Our principal objective is to implement a conditional CAPM that, in addition to the global market risk, specifies the level of market integration, evaluates exchange rate risk, and accounts for local market risk. To investigate the potential for portfolio diversification for foreign investors in this region by examining the impact of financial crises on the evolution of national markets in the MENA region’s financial integration with the global market as well as with the three selected developed markets, namely France, Great Britain, and the United State. In order to test a conditional version of De Santis and Gerard’s ICAPM by admitting a specification of a multivariate GARCH process, this line of research has used a particular methodology (MGARCH).

## I. INTRODUCTION

In modern portfolio theory and with the famous Markowitz theory (52), international diversification is an integral feature of international financial markets.

Any investor will certainly prefer investment opportunities that offer the most attractive prospects all else being equal, the rate of return taken in isolation is not sufficient to characterize an investment opportunity. It is also necessary to consider possible deviations of the rate of return from its expected value, which brings us back to the concept of uncertainty or risk.

Thus, several potential benefits have encouraged investors to internationalize their portfolios; risk reduction, performance improvement. However, these benefits are directly related to the nature of the financial market structures of the countries involved (Hasan and Simaan 2000).

In addition, several factors present an obstacle to the gains of international diversification. Thus, previous works have shown that the exchange rate risk and the political risk present major limits to the benefits resulting from the strategy of international diversification (Eun and Resnik (1987), Cosset and Suret (1995)).

Over time, and depending on the events that have occurred in the financial markets, particularly the incidence of financial crises, the debate has focused on the significant impact of these crises on international portfolio diversification strategies.

Indeed, the strong financial integration between financial markets constitutes a major concern for the investor in search of international portfolio diversification. Since, the direct consequence of financial interdependencies is the propagation of volatility on stock markets.

This transmission of volatility manifests itself in the instability of financial markets in the prices and returns of financial assets and in the levels of stock market indices.

In this context, the international investor is confronted with this risk, which presents a threat that prevents them from achieving their objectives in international diversification strategies.

This observation opens up a rich field of research, and several empirical works have taken into consideration the intensity of the changes that have hit the global financial system since the 1987 crisis.

The first line of research was conducted by Roll (1988) and Miniskey (1992) on this crash. Then other works examined the crises of emerging countries "the Asian crisis, the Mexican crisis" such as Karyoli and Stulz (1996), Schwebach et al (2002), they underlined the stake of the strategy of international diversification in a context revived by rather strong financial disturbances.

As a result, the second line of research studied the effectiveness of this strategy and evaluated the expected gains from international diversification.

Thus, the research focused on developed markets and especially on the emerging markets of East Asia, Latin America and Central Europe with studies by, (Middleton et al (2008), Robert G. Bowman, Kam Fong Chan and Matthew R. Comer (2010), Jacek Niklewski and Timothy Rodgers (2011) and Robert Vermeulen (2013).

The conclusion drawn from this strand of research is that with the growth of comovements between developed and emerging markets and the frequent emergence of financial crises that characterize East Asia, Latin America, and Eastern Europe, the investor should target other emerging markets that provide advantages in managing their portfolio.

Recently, the MENA region has been under the scrutiny of some works in order to measure the potential profit of diversification that it can offer to foreign investors, such as Abraham et al (2001), Simon Neaime

(2005,2012), Lagoarde-Segot et al (2007), Cheng et al (2010), Dağli, H et al (2012) and Balcilar, M et al (2015).

In our turn, in our empirical investigation, we are interested in eight MENA countries (Tunisia, Morocco, Egypt, Turkey, Jordan, Saudi Arabia, United Arab Emirates), three developed countries (United States, Great Britain and France) and the world market, with the objective of measuring the degree of integration of each MENA country in our sample with the world market and to answer the following question: For a foreign investor, are the MENA stock markets advantageous in terms of diversification gain in a context revived by crises?

To achieve this objective, a literature review on international diversification during financial crises will be presented in a first section, as well as an empirical study of the impact of the subprime crisis on MENA stock markets in terms of portfolio management performance which will be the subject of a second section.

## II. LITERATURE REVIEW

Roll (88) showed that during the crash 87 all stock prices of 23 global financial markets studied have sharp declines around $20\%$ per month, similarly the correlations between countries are mainly positive but moderate in size.

Minskey (1992) examined the same crisis by finding that the crash can have a major impact on the architecture of financial markets, he indicated that the crisis has sown the seeds of structural changes across international financial markets.

As a result, the studies of Longin and Solnik (95), Solnik (97), Karolyi and Stulz (1996), Kronor and Ng (1998) Groslambert (2000) have highlighted the increase in correlations of stock market indices during periods of crisis marked by a strong movement of volatility.

Garnaut (1998) argued that the Asian crisis had a major structural impact on the financial architecture of the region through the increase in the degree of correlations.

Schwebach et al (2002) confirmed this result and indicated that correlations between countries increased from 0.18 to 0.274 during the first phase of the crisis and from 0.451 to 0.531 during the second phase, the same results are also affirmed by Bekaert et al (2005).

All these results call into question the effectiveness of international diversification strategy.

Thus, Wan-juin Paul chiou (2008) examined the comparative benefits of international diversification through the analysis of the indices of 21 developed countries and 13 developing countries over a period from January 1988 until December 2004.

To properly assess the gains of international diversification, two simple measures are used, the increase in the risk-adjusted premium by investing in the maximum risk-adjusted return portfolio and the reduction in volatility by investing the minimum variance portfolio on efficient international frontiers.

The empirical results suggest that investors in less developed countries, particularly East Asia and Latin America, benefit from regional and international diversification more than those in developed countries. The study found that the absolute values of the gains are reduced over time due to the integration and financial crises of the international financial market.

However, (Middleton et al 2008) they showed that the opportunities to invest in emerging markets of Central Europe are still significant, even in times of financial crisis.

Lagoarde-Segot, T et al (2009) tested the contagion between the G7 markets through the study of stock market linkages in order to identify the benefits of international diversification, their results show that during periods of turmoil the interdependence is increased but despite this context the benefit is still there for fund managers in these markets, it seems to be robust to strong changes in volatility

Robert G. Bowman, Kam Fong Chan, and Matthew R. Comer (2010) examined the response of global equity markets to the 1997 Asian crisis. The study included 39 countries a portfolio of 17 emerging countries, and a portfolio of 22 developed countries.

