This paper examines the evolution of the personal income tax (IRPEF) over fifty years. It describes the evolution of progressivity, initially based on a bracket structure, while the current dominant role is played by decreasing tax credits, creating excessive elasticity for most incomes. Furthermore, over time, many incomes that were initially included in the IRPEF have been progressively excluded. The system requires a thorough overhaul; the proposals presented are based on the dual system, in which income from work and income from capital are classified under two different taxes. The bracket structure is substituted by a continuous function for all tax payers.

### INTRODUCTION

About fifty years ago, Italy had a lower tax burden than countries like France, Germany[^12], and the United Kingdom, not to mention the Scandinavian countries. However, it had a higher one than Spain and other Mediterranean countries; indeed, the direct relationship between per capita GDP and tax burden has often been noted. What negatively affected our country was the low level of direct taxes as a proportion of the total, just over a fifth. In particular, a personal income tax, characteristic of European and Anglo-Saxon countries, was absent. The main direct $\mathbf{t}\mathbf{a}\mathbf{x}^{1}$ the tax hit each individual income separately with different rates, both for individual and societies. There was a progressive[^2] $\mathbf{t}\mathbf{a}\mathbf{x}^{2}$ that affected a relatively limited number of higher income earners and generated a significantly lower revenue.

On 1971 a general reform established two taxes, Impostasul Redditodelle Persone Fisiche (IRPEF), a personal income tax, and Impostasul Redditodelle Persone Giuridiche (IRPEG), a corporate income tax; according to European agreements, a value-added tax was introduced, in the place of an indirect tax on sales which was a cumulative cascade tax like the US sales tax.

IRPEF was originally introduced with 32 brackets; the first one with a rate of 10 percent up to 2 million litre[^3], and the last rate (72 percent) for incomes exceeding 500 million litre. The rather high progressivity is due (almost) entirely to the structure of brackets and relative rates; deductions and tax credits were extremely limited. As we will see, the initial structure of the tax was completely different from the current one.

The model on which IRPEF was inspired was the Comprehensive Income Tax (CIT) developed by two American economists, Robert Haig (1921) and Henry Simons (1938), preceded by the German Georg von Schanz (1896). The CIT considers income to be the sum of consumption plus the net variation in assets in the period (year) considered. Therefore, not only the remuneration of workers and the profit from business or professional activities (produced income) is considered income, but any sum that enters the subject's availability and may be used for consumption or capital increases. In the 1960s, the CIT was the theoretical model of reference, particularly in the Anglo-Saxon world; it should be remembered that in Italy economists, like Luigi Einaudi, were ardent supporters of the exemption of savings from tax.

### a) IRPEF Leakages from Capital

IRPEF immediately deviates from CIT by excluding all financial income, which should be included as revenue from capital. The reason was due to risk of capital flight, but, after two years, the political world realized[^4] that large business owners (like Agnelli's family with FIAT) and small owners of a few shares paid the same percentage of tax, 30 percent on dividends.

The most logical solution was to include the dividend in the IRPEF tax base, with a tax credit that offset amount already paid in IRPEG, so that each shareholder would pay according to their overall income and therefore corresponding marginal tax rate. Moreover, ordinary shares are registered, and consequently there were no risks of. Thus in 1978 (Pandolfi law) dividends from ordinary shares became part of IRPEF. However, in the following decades, presence of these capital incomes gradually disappeared; from 2017 all dividends are taxed with the same rate of 26 percent, the same applied to all income from financial activities.

While in the case of revenue from financial assets there is a legal exemption from IRPEF, in the case of income from real estate and land, however, it is better to use the term "erosion", meaning that values to be declared in IRPEF are lower than the market ones. In the case of land, income was determined by the specific land registry, which determined land and agricultural income. This income, which was not updated, was generally lower than the actual income. A similar argument applies to cadastral income from real estate, which had to be declared by the owners when they themselves used the property. Residential apartments also had a deduction, which had grown over the years to the point of limiting the number of residents still paying the tax to less than $20\%$. In 2000, cadastral income became formally exempt for all taxpayers.

Eight years later, Berlusconi's government extended the local property tax exemption to residential apartments[^5], except most luxurious ones (a very small percentage of the total). Monti's government reintroduced the tax but subsequent Renzi's government again confirmed the exemption. Italy is at present one of the few countries in the world and it is the only one in Europe to exempt a great part of apartments, so that the burden of property tax hits all other properties more severely. It is easy to explain why politicians of different orientations grant the exemption for first home: percentage of apartment owners in Italy is very high (around $80\%$ ). This high percentage depends to a large extent on the severe shortage of public housing.

Income from non-residential properties and rental housing, to be declared in IRPEF, in the early 2000s, was a rather small amount. But since 2011, there has been an option for a flat-rate tax of 21 percent (reduced to 10 percent in case of popular housing); the option also includes elimination of registration and stamp duty. The flat-rate tax option, with rate 21 percent, from 2019 has also been extended to instrumental leases, in case of shops and stores with a surface area no greater than 600 square meters.

In conclusion only a smaller part of revenue from real estate properties remains to be declared in IRPEF; as Vincenzo Visco[^6](1984) stated, "IRPEF is certainly not a general tax on income, but rather takes on the characteristics of a special tax on certain incomes, in particular on incomes from employment and pensions". These words may even be considered too harsh compared to what happened after the first ten years of the tax.

In conclusion it can be said that IRPEF is very far from the CIT model; it is not a condemnation as such, as there is an alternative model, that of the dual system, as we will see later, where capital income is subject to a separate tax.

### b) IRPEF Work's Leakages

In a dual system the personal income tax personal income tax should include all earnings from work; in the last ten years we have witnessed the progressive exodus of self-employed workers from the personal income tax. The introduction of the flat-rate system for VAT-registered individuals has allowed a greater part of them[^7] to opt for a separate flat tax.

It is interesting to note how an institution originally born to facilitate the start-up and early years of small individual businesses, especially among professionals, has evolved into an alternative tax system for almost two million self-employed people. In 2008 Prodi's government introduced the minimum tax regime for young people eager to start a business (with a VAT number); the regime was valid until the age of $35^{\text{th}}$. Essentially, it was a transitional regime, after which self-employed workers would revert to personal income tax (IRPEF).

Revenue could not exceed €30,000 euro, and purchases of capital goods in last three years of operation could not exceed €15,000. It was not allowed to have employees. Taxable income was determined as the difference between documented revenues and costs (like regular income tax); VAT was not required, while the substitute rate for income tax (IRPEF) and regional production tax (IRAP), initially set at 20%, was subsequently reduced to 5% in 2011 (due to the supervening financial crisis).

With the 2016 Stability Law, the "small operator regime" changed its name to the "flat-rate regime"; more importantly, its nature changed, becoming a permanent option for VAT-registered individuals (with the option to revert to the IRPEF regime after three years). The takings limit was raised to €65,000; the investment limit was eliminated, and was introduced the possibility to employ collaborators up to a cost of €20,000. The tax rate remains at $5\%$ for the first five years, then increases to $15\%$. The nature of the transition from revenue to taxable income also changes: while under the minimum tax regime it was determined by deducting actual costs incurred, under the flat-rate regime it is established with percentages according to ISTAT classification[^9], with percentages ranging from $40\%$ for wholesale or retail trade, to $78\%$ for professions, and $86\%$ for construction and real estate activities. Therefore, deductions for costs (such as those for collaborators) are not allowed, other than social security contributions. With the 2023 Budget Law[^10] the revenue limit was raised to €85,000.

