purchasing supremacy is in the customer's hands, customer satisfaction and creating loyalty is critical for banks.

Explore the service quality dimensions and customer satisfaction in Bangladesh by using the SERVQUAL model has been done by very few researchers on government authorized banks. The foremost rationale of this research is to show how different eminence of service quality dimension and customer satisfaction is allied to each other in the public banking sector. Revealing the association between service quality and customer satisfaction by researching Sonali Bank Limited, Bangladesh, based on customers satisfaction.

## II. LITERATURE REVIEW

Al-hawari, M. (2008) showed that delivering quality services to clients is a must-have for success and survival in competitive banking terrain. Faullant, R, Matzler, K., and Fuller, J. (2008) examined the determinants of quality retail banking services to make a quality scale in banks to more understand the determinants of quality in the assiduity. They employed a two-stage literature review process and empirical analysis of retail banking. They anatomized data through a trust ability test, a factor analysis, and a regression analysis to determine the composition and estimate its trust ability and value. They showed the determinants of quality retail banking services to include assurance, empathy, effectiveness, trust ability, and confidence, reflecting a combination of SERVQUAL scales. Among others, the provision of high-quality services increases the rate of client retention, helps to attract new clients through word-of-mouth communication, increases productivity, expands the request share, reduces staff development and operating costs, and improves staff morale, fiscal performance, and profitability (Hinson, et al., 2006). They concentrated substantially on bank and client factors and close connections grounded on the service quality of banks satisfying clients. Lymperopoulos and Chaniotakis (2006) examined the part of service quality in the selection of banks for deposit services to give a deeper understanding of clients' purchase actions in the bank selection process and offer bank directors some useful perceptive into the development of high-quality customer service through word-of-mouth communication, increases productivity, expands the request share, reduces staff development and operating costs, and improve staff morale, fiscal performance, and profitability (Hinson, et al., 2006). They concentrated substantially on bank and client factors and close connections grounded on the service quality of banks satisfying customers. They measured service quality using SERVQUAL scale factors (tangibility, trust ability, responsiveness, assurance, and empathy) and anatomized data through conformation factor analysis, an ANOVA, and direct regression analysis. Amin, M., and Isa, Z. (2008) examined the part of service quality in the selection of banks for deposit services to give a deeper understanding of clients' purchase actions in the bank selection process and offer bank directors some useful perceptive into the development of high- quality client connections. They reviewed the literature on bank selection criteria, field studies, the identification of factors impacting the choice of customers, and the development of operation-related impacts and conducted a check. They linked factors as the core selection criteria for the choice of consumer banking. In addition, they found the quality of banking services as the most important factor considered by guests in assessing the provider of their mortgage and trying to establish long-term connections. Three other factors were product attributes, right to use and contact. Herington, et al. (2007) explored the goods of quality online services on the position of client interest and the development of client connections. They conducted a check of 200 Australian druggies of online banking services to collect data and employed a factor analysis and a direct structural model to test the model. They found the quality of online services did not affect guests' interest, and the trust in or development of strong connections with guests to be related to fidelity. Still, the effectiveness of quality online services was related to trust and had a circular effect on client connections through trust. Particular requirements, the association's website, and the quality of online services were related to fidelity, and then particular requirements had the topmost. In addition, in fiscal and banking services, mainly deposit services, Vietnamese banks have strengthened and bettered the quality of their services to contend more effectively and therefore grease their foundation and sustainable development to meet these conditions, which are urgently needed in the process of indigenous integration and the world. Further, individual banks may bear specific studies to consider the cross-transparency of their service quality, which can define their most effective marketing strategies.

## III. THEORETICAL BACKGROUND

### a) Service Quality

Service quality meets the needs of customers they expect from a product or service. It is known to provide high-quality service and satisfy customers constantly. Customers always compare their expectations with reality by perceived information, judgment and evaluation process (Kotler & Keller, 2009) define service as any impalpable act or performance that one party offers to another that does not affect the power of anything. According to Parasuraman et al. (1988), service quality can be defined as an overall judgment analogous to station towards the service and is generally accepted as an antecedent of overall client satisfaction (Parasuraman et al. (1988) have defined service quality as the capability of the association to meet or exceed client prospects. We know that getting a new client can bring five times more than retaining the being one, and the only way to survive with the being guests and attract them is to give quality service.