Jacek Niklewski and Timothy Rodgers (2011) sought to answer the crucial question of whether the changes in financial market architectures caused by the global financial crisis have had a permanent impact on international diversification? As such, they sought to examine the conditional correlations between U.S. equity markets and a number of developed, emerging and frontier markets.

Vermeulen Robert (2013) empirically examined during the period of 2001 to 2009, the portfolios of international investors before and during the global financial crisis for 22 countries. The results indicate that during the crisis international investors rebalanced their portfolios towards the less correlated markets.

the diversification where investors manage to hang less correlated stocks when the market situation is very volatile.

However, the question of expected gains from international diversification remains understudied for certain regions such as the Middle East and North Africa: MENA.

Some works have explored this area in order to identify for the international investor the existing opportunities to diversify his portfolio on these markets.

Indeed, Ali F. Darrat et al (2000) examined the degree of integration of three stock markets: Morocco, Jordan and Egypt, using the causality tests of Granger (69) and the cointegration tests of Johnson (88).

They showed that these emerging countries are globally segmented and regionally integrated which means that these studied MENA markets offer diversification potential for international investors.

Abraham et al (2001) selected three oil-producing markets in the Gulf region for a period from 1993 to 1998, with the aim of assessing the substantial benefits of diversification in these markets.

Indeed, using the mean-variance paradigm of Markowitz (59), they highlighted a low correlation of returns between these markets studied and the They indicated that the allocation of funds can be extended up to $(20 - 30\%)$ into the U.S. equity markets, which offers an important opportunity for investors to integrate securities from these markets into their portfolios to enhance returns and reduce risk.

They indicated that the allocation of funds can be extended up to (20-30%) in the stock markets.

In (2003), Assaf selected six Middle Eastern stock markets: Bahrain, Kuwait, Oman, Saudi Arabia and the Emirates, similarly Hassan et al studied ten markets in this region and this was to examine the correlations between these markets.

They pointed out that the benefit of diversification is significant; some markets have low correlation with others and thus may be a better choice to reduce the risk of a regional investment portfolio.

Simon Neaime (2005) examined the integration of seven MENA markets with each other and with major global stock exchanges. Johnson's cointegration tests indicate that the GCC (Gulf Cooperation Council) stock exchanges still offer international investors potential for portfolio diversification.

Thomas et al (2005), using the cointegration method to examine the financial structure of the MENA region and their implication on international portfolio management, showed that the long-term correlation of these markets with the European as well as the US market is not stable. This indicates the existence of an opportunity to diversify the asset portfolio for the three categories of investors.

In (2007), the same authors examined the issue of international diversification this time on seven stock markets in the MENA region "Morocco, Tunisia, Egypt, Jordan, Lebanon, Turkey and Israel".

They constructed international portfolios in both dollars and local currencies for a period from 1998 to 2006, their results highlighted the presence of remarkable diversification benefits in the MENA region.

Cheng et al (2010) studied the return behavior of nine stock markets in the MENA region namely "Bahrain, Egypt, Israel, Jordan, Kuwait, Morocco, Oman, Saudi Arabia, and Turkey" by using different variants of CAPM.

They conducted a comprehensive empirical analysis on the dynamics of returns and risk in the MENA region, overall they found that the markets of Turkey and Israel are the most integrated with the global market, their results suggest that investing in most of the Arab markets in the MENA region for the period of study provides uncorrelated returns with the global market, thus an opportunity of profit by exercising international diversification in these markets.

Mansourfour et al (2010) divided the MENA region into two groups "oil producing countries" and non-oil producing group, in order to examine the role of each group in the benefit presented to international investors in terms of international diversification.

The results of this study indicate that oil-producing countries offer more advantageous opportunities for international portfolio diversification than the countries in the second group

However, during the global financial crisis in 2008 the returns in these markets collapsed.

Neaime (2012) in this study the author analyzed the impact of the global financial crisis 2007-2008 on the emerging markets of the MENA region, through the examination of financial linkages between the markets of the MENA region and the most developed financial markets as well as the intra-regional linkages between the financial markets of the MENA countries among themselves.

Thus, through a detailed examination of financial integration in seven stock markets in the MENA region namely: Egypt, Jordan, Morocco, Tunisia, Kuwait, Saudi Arabia, and the Emirates with France, Great Britain, and the United States, while taking into consideration the volatility in these markets as well as the phenomenon of contagion during the period of the financial crisis, Simon Neaime showed that the stock market of Saudi Arabia is the market least affected by the global financial shock and still offers opportunities for portfolio diversification, while the markets of non-oil producing countries offer less opportunities for diversification.

Michael et al (2013) took by study the stock market comovements of the MENA region; "Egypt, Jordan, Saudi Arabia, Kuwait, Quater, Emirates" with the US market and between them for a period of 9 years from 2002 to 2010.

The results show that there is a modest degree of correlation between the MENA region and the U.S. market which implies opportunities for diversification in the near term.

Houseyin et al (2013) conducted an empirical study on emerging markets in Europe, the Middle East and Africa to identify the benefits of international diversification among the markets of the Czech Republic, Egypt, Hungary, Morocco, Poland, Russia, South Africa and Turkey.

Using, Johansen's (1988) cointegration tests for a period from 1994 until 2010, they showed the existence of cointegration relationships between most of these markets with a finding that the benefits of portfolio diversification in these markets are limited for investors.

Mehmet Balcilar et all (2015) examined the opportunities for international diversification in the stock markets of GCC countries, some countries show segmentation with the global market during periods of disruption and thus can offer diversification opportunities despite the crisis environment.

Mouna Boujelbene et all (2015) conducted an empirical investigation on developed and emerging Islamic stock markets "European, Asian, North American, MENA and Latin American markets, with the aim of examining the benefits of international diversification during quiet and disruptive periods.

Their study using the multivariate cointegration test highlights that Islamic stock market movements are partially segmented, in addition the level of integration between markets tends to change over time especially during periods characterized by financial crises.

Their results suggest that Islamic Shariahcompliant assets may offer potential diversification benefits, a finding that has important implications for the design of investment strategies for investors who wish to diversify their portfolios especially during periods of crisis.

In sum, the works that are interested in the study of the dynamics of the gains expected from international diversification as a function of integration, they have ignored the exchange rate risk, in other words, they have assumed that investors do not hedge their exposure to exchange rate risk, so that the price of exchange rate risk is equal to zero, as is the price of local market risk "Giovannini and Jorion (89), Harvey (91), Chan et al.

