Green investments play an important role in achieving the sustainable development goals and creating an environmentally friendly structure of the economy as a whole. At the same time, at the present stage there is a significant deficit of green investment, which is largely a consequence of the imbalance between short-term financial and long-term environmental interests. Among the main reasons for the lack of green investments attractiveness is their increased riskiness from the point of view of existing financial markets. The existing system for assessing investments within the framework of the risk-return matrix does not fully take into account a number of social and environmental effects that do not have a direct monetary value and do not contribute to increasing market returns. Based on the analysis of the category of green investments itself, as well as the risks associated with it, the article proposes a comprehensive approach to managing investment risks based on their structurally functional classification and inclusion of potential effects from reducing environmental risks in the analysis.

## I. INTRODUCTION

Within the modern economic paradigm, growth of consumption is considered as one of the key measures of social progress. As a result, human development is accompanied by considerable pressure on the environment, which today has reached a critical level in a number of parameters. Climate change, resource depletion, ecosystem degradation and a number of other environmental problems threaten the possibility to maintain and improve the quality of life in the long run. Elimination (significant mitigation) of this threat is possible only with a fundamental systemic restructuring of the existing model of production and consumption, which requires significant investments. In recent years, economics and related sciences have paid much attention to the category of green investments, the distinctive feature of which is the focus on achieving an environmental effect. These investments play a decisive role in environmentally friendly structural transformation and the development of an environmentally sustainable economic model. According to some assessments, to achieve climate change goals the global economy needs at least $6 trillion investments per year only in green infrastructure [1]. However, their actual volume today is about $500 billion annually [2]. At the same time, affordable savings potential allows to overcome the shortage. The amount of private capital under management in various financial funds in the world is over $100 trillion. [3]. Nevertheless, the increased risk associated with the implementation of green projects and the financing of environmentally oriented activities makes it hardly possible to close the investment gap. From this perspective, the problem of risk-management in the field of green financing requires special consideration.

### a) Methodological Aspects of Risk-Management in the Field of Green Finance

Increasing interest in green investments among researchers and practitioners is a cause of a rapid growth of the number of publications on this topic, which concern a wide range of aspects related to the definition of the category itself, the analysis of various investment instruments, the necessary investment institutions, etc. One of the least studied aspects and, at the same time, one the most important for the attractiveness of green investments is risk. Its assessment and the development of an effective risk-management system assume the development of a classification system necessary for the identification and typology of green investments in accordance with the most significant parameters for risk measurement. However, this task is complicated by the lack of a clear, generally accepted definition of the category of green investments itself [4]. Although there has been progress towards some unification in recent years, various institutions and organizations establish their own criteria, which can be quite widely interpreted.

There are a number of approaches to green activity taxonomy that can be used as a basis for identifying if the investment is green. One of them is the EU taxonomy for sustainable activities [5]. Its development was aimed at solving the problem of defining and measuring environmentally sustainable economic activities, but serious usability challenges are emerged when the taxonomy is applied for practical purposes [6].

The more detailed taxonomy system for determining green investments is developed at the project level as well as for specific financial assets and instruments, for example, green bonds, green loans, green insurance [2], etc. According to the definition of International Capital Markets Association (ICMA) [7], green investments are aimed at financing projects which help to solve environmental problems, including slowdown and prevention of climate change, combating pollution, preserving biological diversity, etc. As a rule, the top priority of environmentally friendly finance is low-carbon projects and assets that contributes to decreasing of greenhouse gases emission [8].

An OECD study [9] ranks green investments based on the nature of their contribution to achieving environmental goals, distinguishing direct and indirect investments. Direct investments are usually associated with participation in the creation of green jobs and green infrastructure. Indirect investing is related to buying green securities or funding financial institutions, which are engaged in green projects. The mediating character of indirect investments may affect their effectiveness in the achievement of environmental goals.

