## I. INTRODUCTION

The concomitance of the development of the Internet and mobile telephony has had an outstanding influence on the lives of many people in both developing and developed countries (Fall, Ky and Birba, 2015), even though they are not the only factors contributing to current progress. Although it is a relatively recent creation, mobile money (or mobile payment) has already made a positive and lasting impact on the socio-economic landscape of developing countries where the banking rate is low, imposing a revolution in money. Mobile currency is likely an incremental innovation from service delivery companies, specifically mobile network operators aiming for significant growth in their customer base, in digital financial services accessible to all individuals via mobile phones.

According to the definition given by Ondrus and Pigneur (2005), as referenced by Bidiasse and Mvogo (2019), mobile money is a transaction of monetary value between two parties, through the channel of a mobile device capable of securely processing a financial operation over a wireless network. Thus, mobile money is essentially a financial service provided through a mobile network, which allows users to directly make deposits and withdrawals of funds into their SIM card, to transfer funds via short messages, to pay bills (Mbiti and Weil, 2013), according to a certain fee. In this way, the phone number serves as the account number. Mobile money, according to the definition given by Ondrus and Pigneur (2005), as referenced by Bidiasse and Mvogo (2019), is a transaction of monetary value between two parties, through the channel of a mobile device capable of securely processing a financial operation over a wireless network. Thus, mobile money is essentially a financial service provided by a mobile network, which allows users to directly make deposits and withdrawals of funds into their SIM card, to transfer funds via short messages, to pay bills (Mbiti and Weil, 2013), according to a certain fee. In this way, the phone number serves as the account number.

The World Bank (2025) presents financial inclusion as "the ability for individuals and businesses to access a full range of financial products and services (transactions, payments, savings, credit, insurance) that are affordable, useful, tailored to their needs, and offered by reliable and responsible providers." The field of financial inclusion has experienced unprecedented upheavals in terms of digital finance with the development, especially, of mobile money services (Thulani, Chitakunye, and Chummun, 2014, cited by Ngono, 2020), which have become essential, combining practicality with usefulness. Indeed, being more accessible and easier to use, mobile money has helped overcome some clear and compelling barriers that hindered the efforts for a significant transformation of the traditional financial sector. While it is clear that the demand for mobile money services should remain high, various and complex challenges, such as the lack of reliability on the mobile and electricity networks and the lack of digital culture, present significant obstacles that require effective responses to improve financial inclusion. In this regard, the issue on the use, or resistance to the use of mobile money is a subject of current concern. For this reason, understanding the background of the actual use of mobile money services must be an immediate priority and not a fundamentally meaningless research pursuit.

"In the field of technology usage, this type of study falls under what is commonly referred to as the study of usages" (Terrade et al., 2009: 384). Theoretically, the foundations of the Unified Theory of Acceptance and Use of Technology - UTAUT, known as " théorie unifiée de l'acceptation et de l'utilisation de la technologie" in French - by Venkatesh et al. (2003) have been mobilized to anticipate the acceptance and usage behavior of mobile money services in various contexts. The UTAUT model has been integrated with other individual models such as the Technology Acceptance Model (TAM) proposed by Davis (1989). It has been judged the most robust, reliable, and predictive, possessing great explanatory power regarding the intention to use a technology. The theoretical model derived from this theory is deterministic, as it associates individuals' intentions with actions of utilizing a new technology.

The utility of the UTAUT framework (Venkatesh et al., 2012; 2003) in the study of mobile money services has been demonstrated in previous studies such as those by Ndjambou, Olaba, and Vinga (2023), Nur and Panggabean (2021), Sossou, Gaye, and Wade (2021), Kofi Penney et al. (2021), Kuria Waitara et al. (2015), Osman, Tareq, and Matsuura (2020), and Lee, Lee, and Rha (2019). Tobbin (2010) models the antecedents of consumer behavior towards the adoption of mobile money transfer in Ghana. In this perspective, he combines Davis's Technology Acceptance Theory (TAT) (1989) with Roger's Innovation Diffusion Theory (IDT) (1991): to the two essential variables of TAM (perceived usefulness, perceived ease of use), the author adds some aspects of IDT (traceability, relative advantage). The structure is supported by other constructs such as perceived risk, perceived trust, transaction cost, and testability (trialability). On one hand, the analysis confirms the relationship of the TAM between perceived usefulness and the intention to adopt a new technology. Relative advantage would have a positive effect on perceived usefulness. On the other hand, it finds that perceived ease of use predicts users' intention to use mobile money transfer services. The structural links between trust and the adoption of mobile currency as well as the trial and adoption of mobile currency have also both proven to be significant.

