This study examines the impact of firm characteristics on the profitability of listed consumer goods companies in Nigeria. The specific objectives are to assess the influence of firm characteristics (liquidity, leverage, and age) on the profitability of these companies in Nigeria, and to explore the moderating effect of firm size on the relationship between firm characteristics and profitability. The ex post facto research design was implemented for this study. The data were collected from secondary sources, particularly the audited financial reports of 16 consumer goods companies listed on the Nigerian Exchange Group as of December 31, 2022, spanning a decade (2013-2022) using purposive sampling techniques. The Descriptive and inferential statistics were employed to analyze the data. The Panel regression analysis was conducted for hypothesis testing, and pre-estimation and post-estimation procedures were executed. The Hausman test confirmed that the random effect model was appropriate. The findings indicate that liquidity has a negative and significant impact on profitability, while leverage and firm age exhibit positive but insignificant effects.

## I. INTRODUCTION

Consumer goods companies produce products that play a significant role in the Nigerian economy by creating job employment, supporting the GDP, and providing goods that meet the demands of the growing population. The country of Nigeria has a large and a growing population that provides a major demand for consumer goods, thereby creating a significant market for the industry. The consumer goods sector has developed as the fastest-growing segment of the FMCG in Africa (Oduogu et al., 2024). The expanding middle class of the population, increase in urbanization, rising disposable income, e-commerce, export potentials have significantly influenced the high demand for goods in this sector. The consumer goods companies are expected to profit from achieving these goals.

Firm characteristics impact the actions of a company that is internally controlled and help facilitate the achievement of set objectives (Wakaisuka-Ilsignoma, 2016). The Handoyo et al. (2023) described firm characteristics as anticipating strategic outcomes that enhance performance. The failure of a company to maximize its profitability through internal resources is perceived to have a major challenge (Msomi & Nyide, 2021). Hence, there is a need for an in-depth understanding of the relationship between specific firm characteristics and profitability, as these factors are key determinants of a firm's profitability. The profitability of consumer goods companies can be affected by the influence of firm size on company characteristics. Therefore, the moderating effect of firm size on firm characteristics and profitability of consumer goods companies in Nigeria is crucial to this sector, as different studies have shown varied and inconsistent results.

Profitability is a significant condition for the survival of any entity. Profitability indicates the financial health of a definite period (Alhasanko, 2024). It also affects the performance of other organizational goals, whether financially or otherwise. The ability of an organization to generate a profit is a key indicator that attracts prospective investors to the organization.

The current inflation in Nigeria reached a record high of over $33.9\%$ in October 2024, significantly impacting production costs and directly affecting the purchasing power of citizens. With the high inflation rate and unified foreign exchange rate, many businesses, including consumer goods companies, encounter low profitability as economic conditions take their toll on the

Nation. Therefore, the internal factors influencing the profitability of consumer goods companies should be examined as they develop strategies to enhance profitability.

Many studies have explored firm characteristics, including those of Chabachib et al. (2020), who analyze companies' characteristics of firm value with profitability serving as an intervening variable. Zubairu et al. (2022) examined the effect of several key monetary variables as a moderator. Morris et al. (2023) utilized cash conversion to moderate the firm attributes and financial leverage of listed consumer goods firms in Nigeria. The study of Adenle et al. (2024) employed leverage as a moderating variable to determine the influence of firm attributes on the financial performance of listed Nigerian consumer goods firms. Idris and Adediran (2023) used firm size as a moderating variable for corporate attributes and financial reports of consumer goods companies in Nigeria. The study by Onatuyeh et al. (2024) examined financial reporting quality and performance, with emphasis on the mediating role of firm characteristics. These studies have focused on consumer goods companies. The existing literature has not examined the effect of firm size as a moderating variable of firm characteristics and profitability of listed consumer goods companies in Nigeria. This study fills the gap in the existing literature by examining the effect of firm size on firm characteristics (liquidity, leverage, and firm age) and broadens the understanding of the variables that impact the profitability of consumer goods companies in Nigeria.

The study aims to examine firm characteristics and profitability of listed consumer goods companies in Nigeria: The moderating effect of firm size.

