I. INTRODUCTION

Over the past few years, the world economy has been declining, and the recession has caused inflation, unemployment, and a decline in financial well-being. The decline in financial well-being has harmful effects on mental and physical health. It creates problems of stress, anxiety, depression, and suicide in our society (Taft et al., 2013). Financial literacy has become a much-discussed topic in recent years for the financial empowerment of people and their lives. It catches the attention of a common person who is willing to meet their daily financial needs and plan for a secure future. Financial literacy strengthens people's ability to access financial services, manage their budgets, and maximise resource utilization, which encourages economic development. Financial literacy increases people's confidence and self-control, which encourages their participation in the formal economic system. It will boost your confidence and well-being. As the literature shows, almost all countries in the world are dealing with the issue of financial literacy. But the concept of financial literacy is not yet clear. Different researchers use different definitions of financial literacy. Financial literacy is defined by the OECD (OECD, 2017) as "a combination of understanding, expertise, ability, attitude, and action required to make sound financial decisions and eventually achieve individual well-being". "Financial literacy is the ability to make sound decisions and appropriate choices regarding the use and management of capital" (Huston, 2010)." Financially literate people make good choices about their finances and reduce their risk of being deceived on financial issues" (Beal &Delpachitra, 2003). Financial literacy is affected by the level of education and income of an individual (Nahar et al., 2022) in previous work on financial literacy, researchers used various aspects of financial literacy. Few scholars have used financial literacy and financial knowledge as the same term, while others find financial knowledge is associated with financial literacy and has a high correlation. The OECD has given a detailed view of financial literacy. According to the OECD (2011), "financial literacy is a blend of financial behaviour, financial attitude, and financial awareness," but in this study, researchers added one more determinant to financial literacy, so it is therefore important to gain insight into the association between "financial knowledge, financial attitude, financial behaviour and financial socialisation with financial wellbeing" among the younger generation related to the financial aspects.

II. LITERATURE REVIEW

Financial literacy has been researched in a number of ways. Government bodies, private organisations, and individuals have undertaken studies in various countries to check the level of financial literacy in their countries. Lusardi and Mitchell (2014) "People's willingness to process financial information and make a rational financial saving, capital accumulation, debt, and pension decisions." Atkinson and Messy (2012) "A combination of awareness, knowledge, skill, attitude and behaviour necessary to make sound financial decisions and ultimately achieve individual financial wellbeing". Huston (2010) "Financial literacy has introduced an implementation layer enabling individuals to have the capacity and trust to use financial skills to make financial choices". The notion of financial literacy is still being debated. In the present literature, financial literacy has numerous interpretations since financial literacy authorities have given researchers and authors the freedom to express and assess financial literacy (Remund, 2010). "Financial literacy, financial behaviour, and financial awareness should be seen interchangeably" by ("Hassan Al-Tamimi and Anood Bin Kalli, 2009, Howlett, Kees and Kemp, 2008, Yoong, See and Baronovich, 2012"). Most of the research used an objective evaluation method to assess individual financial literacy. Various researchers used objective tests used in different ways in which they assess the financial literacy of the individual. Bhushan and Medury (2014) measure financial literacy by giving objective questions related to "income, savings, investment, budget management, and credit management". Fessler, et al. (2020), takes "Time Value of Money, Risk and Return, Interest, Diversification, and Inflation" to test financial literacy. Previous study results show low levels of financial literacy among the low-income group, females, students, less educated, lower-income group and minorities ("Hassan Al-Tamimi & Anood Bin Kalli, 2009, Grohmann, 2018, (NISM, 2014), Fernandes et al., 2014"). Thakur & Mago (2021) found that financial knowledge, financial attitude, and financial well-being have a significant positive relationship with financial literacy. In reviewing the literature, it can be said that, in most research on the assessment of literacy among the population, researchers consider only one dimension of financial literacy, i.e., financial knowledge, and other aspects, such as financial attitudes and financial behaviour, have been considered only in a few studies. The concept of financial literacy is different from person to person. In India, governments, the Reserve Bank of India, NGOs, and financial institutions are taking numerous steps to increase awareness. To increase financial literacy, FLCs (financial literacy centres) are playing a very important role in creating awareness. Financial literacy centres organise camps on a regular basis in rural Haryana to spread awareness among women, children, farmers, low-income groups, etc.