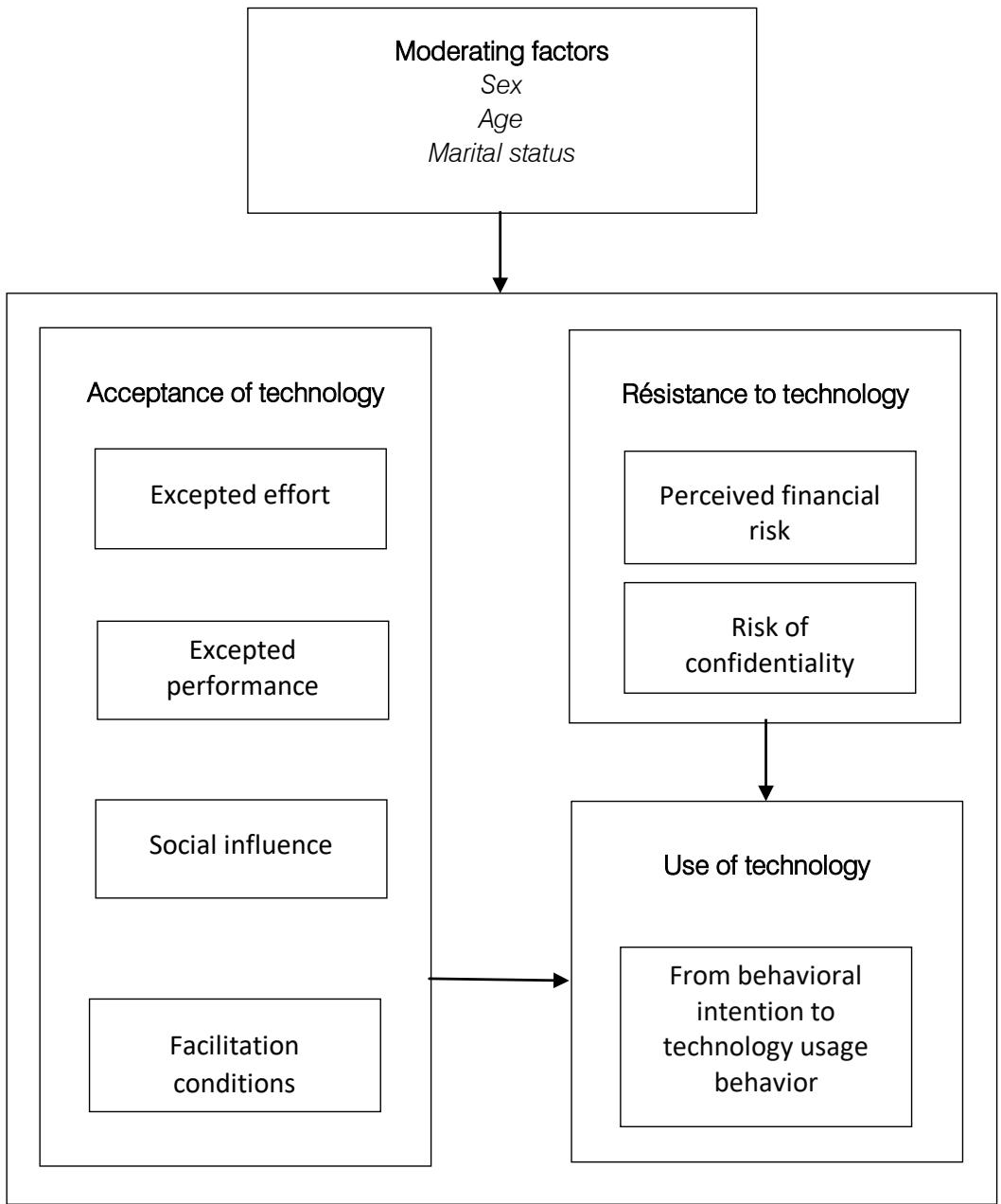

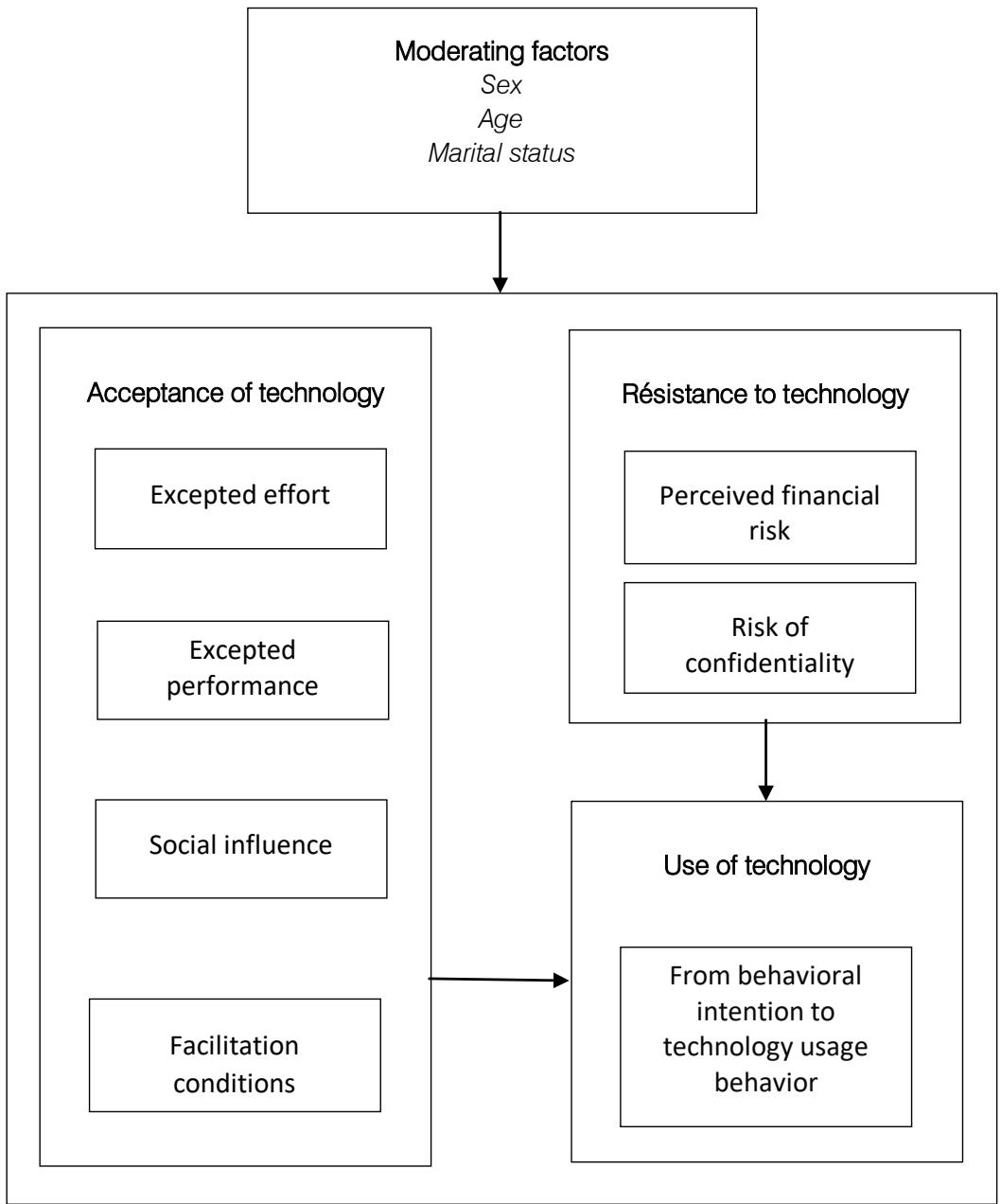

The main objective of this article is to assess the impact of moderating factors on behavioral intuition and the usage behavior of mobile money technology. It seeks to answer the question: to what extent do key factors such as age, gender, and marital status affect the degree of resistance to the use of mobile money technology in the specific context of Congo? To this end, it is essential to have a theoretical framework, and after a systematic review of the literature, a comprehensive approach is adopted to better understand the issue at hand and to lead to managerial implications. This research applies the framework of the revised UTAUT model, integrating perceived risks (financial risk, risk of confidentiality). It focuses on a mobile phone operator, Airtel Congo, and its customers in the Brazzaville department. It particularly addresses the predictions that can be made regarding the use of a service or technology a posteriori, that is to say, after it has been put into service. Undoubtedly, it is possible to foresee the study of usages a priori to understand the acceptance of a service or technology.

In order to address the core question, a quantitative approach was adopted and 500 questionnaires were distributed to users of Airtel Money services (420 questionnaires were returned to us, representing a response rate of $84\%$ ). Moreover, to empirically analyze such an issue, the use or resistance to the use of mobile money is not considered here as an attribute that an individual possesses or does not possess, but as a situation whose intensity varies from one individual to another. Furthermore, the use or resistance to the use of mobile money is perceived as a fuzzy multidimensional condition. The dimensions are constructed based on the revised UTAUT.

The main attraction of multi-dimensionality lies in the possibility of referring the analysis to a vast array of fuzzy indicators of subjective assessments (including "pre-test before adoption," "ease of use," "service convenience," "social influence," "perceived usefulness," and "service costs"), facilitating conditions ("income," "level of education," and "status"), and perceived risks ("financial risk" and "risk of confidentiality") on one hand, and calculating indices that allow for assessing the situational dimension, considering different aspects of resistance to mobile money, on the other hand. Initiated by Zadeh (1965) and developed by Dubois and Prade (1980), "fuzzy set theory provides a formal framework, a logical support, and a rigorous mathematical tool to axiomatic" (Rolland-May, 1987: 47) and to explaining fuzzy behaviors, notably: fuzzy behaviors. And, by deploying the approach based on totally fuzzy and relative logic (TFR) operationalized by Cheli and Lemmi (1995), which fundamentally interrogates the nature of frequencies and proposes a membership function, the degree of an individual's resistance to the use of mobile money is explicitly formulated as their degree of membership in a fuzzy set of resistants to imprecise limits.

This article aims at not only enriching the academic literature: theorists on the factors of acceptance and use of a new technology, that will find information on certain utility to improve their conjectures and theoretical assumptions, and theorists on fuzzy sets, who will discern a concrete illustration of their theory regarding the degrees of resistance to the use of mobile money, but also providing practical insights for professionals in terms of the issue of mobile money.

The rest of the article is organized in such a way that first, we explore a literature review of theories and models for measuring technology acceptance, prior to outlining the research model we adopt. Finally, we explain our research methodology and the data analyses performed.

## II. LITERATURE REVIEW

The outstanding question in this authentic research corpus is the following: what are the factors that promote the adoption of a technology by the user? The literature on this question has been the subject of several research works. It presents multiple models derived from theories that explain technology adoption (cf. Engesser et al., 2023). These models involve different measurement constructs. Aside from the divergence of their key constructs, the works continue to share common concerns, particularly the following (Kéfi, 2010) ones: 1) to use individual measurement factors with predictive power on one hand; and 2) to reflect one of the following causal order patterns: "beliefs-cognition-intention" or "beliefs-affect-intention", on the other hand.

A more classic explanation on these two variants of causal order diagrams proposed in the literature is provided by Ortiz de Guinea and Markus (2009). Theories linking cognitive order factors assume a rational calculation and a comparison in terms of advantages or disadvantages by users who assess the confirmation (or non-confirmation) of expected benefits, taking into account a number of constraints. Among these factors, we cite perceived ease of use, perceived utility, perceived behavioral control, etc. Many authors, such as Fishbein and Ajzen (1975), Bagozzi (1982), Kim and Malhotra (2005), Thong, Hong, and Tam (2006), Hsieh, Rai, and Keil (2008), have indeed confirmed the emphasis laid on such factors in understanding intentions.

Whereas the theory linking affect obscure the non-cognitive emotional and affective factors such as attitude, satisfaction, perceived enjoyment, affect, computer anxiety, subjective norms, etc. Many authors have been able to illustrate the critical role of these factors: Davis et al. (1992), Malhotra and Galletta (1999), Venkatesh (2000), and Bhattacherjee (2001).

The preceding works on the understanding of the issue related to intention are: the Theory of Reasoned Action (Fishbein and Ajzen, 1975), the Theory of Planned Behavior (Ajzen, 1985), social cognitive theory (Bandura, 1986), motivation theory (Davis, Bagozzi and Warshaw, 1989), the diffusion of innovations theory (Rogers, 1962, 1983, 1995), the computer usage theory (Thompson, Higgins and Howell, 1991), the Technology Acceptance Theory (Davis, 1989), and the mixed theory combining the Technology Acceptance Theory (Davis, 1989) and the Theory of Planned Behavior (Taylor and Todd, 1995). A unified theory of acceptance and use of technology (Venkatesh et al., 2003) has been proposed, which identified five key constructs: performance expectancy, effort expectancy, social influence, facilitating conditions, and behavioral intention.

### a) Theoretical Literature and Development of the Conceptual Framework

The core question in this research corpus is the following: what are the factors that promote the adoption of mobile money technology by the user? Here, we explore the most significant theories that have shaped our understanding of this complex research question, and which will help construct our conceptual model.

## i. Basic Theories and Models

The theories developed over the years have evolved, and are the result of particular and increased efforts in validating and extending the models, which have been carried out during the period in which each was produced.

a. Theory of Reasoned Action (TRA)

Implemented by Fishbein and Ajzen (1975) and framed within a social psychology context, it establishes that behavior is directly and solely determined by behavioral intention. The intention to adopt a given behavior is influenced by two key constructs (or key factors) which are determining elements, namely:

- The individual's attitude towards this behavior, defined as the positive or negative feelings regarding the performance of a behavior;

- The subjective norm (or social influence), defined as an individual's perception of the opinion of people that are important to them regarding whether or not they perform a given behavior.

The TRA has helped explain the interdependence between attitude, subjective norm, and the intention to adopt a behavior (cf. Sossou, Gaye, and Wade, 2021); which is essential for understanding technology adoption. This theory has also been used to instruct technology adoption in an organizational context.

Ajzen and Fishbein (1980) aimed to produce an original theoretical framework for analyzing human behavior, focusing on the relationship between certain specific variables that could lead to a possible model for predicting intentions and behaviors, highlighting beliefs, attitudes, subjective norms.

And thus, this influential theory had its limitations, not taking into account factors other than personal ones. It is consequently following this observation that Ajzen developed, in 1985, the Theory of Planned Behavior which, in its own way, sought to provide answers to the major limitations of the hypotheses formulated by the TRA and, therefore, a model that also considers factors not directly under the control of individuals.