The aim of the parties (above all Liga) in the current government is to apply the flat tax to all self-employed workers; the next step is that of rising revenue limit to €100.000. In 2015 the purpose was that of encouraging the growth of self-employed, by offering permanent tax relief (provided that revenues remained within the established limit). Subsequent measures tended to implement the flat tax, with the aim of extending flat tax method to all economic operators (natural persons), as alternative to the progressive tax. Italy would be the first western European country to follow the proposal formulated by Milton Friedman (1962) and developed by Robert Hall and Alvin Rabushka (1981). Indeed, in 2023, before the revenue limit was raised to €85,000, almost 2 million tax payers have chosen the flat-rate regime.

Even some employee wages are taxed at fixed rates; in fact, the high marginal rates (as we will see later) make it make it convenient for both workers and employers to have the sums taxed outside personal income tax. For employees, from 2008, for incentive target, first with reference to overtime and subsequently (2016) with company and territorial productivity bonus agreements, a flat rate tax was established, with a rate of $10\%$ and from 2023 at $5\%$, for variable amount of performance bonuses; in theory, although the controls are not easy, payments are linked to "increases in productivity, efficiency and innovation". According to recent data from the Ministry of Labor, over 5 million workers currently benefit from bonuses, for total of approximately 7.5 billion. The sum is a relatively modest one, so that the Meloni's government is considering applying the flat tax to wage increases, thus making a significant step forward towards the flat tax; the only obstacle is the high cost of the measure.

### c) Evasion

Italy has been always characterized by tax evasion, as a country where the productive structure is composed by a high number of small businesses; according the National Institute of Statistics (ISTAT 2024) the average number of employees is 3.9. Self-employed workers make up $27.1\%$ of the total (almost doubling the European rate 15.9), percentage rising to 33.8 in Southern Italy. This fragmentation of production, combined with a centuries-old history of foreign domination, explains the high rate of evasion, distributed according to south-north gradient. The Report of Minister of Economic and Finance on the unobserved economy and on tax and social security evasion (2024) presents the weight on the added value of the unobserved economy by region: the highest percentages are found in the Southern Regions (led by Calabria with $19.2\%$ ), followed by those in the Centre, and finally those in the North (last being the Autonomous Province of Bolzano with $8\%$ ).

Regarding the personal income tax (Table III.1.1.1), evasion rates are obviously particularly high in the business and professional sectors, with a total value of 29.6 billion (something less than 33.3 billion in 2017). Compared to the potential tax and GDP, the percentages are 66.8 and 1.6 respectively. One might wonder whether the widespread use of the flat-rate regime has played a role in the 11 percent drop in evasion over the last seven years; the reduction in the burden of personal income tax, which is achieved by opting for the flat-rate regime, may have led to an increase in compliance, but since many operators have aimed to stay within the revenue limits (€85,000), there has been an inverse effect, increasing evasion.

### d) Tax Progressivity

At the time of the 1973 reform, the tax burden[^11] in Italy was about fifteen percentage points lower than that of countries like France, Germany, and the United Kingdom, and more than twenty percentage points lower than that of Scandinavian countries; after about twenty years, the gap had essentially closed, mainly thanks to the personal income tax (IRPEF).

Table 1: Tax Burden in Relation to GDP

<table><tr><td colspan="3">1975</td><td colspan="2">1995</td></tr><tr><td></td><td>Direct</td><td>Total</td><td>Direct</td><td>Total</td></tr><tr><td>France</td><td>5,6</td><td>35,4</td><td>7</td><td>42,9</td></tr><tr><td>Germany12</td><td>11,8</td><td>34,4</td><td>11,3</td><td>37,2</td></tr><tr><td>Italy</td><td>5,4</td><td>25,4</td><td>14,2</td><td>40,1</td></tr><tr><td>Spain</td><td>4,1</td><td>18,4</td><td>9,4</td><td>32,1</td></tr><tr><td>Swedan</td><td>20,2</td><td>52,7</td><td>18,9</td><td>48,1</td></tr><tr><td>U.K</td><td>15,8</td><td>35,3</td><td>12,8</td><td>34,7</td></tr></table>

The reason depends on the increasing elasticity of the tax (that is the ratio between marginal and average tax rate, also known as liability progression), which will be described now.

The overall level of progressivity is calculated by the Kakwani index, as difference between Gini index (which measures income inequality) and Tax Concentration Index, that is Gini index of tax distribution. The redistributive effect (Reynolds-Smolensky index) depends both on the value of the Kakwani index and on the weight of the income tax. According to Baldini (2020) redistributive effect in forty years has increased by 70.8[^13]; this strong increase is mainly due to the increase of the incidence of the tax $^{14}$ (58.6 percent) and only to a lesser extent to the greater progressivity (9.9 percent).

However, the nature of the tax's progressivity has completely changed over the past four decades. Initially, progressivity depended on tax brackets, while tax credits were very limited. Progressivity was therefore based on increasing tax rates; the ones that really mattered were the first ten brackets (rates 10-32), where 99 percent of taxpayers fell. Tax elasticity was on average 1,3.

Nowadays things have changed profoundly; according to a statistical analysis (Barbetta et al. 2018), more than half of the total PIT redistributive effect is due to the two most important tax credits (the tax credit for employment and the tax credit for retired people), while the marginal rates schedule contribution is about 40 percent. On the contrary, most of the itemized expenditures do not show any sizable impact on redistribution.

To explain this change in the factors influencing progressivity, we need to look at the inflationary process of the 1970s and early 1980s. The increase in IRPEF burden in two decades of the 70s and

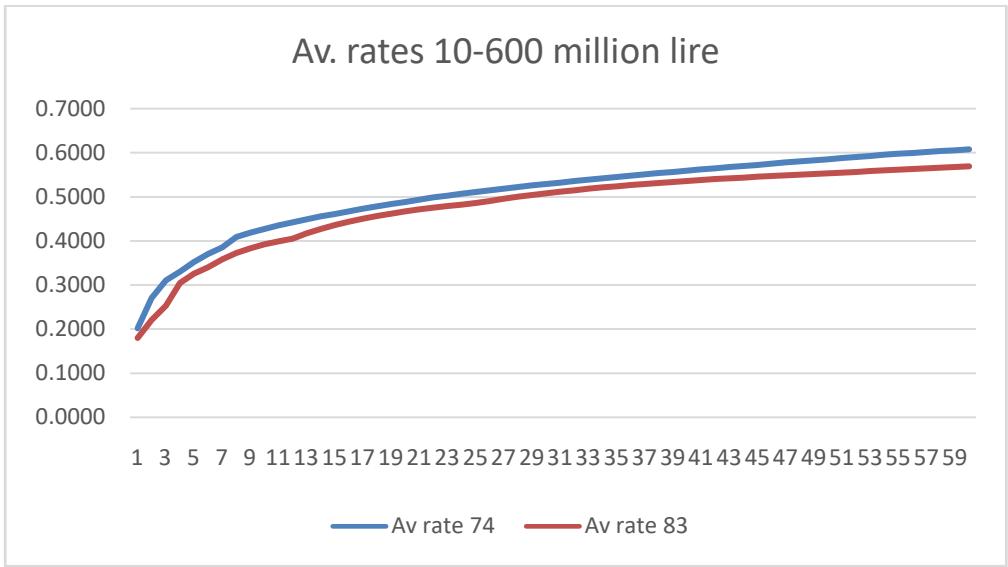

80s derives from the strong inflationary process and the high elasticity of the tax, producing a continuous process of bracket creeping. From 1973 to 1981 the annual rate of increase in prices was almost 17 (16,95) percent. In 1982, Prof. Bruno Visentini, a tax law scholar and Minister of Finance, carried out a transformation of IRPEF, reducing from 32 brackets to 9, raising the first one to 18, and reducing the last one to 65 percent.