III. FINANCIAL LITERACY DETERMINANTS

a) Financial Knowledge

A person with a basic understanding of financial concepts and financial products is considered to be financially literate. One of the most important factors in financial literacy is financial knowledge, as per the OECD. Huston (2010) provides a definition for this term. Authors have identified four critical elements of financial literacy after evaluating more than 71 studies. All aspects of money, including saving, investing, and borrowing, are explored. One of the five financial concepts included by the OECD is the notion of the time value of money, which explains how inflation affects investments and prices. According to Gerrans and Heaney (2019), financial literacy has an impact on both financial behaviour and financial well-being in the long run. It has been hypothesised that knowledge of personal finance, saving, loans, investment, and insurance are all indicators of financial literacy and have an association with financial behaviour.

b) Financial attitude

Generally speaking, a financial attitude is described as a personal tilt toward financial products, which can only be achieved when people have a favourable attitude toward the financial product and help to build a positive attitude toward the financial product. Financial literacy is critical in today's society. Chijwani (2014) concluded that in order to achieve strong financial literacy, emphasis should be placed on establishing favourable financial attitudes among the people of this country. Only then will any financial education programme be able to give meaningful benefits to its participants. Ajzen (2011) has demonstrated that decision-makers actions have an impact on their financial attitudes and that their perceptions of the economy and non-economic factors will enhance their opinions. Ibrahim and Alqaydi (2013) came to the conclusion in their study that financial education can help people modify their personal financial views and minimise their reliance on credit cards even further. According to Yuesti, Rustiarini and Suryandari (2020), addition, financial attitudes and financial behaviour variables have been shown to have a favourable impact on financial literacy and financial wellbeing. Financial attitudes, in addition to financial behaviour, can have an impact on one's financial wellbeing. Research by Ibrahim and Alqaydi (2013) discovered that those who had a good financial attitude borrowed less money from banks and credit cards. According to Sohn et al. (2012), the "financial socialisation agent, financial attitude, and financial literacy, all have a favourable impact on financial literacy levels." Ultimately, Haque, Abdul; Zulfiqar (2016) came to the conclusion that a "positive financial attitude and financial literacy are beneficial to women's financial wellbeing and empowerment".

c) Financial behaviour

People's actual financial decisions in the financial market are referred to as "financial behaviour," and they are linked to their levels of savings, debt, and expenditure. Research by Atkinson and Messy (2011) discovered that realistic financial attitudes, such as effective budget preparation and financial stability, help people improve their financial literacy. Conversely, people with negative financial attitudes, such as reliance on loans and credit, have a negative impact on their finances. Financial literacy and financial attitude can lead to positive financial behaviour, according to Taft et al. (2013), who concluded that "it is necessary to consider the impact of financial literacy on financial behaviour. According to the findings of this study, "financial literacy aids in the modification of behaviour and the improvement of decision-making abilities as well as the improvement of living standards". According to Morgan and Trinh (2017), "financial behaviour is extremely important and is a key component of financial literacy". According to Mokhtar & Rahim (2016), "the work environment, financial stress, locus of control, and financial behaviour are all strongly associated with financial well-being." They discovered that these factors are all strongly associated with financial well-being. Aside from that, financial stress was found to be the most significant factor influencing financial well-being, followed by the workplace environment.

d) Financial Socialisation

The acquisition of values, attitudes, standards, norms, knowledge, and behaviour makes up financial socialisation (Gudmunson and Danes 2011) Significant financial socialisation concepts include earning, spending, saving, borrowing, and sharing (Lanz, Sorgente, and Danes 2020). Socialization is a crucial aspect of decision-making. A socialised individual can make rationing decisions following discussion. The majority of children's financial knowledge, skills, and attitudes are formed by their parents and guardians (Danes, 1994). Numerous studies have established a link between parental influence and monetary values, attitudes, behaviours, and abilities.