### b. Theory of Planned Behavior (TPB)

After addressing the issue of voluntary control, since the TRA originally only concerned volitional behaviors that are entirely under the control and decisions of an individual regarding a given behavior, Ajzen (1985) attempted, in his own way, to resolve it by proposing an extension of the TRA, called the Theory of Planned Behavior (TPB). However, it is Ajzen (1991) who formulated the most precise TPB, aimed at interpreting behaviors that are not under the volitional control of the individual and popularized it in the literature. By emphasizing this main idea, Ajzen (1991) introduced a third essential construct in the TPB, namely: the perception of control over behavior, reflecting the perceived ease or difficulty of adopting a given behavior. This variable allows for going beyond the limitations of the TRA, by taking into account the external or internal factors that influence the individual's ability to adopt a new technology in the understanding and adequate prediction of human behavior. This one fully takes into account the roles of organizational members, individuals, and social systems in this process (cf. Ajzen, 1991).

Thus, the TPB considers a total of three key constructs: attitude (adapted from the TRA), perceived social influence (adapted from the TRA), and perceived behavioral control.

## c. Social Cognitive Theory

Propounded by Bandura (1986), it actually aims at describing individual behavior through the ongoing and reciprocal interactions between three elements, namely: The individual (internal personal factors), behavior (cognitive factors), and external events (environmental factors). The interaction is triadic: individual-behavior interaction; individual-environment interaction; and environment-behavior interaction.

According to Bandura (1986), behavior is the product of personal and environmental factors, which mutually influence each other, rather than a response to a single external stimulus. Furthermore, personal factors are the same for all individuals. They include cognitive processes, affects, and biological components. The concept of the environment consists of three dimensions: the imposed environment (which acts upon the individual, regardless of whether they agree with it or not), the chosen environment (that which the individual pays attention to), and the constructed environment (what the individual creates to exert better control over their life).

The general socio-cognitive theory of Bandura provides good reasons to justify that behavior is not solely a function of the interaction between personal and environmental factors. The interaction should be seen as a reciprocal and continuous determinism, which significantly influences the three factors in a mutually interdependent way. Moreover, the relative force of influence of these three elements varies according to the contexts.

This theory evokes three complementary constructs that take into account the individual in a global context and environment (cf. Bandura, 1986):

- Outcome expectations, which represent the individual's beliefs about the likely consequences and results of a given behavior;

- Socio-cultural factors, that illustrate the levers or barriers to the adoption of particular behaviors;

- Personal goals, which are one of the main sources of motivation (Bandura, 1986). They are defined as the intention that an individual has, in effect, to engage in a specific activity to achieve a particular goal (Bandura, 1986). Long-term goals function to guide behaviors, while short-term goals function to regulate effort and guide action.

Bandura's social cognitive theory, with its ideas on reciprocal triadic causation, provides a useful framework for explaining the adoption of a technology.

## d. Theory of Diffusion of Innovations (TDI)

The theory of diffusion of innovation (known as Innovation Diffusion Theory in English) was devised in 1962 by Rogers in his emblematic work Diffusion of Innovations, updated in 1983, and has been applied both on an individual level (Rogers, 1995) and on an organizational level (Zaltman, Duncan, and Holbeck, 1973). According to Rogers (1983, 1995), diffusion is "the process by which an innovation is communicated, over time and through certain channels, among the members of a social system" (1983: 5). This theory focuses not on invention, but rather on the 'after' of technical innovation, or more precisely on its dissemination (Fèvres, 2012). The TDI has the advantage of providing a conceptual framework for the concept of acceptability, since its goal is to explain how a technological innovation evolves from the stage of invention to that of widespread use.

Moreover, the decision-making process follows five stages (Rogers, 1995):

- The awareness of an innovation, which is the information phase: initially, the individual expresses the need to have the technology, seeks to acquire information about the existence, use, or functioning of an innovation, and assesses its suitability for their problem. During this phase, the individual reacts

based on their personal profile and the social system in which they operate;

- Persuasion, which is the Phase of Interest: The one where the individual forms a favorable or unfavorable attitude towards the considered innovation. During this phase of the decision-making process, five key constructs play an important role (Rogers, 1983): relative advantage in economic and social terms (this is the degree to which an innovation is perceived as being better than those that already exist); compatibility with the values of the group to which one belongs (this is the degree to which an innovation is perceived as being consistent with existing values, past experiences, social practices, and norms of the users); the complexity of innovation (the degree to which an innovation is perceived as difficult to understand and use); testability (the possibility of testing an innovation and modifying it before committing to use it); visibility of results (the degree to which the results and benefits of an innovation are clear to others). These perceived attributes of innovation are the subject of specific inquiries;

- The Decision: The individual (or an organization) engages in activities of use/evaluation that will allow them to adopt or reject the innovation;

- The Implementation: The individual makes use of this innovation. At this stage, they need assistance to reduce uncertainties about the consequences;

- The Confirmation: The individual seeks reinforcement regarding the decision they have already made; they attempt to obtain information that will subsequently reinforce their choice, but there is a possibility of reverting back to their choice.

### e. Theory of Personal Computer Use (TPCU)

Thompson et al. (1991) delve deeper into Triandis's (1977) theory to adapt it to the specific context of information systems. They built and employed their theory to describe and predict personal computer use as a dependent variable. More specifically, this theory is based on a set of six key constructs. These essential constructs are as follows:

- Job Fit: The degree to which an individual believes that using a technology can improve their job performance (Thompson et al., 1991: 129);

- Complexity, which corresponds to "the degree to which an innovation is perceived as relatively difficult to understand and use" (Thompson et al., 1991: 128);

- Long-Term Consequences: They refer to "outcomes that have impacts in the future" (Thompson et al., 1991: 129);

- Affect, Regarding use (Adapted from Triandis, 1977): It corresponds to "feelings of joy, exhilaration or pleasure, or of depression, disgust, dissatisfaction

- Or Hatred Associated by an Individual with a Particular Act" (Thompson et al., 1991: 127);

- Social Factors (Adapted from Triandis, 1977): They are defined as "the internalization by the individual of the subjective culture of the reference group, and the specific interpersonal agreements that the individual has made with others, in specific social situations" (Thompson et al., 1991: 126);

- Facilitating Conditions (Adapted from Triandis, 1977): These are objective factors arising from the environment that users have no control over it.

### f. Motivational Theory of Technology Acceptance (MTAT)

Supported by Davis et al. (1989), the motivational theory of technology acceptance is based on the intrinsic and extrinsic motivation from Deci and Ryan's Self-Determination Theory (SDT) (1985). Extrinsic and intrinsic motivations are the key constructs for measuring an individual's intention to adopt technology usage behavior:

- Intrinsic motivation to use technology refers to the perceived pleasure of using technology, regardless of the performance outcome that may be achieved;

- Extrinsic motivation to use a technology at work - provided that this technology is perceived as useful for achieving these goals - will be supported by an expected or anticipated reward.

Motivational theory, aimed at explaining the adoption of technology by users through modeling intrinsic and extrinsic motivation, helps understand how the environment influences individual intentions to smartly engage in technology use behavior.

### g. Technology Acceptance Theory (TAT)

Davis (1989), informed by two cognitive theories, namely: the Theory of Reasoned Action (TRA) by Ajzen and Fishbein (1980) and Triandis' decision-making behavior theory (1980) which establishes that an individual's choice stems from a cognitive choice between the effort required and the quality of the action (resulting decision), constructed the TAT. This theory "has the advantage of integrating several aspects of individual behavior theories developed by social psychology." (Baile, 2005: 12).

The TAT is based on key constructs that relate to (Davis, 1986):

- Perceptions: Perceived usefulness and perceived ease of use;

- The Subjective Norm Adapted from TRA (Ajzen and Fishbein, 1975): attitude influences the formation of individual intentions to use a technology.

Perceived usefulness corresponds to the degree to which a person believes that using a particular technology will enhance their professional performance and productivity effectively and efficiently (Davis, Bagozzi, and Warshaw, 1989; Hong et al., 2001/2002;

Venkatesh et al., 2003; Brangier et al., 2010; Fadwa and Ez-zohra, 2019). As for perceived ease of use, it refers to the degree to which a person thinks that using a given technology does not require effort (Davis, Bagozzi, and Warshaw, 1989; Hong et al., 2001/2002; Venkatesh et al., 2003; Brangier et al., 2010; Fadwa and Ez-zohra, 2019). The Technology Acceptance Theory (TAT) provided initial insight into the role of attitude in forming individual intentions.

These constructs induce behavioral intentions to use a technology. Models derived from this theory assert that technology use intentions are functions to attitudes, the latter being influenced by the perceived usefulness and ease of use (usability) according to users (Poyet, 2015). Several studies have found that the two general and abstract representations of perception, according to the TAT, namely perceived usefulness and perceived ease of use, are fundamentally relevant in explaining the factors that users may consider before accepting and using a new technology (see for example Tobbin, 2010). However, Moon and Kim (2001) specify that these basic concepts alone are likely insufficient to denote the influence of factors that seem to encourage the actual use of a technology.

Most researches based on social cognition have been conducted within the framework of the Technology Acceptance Model (TAM) and its various versions: TAM1 (Davis, 1989), parsimonious TAM (Davis, Bagozzi, and Warshaw, 1989), TAM2 (Venkatesh and Davis, 2000), and TAM3 (Venkatesh and Bala, 2008).