The effect of the intervention on the tax brackets can be seen in Fig. 1, where on a large scale, the intervention consists of an almost uniform reduction in the tax rates.

Fig. 1: Brackets and Rates 1974-1983

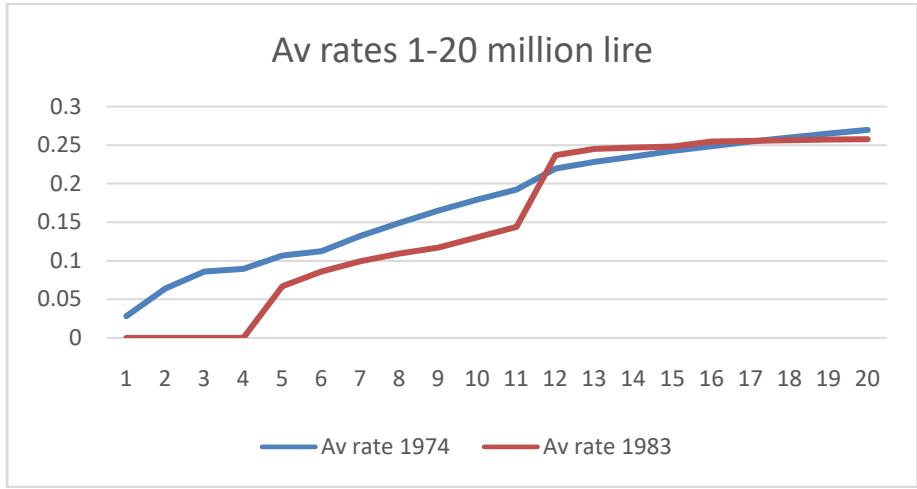

Visentini also introduced tax credits that were reduced in steps up to 16 million for employed workers and pensioners. Zooming in on low incomes, in fig. 2 we can see that the intervention aims to protect workers and pensioners with the lowest incomes. Due to budget constraints, it does make sense to try to protect the poorest.

Fig. 2: Role of Tax Credits

The main aspects in the following twenty years are two: I) tax brackets are reduced from 9 to 5, with the top rate dropping from $65\%$ to $45\%$; II) the system of depressive tax credits is made more complex. In

2001(last Prodi's law) the steps increased to twenty $^{15}$, with a significant tax credit increase (1,147 euro). It remains fixed up to revenue 6,197, then it halves (578), with ten steps, to 9,813[^16]; from 6,300 to 8.400 tax elasticity is on average 7.8, with deep oscillations.

The philosophy behind the intervention is always based on protecting and even supporting lower incomes; moreover, the budgetary costs made it impossible to completely eliminate the effects of inflation on average tax rates. Criticism of high marginal tax rates had led to a sharp reduction in the highest rates, even maintaining the idea of tax progressivity. In this way highest income earners get a benefit, while the middle classes had an increase in tax burden; the elasticity can be seen in fig. 3 below. However, compared to the formal rate of 18 percent of the first bracket, workers (who benefit an increase in their wage) could have a high probability of a reduction of the tax credit; so, depending on the increase in income, they could add an implicit marginal rate of 15 points or even more. From 9,813 to 51,646 probability of an implicit rate decreases because the intervals between one step and the next increase.

In this way, the new tax credit system increases the redistributive effect, despite the elimination of the highest marginal rates, because, next to official rates of the five brackets, we have to add implicit marginal rates due to decreasing steps. As we shall see, this paved the way for a continuous increase in tax elasticity.

### e) Implicit Marginal Rates

In 2003, the first phase of the Berlusconi government's reform came into force, with the declared ultimate goal of applying a flat tax to almost all (99%) taxpayers (with incomes up to 100,000 euros). Initially, however, the tax brackets and rates remained five, with the first two (which affected the majority of taxpayers) increasing from 18 to 23 and from 24 to 29 percent. A main innovation was the introduction of decreasing deductions from income, with a continuous formula and no longer in steps.

Taxable income (Ri) is generally defined as the remuneration for work (Y) minus the taxpayer's actual deduction (De):

$$

Ri = Y - De.

$$

The actual deduction, in turn, is calculated using the following formula:

$$

D e = D i ^ {*} (2 6, 0 0 0 + D i - Y) / 2 6, 0 0 0 \tag {2}

$$

$D_i$ is equal to 7,500 for employees, 7,000 for pensioners, 4,500 for the self-employed (businesses and professions), and 3,000 for pure rentiers. Looking at the formula, we note that the applicable deductions exempt from tax up to 7,500 and end at 33,500 for employees, exempt up to 7,000 and end at 33,000 for pensioners, and so on.

From (1) and (2) we get:

$$

R i = Y - D i * (2 6.0 0 0 + D i - Y) / 2 6.0 0 0 \tag{3}

$$

Looking at (3) we note that an increase in $Y$ of 100 euros determines has a greater effect on disposable income ( $Ri$ ), equal to 128.85 for employed workers, 126.92 for pensioners, 117.31 for self-employed workers and 111.54 for rentiers; to these increases is applied the tax rate of the bracket. But the identical result can be obtained by multiplying the formal rate by $Di/26,000$ and applying the result to the increase in $Y$. Thus, considering the first bracket, the marginal tax rate of the employed worker goes from 23 to 29.63, that of the pensioner from 23 to 29.19 percent. One could outline, alongside the structure with formal rates and decreasing deductions, a structure with fixed deductions for all (differentiated by category) and increased tax credit of 1,2885 (employees), 1,2692 (pensioners), and 1,1731 (self-employed). The results, in terms of net tax, are identical (Libro Bianco 2008) and they make explicit what might not seem so: that the true marginal rates have increased. The deduction certainly reduces the average rate, but, given its decreasing nature, it increases the marginal rate.

The lack of full awareness of new system implications can be seen in the lack of coordination between the limits of the brackets and those of deductions; the consequence is that the elasticity of the tax, in addition to increasing for low and medium incomes, presents significant oscillations, as it can be seen in the following Fig. 3. Overall, the elasticity of the tax, which measures the progressivity of the incomes involved, increases significantly.

Another news is the different treatment of employees and pensioners who previously received the same tax credits. The difference is certainly small, but, as we'll see, it will tend to increase in subsequent years.

In 2006 the second phase of tax reform reduced from five to four the brackets cutting the highest rate by two points $^{17}$, and extending the first bracket limit from 15,000 to 26,000. In this way, low-middle and high-income taxpayers received a noticeable tax reduction, while, for those between 26,000 and 70,000, the reduction was symbolic.

Deductions for spouses and children are also made depressive with respect to income, unlike tax credits which were fixed. Further implicit marginal rates were then added to those introduced with first phase; even in this case average rates fell and marginal ones rose, determining an increase in tax elasticity.

The 2007 Prodi government went back to five brackets, similar to Berlusconi's first phase (2003), but leaving the highest rate at $43\%$. However, the new bracket structure resulted in a tax increase for all taxpayers; an increase of 2,490, peaking at 101,000 and then remaining constant.