A wider interpretation of green investments is offered in the G20 report [10], according to which green investments provide environmental benefits and contribute to the implementation of environmentally sustainable development goals. In line with such an approach, it is more correctly to speak about sustainable or ESG investments [2]. Their classification can be based on the broad system of criteria, including the objective of investments, their impact, the specifics of pre-investment and post-investment strategies and so on [11]. However, this approach to taxonomy, as well as the ones considered earlier, are not openly related to risk-management.

Given the specifics of green investments, it is reasonable to take the interrelations of risk and environmental effect as the basis of classification. The impact of risks on the attractiveness of green investments can be considered in two aspects.

On the One Hand: Green investments as a separate financial category became relevant due to the need for improving the environmental sustainability of development and mitigating the risks caused by the negative consequences of human impact on the environment. According to a widespread in finance practice approach [2, 12], there can be distinguished three groups of risks, the reduction of which is driven by green investments: physical, transition and liability risks.

Physical risks are the cause of damage resulting from the changes in the physical characteristics of the natural environment, for example, an increase in the concentration of greenhouse gases, growing precipitation deficit, a decrease in the area of natural ecosystems, etc. In turn, investments aimed at prevention of these

changes and mitigation of anthropogenic impact make it possible to reduce the level of physical risks.

The emergence of transition or transformation risks is caused by a decrease in the value of assets or inability to use assets because of structural reorganization of the economy. For example, the development of the carbon market could lead to the inefficiency of coal energy, and consequently to the depreciation of hard coal deposits and the stock of coal power plants. Environmentally oriented structural changes through green investments and a decrease of the environmentally unfriendly assets share on the balance will reduce the level of transformation risk.

Liability risks are associated with the potential litigation damage and depend on the probability of being sued for the environmental impact caused by the company activity. In that case, not only direct, but also indirect damage, like reputational losses, should be taken into account. The level of this type of risks is to a great extent determined by the nature of the legal system under consideration, the characteristics of environmental legislation and law enforcement practice in a particular country. An additional uncertainty is caused by the fact that the potential losses can be based on the subjective assessments and judgments. As a result, the damage from the liability risks is largely dependent on the reaction on the environmentally hazardous activities from consumers, contractors, government agencies and other stakeholders.

Integrating the risks considered above into the system of risk-management can have a significant impact on investment decision-making [13], since risk-profitability relationship forms the basis of performance measurement in finance. It suggests the increasing influence of green investments on efficiency assessments. Unlike traditional investments, the notion "green" implies the focus on environmental results. The latter have become an important part of investment decision-making mainly due to the negative environmental consequences of regular economic activity, which adverse impact on the quality of life is increasingly evident. From this perspective, green investments should not be considered as an alternative to traditional investing. They are rather a compensating component of investment portfolio (investment strategy of any entity or state) aimed at mitigation (prevention) of environmentally related risks [14].

The appropriate way to demonstrate such an approach to green investments is to use the Sharpe ratio [15], which is calculated as an additional portfolio yield per unit of risk measured in terms of volatility. This ratio can be improved by not only enhancing the profit on investments, but also reducing the risk of portfolio. Even decreasing profitability is regarded as acceptable, if the degree of risk reduction is sufficient to ensure the Sharpe ratio growth.

Representing environmental risks in terms of market volatility is a challenge that hardly can be adequately addressed today. Nevertheless, including them in any implicit or explicit way into consideration when assessing profitability-risk ratio essentially changes the role of green investments in decision-making. Green investments becomes an important component of diversification, which, in line with the approach of H. Markowitz [16], is the most efficient way of portfolio risk optimization.

On the other hand: The orientation of green investments towards achieving an environmental effect, which in modern conditions cannot always be transformed into financial income for a number of institutional and other reasons, becomes a source of risk given the uncertainty regarding the monetization of this effect. In these circumstances, if decision-making is based on risk-profitability matrix, green investments may be too risky in comparison with the expected return. From this perspective, improving the risk-management system becomes the key factor of improving the attractiveness of green investments.