### b) Customers' Perception

Customers' perception is what they think and feel about a product or service. A company can succeed in the market if customers' perception is optimistic about its service quality. When a company can understand customers' perceptions better, it can meet the critical need of customers. By the opinion and customers' perception company's strong and weak points are revealed themselves, and they can compare their service with their competitors. So, the path to customer satisfaction is finding out customers' perceptions about the company's service quality.

### c) Customer Satisfaction

The conception of "Client or Stoner Satisfaction" as a crucial performance index within businesses has been used since the early 1980s (Bailey & Pearson 1983; Ives, Olson & Baroudi 1983). Also, the end stoner calculating reparations has been studied since 1980 (Bailey & Pearson 1983; Chin, Diehl, & Norman 1988; Ives et al., 1983; Rivard & Huff 1988).

Customer satisfaction largely depends on feelings, attitudes and opinions toward many factors. With the technological advancement in the business sector and internet-based market system, customers are more experienced, which has become a significant factor in attaining customer satisfaction. Most customers pay money for a product or service based on experience and satisfaction level. Therefore, to attain profit margin, companies have to give quality, quantity, aesthetics, and appeals as a whole, which can match customer satisfaction. If customers are satisfied with the product or service, they try to share their experience with others, spreading a good word of mouth.

On the other hand, dissatisfied customers whose expectations do not meet with the perceived performance will share a bad experience with others. This will spread a bad word of mouth that will affect the company's profit margin. To measure customer satisfaction, a company can use either a Likert scale, semantic scale or any other type of questionnaire for users.

### d) Satisfaction Vs Service Quality

When customers give their feedback after using a product to match their expectations is called satisfaction. Satisfaction mainly indicates the difference between a pre-purchase perception and what they are receiving.

Talking about any organisation's satisfaction and service quality, we can see links between these two. Sometimes it becomes a challenging task to distinguish between satisfaction and service quality. When consumers intake any service, they can only judge the service quality after using it, which leads to consumers' satisfaction or dissatisfaction. So we can see that service quality and satisfaction are primarily dependent on each other.

There are many similarities between service quality and customer satisfaction, but they are fundamentally different in their underlying outcomes and causes. Despite being the same in many ways, satisfaction is a broader concept than service quality which dimensions of service can assess. Based on this entire viewpoint, we can say that service quality is only a part of customer satisfaction without which no organisation can forecast customer demand.