The same approach was adopted by the works that considered the effect of financial crises "Roll (88), Rahm and Yung (94), Hamao et al (90), Arrouri and Jawadi (2011), Kenourgios et al (2011).

In addition, according to the literature review presented on the issue of international diversification for stock markets in the MENA region, we can see that the period of study is always short, the results of work are heterogeneous and fail to decide between the existence or nonexistence of opportunities for international diversification on the MENA region.

Also, the basic model; "the model of De Santis and Gerard (97)" which was adopted by the majority of previous works to identify the gains of international diversification is based on the assumption of perfect financial integration, however the reality on the financial markets that they are in a situation of partial segmentation, and this after the previous works of Bekaert and Harvey (95,97), Karolyi and Stulz (2002), Dumas et al (2003), Bar and Pristley (2004).

## III. METHODOLOGY

Our contribution at this stage consists in applying a conditional CAPM that takes into account in addition to the global market risk; the specification of the degree of integration of the studied markets, the assessment of the exchange rate risk as well as the local market risk. In order to study the effect of financial crises on the evolution of financial integration of national markets in the MENA region with the global market as well as with the three selected developed markets namely France, Great Britain and the United States and thus to examine the possibilities of portfolio diversification for international investors in this region.

So the methodology adopted for this line of research consists in testing a conditional version of MEDAFI of De Santis and Gerard (97), by admitting a specification of a multivariate GARCH process (MGARCH).

# a) The Dynamic Version of CAPM

In a context of perfect financial integration in the financial markets and with the PPP hypothesis verified, the international extension of the CAPM of Sharpe (64) and Linter (65) presented by Adler and Dumas (83), Solnik (77), Stulz (81), De Santis and Gerard (97) and others, can be written as follows

$$

E \left(R _ {i t} / \Psi_ {t - 1}\right) - R _ {f t} = \beta_ {i m, t - 1} \left[ E \left(R _ {m t} / \Psi_ {t - 1}\right) - R _ {f t} \right]; \forall i

$$

$$

\text{With} \beta_ {i m, t - 1} \equiv \frac{\operatorname{cov} \left(R _ {i t} , R _ {m t} / \Psi_ {t - 1}\right)}{\operatorname{var} \left(R _ {m} / \Psi_ {t - 1}\right)} \tag{2}

$$

This is the variable sensitivity of security $i$ to the market portfolio $m$.

- $R_{it}$: The variable profitability of security $i$ between (t-1) and t

- $R_{ft}$: The return on the risk-free asset between (t-1) and t..

- $R_{wt}$: The return on the global market portfolio between (t-1) and t.

All expectations are made conditional on the information vector available at time t-1.

Equation (1) can be rewritten as follows:

$$

E \left(R _ {i t} / \Psi_ {t - 1}\right) - R _ {f t} = \delta_ {m, t - 1} \operatorname{cov} \left(R _ {i t}, R _ {m t} / \Psi_ {t - 1}\right) \forall_ {i} \tag{3}

$$

$$

\text{With} \delta_ {t - 1} \equiv \frac{E \left(R _ {m t} / \Psi_ {t - 1}\right) - R _ {f t}}{\operatorname{var} \left(R _ {m} / \Psi_ {t - 1}\right)}

$$

This is the world market covariance risk price over time.

Relationship (3) is the most widely used formulation in empirical asset pricing work, and implicitly assumes that financial markets are integrated in a way that the market risk price equals zero; investors are not exposed to currency risk.

Implications for international portfolio diversification.

$$

E \left(R _ {I t} / \Psi_ {t - 1}\right) - R _ {f t} = \delta_ {m, t - 1} \operatorname{cov} \left(\theta_ {t - 1} R _ {m t}, R _ {m t} / \Psi_ {t - 1}\right) = \delta_ {m, t - 1} \theta_ {t - 1} \operatorname{var} \left(R _ {m t}, / \Psi_ {t - 1}\right) \tag{5}

$$

The excess return of portfolio i is expressed as follows:

$$

E \left(R _ {i t} / \Psi_ {t - 1}\right) - R _ {f t} = \delta_ {m, t - 1} \operatorname{cov} \left(R _ {i t}, R _ {m t} / \Psi_ {t - 1}\right) \tag{6}

$$

Since both portfolios have the same risk, the positive coefficient can be deduced from the following system.

$$

\operatorname{var} \left(R _ {i t} / \Psi_ {t - 1}\right) = \operatorname{var} \left(R _ {I t} / \Psi_ {t - 1}\right) \tag{7}

$$

$$

\operatorname{var} \left(R _ {I t} / \Psi_ {t - 1}\right) = \theta_ {t - 1} ^ {2} \operatorname{var} \left(R _ {m t} / \Psi_ {t - 1}\right) \tag{8}

$$

$$

E\left(R_{t} - R_{it} / \Psi_{t - 1}\right) = \delta_{m, t - 1} \left[ \theta_{t - 1} \operatorname{var}\left(R_{mt} / \Psi_{t - 1}\right) - \operatorname{cov}\left(R_{it}, R_{mt} / \Psi_{t - 1}\right) \right]

$$

A first intuition can be drawn from equation (10) by taking the particular case $\theta = 1$

$$

E\left(R_{I_t} - R_{i_t} / \Psi_{t - 1}\right) = \delta_{m, t - 1} \left[ \operatorname{var}\left(R_{m_t} / \Psi_{t - 1}\right) - \operatorname{cov}\left(R_{i_t}, R_{m_t} / \Psi_{t - 1}\right) \right]

$$

Relation (11) presents the measure of portfolio diversification gains developed by De Santis and Gérard (97) for the case of the American investor, which is a special case of (10), according to their relation market i has the same portfolio risk of the world market at each point in time.

According to the relation (10), the expected gains from portfolio diversification are an increasing function of the price of the world market risk and the quantity of the specific risk considered.

In what follows, we will examine the implications of relationship (3) for international portfolio diversification.

Thus, let us consider two portfolios that present the same risk, the first one is internationally diversified noted I and the other one is purely domestic noted i. The CAPMT relationship described in equation (3) allows us to calculate the expected return on each of these portfolios.