The tax increase was offset for employees up to approximately 40,000, and slightly less for pensioners and self-employed workers. Deductions were replaced by tax credits, these too declining. The shift from deductions to tax credits made the implicit marginal tax rates more evident; for example, for employees in the first bracket (up to 15,000), the effective rate is 23 (formal rate) plus 7.14, since the credit is reduced by 7.14 every 100. In the second bracket (up to 28,000), we have $27 + 3.34$, and in the third (up to 55,000) 38plus 3.34; in both cases, the credit is reduced by 3.34 euros for every 100. The effective rates[^18] were 30,17 (I bracket), 30,34 (II bracket), 41,34% (III bracket), 41% (IV bracket), 43% (V bracket).

So even though there were formally five brackets, de facto one could say that for employees there were three brackets and rates. The tax credits determine, until they are cancelled at 55,000, an elasticity of the tax stronger than that determined by bracket rates.

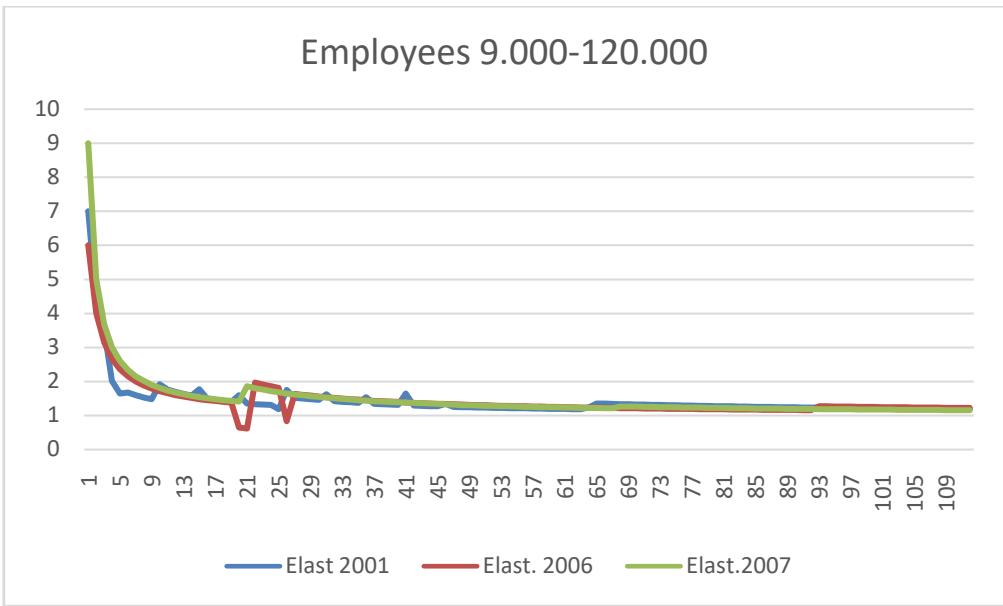

In fig. 3 Three Elasticities 2001-2003-2007 are Compared:

Fig. 3: Elasticities 2001-2007

Apart from some fluctuations, due to the tax credit steps in 2001, and the flaw $^{19}$ in the 2003 tax, the elasticities $^{20}$ are substantially overlapping.

Tax credits for spouses and children also reinforce the elasticity effect. In the following years IRPEF remained substantially stable, with slight increases in tax credits (resulting in a further increase in elasticity); this explains why more than half of IRPEF redistributive effect is due to the tax credits (Barbetta et al. 2018).

### f) The Last Ten Years

In 2014, Renzi's government introduced the "80 euro" bonus. Renzi had two objectives: The first goal was, for those receiving the bonus, to be able to see it on their monthly paycheck; the second was that the bonus was to be considered as a tax reduction rather than an increase in spending. To achieve this second objective, it was established that the bonus would be due, to those with a positive IRPEF (even just one euro) calculating the tax only with reference to the earned income. This was the case for a taxable income of at least €8,148, which triggered the bonus in full (if the individual had worked for the entire year). However, Eurostat-Istat noted that, in this way, the bonus cannot be considered a lower tax, but rather a transfer expense (hence an increase in public spending).

The cost budget, set at ten billion, imposed a limit on the bonus; here too, the preference was to ensure that the largest possible number of recipients received the full bonus; the result was that of imposing a very high implicit tax rate. The bonus is reduced to zero within the space of two thousand euros between 24,000 and 26,000, decreasing by 48 every 100. Adding the formal rate of 27 and the implicit rate of 4.51 of tax credit, the effective marginal tax rate, over the 2,000 range $^{21}$, ended up being 79.51 percent. More than a million workers, each year, who had received the bonus had to repay part (or even all) of it to the Revenue Agency.

A first attempt to resolve the anomaly occurred with the Conte $^{22}$ government (2020), when the bonus was transformed, for incomes from 28,000 to 40,000 into a new decreasing tax credit, adding to the previous one for employed workers. The 79.51 rate was indeed eliminated, but in the third bracket two new rates appeared (because of the new decreasing tax credit), 45.05 percent from 28001 to 35000, and 60.82 percent from 35,001 to 40,000; both rates were higher than the two rates of the fourth and fifth brackets (41 and 43); the anomaly had just been moved forward.

The problem was addressed by the Draghi government in 2022, reducing the tax brackets to four (eliminating the 55,001-75,000 bracket with a rate of $41\%$ ), and cutting the rates of the second bracket by two points (from 27 to 25) and the third by three points (from 38 to 35). To reduce the advantage[^23] to those with incomes above 55,000, the limit for the third bracket was brought forward to 50,000. Furthermore, the tax credit for employees (which the Letta government had raised from 1840 to 1880) was kept fixed up to 15,000, and the Renzi bonus was also limited to that income; From 15,001 it becomes a further tax credit which thus rises to 3,100, decreasing to 1,910 at 28,000 (with an implicit rate of 9.15) and finally reaching zero at 50,000 (with an implicit rate of 8.68). In this way, the slowing down of formal rates (second and third brackets), was compensated by the increase in the implicit rates due to the decreasing tax credits.

The IRPEF structure thus takes on a more regular form; the effective rate of the third bracket (28,000-50,000), equal to 43.68 (35+8.68), is slightly higher than that of the fourth (43); apart from this defect, one could speak of a three-brackets system, with the third starting at 28,001. However, the elasticity of the tax increases for low-middle income workers, being 13.85 at 15,000 and still 2at 29,000; it then drops to 1.39 at 50,000.

It happens that the two-year period 2022-23 was characterized by a high level of inflation (almost absent for many years), which in Italy determined, in the two-year period, a price increase of 15.1 percent. The sharp rise in the average rate determines an increase in tax pressure, leading Meloni's government to intervene by lowering the tax burden on low-middle income workers, thus also benefiting employers. It was clear that action had to be taken to balance the phenomenon of bracket creeping, particularly strong on low and middle incomes; reducing the tax burden was a way of lowering the workers pressure on employers.

An initial intervention (2024 budget law) introduced a reduction, in social security contributions for workers, which ended at salary 35,000, for budgetary reasons. In this way once this threshold was exceeded, a loss of over 1,000 was incurred.

The next budget law (2025) introduces a significant change: the previously introduced relief on employee's contributions has been abolished and replaced by a new bonus, with three decreasing percentages: 7.1 up to 8,500, 5.3 up to 15,000, and 4.8 up to 20,000. This bonus too is considered a monetary transfer that accompanies, but is not formal part of, the tax structure, like the previous Renzi's bonus. Above 20,000, there is an additional tax credit of €1,000, which remains constant up to €32,000 and then decreases linearly to €40,000. This new tax credit solves the problem of the previous intervention; however, it is easy to understand that, within the second formal bracket, a new decreasing deduction with an implicit rate of 12.5 percent (1.000 in the space of 8.000) was added.