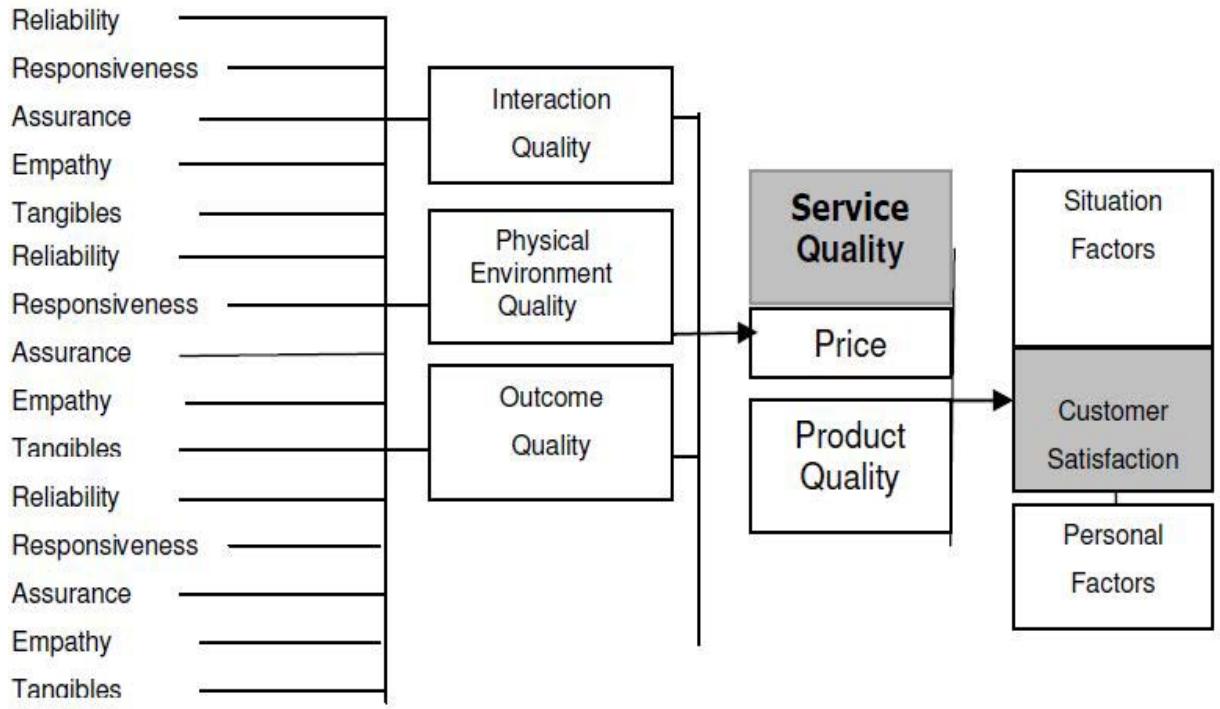

Figure 1: Customer's Viewpoint About Satisfaction Based On Service Quality Dimension

As shown in the figure, we can see that service quality reflects the customers' opinion and thinking about the interaction quality, physical environment quality, and outcome quality of any organisation. They can also be described based on specific services quality dimensions such as tangibility, reliability, responsiveness, assurance and empathy. On the other hand, customer satisfaction is more comprehensive and can be influenced by service given by the organisation, quality of product and price range, and situational factors and personal factors. For example, we can think of an internet-based banking system, where customers' demand is whether it is easy and cheap to use, availability, simple web design, easy-going information and learning process and security during transactions over the net, accuracy of the transactions and skilled human resources maintained by the banks. Whether customers are satisfied or not by using internet banking can be influenced by the service quality perception, including other factors such as quality of product, banking service charge, rate of interest, and individual and external circumstances.