The difference between the two expected returns can be interpreted as the ex-ante gain from international portfolio diversification (the benefit generated by holding international stocks).

This gain can be expressed as follows:

$$

E \left(R _ {I t} - R _ {i t} / \Psi_ {t - 1}\right) \tag {4}

$$

According to Black's (1972) separation theorem, portfolio profitability can be written as a form of a linear combination between the risk-free asset and the market portfolio $R_{I} = \theta_{t - 1}R_{mt} + (1 - \theta_{t - 1})R_{ft}$, where $\theta$ is the measure of risk aversion

Thus, the excess return of the portfolio I is expressed as follows:

$$

\text{Let} \theta_ {t - 1} ^ {2} = \frac{\operatorname{var} \left(R _ {i t} / \Psi_ {t - 1}\right)}{\operatorname{var} \left(R _ {m t} / \Psi_ {t - 1}\right)} \tag{9}

$$

According to equations (5) and (6), the gain of international diversification for a domestic investor according to the conditional version of the CAPM is given by the following relation:

However, our contribution at this level of research consists in developing a conditional version of the FEM which allows on the one hand to measure the expected gains from international diversification and on the other hand it must take into account other factors in addition to the global market risk.

The factors that are ignored by previous studies precisely in this topic, namely: the exchange rate risk, the local market risk and the specification of the degree of integration.

In this regard, the use model developed by Fatma Khalfallah (2023) is appropriate at this level.

Thus, our version of conditional CAPM presents a mixed relationship between the price of market risk,

$$

E \left(R _ {i t} / \Psi_ {t - 1}\right) - R _ {f t} = \phi_ {t - 1} ^ {i} \left[ \delta_ {m, t - 1} \operatorname{cov} \left(R _ {i t}, R _ {m t} / \Psi_ {t - 1}\right) + \sum_ {c = 1} ^ {L} \delta_ {c, t - 1} \operatorname{cov} \left(R _ {i t}, R _ {c t} / \Psi_ {t - 1}\right) \right] + \left(1 - \phi_ {t - 1} ^ {i}\right) \left[ \delta_ {i, t - 1} \operatorname{var} \left(R _ {i t} / \Psi_ {t - 1}\right) \right] \tag{12}

$$

Thus the model application of equation (12) for equations (5) and (6) is as follows.

For equation (5), the excess return on the portfolio $I$ that is internationally diversified is written as a function of market risk and currency risk:

$$

E(R_{I} / \Psi_{t-1}) - R_{ft} = \left[ \delta_{m,t-1} \operatorname{cov}(\theta_{t-1} R_{mt}, R_{mt} / \Psi_{t-1}) + \sum_{c=1}^{L} \delta_{c,t-1} \operatorname{cov}(R_{mt}, R_{ct} / \Psi_{t-1}) \right] = \delta_{m,t-1} \theta_{t-1} \operatorname{var}(R_{mt} / \Psi_{t-1}) + \sum_{c=1}^{L} \delta_{c,t-1} \operatorname{cov}(R_{mt}, R_{ct} / \Psi_{t-1})

$$

For equation (6), the excess return of portfolio $i$ that is purely domestic is written as a function of market risk and local market risk and a measure of degree of integration:

$$

E \left(R _ {i t} / \Psi_ {t - 1}\right) - R _ {f t} = \phi_ {t - 1} ^ {i} \left[ \delta_ {m, t - 1} \operatorname{cov} \left(R _ {i t}, R _ {m t} / \Psi_ {t - 1}\right) + \left(1 - \phi_ {t - 1} ^ {i}\right) \left[ \delta_ {i, t - 1} \operatorname{var} \left(R _ {i t} / \Psi_ {t - 1}\right) \right] \right] \tag{14}

$$

Thus, according to equations (13) and (14), the gain from international diversification according to the conditional version of the CAPM is given by the relation (15)

$$

\begin{array}{l} E \left(R _ {I t} - R _ {i t} / \Psi_ {t - 1}\right) = \delta_ {m, t - 1} \left[ \theta_ {t - 1} \operatorname {v a r} \left(R _ {m t} / \Psi_ {t - 1}\right) - \phi_ {t - 1} ^ {i} \operatorname {c o v} \left(R _ {i t}, R _ {m t} / \Psi_ {t - 1}\right) \right] + \\\left[ \sum_ {c = 1} ^ {L} \delta_ {c, t - 1} \operatorname {c o v} \left(R _ {m t}, R _ {c t} / \Psi_ {t - 1} - \left(1 - \phi_ {t - 1} ^ {i}\right) \delta_ {i, t - 1} \operatorname {v a r} \left(R _ {i t} / \Psi_ {t - 1}\right) \right. \right] \tag {15} \\\end{array}

$$

Then, relation (15) shows that the expected gain from international diversification strategies is determined as a function of the price of market risk, the amount of country-specific risk considered with a measure of the degree of integration

$$

\operatorname{var} \left(R _ {m t} / \Psi_ {t - 1}\right) - \phi_ {t - 1} ^ {i} \operatorname{cov} \left(R _ {i t}, R _ {m t} / \Psi_ {t - 1}\right)

$$

the price of exchange rate risk $\delta_{c,t - 1}$ and local market risk $\delta_{i,t - 1}$

### b) The Data

Our study focuses on the economies of the MENA region, with data for the following countries: Tunisia, Morocco, Egypt, Turkey, Jordan, Saudi Arabia, the United Arab Emirates United Arab Emirates, France, Great Britain, the United States, and the global market. Then, four groups of data are considered: the monthly return series market as well as the world market, the series of real exchange rates expressed in US dollars exchange rate series expressed in U.S. dollars, the financial and macroeconomic variables used to macroeconomic variables used to condition the estimates of risk prices and the instrumental variables related to the degree of related to the degree of integration.

### c) The Yield Series

The observations used are monthly end-of-period prices from January 1995 to December 2013 for Morocco, Egypt, Turkey and Jordan, and from May 2005 to December 2013 for Tunisia, Saudi Arabia and the United Arab Emirates.

Market prices are taken from Morgan Stanley Capital International.

(MSCI), and the market portfolio is approximated by the MSCI world index 25, these market returns are expressed in dollars and adjusted by dividends.

### d) Real Exchange Rate Series

The monthly real exchange rates are expressed in terms of the U.S. dollar 27, and are taken from Intertnaional Financial are extracted from Intertnaional financial statistic (IFS) and obtained by subtracting nominal exchange rates exchange rates by the consumer price indexes (CPI).