IV. FINANCIAL WELL-BEING CONCEPT

In general, the concept of well-being is subjective. Numerous variables are considered when assessing the well-being of society. Physical health and wellness are not the only aspects of well-being, contrary to popular belief. (Kruger, 2011) defines five elements of well-being. The first is career well-being; individuals with high career well-being are more successful and happier than those without a career. Social well-being, social capital, and socialisation are also vital components of an individual's well-being. People whose relationships with friends, family, and co-workers are stronger are more socially well-adjusted. Gao, X at, el. (2022) Income and financial worries impact parents' mental health differently. Future policy or intervention programmes should target parental financial worries. They experience a reduction in stress after discussing the issue with their social groups. It is a well-known adage that a sound mind resides within a healthy body. A person with a healthy body is always able to combat problems and lower their stress levels. Regular exercise reduces stress and promotes happiness in life. People with good physical health are more sociable and make sound decisions regarding their career health. Individuals' wellbeing is also affected by the community in which they reside. Community well-being includes air and water quality, as well as safety and proximity. If a person lives in a peaceful environment, they can think significantly better than if they lived in a hostile environment. Financial well-being refers not only to the amount of money a person has or spends on his or her own needs, but also to spending on others, buying goods with the future in mind, and feeling secure. A person who is financially secure can take calculated risks for the future. Financial well-being relates to all other aspects of well-being, including career well-being, physical wellbeing, social well-being, and community well-being (CFPS, 2017). The quality of a person's life is significantly impacted by their financial situation. Financial security is the ultimate and most common financial objective of an individual. However, there is no standard definition of financial prosperity.

V. RESEARCH PROBLEM STATEMENT

The main goal of this study is to find out what makes people in Ambala Division, Haryana, financially literate and happy.

To comprehend a research problem, it is necessary to investigate a small number of research questions in order to acquire the pertinent information and answers to these questions.

VI. RESEARCH QUESTIONS

This study's purpose is to examine the given research problem.

- "What are the determinants of financial literacy and what are its effects on financial well-being among the younger generation in Haryana, India?"

- Does financial socialisation have a significant effect on financial well-being?

VII. RESEARCH OBJECTIVE

- To identify the determinates of financial literacy and examine the determinants that contribute more to financial literacy and financial well-being,

- To examine the effect of financial literacy on financial well-being after adding new determinants (financial socialisation) to financial literacy.

VIII. RESEARCH HYPOTHESIS

H1: There is a significant relationship between determinants of financial literacy and financial well-being in Haryana.

- H1.1 There is a significant relationship between financial knowledge and financial well-being.

- H1.2 There is a significant relationship between financial attitude and financial well-being.

- H1.3 There is a significant relationship between financial behaviour and financial well-being.

- H1.4 There is a significant relationship between financial socialisation and financial well-being.

IX. FINANCIAL LITERACY FRAMEWORK

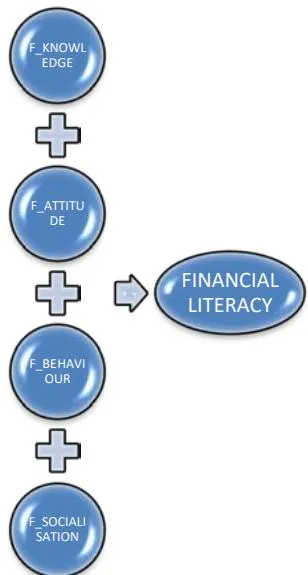

The OECD developed the financial literacy framework by using financial knowledge, financial attitude, and financial behaviour. However, as illustrated in figure 1, financial socialisation has been added to the existing financial literacy framework.

Source: based on reviews of literature, a research framework developed by the authors.