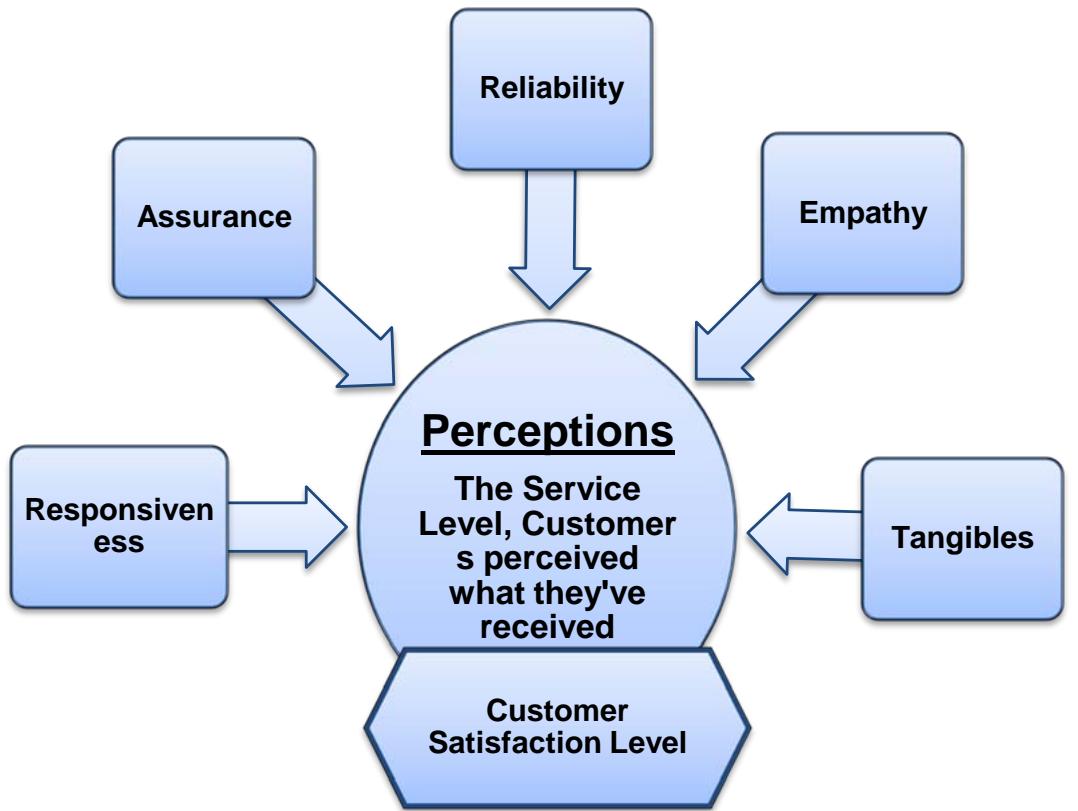

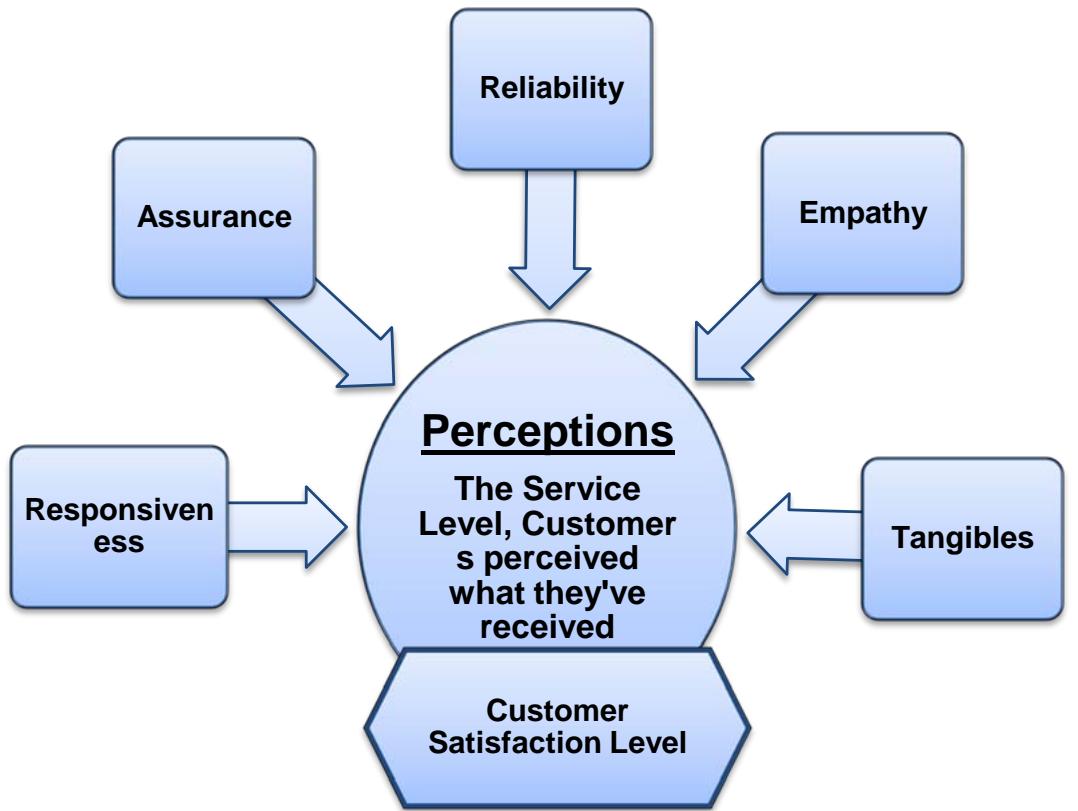

### e) Customer Satisfaction Measurement Model (SERVQUAL Model)

Customer satisfaction and quality of services are co-related to each other. Services that are naturally superior in the quality outcome as high customer satisfaction. In banking service, we can set a standard scale for measuring banking service quality. So to survive in a competitive market, service quality is used as an essential weapon for bankers.

Service quality has unique characteristics, such as intangibility, inseparability, perish ability and heterogeneity, which become difficult to measure. Many service quality models have been developed for these measurement complexities.

Among the entire measurement model, the "SRVQUAL" model is the trendy scale developed by Parsuraman et al. over the past few decades. "SERVQUAL" model has been widely used in various service sectors. Such as hospitals, banking, educational sectors, food restaurants, retail industry, hotels etc.

The SERVQUAL model of Parasuraman et al. (1988) proposes a five-dimensional construct of perceived service quality: efficiency, reliability, responsiveness, fulfillment and privacy - with items reflecting both expectations and perceived performance.