### e) Global and Local Instrumental Variables

The instrumental variables are used to condition estimating the prices of market risk, currency risk and risk local, like Hardouvelis et all (2006) and Carrieri and All (2007) we retain the following factors to condition estimating the prices of market risk and foreign risk:

- The monthly change in dividend yield (dividend to price ratio) of the world market portfolio (MSCI world index) over the 30-day eurodollar interest rate (DRMDV)

- The monthly change in the premium term, it's the difference between a long interest rate (10 years us treasury notes) and short rate (3 months us treasury bills) (DEPTTERM)

- The monthly change in the short term interest rate (3 months us treasury bills) (DSHORT).

- The monthly change in the S&P's 500 stock market index (RSP)

- A constant term

All these information variables are extracted from the international datasstream database and are used with a lag behind the series of excess returns.

For the risk of the local market of each country, we use the following set of information variables is determined by previous studies like Bekaert and Harvey, 1995; Gerard et al., 2003)

- A constant term

- The monthly change in the excess stock returns of each country (DRD)

- The monthly change in 1-month interest rate (DSHORT)

- The monthly change in the regional inflation rate (VIR)

- 4- the instrumentals variables of financial integration

The degree of financial integration for each country is affected by some economic financial and sociopolitical factors at the local and international level. It is, therefore, necessary to identify the determinants of the degree of financial integration. To this end, we use the following variables information

- DGDP: Each country's Gross domestic product (GDP) in volume, which is considered the most appropriate instrument to identify the level of integration by Carieri et al. (2007) and Bhattacharya and Daouk (2002).

- INRD: The interest rate differential between the US market and the local market, this variable reflects the convergence of these emerging markets to the global market

- INFD: The differential between the rate of inflation in each local market and the US, this variable highlights the volatility of exchange rates of the local currency and provides information on the investment costs and consequently the advantage of diversification

Table 1: Anticipated Gains from International Diversification of MENA Markets for the Period 05-2005 to 12-2013 (%)

<table><tr><td></td><td>With the World Market</td><td>With the French Market</td><td>With the British Market</td><td>With the American Market</td></tr><tr><td>Egypt</td><td>1.561

(1.2795)</td><td>1.9299*

(1.2909)</td><td>1.8199*

(1.1794)</td><td>2.009*

(1.1905)</td></tr><tr><td>Emirates</td><td>2.4695*

(0,2876)</td><td>2.8905*

(0,3806)</td><td>2.155*

(0,1887)</td><td>2.305*

(0,1437)</td></tr><tr><td>Jordan</td><td>3.8351*

(0,1117)</td><td>4.491*

(0,2117)</td><td>3.9075*

(0,1001)</td><td>4.101**

(0,123)</td></tr><tr><td>Morocco</td><td>3.8479**

(0,1776)</td><td>3.201**

(0,2228)</td><td>3.9978**

(0,1476)</td><td>6.001**

(0,0869)</td></tr><tr><td>Saudi Arabia</td><td>3.607*

(0,6223)</td><td>4.5071***

(0,7023)</td><td>4.0171*

(0,4988)</td><td>3.9891*

(0,7117)</td></tr><tr><td>Tunisia</td><td>5.021***

(0,0889)</td><td>6.331**

(0,0569)</td><td>5.906***

(0,0780)</td><td>7.122***

(0,033)</td></tr><tr><td>Turkey</td><td>1.132

(2,3441)</td><td>2.0021

(2,0441)</td><td>1.977

(2,2911)</td><td>2.881

(2,0001)</td></tr></table>

According to Table 1, the results show a statistically and economically significant advantage of international diversification for all the markets studied with the global market, the French market, the British market and the American market except for Turkey.

Indeed, over the period of study, Egypt the most correlated with the global market with an average correlation of $62\%$ has the lowest average annual profits $1.56\%$, the same finding with the French market, British and American; the strongest correlation with a low potential diversification that does not exceed $2\%$.

On the other hand, Tunisia the least correlated market with the global market, the French market, the British market and the U.S. market with respective average correlations (32%, 31%, 32%, 31%) and presents the highest profits of diversification (5%, 6.33%, 5.9%, 7.12%).

Morocco presents a diversification gain for the American investor of $6\%$ and around $4\%$ with the world, French and British markets with an average correlation of $40\%$ with all these markets. The same result is also found for Jordan with very close values for the correlation as well as the gains of international diversification.

For the Gulf countries, Emirates and Saudi Arabia have a correlation at the turn of $50\%$ and $40\%$ with the world market as well as with the other developed markets, they present significant diversification gains on average of $2.5\%$ for Emirates and at the turn of $4\%$ for Saudi Arabia.

The results reported in this table of the evolution of diversification gains, indicate that the estimated gains of international portfolio management have significantly decreased during the crisis phase, contrary to the opinion among financial experts and academics.

Indeed, the anticipated gain of Egypt's diversification with the world market and developed markets presents oscillations with positive and negative

### f) Financial Integration

## i. The Degree of Financial Integration

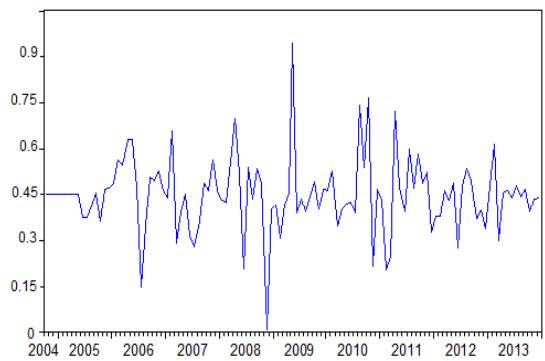

values that explains the low potential of diversification, a sharp drop is recorded twice; $(-25\%)$ during the crisis phase 2007-2009 and $(-28\%)$ during the revolution period 2010-2011.

For Morocco, the profit values are more important before the crisis period, at the time of shock the gains noted a considerable fall $(-13\%)$, this result valid with the world market, French, British and especially with the American market the gains remained slightly weak until the end of the period of study and this compared to the period before the crisis.

For Jordan, the graph shows a sharp drop of $(-23\%)$ between 2008 and 2009 with the world market and the developed markets in our sample. These same findings are also valid for the Saudi and UAE markets with falls of $20\%$ and $27\%$ during the crisis phase.