When identifying the sources of additional uncertainty and risks in the green finance sector, it is reasonable to distinguish two types of them - conditioned by the green economy specifics and not conditioned. Risks of the first type are associated with the uncertainty of assessing the environmental consequences of investments. Analyzing their main sources, the following issues should be paid special attention to:

- Imperfections of institutional environment, including the underdevelopment of the markets for green products and ecosystem services, the lack of effective non-market tools for the transformation of environmentally oriented demand into financial flows, the insufficient role of environmental taxation in the economy regulation, etc.;

- Technical and technological reasons, including the lack of technical capabilities to measure the environmental effects of green investments timely and adequately, the high cost of technologies necessary for such measurements, insufficient personnel qualifications, the lack of infrastructure needed for the effective application of information technologies, satellite monitoring, big data analysis, artificial intelligence, etc.;

- Vague nature of environmental effect caused by the difficulty to ensure its precise spatial and temporal localization. Given that the environmental benefits of green investments may become tangible only in the long run, as well as have an indirect form manifesting through different components of the natural environment, their economic assessment, even made with the application of cutting-edge

technologies, may raise doubts about its relevancy and credibility;

Information uncertainty caused by the lack of necessary information about the environmental consequences of investments. Investors may be intentionally or unintentionally misled about the actual impact of investments, which may not meet certain environmental standards. This phenomenon is also known as green washing. One of the reasons for such a risk is the lack of generally accepted standards that can help to define green investments unambiguously. For example, a company may announce that it will invest in reducing negative environmental impact by replacing dirtier coal with a cleaner grade. Despite the possible environmental improvements when burning new grade of coal, the project itself is based on the development of coal energy, which is difficult to regard as green.

The sources of green investment risks due to the specifics of the green sector are not limited to the factors listed above. At the same time, it is necessary to understand that as the green sector becomes more integrated into the economy, the environmental benefits will be increasingly monetized and transformed into the financial flows. As a result, the green specificity of risks can disappear and the second type risks, which are not conditioned by the peculiar features of the green sector, will become increasingly important. They can be categorized according to various criteria. Theory and practice of risk-management offers a variety of approaches to classification depending on the scope and nature of activity, management goals, and other factors. In particular, dividing risks into systemic and non-systemic is essential for the assessment of an investment portfolio. In the financial sector, special attention is paid to credit, interest rate, and liquidity risks. Special risk assessment systems are used to justify and implement investment projects. From the point of view of risk-management, the promising approach can be the risk classification depending on the role green investments play (or the function they perform) in the development of green economy and formation of its structure.

### b) Risk-Adjusted Typology of Green Investments

The most important areas that require green investments to ensure the balanced structure of green economy include green innovations, green infrastructure, the production of green goods and services, environmental protection and safety [9]. From this position, four enlarged groups of investments can be distinguished:

1. Investments in green technologies;

2. Investments in green infrastructure;

3. Investments in the conservation and restoration of ecosystems;

4. Investments in improving the environmental and resource efficiency of the traditional sector of the economy.

The proposed classification is somewhat arbitrary. It is obvious that the development of green technologies requires the creation of appropriate infrastructure, natural ecosystems can become part of this infrastructure and green technologies can be used to restore them, as well as to increase the resource efficiency of the traditional sector of the economy. However, dividing investments into the specified structural-functional groups makes it possible to take into account the peculiarities conditioned by how an environmental effect is achieved, to identify the most characteristic risks for each group and to manage them more effectively. Any of the presented four groups can be divided into smaller subgroups, for example, environmental protection activities for various industries, conservation of various types of ecosystems, etc. At the same time, the functional approach to analyzing the risk of green investments should not fundamentally change. The risks associated with the first type of investment depend primarily on novelty and the degree of development of the technology. A number of green technologies, for example, wind or solar energy, have become quite widespread on the market. Many companies in this area have an established business model and receive stable income; their shares are listed on the well-known stock exchanges. The last aspect is important from the risk-management perspective, as publicity helps to reduce uncertainty, since companies whose shares are put up for trading on exchanges are required to make their reporting publicly available, although the degree of information disclosure may vary depending on the requirements of the specific exchange or national legislation. Investments in such companies are quite reliable, and sensitivity to systemic risk, although it varies depending on the region, type of technology and other factors, is within the market average[17, 18]. This conclusion is confirmed by the analysis of the $\beta$ parameter for various companies in the green sector of the economy based on data from the world's leading stock exchanges. At the same time, investors, depending on their risk appetite, can choose more risky financing instruments (for example, green company stock) or less risky ones (for example, green bonds).