Figure 2: Service Determinants' impact on Customer Satisfaction Level

Tangibility in the "SERVQUAL" model measures the attributes and physical appearance in the banking industry. Reliability is used to give the promised performance to customers. By assurance, we understand guaranty or warranty which the organisation gives to their customers. Empathy is the measurement element by which an organisation understands customers' feelings. In this research, by using the "SERVQUAL" questionnaire, we will cover five service quality dimensions in two portions. One part will describe the customer expectation from the service, and another will describe what customers perceive from the service. As the service quality dimension is used in a wide range of service sectors, we are using the "SEVQUAL" dimension to measure the service quality of Sonali Bank Limited, Bangladesh.

## IV. RESEARCH METHODOLOGY

Research methodology is a methodical means to break a problem or give an answer to a question. It is a procedure that attendants and directs the experimenters to achieve the objects of the study. An experimenter needs to design a methodology for the chosen problem. The methodology depends on the nature of the exploration. Substantially exploration methodology describes how data are collected, what tools are used for this purpose and from whom the data are collected. To achieve the exploration objects and fulfill the exploration purpose, this study was conducted following the methodology described then for exploration design, data collection, sample selection, and procedure for data analysis and interpretation.

### a) Research Design

The theoretical frame represents the patterns and the structure of connections among the set of predictor and criterion variables. The purpose of the study is to measure the correlations among the variables. Then tangibility, reliability, responsiveness, assurance and empathy are considered a single predictor construct as SERVQUAL. Service quality is considered a single criterion construct under the name of overall service quality. Also, the co-relational study was conducted to institute the actuality of connections among the variables. A co-relational study measures the degree of relationship between two or other variables. So in this exploration, the ideal is to identify and dissect the relationship among the variables by using Descriptive statistics to find out the service quality of Sonali Bank Limited.

### b) Sampling Method

For this study, the population is the customers of Sonali Bank Limited. Judgmental sampling is used for drawing samples from the population since only the University of Dhaka Branch customers are to be surveyed. Judgmental samplings anon-probability sampling approach where the experimenter selects units to be tried grounded on their knowledge and professional judgment.

The study is limited to clients of Sonali Bank, Dhaka University Branch of Standard. Convenience arbitrary sampling system has been espoused to elect clients from the Branch. A sample of two hundred clients, inversely in male and female, aged 18 and over, was requested to fill the questionnaire.

### c) Survey Instrument

The questionnaire is used to gather data for this exploration. The explanation for using questionnaire is the obscurity of the replies and time constraints for both the experimenter and the client. A structured questionnaire is used to collect data from the Retail customers of the Sonali Bank. SERVQUAL was firstly used for assessing client comprehension of service quality in service and merchandising associations. This instrument has been the predominant style used to measure customers' comprehension of service quality. It has five general confines or factors are:

- Tangibility

- Reliability

- Responsiveness

- Assurance (including capability, courtesy, credibility and security)

- Empathy (including access, communication, understanding of the clients) Tangibles

For this exploration, a non-difference score measure was used, and the score for each dimension of service quality was reckoned by taking the average score in particulars making up the dimension, in this case, four particulars per dimension.

The system was used to calculate the unweighted SERVQUAL score is given below in Table

Table 1: Computation to obtain un-weighted SERVQUAL Score

<table><tr><td>Average Tangible SERVQUAL score</td><td></td></tr><tr><td>Average Reliability SERVQUAL score</td><td></td></tr><tr><td>Average Responsiveness SERVQUAL score</td><td></td></tr><tr><td>Average Assurance SERVQUAL score</td><td></td></tr><tr><td>Average Empathy SERVQUAL score</td><td></td></tr><tr><td>Total</td><td></td></tr><tr><td>Standard (=Total/5) UNWEIGHTED SERVQUAL SCORE</td><td></td></tr></table>

### d) Questionnaire Design

The service quality questionnaire is attained from SERVQUAL's question list. Data was collected through a pre-structured questionnaire. The questionnaire is developed to identify the underpinning confines of bank quality and assess Sonali Bank Limited's service quality. The SERVQUAL model was used for Questions in Part-I, composed of 17 questions to measure the crucial confines of service quality: reliability, empathy, responsiveness, assurance, and tangibles.