For Tunisia, the subprime crisis has also affected the gains on this market with a drop in value $(-12\%)$ as well as during the period of revolution 2010-2011, this collapse is recorded with the global market, French, British and American.

Table 2: Estimation of Dynamic Financial Integration

<table><tr><td></td><td>EGYPT</td><td>EMIRATES</td><td>JORDAN</td><td>MOROCCO</td><td>SAUDI ARABIA</td><td>TUNISIA</td><td>TURKEY</td></tr><tr><td colspan="8">Panel A: Estimation Results of the Degree Of Integration as a Function of The Instrumental Variables</td></tr><tr><td>Cons</td><td>-0.099***</td><td>-0.0152*</td><td>0.022***</td><td>-0.0062</td><td>-0.106*</td><td>0.23</td><td>0.0098**</td></tr><tr><td>DGDP</td><td>-0.0037</td><td>0.002</td><td>6.7E-04</td><td>0.001</td><td>0.002</td><td>-0.0019</td><td>4.8E-04</td></tr><tr><td>INRD</td><td>0.004</td><td>-0.0153*</td><td>-0.0065*</td><td>0.001</td><td>-0.0066</td><td>-0.0076</td><td>-3.1E-04*</td></tr><tr><td>IFRND</td><td>0.0756</td><td>0.0018</td><td>-0.0029**</td><td>-0.0045</td><td>0.0019</td><td>9E-04</td><td>2E-04</td></tr><tr><td colspan="8">Panel B: Financial Integration Measurement Statistics</td></tr><tr><td>\(\varnothing_{min} \)</td><td>0.116</td><td>0.103</td><td>0.098</td><td>0.116</td><td>0.098</td><td>0.003</td><td>0.075</td></tr><tr><td>\(\varnothing_{max} \)</td><td>0.889</td><td>0.913</td><td>0.977</td><td>0.903</td><td>0.9</td><td>0.901</td><td>0.9</td></tr><tr><td>\(\varnothing_{moy} \)</td><td>0.663***</td><td>0.651***</td><td>0.578***</td><td>0.633***</td><td>0.601***</td><td>0.457***</td><td>0.448***</td></tr><tr><td>Std.dev</td><td>0.7868</td><td>0.00674</td><td>0.0089</td><td>0.0104</td><td>0.00747</td><td>0.0011</td><td>0.00015</td></tr></table>

This table reports the estimation results for the financial integration metrics.. $\varnothing_{\min}$ $\varnothing_{\max}$,and $\varnothing_{\mathrm{moy}}$ show the maximum, minimum and average degree of integration respectively. The robust standard deviations are indicated by the Std.dev.

According to the estimation results reported in Table 1 panel A, the dynamics of financial integration in our sample is explained especially by the differential between the local interest rate and that of the US and the differential between the local inflation rate and that of the US.

According to the statistics (panel B), Turkey and Tunisia have the lowest degree of integration with values of 0.448 and 0.457 respectively. They are the least integrated countries in the world market as well as the Jordanian market with a level equal to 0.578.

In contrast, Egypt has the highest average level of financial integration with a value of 0.663. After that, we find the Gulf countries Emirates (0.651) and Saudi (0.601) and Morocco with a value of 0.633.

Our results at this stage are close to the results of Khaled Guesmi et al (2014) who studied the financial integration process of 4 countries in the MENA region

(Turkey, Israel, Jordan and Egypt), they also found that Egypt the most integrated market and Jordan is the most segmented.

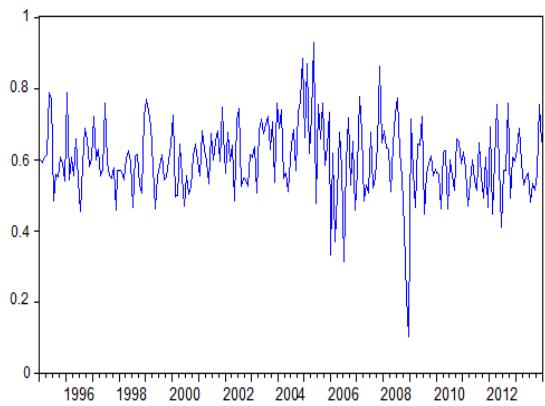

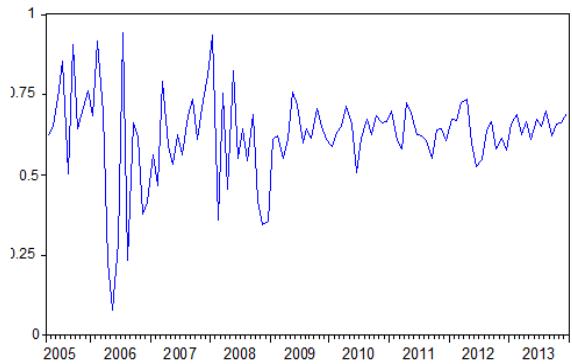

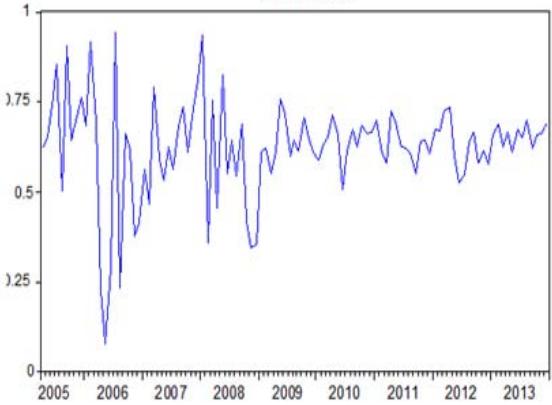

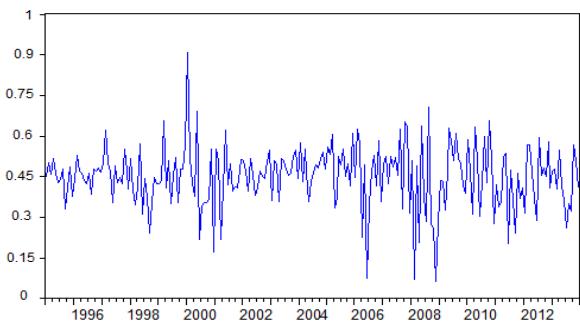

DI_EGY

Panel label: DI JORDANIE.