Therefore, in 2025, considering the personal tax plus the two bonuses, brackets and rates (of which the first is negative) for employed workers are not three but eight (with the first rate negative):

Table 2: Effective Bracket to Employees

<table><tr><td>Tax Bracktes</td><td>Rates</td></tr><tr><td>-8,500</td><td>-7.1</td></tr><tr><td>8,501-15,000</td><td>17.7</td></tr><tr><td>15,001-20,000</td><td>27.35</td></tr><tr><td>20,001-28,000</td><td>32.15</td></tr><tr><td>28,001-32,000</td><td>43.68</td></tr><tr><td>32,001-40,000</td><td>56.18</td></tr><tr><td>40,001-50,000</td><td>43.68</td></tr><tr><td>Over 50,000</td><td>43</td></tr></table>

As far as pensioners and self-employed workers are concerned, the situation has not changed since Draghi's intervention:

Table 3

<table><tr><td colspan="2">Pensioners24</td></tr><tr><td>Brackets</td><td>Rates</td></tr><tr><td>0-8,500</td><td>23</td></tr><tr><td>8,501 – 28,000</td><td>29,44</td></tr><tr><td>28,001-50,000</td><td>38,18</td></tr><tr><td>Over 50,000</td><td>43</td></tr><tr><td colspan="2">Self employed25</td></tr><tr><td>0-5,500</td><td>23</td></tr><tr><td>5,501 – 28,000</td><td>26,4</td></tr><tr><td>28,001-50,000</td><td>37,27</td></tr><tr><td>Over 50,000</td><td>43</td></tr></table>

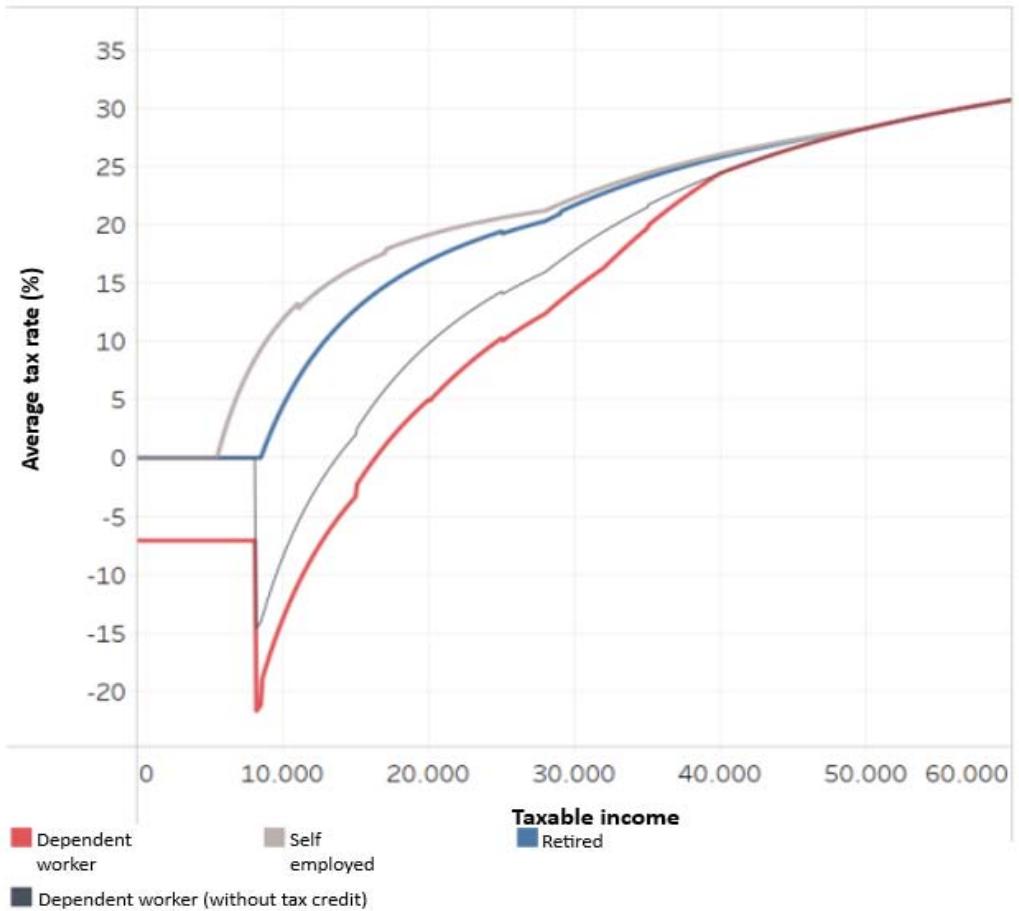

Progressivity has certainly increased, but the use of diversified decreasing tax credits has led to an excessively accentuated differentiation between employed workers and all other tax payers. Only after 50,000 taxpayers of any type find themselves paying the same tax.

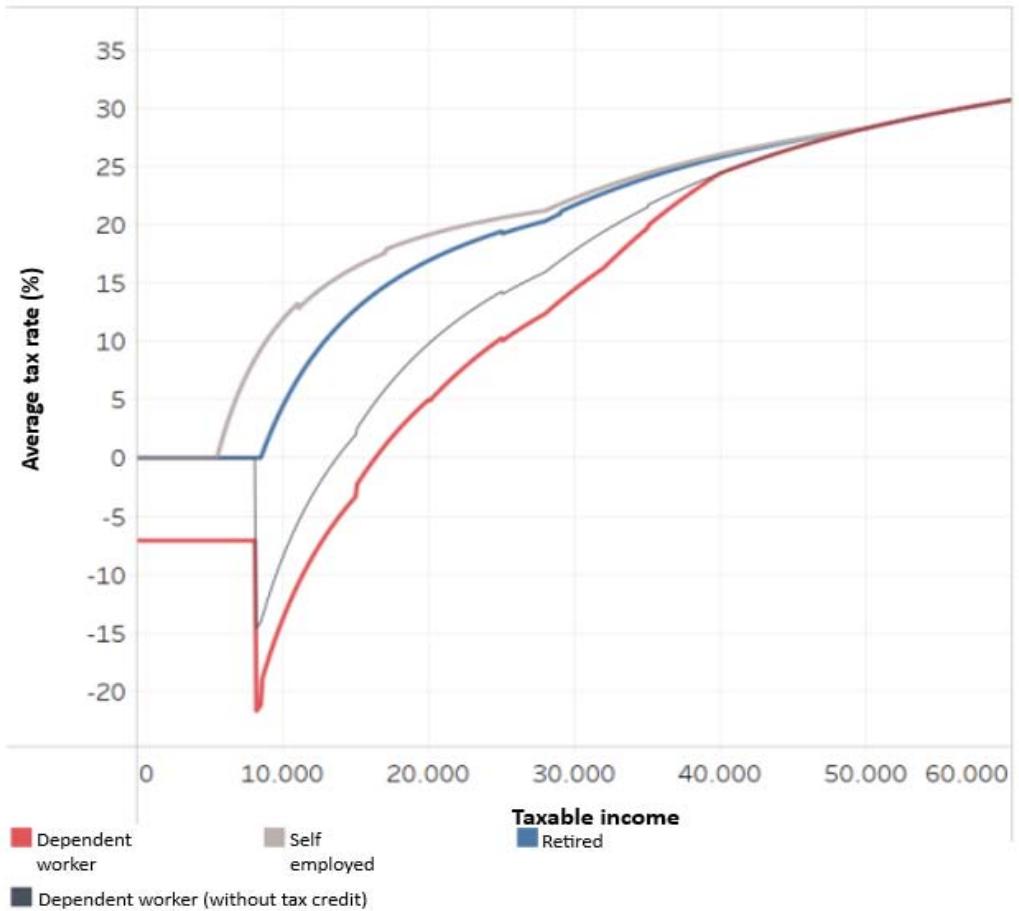

As shown in Fig. 4 (Parliamentary Budget Office UPB 2024), the average rates of employees and pensioners, in about twenty years, have diversified a lot; only after 50,000 taxpayers $^{26}$ of any type find themselves paying the same tax. To a lesser extent the same applies to the difference between pensioners and self-employed workers $^{27}$. The result is that only a small minority of taxpayers has the same personal income tax; all the others have de facto different tax regimes.