Part 2 contains questions regarding the demographic information of the replies (age, gender, occupation). The SERVQUAL model was used for Questions in Part-I, composed of 17 questions to measure the crucial confines of service quality: reliability, empathy, responsiveness, assurance, and tangibles. The first 11 questions of each item are on 5 points Likert scale ranging from 1 (enormously differ) to 5 (strongly agree). This study concentrates on 5 "Quality Characteristics", which were preliminary placed significant by various studies with many uniquely functional characteristics, especially in the SERVQUAL model. In other information questions, there are double-barreled questions, Dichotomous questions, and Multiple Choice questions. The guests were named by Hypercritical Probability Slice. The qualitative is data converted into quantitative. SPSS 20 was used to dissect the data

### e) Data Analysis Techniques

i. Descriptive Statistics: Descriptive statistics were used to dissect the variables. The mean and Standard Deviation of the dimension indicators were used to conclude the overall service quality of Sonali Bank Limited. ii. Regression Analysis: Multivariate regression analyses were performed to understand the overall service quality of Sonali Bank Limited. All the regressions were direct in parameter. Overall service quality was used as the dependent variable, and Tangibility, Reliability, Responsiveness, Assurance and Empathy were Independent Variables.

## iii. Hypothesis Testing:

Null Hypothesis (H0) = Overall Service Quality does not depend on tangibility, reliability, responsiveness, assurance and empathy.

Alternative Hypothesis (H1) = Overall Service Quality depends on at least one of the following variables: tangibility, reliability, responsiveness, assurance, and empathy.

## V. DATA ANALYSIS & FINDINGS

### a) Regression Analysis

Table 2: List of Regression Equations

<table><tr><td>Description</td><td>Regression Equation</td><td>Regression Type</td></tr><tr><td>Overall Service Quality (Dependent)</td><td rowspan="6">Overall Service Quality= 1.014 +2.356 Tangibility +1.150 Reliability -.7 78 Responsiveness -.994 Assurance + 6.629 Empathy</td><td rowspan="6">Multiple</td></tr><tr><td>Tangibility (Independent/Predictor)</td></tr><tr><td>Reliability (Independent/Predictor)</td></tr><tr><td>Responsiveness (Independent/Predictor)</td></tr><tr><td>Assurance (Independent/Predictor)</td></tr><tr><td>Empathy (Independent/Predictor)</td></tr></table>

The Multiple Regression Equation is found as:

- In this equation coefficient of tangibility is 2.356, which indicates that if the score of Tangibility increases by 1 point, the score of overall service quality increases by 2.2356, provided Reliability, Responsiveness, Assurance, and Empathy remain unchanged.

- In this equation coefficient of reliability is 1.150, which indicates that if the score of Reliability increases by 1 point, the score of overall service quality increases by 1.150, provided Tangibility, Responsiveness, Assurance and Empathy remain unchanged. The regression function shows a positive relation between reliability and overall service quality.

- In this equation coefficient of responsiveness is -.778, which indicates that if the score of responsiveness increase by 1 point, the score of overall service quality decreases by.778, provided Tangibility, Reliability, Assurance, and Empathy remain constant.

- > In this equation coefficient of assurance is -.994, which indicates that if the score of assurance increase by 1 point, the score of overall service quality decreases by.994, provided Tangibility, Reliability, Responsiveness, and Empathy remain unchanged.

- In this equation coefficient of empathy is 6.629, which indicates that if the score of Empathy increases by 1 point, the score of overall service quality increases by point 6.629, provided

Tangibility, Reliability, Responsiveness, and Assurance remain unchanged.

The association among the Independent Variables in relative expression

The relationship among the Independent Variables in relative terms can be assessed with the help of multiple corrlatives

$$

R = . 4 6 8

$$

It indicates a Moderate degree of positive relationship among Tangibility, Reliability, Responsiveness, Assurance and Empathy.

can be assessed with the measure of multiple determinants. Then multiple regression yields a measure of multiple determinations,

$$

\mathrm {R} ^ {2} = 0. 2 1 9

$$

That indicates that $21\%$ of the variation in overall service quality can be explained by the combined variation of tangibility, reliability, responsiveness, assurance and empathy.