With regard to the development of new green technologies, we can talk about the existence of risks inherent in venture financing. All other things being equal, the level and character of venture risks depend on the stage of technology development. As a rule, the initial stages are characterized by the greatest uncertainty. As technology progresses and a target market grows, the level of risk decreases. In this context, effective venture risk management assumes that the choice of financing tools and investment goals is determined by the stage of commercialization of the green innovative project [19].

As a whole, the risks associated with investments in the development of green technologies include both - risks proper to innovative business in general and risks caused by the specifics of the green sector of the economy. The latter are largely determined by institutional factors, including the presence of appropriate legislation, the level of development of the market for green goods and services, the character of policy measures regarding the green economy, etc., which determines the possibility of monetizing the environmental benefits that green technologies are aimed at achieving.

The second type of investment is closely related to the risks characteristic of infrastructure projects. Their distinctive feature is high capital intensity and a long (sometimes extremely long) planning horizon. As a rule, upgrading and creating new infrastructure requires significant financial resources, and its service life is usually characterized by an increased duration that often exceeds the time frame adopted in the decision-making of most investors and financial institutions. In view of the above, the level of risk of infrastructure projects is often too high for market participants. This is also true for green infrastructure, although, it is worth noting that this category can be interpreted quite broadly. Given that new infrastructure in many cases involves the use of modern, more resource-efficient materials and technologies, such projects can be conditionally considered green, even if they are not directly aimed at the development of any element of green economy.

The need for significant amounts of initial investment and a long payback period make infrastructure projects too risky limiting the possibilities of their financing. Effective risk management in this situation involves creating conditions for attracting so-called "long money". Most investors in the market, including commercial banks, are focused on optimizing the risk-return ratio and cannot afford investments that take more than ten years to pay off. A feature of this group of investments is the disproportionate shift of risks for the initial period. As analysis shows, the cost of infrastructure bonds and their riskiness decrease as the project is implemented (5, 10 years from the moment of operation) [20].

Therefore, financial institutions such as pension funds and development banks play an important role in attracting infrastructure investments. The former accumulate the savings of investors for the period of working activity until retirement, and therefore have the resources to invest for a sufficiently long period. The latter are not only an important source of long-term investments, but also the providers of associated services, including various tools for reducing risks, expert assistance in the assessment and management of projects. Development banks play a special role in countries with underdeveloped financial markets and limited availability of private capital. At the same time, in developed countries these institutions can also play an important role for financing green infrastructure. They are often specialized, may be called green investment banks or green development banks. Typical examples of such institutions are the UK Green Investment Group or the German Reconstruction Bank (Kreditanstalt für Wiederaufbau)[2]. The latter has specialized in green finance since the early 2000th and played an important role in the development of renewable energy.