Fig. 4: Average Rates 2025

Source:UPB (2094),fig.4.5,p.82.

As far as employees are concerned, from the level of 9,000 euros, where the (negative) rate reaches its lowest level (i.e., the largest benefit to the worker), a rapid increase begins, making the tax elasticity very high; up to 40,000, it remains above 2, then declines first slowly (at 50,000, the elasticity is 1.54, still quite high) and then more rapidly (at 100,000, the elasticity is 1.21). Essentially, IRPEF, particularly with regard to employees, has become a highly progressive tax on low- and middle-income earners, where over $90\%$ of taxpayers live.

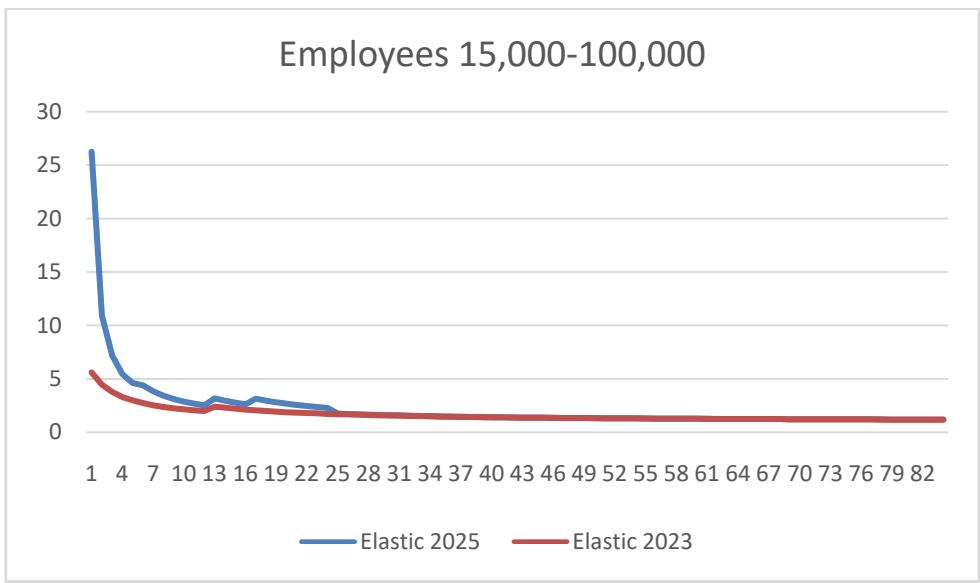

Fig. 5: Elasticities 2023-2025

As can be seen, the elasticity $^{28}$ in 2025 (Meloni) is clearly higher than that in 2023 (Draghi) up to 40,000, but even after that it remains slightly higher.

The decreasing tax credit method determines a reduction in the average rate, but, at the same time, it increases the marginal rate. All this paves the way for a further effect of brackets creeping: from 2021 to 2024 IRPEF increased by 28 percent. Of course, the two-year period 2022-23 was characterized by high inflation, but even with moderate inflation (2-3 percent), after a few years, taxpayers, especially employees, with incomes up to 50,000, find themselves[^29] suffering from an increase in tax pressure.

In conclusion, we can ask ourselves what went wrong. We can distinguish three periods: in the first, an attempt was made to limit the increase in tax pressure, especially on low incomes, as there were not the resources to eliminate the effect of inflation on all incomes. In a second period motivations were more strictly political, also connected with the hypothesis of a flat tax, while in more recent years need to protect poor and middle classes workers from inflation has emerged again, thus easing the pressure on employers.

### g) Tax Reform Proposals

Fifty years ago, IRPEF had thirty-two brackets with rates ranging from 10 to 72 percent. In the current year the (formal) rates are three, ranging from 23 to 43 percent[^30]. However, the intensity of progressivity cannot be inferred from the number of rates; as we have seen, progressivity has increased for most taxpayers, thanks to decreasing tax credits. These effectively create four brackets for pensioners and the self-employed, and eight brackets (considering two bonuses that are closely linked to the IRPEF structure). However, the strong elasticity determines a self-perpetuating process: to tone down bracket creeping, further increases in tax credits are necessary, always decreasing in relation to income; in this way average rates lower but not marginal rates, thus further increasing tax's elasticity.

In November 2021, the Draghi government presented a law for tax reform. Regarding direct taxation a dual system is proposed: income from work is subject to personal income tax (IRPEF), while income from wealth is subject to a single tax that would treat all the various taxes on capital income uniformly. These would be reduced to two: an existing one, tax on corporate income (IRES), and a second one that would unify the taxation of income from capital owned by individuals, currently subject to various taxes.

The law, after outlining the dual system, establishes that income from employment (and pensions) will be taxed in personal income tax (IRPEF), including that of self-employed workers (for the part related to the remuneration of work). Although not explicitly stated (for obvious reasons of political prudence), this would have entailed the elimination of flat-rate system for VAT-registered individuals (self-employed) and of separate taxation of productivity bonuses.

The main objectives are illustrated in the report of the Minister of Economy and Finance Daniele Franco (an expert of public economy). After stating that the revision must respect the principle of progressivity, offers two recommendations: "1) gradually reduce the average effective tax rates resulting from the application of personal income tax, also to incentivize labor supply and labor market participation, with particular reference to young people and second-income earners, as well as entrepreneurial activity and the disclosure of taxable income; 2) gradually reduce excessive variations in the marginal effective tax rates resulting from the application of personal income tax." The 2022 personal income tax reform had moved in this direction, but it had small effects on the elasticity of the tax, since the latter depends on the ratio between marginal and average rates. The excessive variations in marginal rates had been reduced, but the reduction in average rates offset the effect, maintaining high tax elasticity.

To understand the caution towards any proposal that could be perceived as a tax increase, it is worth emphasizing an interesting point of the proposed law concerning real estate registry; it is well known that, in Italy, cadastral revenue values differ from market values, as recorded by the Revenue Agency's Real Estate Market Observatory. Generally speaking, the older the property, the greater the discrepancy; overall, actual values are double the cadastral values, but with very marked fluctuations. Reconstructing the values and related incomes had long been necessary; it was therefore particularly appropriate to bring the cadastral values closer to market values.

However, since the government was aware of the extreme political sensitivity on the issue, the law declared that until 2026 "the provision that the information collected according to the above-mentioned principles will not be used to determine the tax base of taxes whose application is based on land registry results and, in any case, for fiscal purposes." Essentially, it proposed to implement an adjustment to the Land Registry but to postpone any potential tax consequences for five years, and therefore to another legislation. Consequences which are inevitable, not only for local taxes (IMU), but also if one wanted to move towards the dual system proposed by the reform.

The proposed reform law expires with the advancement of the general elections in 2022, due to the fall of Draghi's government.