In fact, the optimism of the main teachings of the TAM has been nuanced by a more or less in-depth criticism by Venkatesh and Davis (2000). These authors were indeed concerned with the limitations of the original TAM model (TAM1) proposed by Davis (1989) and attempted to extend this first version by adding cognitive and social influence variables, admitting that the latter variables have an influence on the beliefs associated with perceived utility; which led to TAM2. In this perspective, they emphasized the following variables (cf. Bennaceur, 2019): subjective norm, voluntariness, image, experience or ability to use a technology, relevance to work, output quality of a technology, demonstrability of results. However, the conclusions drawn about perceived usefulness, perceived ease of use, intention to use, and usage behavior were produced by the findings of the original model (Bennaceur, 2019). The TAM2, which has the same theoretical foundation as Davis's model (1989) and focuses only on the determinants related to perceived usefulness and intention to use, did not undermine the conclusions of the original analysis.

TAM3, proposed by Venkatesh and Bala (2008), is an integration of Venkatesh and Davis's (2000) TAM2 and Venkatesh's (2000) model of the determinants of perceived ease of use. TAM2 added the antecedents of expected utility, while the perceived ease of use model focused on the determinants of perceived ease of use (this involved introducing control, intrinsic motivation, and emotion into the TAM). Thus, TAM3 produces a very comprehensive network of the determinants of technology adoption and use. However, Venkatesh (2000) argued that the TAM does not facilitate the explanation of individuals' acceptance of ICT, nor does it determine the criteria that have a real effect on perceived ease of use (cf. Fadwa and Ez-zohra, 2019).

Basic theories and models, although using different terminologies, interpret and justify similar concepts (Bourdon and Hollet-Haudebert, 2009). Under such conditions, the theoretical challenge has been to integrate them into a single theoretical whole. This theoretical challenge, which is well explained from a logical point of view, has given hope to those who advocated for it to turn to an attempt of modeling through integrated intentional models. This is the reason that made it possible to develop a unified theory of technology acceptance and use.

### h. Theory of Social Influence (TSI)

This theory was developed by Schmitz and Fulk (1991), who were inspired by the works of Bandura (1977), with the objective of demonstrating that an individual's behavior regarding the use of technological systems is influenced by the prevailing social context. Ultimately, it is possible to distinguish two fundamental constructs of the TSI:

- Social influence, which is noticed by the impact that social norms and the attitudes of work partners have on the individual's perception of the improvement of conditions when using a given technological system;

- The experience of potential users regarding technological systems, which is reflected by the past experiences of users with the technological system.

In short, the fundamental theories reviewed here hold truth and relativity within them; the conditions of this relativity are specified in the milestones and conceptual markers of a broader theory, which aims at integrating them.

## ii. An Integral Theory: The Unified Theory of Technology Acceptance and use (UTAUT)

In the existing and already abundant literature, one of the most popular theories that scrutinizes the intention to adopt a new technology or process is the unified theory of acceptance and use of technology. In 2003, a more thoughtful investigation, particularly with the works of Venkatesh and his associates who synthesized, through refinements of thought and simultaneous improvements of the model, the main theories on individual intention, resulted - with the adoption of the unified theory framework - in the integral theory. The unified theory of acceptance and use of technology, or UTAUT, represents, to this day, the most advanced theory of the intention to use new technologies (Jawadi, 2014; Désiré and Bordel, 2013), and the most widely used (Venkatesh, 2022; Venkatesh et al., 2003). It has been deployed in numerous studies, both theoretical and empirical, to strengthen expectations regarding the acceptance and use of technologies in diverse and varied situations. Venkatesh and his associates (2003) demonstrated the importance of four key drivers:

- Three are Direct Determinants of use Intentions: These are expected performance, expected effort, and social influence, and

- One Constitutes a Direct Determinant of use Behavior: Behavioral intention and facilitating conditions.

It is important to elaborate more for each of these concepts. Expected performance corresponds to the degree to which an individual believes that using a technological system should enhance their performance and capacity (Venkatesh et al., 2003). It is "a scale through which the person positions themselves according to their perception of the technology in terms of performance gains in their work, if they believe that using this system will help them improve their performance" (Lafraxo et al., 2018: 138).

The expected effort corresponds to the degree of ease inherent in using a system (Venkatesh et al., 2003). "This element refers to whether the future user perceives the system as easy to use, easily understandable, or usable without too much effort" (Désiré and Bordel, 2013: 4) and is explained by three concepts: complexity, perceived ease of use, and ease of use.

Social influence, adapted from the theory of social influence by Schmitz and Fulk (1991). Social influence is defined as the degree to which an individual perceives that important people in their life believe they should use the new system (Venkatesh et al., 2003: 451). Marinkovic and Kalinic (2017) consider that social influence plays a particularly important role in the early stages of developing new technologies, when a large number of users lack experience or information about the technology in question and consequently rely on public opinion. This variable assesses whether potential users can be directly influenced (through advice, encouragement...) or indirectly (through a positive or negative image...) by their peers (friends, colleagues...) or their hierarchy regarding whether or not to use the system (Désiré and Bordel, 2013: 4).

Facilitating conditions are a concept from the UTAUT, which are considered likely to have a direct impact on technology adoption. These conditions indicate the "degree to which an individual believes that an organizational and technical structure exists to support the use of the system" (Venkatesh et al., 2003:

453). This measure makes it possible to "assess the perception that future users have of the internal (knowledge, skills) and external (training, support, intermediary person) resources that they may have" (Désiré and Bordel, 2013: 4). While behavioral intention refers to the users' propensity to adopt a behavior (Ajzen, 2002). Thus, behavioral intention is noticed through people's actions. Furthermore, the effect of behavioral intention on the use of technology is well established in the existing literature (Venkatesh et al., 2012).

The UTAUT model includes other variables that moderate the influence of the four primary determinants of intention and usage behavior, referred to as moderating variables. The integration of these variables into the model helps address the inconsistencies and low explanatory power of previous models, and better explains the differences in behavior among different types of consumers (Venkatesh et al., 2003; Lee, Lee, and Rha, 2019). In general, it includes four main moderating variables:

- Three of which are individual and related to past experience with the system, age, and user gender;

- The last moderating variable relates to the context of use: the voluntary or involuntary nature of actual usage from the perspective of social psychology.

Venkatesh, Thong and Xu (2016) specify the four main exciting developments of the UTAUT model:

- The introduction of new exogenous mechanisms that refer to the impacts of external predictors on the four exogenous variables (expected performance, expected effort, social influence, and facilitating conditions) of the unified theory;

- The introduction of new endogenous mechanisms that refer either to the impact of new predictors on the two endogenous variables in UTAUT (i.e., behavioral intention and behavioral usage), or to the enrichment of the four exogenous variables and the two endogenous variables in the original UTAUT.

- The introduction of new moderation mechanisms that add new moderating effects to the original UTAUT, including the moderation of new relationships; - the introduction of new mechanisms that refer to the new consequences of behavioral intention and technology usage, which represent additions to the original UTAUT. Extensions of UTAUT are the category of research that has the greatest potential to make significant contributions to research on technology acceptance and use (Venkatesh et al., 2016).

The various aspects of the proposed representation being analyzed, our theoretical task seems almost accomplished, but it is still appropriate to question the value of this theoretical work, which provides a theoretical foundation for the empirical results to be obtained during empirical work. Thus, we propose to engage in a discussion of a few empirical studies solely in the field that interests us, that of mobile money.

### b) Empirical Literature

The dominant perspective in the literature on individual intention mainly focuses on analyzing new technologies (see for example: Davis, 1989; Fishbein and Ajzen, 1975). Regarding the field of mobile money, many authors, such as Nur and Panggabean (2021), Sossou et al. (2021), Kofi Penney et al. (2021), Osman et al. (2020), Lee et al. (2019), and Kuria Waitara et al. (2015), have been able to validate the robustness of the UTAUT model through empirical studies; which means that the theoretical and empirical knowledge related to this field can be considered robust.

Kuria Waitara et al. (2015), in the Kenyan case and using a sample of 248 people, apply structural equation modeling to model the adoption and use of mobile money transfer services and show that the independent variables (expected performance, expected effort, and social influence) have a significant impact on the behavioral intention to use mobile money. In contrast, facilitating conditions have no significant influence on the adoption and use of a given mobile money transfer system.

Lee et al. (2019) present the results of an empirical study conducted on a sample of 528 respondents in South Korea. The collected data were analyzed using the structural equation modeling approach, which showed that expected performance and social influence have a positive effect on the behavioral intention to use mobile payment services. In fact, the risk of confidentiality has a negative effect on this intention. A high level of facilitating conditions increased the behavioral intention to use mobile payment services for men, but not for women.

An empirical study by Kofi Penney et al. (2021) seems to confirm the findings of Kuria Waitara et al. (2015). Kofi Penney et al. (2021) used UTAUT 2 (an improved version of UTAUT) and also applied structural equation modeling. The data necessary for the study were collected through a convenience sample of 403 Ghanaians, mobile money users, in five cities: Accra, Kumasi, Takoradi, Koforidua, and Sunyani. They demonstrate that expected performance, expected effort, and social influence have a positive effect on the behavioral intention of mobile money users, whereas facilitating conditions do not have any effect on the behavioral intention of users of mobile money services. The expected performance is the main factor that affects the behavioral intention to use mobile money. The expected effort has a positive impact on both behavioral intention and expected performance. Among the new exogenous variables added to the model (hedonic motivation, habit, price value, perceived risk, trust), hedonic motivation was found to have no effect on behavioral intention. Habit impacts behavioral intention and the usage behavior of mobile money. Trust affects both expected effort, perceived risk, and behavioral intention.