For a number of reasons, investments in the conservation and restoration of ecosystems can be considered among the most risky. Firstly, the possibilities for implementing such projects are often limited by natural reproduction processes and require considerable time. For example, restoration of forest and wetland ecosystems can take decades. Secondly, the natural environment is characterized by many complex and entangled relationships between various elements. Changes in one ecosystem can lead to various unforeseen effects (both negative and positive) in other ecosystems, which further increases the level of uncertainty when making investment decisions. Thirdly, the financial attractiveness of this type of investment largely depends on the institutional environment necessary for monetizing the environmental effect, in particular, the development of the market for green products, the availability of other effective payment systems for ecosystem services. A typical example is the carbon market. Forest and wetland ecosystems are regarded as the main natural absorber of carbon dioxide. So integrating landowners and forestry companies in the carbon market may create an additional source of income and encourage new investments in the forest restoration [21, 22]. As an assessment carried out for the forest growing sector in Belarus showed, the participation of the republic in the European carbon trading system would become an important source of the financial revenues for its forestry. This will increase the profitability of investments in the restoration of forest ecosystems by more than 2 times and significantly increasing their attractiveness for a wide range of investors [23].

At the present stage, a number of technical and institutional factors limits the possibility of generating income from projects in the field of the restoration of natural ecosystems and the conservation of biological diversity. This makes them risky for commercial investors. Therefore, an important role in financing such projects is played by budgetary funds, non-profit, sovereign funds, international and other financial institutions that provide resources on a free or preferential basis. The key factor in reducing the risk of this group of investments to an acceptable level is shaping a stable institutional environment capable of providing the necessary financial flow from the use of ecosystem services.

Investments of the fourth group are primarily associated with risks characteristic of the type (object) of economic activity within which projects on the improvement of environmental efficiency are being implemented. Since organizational, production, and technological processes can vary greatly in their complexity, danger, and degree of impact on the environment, the risks that must be assessed and taken into account can also vary significantly. In this case, effective risk management requires good knowledge of the field of activity in which the project is being implemented, as well as an understanding of the main trends in its development.

Despite the fact that investments in this group are associated with a variety of risks caused by production and technological differences, their common feature is the ability to reduce operational risks of economic activity. Increasing resource and environmental efficiency implies reducing the consumption of raw materials and energy, abating environmental pollution, which should lead to a decline in material costs and environmentally related tax payments. Lower resource intensity means not only cost savings, but also reduced dependence on suppliers of energy and materials and at the same time limits the impact of the risk of price volatility, which is especially important for the imported resources.

One of the most typical areas of such investments is the implementation of energy saving projects in both the manufacturing and housing utility sectors. Reducing operational risks by cutting costs for the consumption of heat, electricity, water, various types of raw materials and decreasing their impact on the final financial results is an important factor in investment attractiveness. The investor's decision-making depends on how he assesses the level of operational risks reduction in the future in comparison with the risks associated with capital investments now. This relationship can be demonstrated using the example of a green mortgage. According to some estimates, among green mortgage loans borrowers the percentage of non-payments is lower than in the case of a conventional mortgage [24]. This is due to the lower financial burden on owners of environmentally efficient housing, since they consume comparatively less water and energy resources. Since the risk of a green mortgage is lower than for a conventional one, some financial institutions offer mortgages for the purchase of green (resource- and energy-efficient) housing at reduced rates, increasing the attractiveness of financial investments in environmentally efficient construction projects.

When assessing the risks of the fourth group of investments, the key role is played by the price factor and institutional regulation of environmental protection.

The rising cost of raw materials and energy, increasing environmental taxes and tightening environmental standards will contribute to the attractiveness of green investments. At the same time, under the conditions of market pricing, additional risks may be associated with the dynamics of resource prices and their volatility.