# h) A Continuous Tax on Earned Income

For a long time, from 1926 to 1973, Italy had a continuously progressive tax system: the Progressive Complementary Income Tax. The tax was imposed on a minority of income earners, starting from those who earned above-average incomes. As we have seen, the personal income tax (IRPEF) instead adopts the model, with numerous brackets, typical of Anglo-Saxon and Scandinavian countries; however, there was the exception of Germany (then federal). The continuous function is applied for the majority of Einkommensteuer taxpayers up to 67,000[^31]; this is because the marginal tax rate grows linearly, and therefore too quickly. Sotwo different (quadratic) functions are applied, before moving on to a two brackets system for the highest income earners. Diana Estevez-Schwarzand Eric Sommer (2018) instead propose a single function that has a zero marginal tax rate at zero income, and a rate that tends to a finite value as the taxpayers' income increases.

The simplest form is the fractional function; it has two parameters: the tax rate $a$ toward which the tax incidence tends (to infinity $^{32}$ ) and $K$, a parameter on which the curvature of the average and marginal tax rates depends. Since $Y$ is income, the average tax rate (tav) is given by the function

$$

\operatorname{tav} = \mathrm{a Y} / (\mathrm{K} + \mathrm{Y}) \tag{1}

$$

while the marginal tax rate (tma) is

$$

\mathrm{t m a} = \operatorname{tav} (2 \mathrm{K} + \mathrm{Y}) / (\mathrm{K} + \mathrm{Y}) \tag{2}

$$

For example, if $a = 0.45$ and $K = 30,000$, both the average and marginal tax rates start at zero. As income increases, the marginal rate increases more rapidly, but the difference with the average tends to decrease because $K$ remains constant while $Y$ increases. The tax elasticity reaches 1.71 at €6,000, then slowly begins to decrease. These are more reasonable values than the exaggerated ones caused by decreasing tax credits.

At the Following Four Income Levels, we have:

Table 4

<table><tr><td></td><td>Average Rate</td><td>Marginal Rate</td><td>Elasticity</td></tr><tr><td>15000</td><td>15</td><td>24.5</td><td>1.65</td></tr><tr><td>30,000</td><td>22.5</td><td>33.6</td><td>1.49</td></tr><tr><td>60,000</td><td>30</td><td>39.9</td><td>1.33</td></tr><tr><td>120,000</td><td>36</td><td>42.2</td><td>1.19</td></tr><tr><td>240,000</td><td>40</td><td>44.4</td><td>1.11</td></tr></table>

However, this function does not take into account the necessity of a minimum exempt level. Currently, as we have seen, employees are exempt up to 8,500 euros, having a deduction of 1,955 and a tax rate of 23 percent. But the continuous function (as described) at 8,500 has a rate of 9.94, much lower than the current IRPEF rate. Therefore, a (fixed) deduction of 845 euros would be sufficient to obtain the same level of exemption. Certainly, in this way, elasticity at low-income levels[^33] increases significantly, as the marginal tax rate remains unchanged, while the average rate decreases. However, the decrease quickly attenuates, and the elasticity falls below 2 at 21,000.

The fixed tax credit would be the third parameter of the fractional function indicated by Estevez Schwarz-Sommer (2018), which instead opt for a fixed deduction. The difference consists in the reduction not only of average rates but also of marginal ones. By setting the exemption at 8,500, the tax elasticity remains high, dropping below 2 only at 38,000. In this way, allowing diversified deductions for employees, pensioners and self-employed, we would not have a single function, but three distinct functions, although much less than in the current situation.

### i) Dual System on Labor Income

In a dual system, the taxable base for personal income tax would consist not only of earned income, but without exceptions. Therefore, as mentioned, the flat-rate regime for self-employed people should be abolished. However, in individual businesses or partnerships, income derives not only from the work performed, but also from the capital employed; this component should be separated to identify only earned income. Even in some professions, such as medicine, professionals' work requires the use of expensive equipment and tools.

If leasing is used, this problem does not arise, as the financing cost is deductible. However, in the case of owned capital, the value of the appropriate rental fee (for the business or a branch of a business) should be determined by a rate of return on business capital. The value of the capital is estimated using various methods to arrive at an adjusted net worth, to which unaccounted intangible assets (typically goodwill) are added. The value (or its return) will be subject to taxation under the other tax of the dual system, the tax on capital gains (directly or indirectly).

Self-employed workers often complain about the uncertainty of their jobs and the risks of illness, arguing that the progressive nature of the tax is detrimental to them; this is one of the arguments in favor of the flat tax. However, a response to these real concerns was provided long ago by William Vickrey (1939, 1947) with the proposal of a cumulative average that, based on income trends over time, recalculates the tax due by averaging the income stream. The proposal has never been fully implemented, except in a rather limited way for the carry-forward and carry-back system.

Among the characteristics of a tax system, one of the most important should be respect for horizontal and vertical equity. Article 53 of the Italian Constitution consists of two statements; the first says that "Everyone is required to contribute to public expenditures in proportion to their ability to pay." This implies that, with equal ability to pay, two people should pay the same amount of tax (horizontal equity). The second states that "The tax system is based on progressive criteria"; therefore, as the ability to pay increases, the tax should increase more than proportionally (vertical equity).

Economists and jurists have long debated how to define the ability to pay (Adam Smith). It has also been argued that vertical equity conflicts with productive efficiency $^{34}$ (Hall-Rabushka, 1981) and should therefore give way to the latter (introducing instead a flat tax, the stated objective of tax reform of Meloni government). There is no doubt, however, that our tax system is far from respecting both horizontal and vertical equity. Personal income tax (IRPEF) is now composed of three distinct tax systems with different average and marginal rates, in addition to a fixed rate on the notional income of many self-employed individuals.

In the previous pages, we've seen how our main tax, created precisely to implement the two aforementioned criteria, has changed radically; from a structure of equal rates for all taxpayers, with minimal differentiation, we've moved to separate structures. From a progression based on increasing marginal rates, we've moved to a system in which there are only three marginal rates, and progressivity, for most taxpayers, is provided by decreasing tax credits, which introduce implicit, differentiated rates; one for retirees and self-employed and five[^35] for employees. It is therefore necessary to return to a unique tax that applies to all income from work, respecting the two principles of horizontal and vertical equity, with a more moderate progressivity on low and medium incomes, and a more accentuated one on high incomes.

[^3]: At the end of 1998 the euro-lira exchange rate was set at 1936.27 lire for one euro. _(p.1)_

[^4]: How this happened is worth telling. The law established that the list of taxpayers, resident in each area, was to be displayed in the municipal offices; when this happened, the first to consult the lists were, obviously, journalists. They discovered, with some surprise, that well-known car manufacturer, like Gianni Agnelli, was not at the top of the list in Turin, nor Alberto Pirelli, car tires and cables, in Milan. _(p.1)_

[^5]: So called "prima casa" (first home). _(p.2)_

[^6]: $^{6}$ Future Minister of Finance in 1996 Prodi's government and Deputy Minister of Economy and Finance in 2006 Prodi's government. _(p.2)_

[^7]: In the 2023 tax return, 54 percent of more than 3.5 million self-employed workers. _(p.2)_

[^9]: Classification of economic activities ATECO Code. _(p.2)_

[^10]: Meloni's government first budget law. _(p.2)_

[^11]: Direct and indirect taxation plus social contributions. _(p.3)_

[^13]: From 0,0253 to 0,0432. _(p.3)_

[^16]: From 9,813 tax credits decrease more slowly up to 51,646 with a remaining credit of 50. _(p.5)_