Panel label: DI MAROC.

DI_SAOUDITES

DI_EMIRATES

DI_TUNISIA

DI_TURKEY Graphic 1: The Evolution of the Level of Financial Integration

Graphic 1 traces the evolution of the level of financial integration of seven MENA markets with the global market and shows that this integration is not homogeneous. According to the chart, Egypt is the most integrated market with a threshold of $85\%$ during the period 1998-2000, after which the level dropped to around $70\%$ for the rest of the period.

For the Emirates, their degree of integration with the global market has experienced two peaks during the year 2005 and the year 2010 with a level of $90\%$. The same thing for Saudi Arabia has experienced a financial integration rate between 2006 and the end of 2007 with a value that reaches a threshold of $85\%$.

This upward trend can be explained by the increase in investment capital flows to these countries.

## ii. Measure of Integration Versus Conditional Correlation

Turkey, Tunisia and Jordan show the lowest level of integration with an average rate of $50\%$ during the study period. However, all of the markets studied experienced a considerable drop during the 2007-2008 period.

This decline is due to the impact of the subprime crisis on these markets and on the global market in general.

In sum, an upward trend then is recorded when examining the dynamics of financial integration in MENA markets. In what follows, we will conduct a comparative analysis between financial integration and conditional correlation in order to confirm these results.

Table 3: Statistics of Conditional Correlations

<table><tr><td></td><td>EGYPT</td><td>EMIRATES</td><td>JORDAN</td><td>MOROOCO</td><td>SAUDI ARABIA</td><td>TUNISIA</td><td>TURKEY</td></tr><tr><td>ρmin</td><td>0.786</td><td>0.397</td><td>0.298</td><td>0.3</td><td>0.177</td><td>0.477</td><td>0.455</td></tr><tr><td>ρmax</td><td>0.813</td><td>0.925</td><td>0.901</td><td>0.887</td><td>0.947</td><td>0.937</td><td>0.803</td></tr><tr><td>ρmoy</td><td>0.801***</td><td>0.831***</td><td>0.723***</td><td>0.697***</td><td>0.733***</td><td>0.788***</td><td>0.701***</td></tr></table>

$\rho$ max., $\rho$ min. and $\rho$ moyenne mean are the maximum, minimum and mean correlation coefficients, which are obtained from the multiple bivariate DCC-GARCH processes. \*\*\* indicates that the coefficient in question is significantly different from zero.

The purpose of correlation estimation is to provide conditional investors with a complete picture of the actual financial and economic situation in each market.

Since the correlations approach is a technique for measuring financial integration that has been applied by previous works "Longin and Solnik (1995), Kroly and Stulz (1996), Manuel and Croci (2004). However, the appeal to the simple calculation of conditional correlations does not allow us to affirm this purpose, which justifies the use of instrumental variables of financial integration "Dumas et al (2006), Carrieri et al (2007)".

The examination of this observation is presented in Table 6, which compares the integration index of each local market to its conditional correlation with the world market. Then the analysis of the statistics shows us that the conditional correlations in sum are more important in terms of values compared to the financial integration index.

Egypt has an average correlation coefficient of 0.801 against an average degree of integration 0.663. Similarly, for Emirates, Jordan, Saudi Arabia, Tunisia and Turkey.

However, an almost small gap is observed for Morocco 0.697 against 0.633.

To summarize, the dynamics of conditional correlations show an overestimation of the degree of integration of the markets studied, so our results confirm the questioning of the relevance of the correlation technique as an index of financial integration.

## IV. CONCLUSION

The conclusions drawn from the literature indicate that the framework of financial crises, which is characterized by strong interdependence between financial markets and high volatility, is a major concern for the investor seeking international portfolio diversification.

Thus, with the growth of co-movements between developed and emerging markets and the frequent emergence of financial crises that characterize East Asia, Latin America and Eastern Europe, the investor should target other emerging markets such as MENA countries.

The appreciable profits realized by the strategy of international portfolio diversification have been detected by the works of Markowitz (52), Grubel (1968),

- Levy and Sarnat (1972), Solnik (1974) and Hilliard (1979).

- In addition to these classic works, a group of studies have explored the benefits of portfolio diversification among developed markets as well as emerging countries such as Harvey (91), Campbell and Hamao (1992), Odier and Solnik (93), Solnik (95) Gerke et al (2005), Markellos and Siriopoulos (1997), Rezayat and Yavas (2006), Chiou (2008), Chonghui jiang et al (2010).

- During periods of financial crisis the results found by several studies question the effectiveness of international diversification strategy. Garnant (1998) Schwebach et al (2002) Middleton et al (2008), Robert G. Bowmana, Kam Fong Chan and Matthew R. Comer (2010) RG Bowman et al (2010) Robert vermenh (2011).

- For the MENA region the axis of work that has been conducted is oriented towards the objective of seeking opportunities of international diversification for the international investor in these markets following the example of Darrat et al (2000) Abraham et al (2001) 2003), Assaf Simon Neaime (2005) Thomas et al (2005 (2007), Cheng et al (2010 Mansourfour et al (2010) S. Neaime (2012) Graham et al (2013) Houseyin et al (2013), Mehmet Balcilar et al (2015).

- However, the classical and recent works on this topic there in times of crisis and non-crisis have carried some limitations in their basic strategies. Indeed, the assumption of the absence of hedging to international investment has made ignore the exchange rate risk in the modeling as well as the local risk.

- In addition, most of the works have adopted only the assumption of perfect financial integration in the financial markets when studying the expected gains from international diversification.

- In this regard, our contribution to the literature has sought to test a conditional version of CAPMFI that includes both in addition to global market risk, foreign exchange risk and local market risk in order to identify the potential of diversification that offers MENA countries for investors and their significance in times of crisis with a consideration of the specification of degree of integration of markets studied.

- Then, our results indicated that the anticipated gains from diversification sought in MENA markets are present and significant during the study period with temporary absence during the mortgage crisis phase for all the studied markets and during any period of political disturbance, the case of revolution for Egypt and Tunisia.

Generating HTML Viewer...

References

47 Cites in Article

M Abbes,Y Trichilli (2015). Islamic stock markets and potential diversification benefits.

A Abraham,F Seyyed,A Al-Elg (2001). Analysis of diversification benefits of investing in the emerging gulf equity markets.