Osman et al. (2020) use a sample of 375 mobile money users in Somalia, also applying a structural equation model. The essential result obtained from this research has shown that certain factors, such as performance expectancy, effort expectancy, social influence, and facilitating conditions, directly affecting the intention to use mobile money, are likely to impact it positively and significantly. Furthermore, technological resistance factors such as perceived risk of financial loss and perceived risk of systemic error have a significantly negative influence on the behavioral intention to use mobile money. These data allow for a better understanding of the technological resistance issues that were not addressed in previous studies.

Sossou et al. (2021) also experimented with the enhanced UTAUT approach to understand the explanatory factors for the acceptance and use of mobile money services by customers of mobile phone operators in Dakar (Senegal). A sample of 251 Dakar residents was constructed for this study. However, the methodological approach is different compared to the studies outlined above; because, the analysis is based here on the econometrics of qualitative variables and more specifically, on a binary logistic regression. By focusing on the essential elements (expected effort, perceived risk, service testability, perceived usefulness, social influence) that lead to the impact on behavioral intention to use and the expected usage behavior, the authors show that the intention to use is explained by perceived risk, testability, and perceived usefulness. The effect of perceived risk is negative on intention. The actual factors that explain less the intention to use are the expected effort and social influence, which is not in line with the theoretical assumptions of Venkatesh et al. (2003). Nevertheless, the expected effort has some influence on intention when convenience is taken into account. Furthermore, the intention to use and convenience have a direct and significant effect on the adoption of service innovation, while the financial cost has a futile effect on the adoption of innovation.

The quantitative study by Nur and Panggabean (2021) on a sample of 100 respondents from Jakarta and its surroundings (Indonesia) shows that perceived performance, social influences, facilitating conditions, perceived enjoyment, and trust significantly affect the behavioral intention of Generation Z to adopt mobile payment services.

From this interesting literature, which already reflects the abundance of empirical studies on the issue of using mobile money services, different works illustrate a divergence on results: the constructs that would have a favorable effect on the acceptance or resistance to mobile money technology vary from one country to another, on one hand, and would certainly be different from one continent to another, on the other hand. And, especially regarding the effect of expected effort and social influence: the results are therefore mixed. Ultimately, this research adopts as a theoretical basis for developing our theoretical hypotheses a model that extends the UTAUT by integrating perceived financial risk and perceived risk of confidentiality into the theory. Indeed, "the use of mobile money services is perceived as risky by subscribed customers" (Sossou et al., 2021: 407). Furthermore, we propose in this research to add to

the basic UTAUT framework three sociodemographic factors, namely: gender, age, and marital status of customers, which we consider as moderating variables.

The Research Proposal Defined for the Study: The factors of acceptance of technology and the factors of resistance to mobile money technology directly influence the behavioral intention to use mobile money technology. The moderating factors operate on both the behavioral intention and the usage behavior of mobile money technology. The research model we propose is illustrated in figure 1 below.

Figure 1: Research Model

The findings of this literature review, after analyzing the various factors influencing the acceptability and use of mobile money services and presenting our research model, would be incomplete if the concept of resistance were neglected. Resistance is a social practice, and as a concept, resistance to

innovation is the result of a process that incorporates perceptions, cognitions, and emotions (Bagozzi and Lee, 1999). And, more fundamentally, there are different ways users resist innovation. So, Szmigin and Foxall (1998) identify three types, namely: rejection, opposition, and postponement. Rejection happens when the innovation doesn't seem beneficial or is seen as too complicated to use. Opposition arises when consumers see a downside to the innovation. Postponement occurs when users delay adopting an innovation. Darpy's (2000) words have clearly expressed the definition of this delay: the potential user procrastinates because they consciously defer the action to a later time, waiting for the ideal moment according to their criteria, or to learn more about the innovation first. On top of that, Mani and Chouk (2016) point out that resistance to innovation can be directed against the products themselves, their market, or even the marketing hype promoting them. Resistance to innovation seems to be the appropriate theoretical framework to understand resistance behaviors towards mobile payments.

## III. RESEARCH METHODOLOGY

This study is based on Venkatesh et al.'s (2003) UTAT, which is derived from quantitative research based on surveys. As Bobillier-Chaumon (2009: 359) states: "The process of technological adoption is part of a continuum, a gradual and complex phenomenon." This helps to better explain the variations in usage behavior. Thus, in this research, we decided to experiment with a new methodological approach. In this perspective, the use or resistance to the use of mobile money is not perceived as an attribute that an individual possesses or does not possess, but rather a situation whose intensity differs from one individual to another. The following lines provide a presentation of the multidimensional measures of the degree of resistance to the use of a technology. The dimensions are constructed based on the theory being considered.

### a) Totally Fuzzy and Relative Approach to Resistance to the use of Mobile Money

The theory of fuzzy sets first appeared in Zadeh (1965) as a kind of extension of classical set theory, considering that an element can partially, but not wholly, belong to a category (Pi Alperin and Berzosa, 2011). However, non-fuzzy sets are subsets of fuzzy sets. This means that they are still fuzzy sets. "The theory of fuzzy sets opens up a vast and rich scientific domain" (Rolland-May, 1987: 43).

The basic idea, simple and effective, regarding fuzzy sets, is as follows. Given a set $\mathbf{E}$ of elements $\mathbf{x}$ $(\mathbf{x} \in \mathbf{E})$ and a fuzzy subset $\mathbf{A}$ of $\mathbf{E}$ $(\mathbf{A} \subset \mathbf{E})$ defined as follows: $\mathbf{A} = \{\mathbf{x}, \mu_{\mathbf{A}}(\mathbf{x})\}$. For every $\mathbf{x} \in \mathbf{E}$, $\mu_{\mathbf{A}}(\mathbf{x})$ is a membership function in the fuzzy subset, taking values in the closed interval [0, 1]. The value of $\mu_{\mathbf{A}}(\mathbf{x})$

represents the degree of membership of x in A. Therefore:

- $\mu_{\mathrm{A}}(\mathbf{x}) = 0$ if and only if $\mathbf{x}$ does not belong to $\mathrm{A}$;

- $0 < \mu_{\mathrm{A}}(\mathbf{x}) < 1$ if and only if $\mathbf{x}$ partially belongs to $\mathsf{A}$, and its degree of membership is given by the value of $\mu_{\mathrm{A}}(\mathbf{x})$;

- $\mu_{\mathrm{A}}(\mathbf{x}) = 1$ if and only if $\mathbf{x}$ completely belongs to $\mathsf{A}$.

It should be noted that a single idea seems to achieve consensus in all empirical studies that rely on fuzzy sets. This idea is simply that if, as a mathematical expression, the membership function is, by nature, allowed to take variable and varied forms, the only condition that such a function must fulfill is that it takes only values between 0 and 1 (Lelli, 2001).

The original proposition by Cerioli and Zani (1990), namely the Totally Fuzzy approach, was reformulated by Cheli and Lemmi (1995) who are behind the Totally Fuzzy and Relative approach (TFR). Both methods have been applied by many authors subsequently, but with a preference for the TFR approach. The latter approach enjoys our highest favor.

We consider that the theory of fuzzy sets, more specifically the TFR logic approach by Cheli and Lemmi (1995), can also be applied to the analysis of individuals' use or resistance to mobile money. It allows for the conceptualization of the adoption of mobile money services as a continuum of levels of belonging.

### b) TFR Logic and Normalized Form of the Membership Function

Given the multidimensional nature of an individual's resistance to the actual use of mobile money, it is necessary to estimate the degree of belonging of each client to the fuzzy subset of users, or resistors, based on two categories of factors: the acceptance and use of technology factors and the resistance to technology factors. As the resistance to the use of mobile money is not perceived as an attribute possessed or not by an individual, but rather as a situation whose intensity may vary from one individual to another. The estimation faces a major difficulty, that of choosing an appropriate membership function for each of the resistance indicators.

Assuming that for each statistical unit, we observe a vector $X$ of $k$ characteristics: $\mathbf{X}_1, \mathbf{X}_2, \dots, \mathbf{X}_n$. Let $\mu(\cdot)$ represent the specific membership function for the indicator $\mathbf{X}_j$ ( $\mu(\mathbf{x\_ij})$ ) illustrates a measure of the specific resistance for variable $j$ ), it is, in this context, defined in terms of its distribution function, denoted $F(\cdot)$, as follows:

1. $\mu (\mathbf{x}_{\mathrm{ij}}) = \mathbf{F}(\mathbf{x}_{\mathrm{ij}})$ when the resistance in unit j increases as $\mathbf{X_j}$ increases, and $\mu (\mathbf{x_{ij}}) = 1 - \mathbf{F}(\mathbf{x_{ij}})$ when the resistance in unit j increases as $\mathbf{X_j}$ decreases. Its normalized form, when it comes to a discrete variable, is given by:

2. $\mathbf{g}(\mathbf{x}_{\mathrm{ij}}) = 0$ if $\mathbf{x}_{\mathrm{ij}} = \mathbf{x}_{\mathrm{j}}^{1}$ and $\mathbf{g}(\mathbf{x}_{\mathrm{ij}}) = \mathbf{g}(\mathbf{x}_{\mathrm{j}}^{\mathrm{k - 1}}) + \frac{\mathbf{F}(\mathbf{x}_{\mathrm{j}}^{\mathrm{k}}) - \mathbf{F}(\mathbf{x}_{\mathrm{j}}^{\mathrm{k - 1}})}{1 - \mathbf{F}(\mathbf{x}_{\mathrm{j}}^{\mathrm{l}})}$ if $\mathbf{x}_{\mathrm{ij}} = \mathbf{x}_{\mathrm{j}}^{\mathrm{k}}$ (k > 1) This allows us to have:

3. $g(x_{ij}) = \frac{F(x_j^k) - F(x_j^1)}{1 - F(x_j^1)}\quad \forall x_{ij} = x_j^1$

In this context, $\mathbf{x}_j^1$, $\mathbf{x}_j^2$,..., $\mathbf{x}_j^m$ represent the various categories of the variables $\mathbf{X}_j$ (or the values that it assumes if $\mathbf{X}_j$ is quantitative and discrete). They are arranged in ascending order relative to the degree of resistance to the use of mobile money, such that $\mathbf{x}_j^1$ indicates the minimum degree and $\mathbf{x}_j^m$ the maximum degree of resistance. This membership function is therefore increasing with the degree of resistance. In this logic, a value of 0 for the membership function is associated with the category (or value) corresponding to the lowest degree of resistance, while a value of 1 is associated with the category corresponding to the highest degree of resistance. The values between 0 and 1, which depend on the distribution of characteristics in the population, correspond to the intermediate categories.