X. RESEARCH METHODOLOGY

a) Sample Size and Sampling Technique

The demographic area of interest in this study was the Ambala district of Haryana. Three professors from different disciplines at Sharda University in Greater Noida, India, approved a self-administered questionnaire. Data were collected both online and offline. Due to time constraints, only 117 people were chosen for this study. This research employed probability sampling.

b) Instrumentation

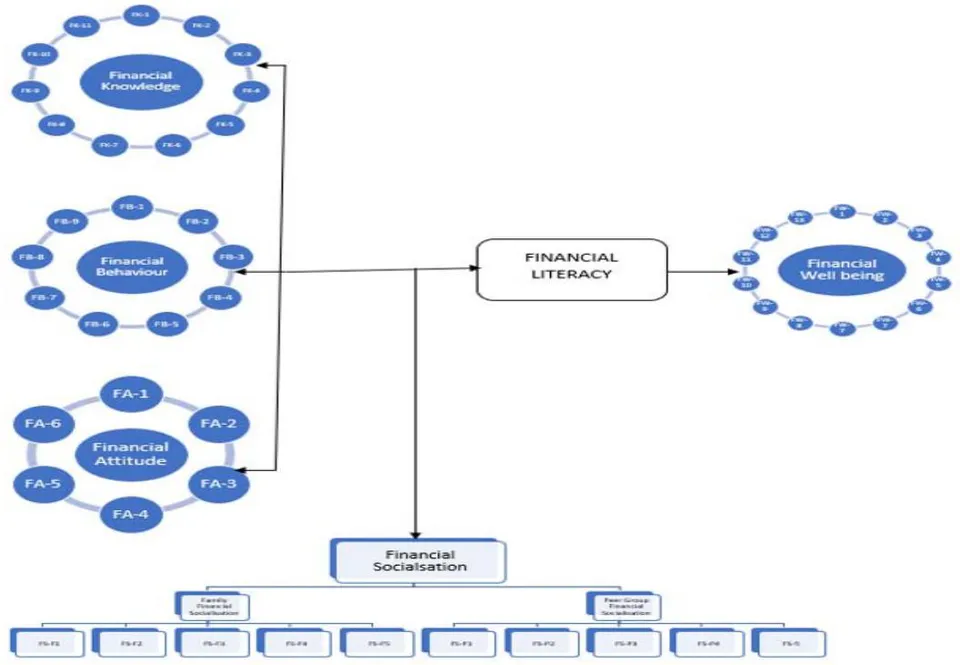

Computers were used to analyse nearly all of the data, which had been gathered via a self-administered survey. There were two sections to the survey. There are questions on demographics in the first segment, and then there are questions on independent and dependent variables in the second. The question was developed using previous research and the OECD, and it was tailored to the needs of this research paper. In this study, 15 questions were asked to measure financial knowledge and understanding, 6 questions connected to financial attitude; 9 questions linked to financial behaviour; 10 questions related to financial socialisation; and 15 questions related to financial wellbeing. After factor analysis, a few questions from financial knowledge, financial attitude, financial behaviour, financial socialisation, and financial wellbeing were deleted because their loading was less than.50. A 5-point Likert scale was used to collect data in this study. The total Variance Explained in the factor analysis process table is shown in Below tables 1 and table 2.

| Total Variance Explained | |||||||||

| Initial Eigen values | Extraction Sums of Squared Loadings | Rotation Sums of Squared Loadings | |||||||

| Component | Total | % of Variance | Cumulative% | Total | % of Variance | Cumulative% | Total | % of Variance | Cumulative% |

| 1 | 12.594 | 32.293 | 32.293 | 12.594 | 32.293 | 32.293 | 7.604 | 19.497 | 19.497 |

| 2 | 4.889 | 12.536 | 44.829 | 4.889 | 12.536 | 44.829 | 6.658 | 17.073 | 36.57 |

| 3 | 4.009 | 10.279 | 55.108 | 4.009 | 10.279 | 55.108 | 5.275 | 13.526 | 50.096 |