Michael Adler,Bernard Dumas (1983). International Portfolio Choice and Corporation Finance: A Synthesis.

M Arouri,F Jawadi (2010). On the impacts of crisis on the risk premium: Evidence from the US stock market using a conditional CAPM.

Ata Assaf (2003). Transmission of Stock Price Movements: The Case of GCC Stock Markets.

M Balcılar,R Demirer,S Hammoudeh (2015). Regional and global spillovers and diversification opportunities in the GCC equity sectors.

David Barr,Richard Priestley (2004). Expected returns, risk and the integration of international bond markets.

Geert Bekaert,Campbell Harvey (1995). Time‐Varying World Market Integration.

Geert Bekaert,Campbell Harvey (1995). Time‐Varying World Market Integration.

G Bekaert,C Harvey (1997). Emerging equity market volatility.

Robert Bowman,Kam Chan,Matthew Comer (2010). Diversification, rationality and the Asian economic crisis.

Ai-Ru Cheng,Mohammad Jahan-Parvar,Philip Rothman (2010). An empirical investigation of stock market behavior in the Middle East and North Africa.

Wan-Jiun Paul Chiou (2008). Who benefits more from international diversification?.

Jean-Claude Cosset,Jean-Marc Suret (1995). Political Risk and the Benefits of International Portfolio Diversification.

H Dağli,U Sivri,S Bank (2012). International portfolio diversification opportunities between Turkey and other emerging markets.

A Darrat,K Elkhal,S Hakim (2000). On the integration of emerging stock markets in the Middle East.

G De Santis (1997). Stock returns and volatility in emerging financial markets.

G De Santis (1997). Stock returns and volatility in emerging financial markets.

Bernard Dumas,Campbell Harvey,Pierre Ruiz (2003). Are correlations of stock returns justified by subsequent changes in national outputs?.

C Eun,B Resnick (1986). Supply Chain Risk: Diversification Vs Under-diversification.

Fatma Khalfallah (2023). The risk premium in times of financial crisis: an assessment from ICAPM on the MENA region.

Alberto Giovannini,Philippe Weil (1989). Risk Aversion and Intertemporal Substitution in the Capital Asset Pricing Model.

Michael Graham,Jarno Kiviaho,Jussi Nikkinen,Mohammed Omran (2013). Global and regional co-movement of the MENA stock markets.

C Granger (1969). Investigating Causal Relations by Econometric Models and Cross-spectral Methods.

Yasushi Hamao,Ronald Masulis,Victor Ng (1990). Correlations in Price Changes and Volatility across International Stock Markets.

Campbell Harvey (1991). The World Price of Covariance Risk.

Iftekhar Hasan,Yusif Simaan (2000). A rational explanation for home country bias.

S Johansen (1988). Statistical analysis of cointegration vectors.

G Karolyi,René Stulz (1996). Why Do Markets Move Together? An Investigation of U.S.‐Japan Stock Return Comovements.

G Karolyi,René Stulz (1996). Why Do Markets Move Together? An Investigation of U.S.‐Japan Stock Return Comovements.

G Karolyi,René Stulz (2003). Chapter 16 Are financial assets priced locally or globally?.

Dimitris Kenourgios,Aristeidis Samitas,Nikos Paltalidis (2011). Financial crises and stock market contagion in a multivariate time-varying asymmetric framework.

Thomas Lagoarde-Segot,Brian Lucey (2007). International portfolio diversification: Is there a role for the Middle East and North Africa?.

Thomas Lagoarde-Segot,Brian Lucey (2007). International portfolio diversification: Is there a role for the Middle East and North Africa?.

J Lintner (1965). Security prices, risk, and maximal gains from diversification.

François Longin,Bruno Solnik (1995). Is the correlation in international equity returns constant: 1960–1990?.

François Longin,Bruno Solnik (1997). Extreme Correlation of International Equity Markets.

G Mansourfar,S Mohamad,T Hassan (2010). The behavior of MENA oil and non-oil producing countries in international portfolio optimization.

Harry Markowitz (1952). Portfolio Selection.

C Middleton,S Fifield,D Power (2008). An investigation of the benefits of portfolio investment in Central and Eastern European stock markets.

C Middleton,S Fifield,D Power (2008). An investigation of the benefits of portfolio investment in Central and Eastern European stock markets.

H Minsky (1992). The financial instability hypothesis, working paper.

Simon Neaime (2005). Financial Market Integration and Macroeconomic Volatility in the MENA Region: An Empirical Investigation.

Simon Neaime (2005). Financial Market Integration and Macroeconomic Volatility in the MENA Region: An Empirical Investigation.

Simon Neaime (2012). The global financial crisis, financial linkages and correlations in returns and volatilities in emerging MENA stock markets.

Simon Neaime (2012). The global financial crisis, financial linkages and correlations in returns and volatilities in emerging MENA stock markets.

Jacek Niklewski,Timothy Rodgers (2011). International Portfolio Diversification and the 2007 Financial Crisis.

No ethics committee approval was required for this article type.

Data Availability

Not applicable for this article.

How to Cite This Article

Fatma Khalfallah. 2026. \u201cFinancial Crises and the Success of Global Portfolio Management: A Study of the Middle East and North Africa\u201d. Global Journal of Management and Business Research - D: Accounting & Auditing GJMBR-D Volume 23 (GJMBR Volume 23 Issue D2): .

Explore published articles in an immersive Augmented Reality environment. Our platform converts research papers into interactive 3D books, allowing readers to view and interact with content using AR and VR compatible devices.

Your published article is automatically converted into a realistic 3D book. Flip through pages and read research papers in a more engaging and interactive format.

Our principal objective is to implement a conditional CAPM that, in addition to the global market risk, specifies the level of market integration, evaluates exchange rate risk, and accounts for local market risk. To investigate the potential for portfolio diversification for foreign investors in this region by examining the impact of financial crises on the evolution of national markets in the MENA region’s financial integration with the global market as well as with the three selected developed markets, namely France, Great Britain, and the United State. In order to test a conditional version of De Santis and Gerard’s ICAPM by admitting a specification of a multivariate GARCH process, this line of research has used a particular methodology (MGARCH).

Our website is actively being updated, and changes may occur frequently. Please clear your browser cache if needed. For feedback or error reporting, please email [email protected]

Thank you for connecting with us. We will respond to you shortly.