Relative Importance of Independent Variables

The relative importance of the independent variables (tangibility, reliability, responsiveness, assurance and empathy) can be indicated with the help of the Beta coefficient, and to do so, a normalized regression equation has been calculated. The regression equation is

### b) Correlation Matrix

Table 3: Pearson Correlation Matrix

<table><tr><td></td><td>Tangibility</td><td>Reliability</td><td>Responsiveness</td><td>Assurance</td><td>Empathy</td><td>Service Quality</td></tr><tr><td>Tangibility</td><td>1</td><td>0.418</td><td>0.413</td><td>0.401</td><td>0.071</td><td>.182</td></tr><tr><td>Reliability</td><td>.418</td><td>1</td><td>0.596</td><td>0.486</td><td>0.132</td><td>0.144</td></tr><tr><td>Responsiveness</td><td>0.413</td><td>0.596</td><td>1</td><td>0.567</td><td>0.148</td><td>0.078</td></tr><tr><td>Assurance</td><td>0.601</td><td>0.486</td><td>0.567</td><td>1</td><td>0.123</td><td>0.149</td></tr><tr><td>Empathy</td><td>.071</td><td>0.132</td><td>0.0418</td><td>0.123</td><td>1</td><td>0.431</td></tr><tr><td>Service Quality</td><td>0.182</td><td>0.144</td><td>0.078</td><td>0.049</td><td>0.431</td><td>1</td></tr></table>

From the Table 4, We have seen that there is no presence of severe multidisciplinary among the dependent variables. Which is desirable.

### c) Test of Hypotheses

- Null Hypothesis $(\mathrm{H\_0}) =$ Overall Service Quality does not depend on Tangibility, Reliability, Responsiveness, Assurance and Empathy.

- Alternative Hypothesis (H_1) = Overall Service Quality depends on at least one of the following

variables- Tangibility, Reliability, Responsiveness, Assurance and Empathy.

To accomplish test of hypotheses, Analysis of Variance (ANOVA) is used. According to Analysis of Variance (ANOVA), if estimated F_E is more significant than the Critical or Table value of F then Null Hypotheses (H_0) will be rejected, which means Alternative Hypotheses (H_1) will be accepted. For analysis of Variance, the selected Significance level is $5\%$.

Table 4: Analysis of Variance

<table><tr><td colspan="2">Model</td><td>Sum of Squares</td><td>df</td><td>Mean Square</td><td>\(F_{E}\)</td><td>Sig.</td></tr><tr><td rowspan="3">1</td><td>Regression</td><td>67.112</td><td>5</td><td>13.422</td><td>10.906</td><td>.000</td></tr><tr><td>Residual</td><td>238.768</td><td>194</td><td>1.231</td><td></td><td></td></tr><tr><td>Total</td><td>305.880</td><td>199</td><td></td><td></td><td></td></tr><tr><td colspan="7">Dependent Variable: Overall Service Quality of Sonali Bank Bangladesh Limited</td></tr><tr><td colspan="7">Predictors: (Constant), Empathy, Responsiveness, Tangibility, Reliability, Assurance</td></tr></table>

Here, the Estimated value of $F\_E = 10.906$ >Table value of $F\_T = 9.12$, which means Null Hypotheses (H_0) is Rejected that Overall Service quality does not depend on Tangibility, Reliability, Responsiveness, Assurance, Empathy and Alternative

Hypotheses (H_1) is Accepted that Overall Service Quality depends on at least one of the following mentioned variables- reliability, responsiveness, assurance and empathy, tangibility,

### d) Descriptive Statistics (Measuring Opinion of Customers Regarding the Service Quality)

Table 5: Mean and Standard Deviation obtained in the Survey and Remarks

<table><tr><td>Variables</td><td>Mean</td><td>Std. Deviation</td><td>N</td><td>Remark</td></tr><tr><td>Overall Service Quality</td><td>3.340</td><td>1.239</td><td>200</td><td>Moderate</td></tr><tr><td>Tangibility</td><td>2.00</td><td>1.62</td><td>200</td><td>Not Satisfactory</td></tr><tr><td>Reliability</td><td>2.33</td><td>1.50</td><td>200</td><td>Not Satisfactory</td></tr><tr><td>Responsiveness</td><td>2.94</td><td>0.47</td><td>200</td><td>Not Satisfactory</td></tr><tr><td>Assurance</td><td>3.59</td><td>1.60</td><td>200</td><td>Moderate</td></tr><tr><td>Empathy</td><td>5.00</td><td>1.21</td><td>200</td><td>Satisfactory</td></tr></table>