| 4 | 2.238 | 5.74 | 60.848 | 2.238 | 5.74 | 60.848 | 3.643 | 9.34 | 59.436 |

| 5 | 1.792 | 4.596 | 65.444 | 1.792 | 4.596 | 65.444 | 2.343 | 6.007 | 65.444 |

| 6 | 1.472 | 3.774 | 69.218 | ||||||

| 7 | 1.208 | 3.097 | 72.314 | ||||||

| 8 | 0.99 | 2.539 | 74.853 | ||||||

| 9 | 0.925 | 2.373 | 77.226 | ||||||

| 10 | 0.897 | 2.3 | 79.526 | ||||||

| 11 | 0.77 | 1.974 | 81.5 | ||||||

| 12 | 0.716 | 1.836 | 83.335 | ||||||

| 13 | 0.651 | 1.67 | 85.006 | ||||||

| 14 | 0.568 | 1.456 | 86.462 | ||||||

| 15 | 0.523 | 1.341 | 87.802 | ||||||

| 16 | 0.485 | 1.243 | 89.045 | ||||||

| 17 | 0.455 | 1.167 | 90.212 | ||||||

| 18 | 0.413 | 1.059 | 91.27 | ||||||

| 19 | 0.369 | 0.945 | 92.215 | ||||||

| 20 | 0.327 | 0.838 | 93.053 | ||||||

| 21 | 0.319 | 0.818 | 93.871 | ||||||

| 22 | 0.287 | 0.736 | 94.607 | ||||||

| 23 | 0.26 | 0.667 | 95.274 | ||||||

| 24 | 0.251 | 0.643 | 95.917 | ||||||

| 25 | 0.215 | 0.551 | 96.468 | ||||||

| 26 | 0.21 | 0.538 | 97.006 | ||||||

| 27 | 0.17 | 0.435 | 97.441 | ||||||

| 28 | 0.163 | 0.418 | 97.858 | ||||||

| 29 | 0.147 | 0.377 | 98.235 | ||||||

| 30 | 0.146 | 0.375 | 98.61 | ||||||

| 31 | 0.114 | 0.292 | 98.902 | ||||||

| 32 | 0.085 | 0.219 | 99.121 | ||||||

| 33 | 0.078 | 0.199 | 99.32 | ||||||

| 34 | 0.067 | 0.173 | 99.493 | ||||||

| 35 | 0.06 | 0.153 | 99.646 | ||||||

| 36 | 0.05 | 0.129 | 99.774 | ||||||

| 37 | 0.038 | 0.098 | 99.872 | ||||||

| 38 | 0.031 | 0.079 | 99.952 | ||||||

| 39 | 0.019 | 0.048 | 100 | ||||||

| Rotated Component Matrix(a) | |||||||

| Component | |||||||

| Variables | 1 | 2 | 3 | 4 | 5 | ||

| Independent Variable | Financial Attitude | FA_1 | 0.658 | ||||

| FA_2 | 0.775 | ||||||

| FA_3 | 0.754 | ||||||

| FA_6 | 0.728 | ||||||

| Financial Behaviour | FB_1 | 0.78 | |||||

| FB_2 | 0.735 | ||||||

| FB_3 | 0.587 | ||||||

| FB_4 | 0.577 | ||||||

| FB_6 | 0.728 | ||||||

| Financial Socialisation | FS_F1 | 0.837 | |||||

| FS_F2 | 0.861 | ||||||

| FS_F3 | 0.653 | ||||||

| FS_F4 | 0.763 | ||||||

| FS_P1 | 0.835 | ||||||

| FS_P2 | 0.852 | ||||||

| FS_P3 | 0.676 | ||||||

| FS_P4 | 0.755 | ||||||

| Financial Knowledge | FK_1 | 0.625 | |||||

| FK_2 | 0.866 | ||||||

| FK_3 | 0.848 | ||||||

| FK_4 | 0.883 | ||||||

| FK_5 | 0.902 | ||||||

| FK_8 | 0.907 | ||||||

| FK_9 | 0.732 | ||||||

| FK_10 | 0.743 | ||||||

| FK_11 | 0.718 | ||||||

| Dependant Variable | Financial Wellbeing | FW_2 | 0.624 | ||||

| FW_3 | 0.808 | ||||||

| FW_4 | 0.676 | ||||||

| FW_5 | 0.634 | ||||||

| FW_6 | 0.671 | ||||||

| FW_7 | 0.715 | ||||||

| FW_8 | 0.799 | ||||||

| FW_9 | 0.616 | ||||||

| FW_10 | 0.799 | ||||||

| FW_11 | 0.737 | ||||||

| FW_12 | 0.661 | ||||||

| FW_13 | 0.668 | ||||||

| FW_14 | 0.643 | ||||||

| Extraction Method: Principal Component Analysis. | |||||||

| Rotation Method: Varimax with Kaiser Normalization. | |||||||

| a. Rotation converged in 7 iterations. | |||||||

In Total 55 questions were designed but after factor analysis, only 39 questions were left and all the questions were removed whose loading was less than 0.50.

c) Demographic and socioeconomic factors