[^18]: A similar conclusion applies to pensioners. Note that the fourth bracket had a slightly lower rate than the third, which is not entirely appropriate. _(p.6)_

[^23]: Reduction from 960 to 270. _(p.7)_

[^29]: Of course, even all other taxpayers over 50,000 suffer the effects of inflation, but in a more attenuated way, since the increase in average rate is smaller. _(p.10)_

[^30]: The intermediate rate of 35 percent will drop by two points from 2026. _(p.10)_

[^31]: Above 67,000 two brackets apply with rates of 42 and 45 percent. _(p.11)_

[^33]: For low-income workers it is advisable to combine the IRPEF with an incentive tool such as Earned Income Tax Credit (EITC) replacing the two bonuses currently in force. _(p.11)_

[^35]: Five if the two bonuses are considered strictly linked to IRPEF, as is in fact more logical, otherwise in any case three. _(p.12)_

[^1]: Imposta di Ricchezza Mobile (Mobile Wealth Tax). _(p.1)_

[^2]: Imposta Complementare (Complementary Tax). _(p.1)_

[^8]: With the exception of employees undergoing redundancy, but in this case the regime was only valid for five years. _(p.2)_

[^12]: West Germany. _(p.3)_

[^14]: That is the ratio of total tax revenue to GDP. _(p.3)_

[^15]: Twelve for self-employed. _(p.4)_

[^17]: Since 2005, the $43\%$ rate has remained unchanged, making it one of the lowest rates in Western European countries. _(p.5)_

[^19]: From 29,000 to 34,000. _(p.7)_

[^20]: Both drop below 1.5 after 40,000. _(p.7)_

[^21]: Later moved from €24,600 to €26,600, which did not change the nature of the problem. _(p.7)_

[^22]: Called Conte 2, because the new government, with the same prime minister, was supported by the Democratic Party and not by the League (this party supported Conte 1, 2018-2019). _(p.7)_

[^24]: Second bracket implicit rate 6.44, third 3.18. _(p.8)_

[^25]: Second bracket implicit rate 3.28; third 2.2. _(p.8)_

[^26]: 7 percent, according to 2023 Revenue Agency data. _(p.8)_

[^27]: Obviously, we're referring to those self-employed workers who remain in IRPEF; the majority now opt for the flat rate of $15\%$ (declaring a turnover not exceeding 85,000). _(p.8)_

[^28]: The interval considered starts from 15,000 because the elasticity 2025 at lower values is quite erratic with very high values. _(p.10)_

[^32]: At infinity, both tax rates tend to a. But since even Elon Musk does not have an infinite income, for all incomes marginal tax rate is higher than the average rate. _(p.11)_

[^34]: Moreover, the thirty years after the Second World War, known as the Thirty Glorious Years, had very high marginal tax rates. _(p.12)_

Generating HTML Viewer...

References

14 Cites in Article

M Baldini (2020). Redistribution and progressivity of the Italian personal income tax, 40 years later.

Guido Barbetta,Pellegrino Simone,Gilberto Turati (2018). What Explains the Redistribution Achieved by the Italian Personal Income Tax? Evidence from Administrative Data.

Estévez Schwarz,D. - Sommer,E (2018). Smooth Income Tax Schedules: Derivation and Consequences.

Friedman Milton (1962). Capitalism and Liberty.

Haig Robert,M (1921). the Federal income Tax.

R Hall,A Rabushka (1981). A Proposal to Simplify Our Tax System.

Libro Bianco (2008). l'imposta sui redditi delle persone fisiche e il sostegno alle famiglie (personal income tax and support for families).

Schanz George,Von Der Einkommensbegriff und die Einkommerstenergesetze.

Simons Henry,C (1938). Personal Income Taxation.

(2024). Establishment of Uganda's Parliamentary Budget Office and the Parliamentary Budget Committee.

Vickrey William (1939). Averaging of Income for Income-Tax Purposes.

Vickrey William (1947). Agenda for Progressive Taxation.

Visco Vincenzo (1984). RENZO PREDI, Un progetto per i materiali dell'Istituto delle Scienze; EZIO RAIMONDI, Scienze e Letteratura; ALBERTO PASQUINELLI, Epistemologia e storia della scienza; CARLO GENTILI, Il modello epistemologico dell' Institutum scientiarum et artium di Bologna; MARTA CAVAZZA, La Casa di Salomone ; VINCENZO PALLOTTI, Per una storia dell'Istituto delle Scienze; FRANCO FARINELLI, Multiplex GeographiaMarsili est difficillima: MAURIZIO MATTEUZZI, La matematica a Bologna nel secolo XVIII; GABRIELE BARONCINI, Alcune ipotesi sulla evoluzionedella cultura scientifica a Bologna nella seconda met del '600; SANDRA TUGNOLI PATTARO, L'eredit aldrovandiana;CARLO GENTILI, I musei Aldrovandi e Cospi e la loro sistemazionenell'Istituto; MASSIMO FERRETTI, Il notomista e il canonico; PIER LUIGI CERVELLATI, Palazzo Poggi e la Specola; ANDREA EMILIANI, Un modello museografico per i materiali dell'Istituto delle Scienze. CATALOGO DEI MATERIALI Tavola cronologica; ENRICO NO, La raccolta dei ritratti; LIVIA FRATTAROLO ORLANDI, IRENE VENTURA FOLLI, La biblioteca dell'Istituto delle Scienze; MARCO BORTOLOTTI, ALESSANDRO SERRA, La stamperia dell'Istituto e i dalla Volpe; FRANCO FARINELLI, Gli strumenti del dominio sul mondo; BRUNO SABELLI, STEFANO TOMMASINI, I materiali della storia naturale; GIORGIO DRAGONI, VINCENZO PALLOTTI, Strumenti, didattica e ricerca: la fisica sperimentale nell'Istituto delle Scienze;GIORGIO PEDROCCO, Gli studi di chimica all'Istituto delle Scienze di Bolognanel corso del XVIII secolo; VINCENZO BUSACCH, Le cere anatomiche dell'Istituto delle Scienze; MARCO BORTOLOTTI, Insegnamento, ricerca e professione nel museo ostetricodi Giovanni Antonio Galli; ENRICA BAIADA, ALESSANDRO BRACCESI, Astronomia e Istituto delle Scienze..

No ethics committee approval was required for this article type.

Data Availability

Not applicable for this article.

How to Cite This Article

Dr. Ruggero Paladini. 2026. \u201cFifty Years of Italian Personal Income Tax\u201d. Global Journal of Management and Business Research - B: Economic & Commerce GJMBR-B Volume 25 (GJMBR Volume 25 Issue B2): .

Explore published articles in an immersive Augmented Reality environment. Our platform converts research papers into interactive 3D books, allowing readers to view and interact with content using AR and VR compatible devices.

Your published article is automatically converted into a realistic 3D book. Flip through pages and read research papers in a more engaging and interactive format.

This paper examines the evolution of the personal income tax (IRPEF) over fifty years. It describes the evolution of progressivity, initially based on a bracket structure, while the current dominant role is played by decreasing tax credits, creating excessive elasticity for most incomes. Furthermore, over time, many incomes that were initially included in the IRPEF have been progressively excluded. The system requires a thorough overhaul; the proposals presented are based on the dual system, in which income from work and income from capital are classified under two different taxes. The bracket structure is substituted by a continuous function for all tax payers.

Our website is actively being updated, and changes may occur frequently. Please clear your browser cache if needed. For feedback or error reporting, please email [email protected]

Thank you for connecting with us. We will respond to you shortly.