## VI. CONCLUSION

Sonali Bank Ltd. is furnishing and maintaining affable working terrain to deliver better quality services and an edge over the challengers. It is not possible to do a profitable business without concerning the client's benefits. SBL has a remarkable eventuality in the country to achieve the asked position in the request. This exploration has brought some intriguing sapience into what kind of service the clients give significance and

what quality service they get from SBL. It is relatively egregious that the client's conditions are not entirely met, and they are sometimes displeased with some of the aspects of the Bank. SBL should attract these clients so that the Bank can link over solid relationships with the clients. The efficiency and effectiveness in services only in client service is not obligatory. The only thing a service-acquainted company offers is service. The key to effective client service for internet banking lies in its capability to identify the quality determinants. From the studies and analysis, it is clear that the client's evaluations of the service quality and service delivery process depend on these factors: reliability, responsiveness, assurance, empathy, and its immediate outgrowth feel to be most influential on their overall service quality comprehensions. More comprehension of service delivery leads to client satisfaction. In SBL, Tangibility, Reliability, and Empathy positively affect Overall Service Quality, and Responsiveness and Assurance negatively impact Service Quality. Customer perception reveals that Tangibility, Reliability, and Responsiveness of Sonali Bank Limited are not satisfactory, while Assurance and Empathy are founded as moderate and satisfactory, respectively.

Generating HTML Viewer...

References

18 Cites in Article

Tasneema Afrin (2012). Quality of Customer Service in the Banking Sector of Bangladesh: An Explorative Study.

(2016). Bangladesh Development Update, October 2016.

Mohammad Hossain,Takdir (2010). Measuring Service Quality: A Comparative Analysis Between.

K Malhotra,Naresh,Dash,Satyabhushan (2010). marketing research: an applied orientation.

Md Mia,Rahman Hannan,Mohammad Anisur,Nitaichandra Debnath (2007). Consumer behavior of Online Banking in Bangladesh.

Peter Rose (1999). Commercial Bank Management.

Mohammad Shamsuddoha (2008). Development of Electronic Banking in Bangladesh.

Sonali Bank,Ltd (2016). The World Bank Annual Report 2016.

Bangladesh Bank (2014). Extended Producer Responsibility: For Advancing Circular Economies for Plastics in Bangladesh.

Madhukar Angur,Rajan Nataraajan,John Jahera (1999). Service quality in the banking industry: an assessment in a developing economy.

Muslim Amin,Zaidi Isa (2008). An examination of the relationship between service quality perception and customer satisfaction.

E Babakus,G Boller (1992). An Empirical Assessment of the SERVQUAL Scale.

R Bolton,J Drew (1991). A Multistage Model of Customers' Assessments of Service Quality and Value.

M Al-Hawari (2008). Automated service quality as a predictor of customers' commitment.

(2006). Financial Sector Assessment : Bangladesh.

Josée Bloemer,Ko De Ruyter,Pascal Peeters (1998). Investigating drivers of bank loyalty: the complex relationship between image, service quality and satisfaction.

J Devlin (2001). Consumer evaluation and competitive advantage in retail financial services: a research agenda.

R Faullant,K Matzler,J Fuller (2008). The impact of satisfaction and image on loyalty: the case of alpine ski resorts.

No ethics committee approval was required for this article type.

Data Availability

Not applicable for this article.

How to Cite This Article

Nafisa Tasnim. 2026. \u201cAnalyzing Customer Service Quality of State-Owned Commercial Banks in Bangladesh: A Study on Sonali Bank Limited\u201d. Global Journal of Management and Business Research - E: Marketing GJMBR-E Volume 22 (GJMBR Volume 22 Issue E2).

Explore published articles in an immersive Augmented Reality environment. Our platform converts research papers into interactive 3D books, allowing readers to view and interact with content using AR and VR compatible devices.

Your published article is automatically converted into a realistic 3D book. Flip through pages and read research papers in a more engaging and interactive format.

Our website is actively being updated, and changes may occur frequently. Please clear your browser cache if needed. For feedback or error reporting, please email [email protected]

Thank you for connecting with us. We will respond to you shortly.