Concerning the dichotomous qualitative variable, it is treated as follows:

$$

\mathrm{g}\left(\mathrm{x}_{\mathrm{i j}}\right) = \left\{ \begin{array}{l l} 0 & \text{if the individual shows no resistance} \\ 1 & \text{if the individual shows resistance} \end{array} \tag{3'}

$$

This variable has a binary output; thus, it is a variable derived from a non-fuzzy set. Regarding the continuous quantitative variables, many contributions use a modified membership function which is a combination of the membership function from Cheli and Lemmi (1995) and that of Betti and Vema (1999). It is given by the following algebraic expression:

$$

\mathrm {g} \left(\mathrm {x} _ {\mathrm {i j}}\right) = \left[ 1 - \mathrm {F} \left(\mathrm {x} _ {\mathrm {i j}}\right) \right] \left[ 1 - \mathrm {L} \left(\mathrm {x} _ {\mathrm {i j}}\right) \right] \quad (3 ^ {\prime \prime})

$$

where $F(\cdot)$ is the distribution function of the variable in question, $L(\cdot)$ corresponds to the ordinate of the Lorenz curve. This measure is more sensitive than the simple cumulative distribution function when the dimension displays real and significant disparities. The conceptualization of this methodological approach on resistance to the use of mobile money allows for the definition of two broad interpretations: when it pertains to the individual, in this case, it is applicable to an individual index of multiple resistance; when it pertains to the reference population, in this case, it is applicable to a general index of resistance that is calculated.

The TFR indices result from a multidimensional approach to measuring resistance to the use of a new technology; the different aspects of this phenomenon can be studied either individually or aggregated together and measured by a single index. And once the $k$ values of the membership function $\mathbf{g}_1(\mathbf{x}_{i1}),\dots,\mathbf{g}_k(\mathbf{x}_{ik})$ related to the $k$ resistance indicators corresponding to the i-th individual are calculated, we need to find a way to aggregate them to obtain a new membership function that considers all the information provided jointly by the $k$ indicators.

Such a global membership function can be defined as a weighted average of the values of the specific membership functions. The i-th unit of the membership function in the fuzzy subset of the resistors can be defined as follows:

$$

f\left(x_{i}\right) = f\left(x_{i1}, \dots , x_{ik}\right) = \frac{\sum_{j} w_{j} \cdot g\left(x_{ij}\right)}{\sum_{j} w_{j}} \quad i = 1, \dots , n \tag{4}

$$

and $j = 1,\ldots,m(i$ indicates each individual and indicates each dimension).

In this expression:

- $f(x_{i})$ represents an individual index of multiple resistance, based on the set of variables obtained from a questionnaire;

- les $\mathbf{w}_1, \mathbf{w}_2, \dots, \mathbf{w}_m$ describe a generic system of averages:

$$

w_{j} = w(P_{j}) = w\left[\frac{1}{n}\sum_{i} g(x_{ij})\right]

$$

The determination of the weights $(w_{j})$ in formula 5 is a practical problem of concern that calls for several ad hoc solutions in the literature. For this study, we adopt the following formulation:

$$

w _ {j} = e ^ {- P _ {j}} \tag {6}

$$

It should be noted that, depending on the approach chosen for this problem, there are many mathematical formulations of the weight function. The existing literature presents a large number of possible alternatives for the weight function, which are consistent with the principle of TFR logic. The general index of the multiple resistance under analysis is obtained. It is given by the following mathematical expression: It should be noted that, depending on the approach taken to this problem, there are many mathematical formulations of the weight function. The existing literature presents a large number of possible alternatives for the weight function, which are consistent with the principle of TFR logic.

$$

P = \frac{1}{n} \sum_{i} f(x_{i}) = \frac{1 }{n} \sum_{i} \left[ \frac{\sum_{j} w_{j} \cdot g(x_{ij})}{\sum_{j} w_{j}} \right] = \frac{\sum_{j} w_{j} \cdot \left[ \frac{1}{n} \sum_{i} g_{j}(x_{ij}) \right]}{\sum_{j} w_{j}} \tag{7}

$$

The P index can be calculated either for all resistance indicators or for specific groups of indicators:

thematic index (for example, only the fuzzy subset of risk barriers). In the first case, a general measure of resistance is obtained, while in the second case, a collective measure for a specific type of resistance is obtained.

## IV. EMPIRICAL ANALYSIS: DATA COLLECTION METHODOLOGY AND RESULTS OF FUZZY LOGIC

### a) Data Collection Methodology

To address our issue, a quantitative study was conducted among a convenience sample of Airtel Congo customers in the Brazzaville department. Indeed, an empirical study was conducted with 420 Airtel Congo customers, aged 18 and older. To collect the data, we chose the questionnaire as a collection tool.

Inspired by previous empirical researches on the use or rejection of mobile money and in accordance with the theoretical consensus associated with the UTAUT model, the questionnaire used consisted of three main parts. First, Part A) 'To better know you' allowed for the characterization of the individual (gender, age, marital status, level of education, annual income in CFA francs, occupation). Next, Part B) 'Motivational factors in the use of Airtel mobile money transfer services,' which focused on functional barriers, aimed to understand the role played in the acceptance of mobile money transfer services by certain factors identified in the literature related to UTAUT (testability, ease of use, convenience of the service, social influence, perceived usefulness of the services, low cost of services). Finally, section C) "Factors of resistance in the use of Airtel mobile money services" focused on structural barriers, emphasizing risk factors (financial risk, confidentiality risk).

With a simple constitution, but very operational and technically better suited to the specific context of the study, the non-probabilistic convenience sampling method was applied. Within the framework of this sampling methodology, statistical units are chosen, based on their convenience and availability and for practical reasons of accessibility (the opportunities that arise for the researcher without a predetermined selection criterion). This short survey was conducted from July to early August 2022.

Depending on the objective of the study, the sample structure we produce here is limited solely to the moderating factors (sex, age, and marital status). Table 1, which follows, presents this predefined sample structure according to the conceptual reflection.

Table 1: Distribution of Respondents by Sex, Age, and Marital Status

<table><tr><td>Moderating variables</td><td>Types of Variables</td></tr><tr><td rowspan="2">Sex</td><td>Women = 30%</td></tr><tr><td>Men = 70%</td></tr><tr><td rowspan="3">Age</td><td>[18 – 40 years] = 65%</td></tr><tr><td>[41 – 60 years] = 28%</td></tr><tr><td>61 years and older = 7%</td></tr><tr><td rowspan="4">Marital status</td><td>Single = 77%</td></tr><tr><td>Married = 20%</td></tr><tr><td>Separated = 3%</td></tr><tr><td>Widow/Widower = 0%</td></tr></table>

Table 1 above shows that our sample consists of $30\%$ women and $70\%$ men. The over-representation of the male sex is due to random fluctuations. Among all respondents, $65\%$ of the study subjects are between 18 and 40 years old, $28\%$ are between 41 and 60 years old, and $7\%$ are over 60 years old. Regarding marital status, the survey results indicate that $77\%$ are single, $20\%$ are married, and $3\%$ are separated or divorced.

### b) Measures

Degrees of resistance, according to the different fuzzy indices, were estimated in this study, with data obtained from the survey conducted in the department of Brazzaville, among Airtel Congo customers, and a synthesis of these measures was made.

## i. Selection of Fuzzy Dimensions

In total, we have retained four collections and fourteen fuzzy subsets. These collections and fuzzy subsets are illustrated in the table below.