### c) General Framework for Developing a Comprehensive Approach to Green Investments Risk Management

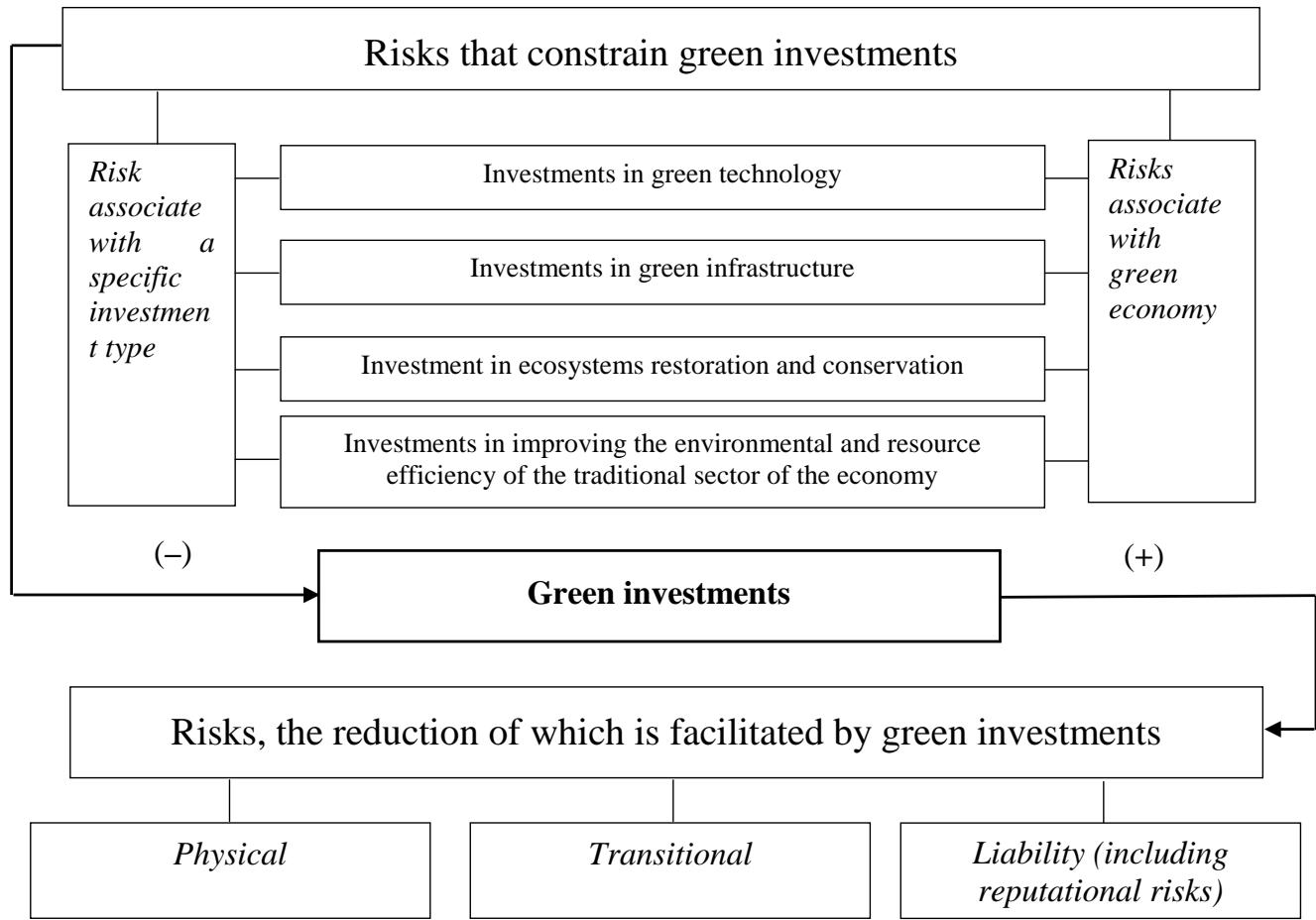

A systematic approach to risk-management involves their comprehensive consideration, including both risks that constrain green investments and risks that green investments contribute to reducing. In view of the above, the comprehensive approach to green investments risk-management in its most general form may be represented by the scheme shown in the figure. As you can see, the upper part of the scheme presents the risks that hinder green investments. They are grouped according to the structurally functional principle, highlighting specific and non-specific green risks. The lower part includes three enlarged groups of risks, the reduction of which is facilitated by green investments.