A sample was collected from the Haryana state in India. Haryana is a state in northern India with 22 districts, and it is the seventeenth most crowded state with a land area of 17,070 square miles (44,212 square miles) and a population of 27.39 million in 2021. Table:3 shows the characteristics of the sample used for the analysis. Out of the total respondents, were female and were male. In the sample, there is no greater difference in marital status between males and females, i.e., are married and are unmarried. In the sample, the maximum number of respondents were graduate masters and professionals, with , and

32%, respectively. In the sample, 5.13 were those who studied at the school level and were illiterate. The sample consists of maximum respondents earning between INR 20,001 and INR 40,000 p.m., i.e., earn INR 20,000 pm, earn INR 40,001-60,000, of the respondents earn INR 60,001-80,000 and earn above INR 80,000. of the respondents were working as professionals, of the respondents were salaried, were still studying, of the respondents were farmers, and were unemployed. And the sample consisted of of respondents from joint families and the rest from nuclear families.

The questionnaire was prepared with extreme seriousness, including all the relevant details, using detailed questions, attitude rating questions, as well as behaviour-related questions and responses, which were analysed on the 5-point Likert scale. The questionnaire was distributed to over 400 people, but only 117 responded, with being female and being male. The reliability of the question was tested by Cronbach's alpha through SPSS. 30 questions were asked related to banking, saving, investment, insurance, taxes, risk, etc.

to check the financial knowledge and Cronbach Alpha was.952. Cronbach Alpha for 10 questions on financial attitude was.825 and for 10 questions on financial behaviour was.708.

| Frequency | Per cent | ||

| Gender of respondent | Male | 51.00 | 43.59 |

| Female | 66.00 | 56.41 | |

| Marital Status of respondent | married | 61.00 | 52.14 |

| unmarried | 56.00 | 47.86 | |

| Qualification of respondent | School Level | 6.00 | 5.13 |

| Graduate | 35.00 | 29.91 | |

| Masters | 36.00 | 30.77 | |

| Professional | 38.00 | 32.48 | |

| Illiterate/Uneducated | 2.00 | 1.71 | |

| Occupation of the respondent | Business/Professionals | 7.00 | 5.98 |

| Salaried Employee | 72.00 | 61.54 | |

| Students | 14.00 | 11.97 | |

| Farming | 2.00 | 1.71 | |

| Not Working | 22.00 | 18.80 | |

| Monthly Family Income | Upto INR 20,000 | 21.00 | 17.95 |

| INR 20,001- 40,000 | 33.00 | 28.21 | |

| INR 40,001-60,000 | 21.00 | 17.95 | |

| INR 60,001-80,000 | 23.00 | 19.66 | |

| Above INR 80,000 | 19.00 | 16.24 | |

| Type of respondent family | Joint Family | 63.00 | 53.85 |

| Nuclear Family | 54.00 | 46.15 |

| Variables | No of Questions | Cronbach Alpha |

| Financial Knowledge | 11 | 0.952 |

| Financial Attitude | 6 | 0.825 |

| Financial Behaviour | 9 | 0.920 |

| Financial Socialisation | 10 | |

| Financial Wellbeing | 14 |

XI. RESULT AND DISCUSSION

To test the hypothesis, the researcher conducted Structural Equation Modeling using AMOS and the results are as follows:

H1: There is a significant relationship between determinants of financial literacy and financial well-being in Haryana

XII. EVALUATION OF MEASUREMENT MODEL

| Model | CMIN | DF | CMIN/DF | CFI | TFI | RMSEA | GFI | AGFI |

| Default | 81.243 | 10 | 2.495 | 0.965 | 0.985 | 0.031 | 0.94 | 0.782 |

| Tolerance limit | < 3 | >0.90 | < 0.080 | >0.80 | ||||

| (Hair, J., Black, W et al.) | ||||||||

As per Table5, Goodness-of-fit has been evaluated via CFA. According to(Hair et al., 2010), the model's fitness is satisfactory if the tolerance limit of the Absolute fit indices CMIN/DF & RMSEA, incremental fit indices (CFI & TLI), and parsimony fit index (AGFI & GFI) are within the acceptable range.

All goodness-of-fit parameters are more significant than their recommended values. Hence it can be assumed that the concluded measurement model provides an adequate level of model fit.

| Estimate | S.E. | C.R. | P | Label | ||

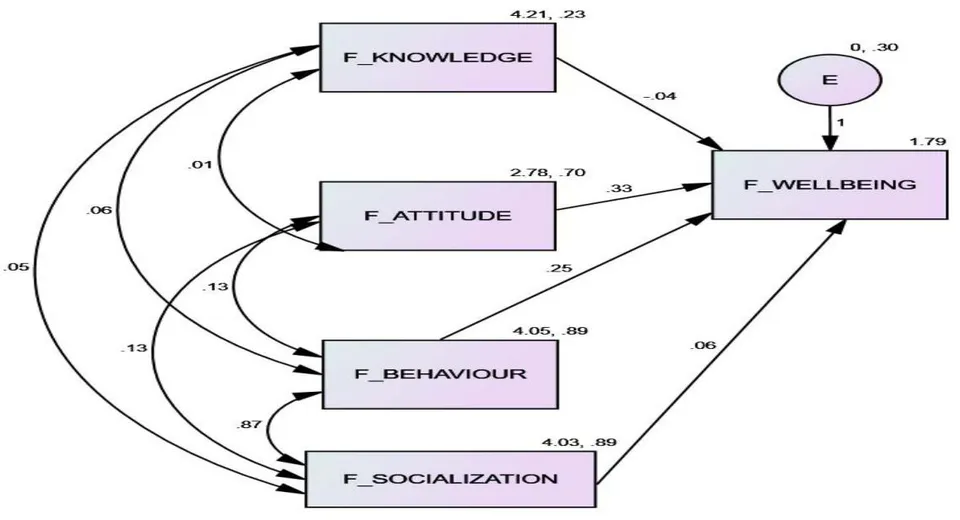

| F_WELLBEING | <--- | F_KNOWLEDGE | -.044 | .053 | -.823 | .411 |

| F_WELLBEING | <--- | F AttITUDE | .331 | .031 | 10.698 | *** |

| F_WELLBEING | <--- | F_BEHAVIOUR | .247 | .121 | 2.048 | .041 |

| F_WELLBEING | <--- | F SOCIALIZATION | .065 | .121 | .537 | .031 |

From Table: 6 it is clear that When F_KNOWLEDGE goes up by 1, F_WELLBEING goes down by 0.044 and

When F AttITUDE goes up by 1, F_WELLBEING goes up by 0.331 and

When F_BEHAVIOUR goes up by 1, F_WELLBEING goes up by 0.247 and

When F_SOCIALIZATION goes up by 1, F_WELLBEING goes up by 0.065 and .