Table 2: Selected Fuzzy Sets and Subsets

<table><tr><td>Fuzzy sets (Attributes)</td><td>Fuzzy subsets (Components)</td><td>Types of variables</td><td>Conditions of resistance</td></tr><tr><td rowspan="6">SUBjective Assessments</td><td>Pre-test before adoption</td><td>Binary 0/1</td><td>Yes = 1</td></tr><tr><td>Ease of use</td><td>Binary 0/1</td><td>Yes = 1</td></tr><tr><td>Convenience of the service</td><td>Binary 0/1</td><td>Yes = 1</td></tr><tr><td>Social influence</td><td>Binary 0/1</td><td>Yes = 1</td></tr><tr><td>Perceived usefulness</td><td>Binary 0/1</td><td>Yes = 1</td></tr><tr><td>Cost of services</td><td>Binary 0/1</td><td>Yes = 1</td></tr><tr><td rowspan="3">Facilitation Conditions</td><td>Income</td><td>Numeric</td><td>≥75000</td></tr><tr><td>Level of education</td><td>Polytomic</td><td></td></tr><tr><td>Status</td><td>Polytomic</td><td></td></tr><tr><td rowspan="2">Perceived Risks</td><td>Financial risk</td><td>Binary 0/1</td><td>Yes = 1</td></tr><tr><td>Risk of confidentiality</td><td>Binary 0/1</td><td>Yes = 1</td></tr><tr><td rowspan="3">Moderating Factors</td><td>Sex</td><td>Binary 0/1</td><td>Yes = 1</td></tr><tr><td>Age</td><td>Polytomic</td><td></td></tr><tr><td>Marital status</td><td>Polytomic</td><td></td></tr></table>

To globally measure the reliability of our measurement instrument, that is, the level of homogeneity of a block of positively correlated variables $\mathbf{x}_{\mathrm{i}}$, we use Cronbach's Alpha. The table 3 below shows the number of fuzzy sets by indicators as well as the value of $\alpha$ of Cronbach. Since our research is only exploratory, a block is considered homogeneous if: $\alpha \geq 0.6$. The obtained Cronbach's coefficients allow us to say that, for each indicator, the variables (fuzzy subsets) selected assess the same reality.

Table 3: Results of Cronbach's $\alpha$ Coefficient

<table><tr><td>Fuzzy sets</td><td>Number of fuzzy subsets</td><td>Coefficient α</td></tr><tr><td>Subjective evaluations</td><td>6</td><td>0.633</td></tr><tr><td>Facilitation factors</td><td>3</td><td>0.970</td></tr><tr><td>Perceived risks</td><td>2</td><td>0.989</td></tr><tr><td>Moderating factors</td><td>3</td><td>0.890</td></tr></table>

## ii. Calculation of Resistance Indices According to Totally Fuzzy and Relative Logic

We have defined the weights of the fixed fuzzy dimensions, each of these dimensions revealing an aspect of the resistance to the use of Airtel Congo's mobile money. Table 4 summarizes the results obtained from the weight calculation.

Table 4: Weights associated with fuzzy dimensions

<table><tr><td>Attributes</td><td>Fuzzy Dimensions</td><td>Weight P</td><td>Fonctiong(xij)</td></tr><tr><td rowspan="6">Subjective Assessments</td><td>Pre-test before adoption</td><td>0.462</td><td>0.771</td></tr><tr><td>Ease of use</td><td>0.417</td><td>0.874</td></tr><tr><td>Convenience of the service</td><td>0.447</td><td>0.805</td></tr><tr><td>Social influence</td><td>0.561</td><td>0.579</td></tr><tr><td>Perceived usefulness</td><td>0.545</td><td>0.607</td></tr><tr><td>Cost of services</td><td>0.480</td><td>0.733</td></tr><tr><td rowspan="3">Facilitation Conditions</td><td>Income</td><td>0.793</td><td>0.231</td></tr><tr><td>Level of education</td><td>0.775</td><td>0.255</td></tr><tr><td>Status</td><td>0.395</td><td>0.930</td></tr><tr><td rowspan="2">Perceived Risks</td><td>Financial risk</td><td>0.645</td><td>0.438</td></tr><tr><td>Risk of confidentiality</td><td>0.746</td><td>0.293</td></tr><tr><td rowspan="3">Moderating Factors</td><td>Sex</td><td>0.497</td><td>0.770</td></tr><tr><td>Age</td><td>0.748</td><td>0.291</td></tr><tr><td>Marital status</td><td>0.442</td><td>0.817</td></tr></table>

The indicators are of a dichotomic, polytomic, and continuous type (see Table 2), and the membership function takes the form given by equation 2. The different values of $\mathbf{x}_j^1$ indicating the minimum degree and $\mathbf{x}_j^m$ the maximum degree are established in such a way as to fully take into account the characteristics of each indicator. The results are recorded in Table 4. If the fact or the status of having no level of education is seen as an indicator of resistance to the use of mobile money, the minimum value is 0.255. If the fact that not doing the pretest before adopting mobile money is seen as an indicator of resistance to the use of mobile money, the average degree of membership in the fuzzy set of resistant is 0.771 (minimum value). The average degree of membership in the fuzzy set of resistant is 0.874 if usability issues (ease of use) are identified as a factor reinforcing users' resistance. The minimum value is 0.579 if resisting social influence (fashion effect only) increases users' resistance. However, it is important to emphasize the need for caution in interpreting these results, particularly when the values of $\mathbf{g}(\mathbf{x}_{\mathrm{ij}})$ for the different types of selected variables are measured and compared: indeed, $\mathbf{g}(\mathbf{x}_{\mathrm{ij}})$ is a proportion in the case where the variables involved are binary, which is not necessarily true in the case of continuous variables.

Social influence, although slightly less dominant than other subjective variables, remains a significant factor explaining the resistance among the individuals surveyed. It is highlighted by the UTAUT model of Venkatesh et al. (2003). A comparison of our results with those of previous studies, such as those by Nur and Panggabean (2021) and Lee et al. (2019), supports the assertion that the opinions of colleagues, friends, and close ones play a key role in the resistance to the use of technology.

It appears that the individual's age is the moderating factor that would play a more reducing role on the resistance of customers to use mobile money services.

By construction, all resistance indices are values between 0 and 1. The closer the index is to 1, the higher the degree of resistance to the use of mobile money. Each of the two specific indicators and the general index have been divided into ordered classes in increasing order of resistance. An arbitrary division of the scale into quartiles has been made to clarify the analysis and establish the consistency of the results with the retained categories of resistance groups to the use of technology. In this sense, concerning the considered indicator, the class of [0.00 - 0.25 [corresponds to individuals with a low degree of resistance to the use of mobile money (the less resistant individuals), while the class of [0.75 - 1.00] groups all individuals exhibiting a high degree of resistance to the use of mobile money (the extremely resistant individuals). The classes of [0.25 - 0.50] and [0.50 - 0.75] are intermediate classes and take into account: individuals who are moderately resistant and those who are resistant, respectively.

The idiosyncratic, thematic, and general indices of resistance have been calculated.

Table 5: Idiosyncratic, Thematic, and General Indices

<table><tr><td>Attributes</td><td>Fuzzy Dimensions</td><td>Indicators</td></tr><tr><td rowspan="4">Idiosyncratic Indices</td><td>Subjective assessments</td><td>0.657</td></tr><tr><td>Facilitating factors</td><td>0.380</td></tr><tr><td>Perceived risks</td><td>0.389</td></tr><tr><td>Moderating factors</td><td>0.549</td></tr><tr><td>Thematic Indices</td><td>Subj. Assess. -Fac. fac.</td><td>0.518</td></tr><tr><td rowspan="2">General Indice</td><td>General resistance index without considering moderating factors</td><td>0.475</td></tr><tr><td>General resistance index after considering moderating factors</td><td>0.494</td></tr></table>

Source: author of the article

The measured value of the fuzzy index of subjective assessments seems to be around 0.657, or $65.7\%$, and is the highest among the selected idiosyncratic indices. While the fuzzy index of resistance due to perceived risks is estimated at 0.390 (39.0%), the fuzzy index of resistance due to facilitation conditions is the lowest at only 0.380 (38.0%). The fuzzy index of resistance due to moderating factors is 0.550 (55.0%). The critical aspects of using mobile money technology are related to subjective assessments.

To see to what extent key factors - age, gender, and marital status - affect the degree of resistance to the use of mobile money technology in the specific context of Congo, one can compare the general fuzzy multidimensional index obtained without considering moderating factors with the general fuzzy multidimensional index obtained with consideration of moderating factors. Regarding the general fuzzy multidimensional index obtained without considering moderating factors, the results indicate that the degree of resistance to the use of mobile money among Airtel Congo customers in the Brazzaville department is 0.475. In other words, $47.5\%$ of the surveyed customers are moderately resistant (moderate resistance). And regarding the estimated fuzzy multidimensional general index, after taking into account the moderating factors, it is 0.494: $49.4\%$ have moderate resistance. The estimated value of the fuzzy general index is slightly increased by about 1.9 percentage points when considering the dimension of moderating factors. The degree of resistance rooted in the moderating factors is largely caused by the individual's gender and marital status.

Tables 6-12 provide information on the distribution by resistance class and, for each attribute, according to the studied indicator.