Figure: The Basic Scheme of Comprehensive Approach to Green Investment Risk-Management

Source:Developed by the Author

The proposed comprehensive approach is based on the integration of key risks for making decisions on green financing. This should help to make assessments more adequate and complete, better understand the relationship between risks and the results of investment activities (including the environmental effects) and improve the quality of information necessary for investors. Applying the comprehensive approach allows more efficient use of risk-management instruments. It should encourage green investments and increase their attractiveness, which according to the proposed scheme is determined by the possibility of reducing the group of risks in the upper part of the figure (focus on risk reduction is indicated by a "minus" sign) and the potential of investments to influence risks in the lower part of the figure (focus on increasing potential is indicated by a "plus" sign).

Successful implementation of the presented approach depends on a number of technical, institutional and managerial factors and involves the use of a wide range of tools necessary to more clearly identify risks, improve comparability and increase the adequacy of their assessments. In this context, solving the problem of green investments encouragement requires additional research into many aspects related both to the specifics of the green sector, including the peculiarities of environmental effects assessment and accounting, as well as to the functional and sectoral differences in investment objects. At the same time, one of the key trends that is important to consider when changing investment priorities is the transformation of the risk profile. Since a typical green business model implies a reduction in the consumption of material resources and energy through the use of more modern technologies and updated infrastructure, it can be assumed that green projects will require higher (compared to traditional) initial investments, ensuring reduction of operating costs in the future. This means that the risk profile of green investments is characterized by a relatively higher level at the initial stage of green project (capital investment stage) and a lower level at the operation stage. An illustrative example is the comparison of business models in the fields of wind (hydro, solar) energy and energy built on fossil fuels.

Comparing the key differences of two business models allows us to conclude that one of the main reasons for the increased risk of green investments is the shift of a significant part of the costs to earlier stages of project implementation, while additional income is expected in the longer term. Under conditions of positive interest rate, all other things being equal, long-term projects are more risky than short-term ones. In this regard, an important financial tool for increasing the attractiveness of green investments is regulating the size and composition of interest rate [14], bringing it into line with the long-term interests of economic development.

The time factor and the interest rate, which is essentially the price of time, are the most important elements of the risk management system in finance, and the risks associated with green investments are no exception. However, the proposed comprehensive approach cannot be limited to these aspects. Its efficient practical implementation presupposes the most complete coverage and disaggregation of risk factors, since the quality of their assessment and the quality of investment decisions depend on this. In turn, the quality of the assessments implies the availability of the necessary information, the availability of technologies for obtaining it, as well as improving the appropriate regulatory framework and increasing the degree of integration of environmental priorities and financial interests in general. Further expansion of technical capabilities for risk assessment, including the development of big data analysis systems, artificial intelligence, the Internet of things, etc. on the one hand, and shaping of the institutional environment necessary for transforming the environmental effects into financial results, on the other, will contribute to increasing the attractiveness of green investments in the wide circles of investors.

## II. CONCLUSION

The proposed comprehensive approach to green investments risk-management implies an expansion of the scope of analysis, going beyond the traditional system of investment risk assessment. The latter does not fully take into account a number of effects, including environmental ones, which can hardly be monetized within the traditional framework of decision-making and have a limited impact on investment profitability. This is a one of the key reasons for the lack of attractiveness of green investments. Systematization of risks on a structurally functional basis and widening the scope of analysis by including impact related to the long-term goals of green finance to improve the environmental sustainability of development will help overcome the limitations inherent in the existing financial systems allowing for a more balanced risk-return assessment. Thus, the implementation of a comprehensive approach to green investments risk-management while simultaneously improving the technical and institutional aspects of assessing the environmental effects will be an important factor in increasing the attractiveness of green investments within the based on the risk-return assessmentsdecisionmaking framework.

Generating HTML Viewer...

References

24 Cites in Article

Globalising green finance: the UK as an international hub.

S Thompson (2021). Green and Sustainable Finance: Principles and Practice / S. Thompson.

(2020). 14 Asset Management.

Ewa Dziwok,Johannes Jäger (2021). A Classification of Different Approaches to Green Finance and Green Monetary Policy.