Hence, it can be concluded that Financial Attitude, Behaviour and Socialisation have a significant relationship with financial well-being as p values are lesser than 0.05 whereas financial knowledge does not have a significant impact on financial well-being as p value=.441 which is greater than the indicator of.05

| Estimate | |||

| F_WELLBEING | <--- | F_KNOWLEDGE | -.030 |

| F_WELLBEING | <--- | F AttITUDE | .395 |

| F_WELLBEING | <--- | F_BEHAVIOUR | .335 |

| F_WELLBEING | <--- | F_socialISATION | .088 |

| F_socialISATION | F_BEHAVIOUR | F AttITUDE | F_KNOWLEDGE | |

| F_WELLBEING | .065 | .247 | .331 | -.044 |

As per Table 8, It is Clear The total (direct and indirect) effect of F_KNOWLEDGE on F_WELLBEING is -.044.

The total (direct and indirect) effect of F AttITUDE on F_WELLBEING is.331.

The total (direct and indirect) effect of F_BEHAVIOUR on F_WELLBEING is.247.

The total (direct and indirect) effect of F_SOCIALIZATION on F_WELLBEING is.065.

| Estimate | S.E. | C.R. | P | Label | |

| F_WELLBEING | 1.790 | .247 | 7.234 | *** | par_14 |

As per Table 9, The intercept in the equation for predicting F_WELLBEING is estimated to be 1.790. The probability of getting a critical ratio as large as 7.234 in absolute value is less than 0.001. In other words, the intercept in the equation for predicting F_WELLBEING is significantly different from zero at the 0.001 level (two-tailed).

On the basis of the result, the researcher comes up with reframed financial literacy and financial wellbeing model as shown in figure 5.

XIII. FINDING AND CONCLUSION

The main purpose of the study is the association between the determinant of financial literacy and financial well-being. In this study, only four determinants of financial literacy are taken into consideration and found that only financial attitude, financial behaviour and financial socialisation have a greater influence on financial well-being. As per this study financial socialisation is also a very important determinant of financial well-being. Socialisation may be family, peer group, etc. This study partially supports the previous studies, as previous research shows that financial knowledge also influences financial well-being but to the current research only financial attitude, financial behaviour and financial socialisation significantly influence financial well-being (Deswal, 2015; Van Praag, Frijters and Ferrer-i-Carbonell, 2003; Barrafrem, Vastfjäll and Tinghög, 2020; Taft, Hosein and Mehrizi, 2013; Gerrans, Speelman and Campitelli, 2014) but we can't ignore the other factors which influence the financial literacy and financial wellbeing. As per the result, financial knowledge may be an important factor in financial literacy but not an important factor in financial well-being. So, Government, financial institutions, Schools and colleges should focus on building attitudes, financial behaviour and financial socialisation for the well-being of society. During data collection, it was seen that in rural areas, females are not allowed to go outside of the home expect a few events, and they got less chance of socialisation. And found that they get together during financial literacy camps to discuss finance and finance-related issues. So, the government should focus on financial literacy camps at frequent intervals because financial literacy camps play a very important role in financial socialisation.

XIV. LIMITATIONS OF THE STUDY

The current analysis is not without constraints. The first limitation, this study was conducted through online forms only and. Secondly study includes only the rural young population of Haryana, India. The third sample size is to sample.

XV. PRACTICAL IMPLICATIONS

The maximum researchers took demographic, and socioeconomic factors as a determinant of financial literacy and took "financial attitude, financial behaviour, financial knowledge and socialisation" as a dimension of financial study. But research is done on taking the dimensions of financial literacy as a determinant of financial literacy. This research will help the researcher to take more focus on the determinants of financial literacy to strengthen financial literacy and financial wellbeing.

XVI. FUTURE SCOPE

The researcher can take more samples to remove the above limitations and consider other important determinates and should also check the association between financial socialisation agents, Family, income and financial wellbeing.