Table 6: Subjective Assessments

<table><tr><td>Subj assess.</td><td>Abs. Freq.</td><td>Rel. Freq.</td><td>Cum. Rel. Freq.</td></tr><tr><td>[0.00 - 0.25]</td><td>11</td><td>2.6</td><td>2.6</td></tr><tr><td>[0.25 - 0.50]</td><td>66</td><td>15.7</td><td>18.3</td></tr><tr><td>[0.50 - 0.75]</td><td>223</td><td>53.1</td><td>71.4</td></tr><tr><td>[0.75 - 100]</td><td>120</td><td>28.6</td><td>100.0</td></tr><tr><td>Total</td><td>420</td><td>100</td><td></td></tr></table>

Note well: Abs. Freq.: absolute frequencies; Rel. Freq.: relative frequencies; Cum. Rel. Freq.: cumulative relative frequencies

<table><tr><td>Fac. Fac.</td><td>Abs. Freq.</td><td>Rel. Freq.</td><td>Cum. Rel. Freq.</td></tr><tr><td>[0.00 - 0.25]</td><td>132</td><td>31.4</td><td>31.4</td></tr><tr><td>[0.25 - 0.50]</td><td>192</td><td>45.7</td><td>77.1</td></tr><tr><td>[0.50 - 0.75]</td><td>67</td><td>16.0</td><td>93.1</td></tr><tr><td>[0.75 - 1.00]</td><td>29</td><td>6.9</td><td>100.0</td></tr><tr><td>Total</td><td>420</td><td>100</td><td></td></tr></table>

<table><tr><td>Ris. Per.</td><td>Abs. Freq.</td><td>Rel. Freq.</td><td>Cum. Rel. Freq.</td></tr><tr><td>[0.00 - 0.25[</td><td>187</td><td>44.5</td><td>44.5</td></tr><tr><td>[0.25 - 0.50[</td><td>49</td><td>11.7</td><td>56.2</td></tr><tr><td>[0.50 - 0.75[</td><td>110</td><td>26.2</td><td>82.4</td></tr><tr><td>[0.75 - 1.00]</td><td>74</td><td>17.6</td><td>100.0</td></tr><tr><td>Total</td><td>420</td><td>100</td><td></td></tr></table>

<table><tr><td>Fac. Mod.</td><td>Abs. Freq.</td><td>Rel. Freq.</td><td>Cum. Rel. Freq.</td></tr><tr><td>[0.00 - 0.25]</td><td>75</td><td>17.9</td><td>17.9</td></tr><tr><td>[0.25 - 0.50]</td><td>165</td><td>39.3</td><td>57.1</td></tr><tr><td>[0.50 - 0.75]</td><td>80</td><td>19.0</td><td>76.2</td></tr><tr><td>[0.75 - 1.00]</td><td>100</td><td>23.8</td><td>100.0</td></tr><tr><td>Total</td><td>420</td><td>100</td><td></td></tr></table>

<table><tr><td>AS-FF.</td><td>Abs. Freq.</td><td>Rel. Freq.</td><td>Cum. Rel. Freq.</td></tr><tr><td>[0.00 - 0.25]</td><td>11</td><td>2.6</td><td>2.6</td></tr><tr><td>[0.25 - 0.50]</td><td>207</td><td>49.3</td><td>51.9</td></tr><tr><td>[0.50 - 0.75]</td><td>178</td><td>42.4</td><td>94.3</td></tr><tr><td>[0.75 - 1.00]</td><td>24</td><td>5.7</td><td>100.0</td></tr><tr><td>Total</td><td>420</td><td>100</td><td></td></tr></table>

<table><tr><td>Gen. Ind.</td><td>Abs. Freq.</td><td>Rel. Freq.</td><td>Cum. Rel. Freq.</td></tr><tr><td>[0.00 - 0.25]</td><td>10</td><td>2.4</td><td>2.4</td></tr><tr><td>[0.25 - 0.50]</td><td>250</td><td>59.5</td><td>61.9</td></tr><tr><td>[0.50 - 0.75]</td><td>140</td><td>33.3</td><td>95.2</td></tr><tr><td>[0.75 - 1.00]</td><td>20</td><td>4.8</td><td>100.0</td></tr><tr><td>Total</td><td>420</td><td>100</td><td></td></tr></table>

<table><tr><td>Gén. Ind.</td><td>Abs. Freq.</td><td>Rel. Freq.</td><td>Cum. Rel. Freq.</td></tr><tr><td>[0.00 - 0.25]</td><td>7</td><td>1.7</td><td>1.7</td></tr><tr><td>[0.25 - 0.50]</td><td>225</td><td>53.6</td><td>55.3</td></tr><tr><td>[0.50 - 0.75]</td><td>177</td><td>42.1</td><td>97.4</td></tr><tr><td>[0.75 - 1.00]</td><td>11</td><td>2.6</td><td>100.0</td></tr><tr><td>Total</td><td>420</td><td>100</td><td></td></tr></table>

The analysis of the distribution of users of mobile money services along the resistance continuum, represented by the general resistance index (not taking into account moderating factors), shows a concentration in the categories between 0.75 and 1.00, while the highest frequency is in the class of [0.25 - 0.50[(59.5% of respondents). It should be noted that 20 individuals, who exhibit extreme resistance, fall into the class of [0.75 - 1.00].

Regarding the general resistance index (taking into account moderating factors), it does show a concentration in the categories between 0.75 and 1.00. However, only 11 individuals end up in the class of [0.75 - 1.00], and the highest frequency, which is still in the class of [0.25 - 0.50[, has decreased (53.6% of respondents), representing a gap of about 6 percentage points. From an empirical perspective, the moderating factors that influence both behavioral intuition and actual behavior in using mobile money technology completely and automatically blur the boundaries of all resistance classes to mobile money services that we have established conceptually.

## V. CONCLUSION

The objective of this work was to understand the impact of moderating factors such as age, gender, and marital status on resistance to mobile money technology in the specific context of Congo. To achieve this goal, a survey was conducted among Airtel Congo customers in the Brazzaville department, and a total of 420 completed questionnaires were collected.

After outlining the theoretical foundations on which we built our research model based on the UTAUT, aimed at describing individual intention and usage behavior of mobile services, the article develops and validates an 'exploratory' empirical approach whose purpose is to highlight the interest of a multidimensional and fuzzy indicator of resistance to the use of mobile money. The main contribution of this work is not merely to refer precisely to the revised UTAUT model which combines insights from several technology acceptance theories, but rather to establish a gradation in the use or resistance to the use of mobile money. Fuzzy set theory, particularly TFR logic, has allowed us to qualify the extent of this gradation, with satisfactory results.

We compared the fuzzy multidimensional general index, obtained without considering the moderating factors, with the one obtained considering the moderating factors, which have a simultaneous effect on behavioral intuition and the behavior of using mobile money technology. The general index, detached from the moderating factors, is estimated at 0.475, meaning that $47.5\%$ of Airtel Congo customers surveyed in the Brazzaville department are moderately resistant to mobile money services. In fact, the gap in the index, calculated by considering the moderating factors, is about 1.9 percentage points compared to the general index extracted from the moderating factors. The moderating factors have blurred the boundaries of the resistance categories to mobile money services that we conceptually established.

The results of this study could indeed provide relevant information for the design of business strategies that, relying on a better understanding of subjective assessments (the ease and convenience of the service, the cost of the service), facilitating conditions (customer status), and moderating factors (gender and marital status), would take into account multiple levels of observation to apply the necessary actions and methods accordingly, in a manner more appropriate to customers.

Beyond the methodological contribution which seems important, the field or the scope of the analysis is original. However, it is worth highlighting some limitations, in line with this exploratory study: this research should continue by expanding the sample size, integrating other mobile money transfer service operators and other dimensions of resistance, and building appropriate level-headed systems. Finally, while we note that the theory of fuzzy sets and the structure of the proposed TFR logic provide empirical analysis of resistance to mobile money with the hope of considering graduations, econometric modeling may allow explaining the intensity of resistance through a set of individual characteristics.

As a final conclusion, it is essential to recognize that our research is not without limitations. Indeed, it does not take into account mobile money transactions categorized by major product types (money transfers, cash withdrawals, mobile top-ups, payments, etc.). Furthermore, it was limited to a single mobile operator and one department. It would be better to conduct the study on all operators and throughout the entire territory of Congo, which would allow for a comprehensive analysis of the results.

### Webography

Generating HTML Viewer...

References

92 Cites in Article

Icek Ajzen (1991). The theory of planned behavior.

Icek Ajzen (1985). From Intentions to Actions: A Theory of Planned Behavior.

I Ajzen,M Fishbein (1980). Understanding Attitudes and Predicting Social Behavior.

Richard Bagozzi (1982). A Field Investigation of Causal Relations among Cognitions, Affect, Intentions, and Behavior.

R Bagozzi,K.-H Lee (1999). Consumer Resistance to, and acceptance of Innovations.

S Baile (2005). L'approche comportementale de l'évaluation des systèmes d'information: théories et taxonomie des modèles de recherche.

A Bakri,Darwis,A Wandanaya,V Violin,T Fauzan (2023). The Application of UTAUT Modified Model to Analyze the Customers Use Behavior of Shopee Paylater.

A Bandura (1986). The Explanatory and Predictive Scope of Self-Efficacy Theory.

A Bandura (1977). Self-Efficacy: Toward a Unifying Theory of Behavioral Change.

Anol Bhattacherjee (2001). Understanding Information Systems Continuance: An Expectation-Confirmation Model1.

A Bennaceur (2019). Aperçu sur les fondements théoriques liés à l'explication de l'adoption des nouvelles technologies sur la base du modèle TAM.

Gianni Betti,Francesca Gagliardi,Vijay Verma (1999). JRR Variance Estimates for Longitudinal Fuzzy Measures of Multi-Dimensional Poverty.

Honoré Bidiasse,Gregory Mvogo (2019). Les déterminants de l’adoption du mobile money : l’importance des facteurs spécifiques au Cameroun.

M Bobillier-Chaumon,M Dubois (2009). L'adoption des technologies en situation professionnelle: quelles articulations possibles entre acceptabilité et acceptation ?.

Isabelle Bourdon,Sandrine Hollet-Haudebert (2009). Pourquoi contribuer à des bases de connaissances ? Une exploration des facteurs explicatifs à la lumière du modèle UTAUT.

É Brangier,S Hammes-Adelé,J Bastien (2010). Analyse critique des approches de l’acceptation des technologies : de l’utilisabilité à la symbiose humain-technologie-organisation.

Andrea Cerioli,Sergio Zani (1990). A Fuzzy Approach To The Measurement Of Poverty.

B Cheli,A Lemmi (1995). A « Totally » Fuzzy and Relative Approach to the Multidimensional Analysis of Poverty.