Dirk Zetzsche,Linn Anker-Sørensen (2022). Regulating Sustainable Finance in the Dark.

N Pluff,O Altun Ensuring the usability of the EU green taxonomy/ICMA. 2022. Ensuring-the-Usability-of-the-EU-Taxonomy-and-Ensuring-the-Usability-of-the-EU-Taxonomy-February-2022.

(2020). High-level definitions.

(2023). Mobilising Finance for Climate Action in Georgia.

G Inderst (2012). Defining and Measuring Green Investments.

(2016). OECD Secretary-General Tax Report to G20 Finance Ministers and Central Bank Governors (Shanghai, China, February 2016).

T Busch (2022). https://inass.org/wp-content/uploads/2022/05/2022083131-2.pdf.

Guillermo Mulville,Julian Gonzalez,Carlos Martin-Delgado (2025). How Emerging Technologies and Solutions in Fixed Connectivity Contribute to Climate Mitigation and Adaptation.

A Dutta (2023). Climate risk and green investments: New evidence.

I Dzeraviaha,C Xie,Z Shao (2022). Assessing the efficiency of green investments based on portfolio approach.

V Zakamouline,S Koekebakker (2009). Portfolio performance evaluation with generalized Sharpe ratios: Beyond the mean and variance.

Harry Markowitz (2005). Market Efficiency: A Theoretical Distinction and So What?.

S Sailendra (2023). Moderating Effect of Green Image: The Influence of Beta on Stock Return.

F Ielasi,P Ceccherini,P Zito (2020). Integrating ESG Analysis into Smart Beta Strategies.

Mahendra Ramsinghani (2021). The Business of Venture Capital.

(2019). Handbook of green finance: energy security and sustainable development.

Anil Shrestha,Sarah Eshpeter,Nuyun Li,Jinliang Li,John Nile,Guangyu Wang (2022). Inclusion of forestry offsets in emission trading schemes: insights from global experts.

F Coleman (2018). Forest-based carbon sequestration, and the role of forward, futures, and carbon-lending markets: A comparative institutions approach.

Игорь Деревяго,Елизавета Минченко,Диана Малашевич (2022). Особенности учета фактора риска при оценке стоимости «зеленого» финансирования.

Raffaele Volante (2007). Mortgage credit contracts and the Green Paper on Mortgage Credit – Controls on Transparency and Fairness.

No ethics committee approval was required for this article type.

Data Availability

Not applicable for this article.

How to Cite This Article

Ihar Dzeraviaha. 2026. \u201cDeveloping a Comprehensive Approach to Green Investment Risk-Management\u201d. Global Journal of Management and Business Research - B: Economic & Commerce GJMBR-B Volume 23 (GJMBR Volume 23 Issue B6): .

Explore published articles in an immersive Augmented Reality environment. Our platform converts research papers into interactive 3D books, allowing readers to view and interact with content using AR and VR compatible devices.

Your published article is automatically converted into a realistic 3D book. Flip through pages and read research papers in a more engaging and interactive format.

Green investments play an important role in achieving the sustainable development goals and creating an environmentally friendly structure of the economy as a whole. At the same time, at the present stage there is a significant deficit of green investment, which is largely a consequence of the imbalance between short-term financial and long-term environmental interests. Among the main reasons for the lack of green investments attractiveness is their increased riskiness from the point of view of existing financial markets. The existing system for assessing investments within the framework of the risk-return matrix does not fully take into account a number of social and environmental effects that do not have a direct monetary value and do not contribute to increasing market returns. Based on the analysis of the category of green investments itself, as well as the risks associated with it, the article proposes a comprehensive approach to managing investment risks based on their structurally functional classification and inclusion of potential effects from reducing environmental risks in the analysis.

Our website is actively being updated, and changes may occur frequently. Please clear your browser cache if needed. For feedback or error reporting, please email [email protected]

Thank you for connecting with us. We will respond to you shortly.