## II. LITERATURE REVIEW

### a) Conceptual Framework

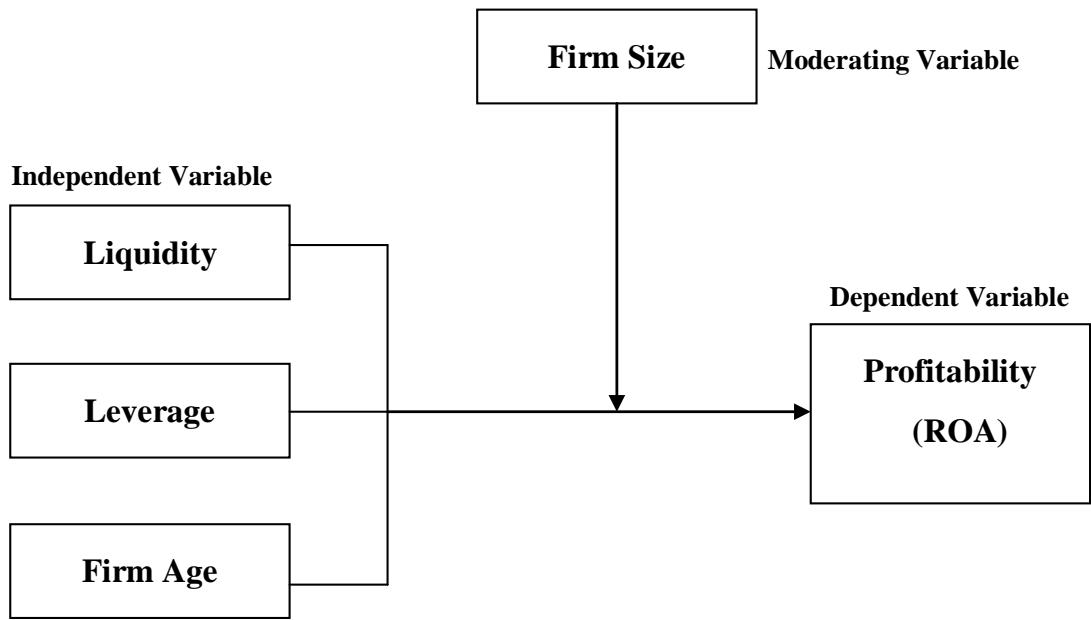

The study's conceptual framework comprises exogenous variables of firm characteristics proxied by liquidity, leverage, and firm age and endogenous variable of profitability proxied by return on assets (ROA). The moderating variable was firm size.

Fig. 2.1: The Framework of the Study

Source: Adapted from Idris & Adediran (2023) and Suleiman & Khalid (2024)

## III. PROFITABILITY

The main objective of a business is to generate profits. The profitability is crucial for a business entity's survival and helps to measure its activities. Profitability connotes efficiency by comparing the results of an activity with the efforts put into it. This is a quantitative factor for assessing economic growth (Geamanu, 2011). An entity's performance primarily refers to its profitability, which effectively contributes to its resources and, in turn, to the national economy's over all development (Lazar, 2016). The management's efficiency is often evaluated by its ability to generate profit; the greater the profit, the higher the efficiency (Toshniwal, 2016). The firm's value is largely a function of its profitability and growth potential (Fajaria & Isnalita, 2018). The interest of an entity is not only to generate profit but also to maintain that profit on an incremental basis. The consistency helps attract and retain stakeholders, which is usually reflected in stock prices. Kuster et al. (2023) identified two methods for measuring profitability: return on assets (ROA) and return on equity (ROE). The method adopted by any organization may not be sanctioned but must be

defensible. Profitability involves two aspects: profit and ability. Profit is the amount obtained by deducting total expenses from the total revenue. The term ability refers to the organization's capacity to generate profits. 'The ability also means earning power, earning capacity, or operating performance of the concerned investment' (Toshniwal, 2016). Increased competition, technological innovation, and price dynamics affect profitability (Fareed et al., 2016).

The study proxied profitability by ROA, in line with the studies by Yau et al. (2024), Adenle et al. (2024), Irwansyah et al. (2023), and Azlan et al. (2022).

## IV. FIRM ATTRIBUTES

### a) Liquidity

Liquidity refers to cash. It is the ability to convert financial assets into cash without diminishing their value. Liquidity is the ability to fulfill monetary and other obligations with minimal expenses. The maintenance of an adequate level of liquidity helps ensure that an entity's goals and objectives align with cash flow expectations, thus preventing adverse effects on its operations. Liquidity management involves strategies (both short- and long-term) that can be utilized to manage cash positions over time. The survival of an organization requires the availability of funds and the assurance that funds will be accessible to meet obligations as they come due in the future. High liquidity signals that an entity can settle its debts. Conversely, low liquidity increases the risk of defaulting on debt repayment (Ali, 2023). An entity that fails to meet its obligations as they fall due may encounter insolvency challenges. The significant lack of liquidity can drive an entity into insolvency (Pandey, 2016). The industry average of 2:1 is typically regarded as a protective ratio against inadequate liquidity. Liquidity can be characterized by both monetary and banking history. Today, it encompasses various explanations, such as market complexities and technological advancements, including financial and security market services (Attila, 2014). The availability of cash can significantly impact a business's efficiency. Various ratios, such as current, acid-test, and cash ratios, are employed to measure liquidity, each presenting distinct advantages and disadvantages.

### b) Leverage

Leverage is a strategy that utilizes outsiders' money to enhance the returns of an entity. It represents the amount of borrowed funds a company uses to finance its assets. A leveraged company is an entity that is highly geared, meaning it relies more on debt than equity in its capital structure. High leverage indicates increased debt and a corresponding increase in financial risk. Companies are typically motivated to use leverage to boost profitability, which ultimately helps maximize shareholders' returns. This strategy is based on the premise that fixed-cost charges can be obtained at a lower cost and yield returns exceeding the entity's rate of return (Pandey, 2016). Financial leverage can be measured through the 'Debt ratio, Debt-equity ratio, and Interest coverage'. The first two are known as capital gearing, based on book or market values, while the last is termed the coverage ratio and measures an entity's income gearing. The necessity for leverage varies among entities; factors such as assets, structure, and operating systems often influence their leverage position.

### c) Firm Age

Firm age is often described as the number of years a firm has existed since its incorporation. The ageing process of firms can occur at different levels, specifically in areas of employees, organizations, or groups of firms (Coad, 2018). The profitability of a firm appears to decline as it grows older. This decline may be attributed to rising costs, slow growth, obsolescence, and a reduction in research and development activities (Claudio & Urs, 2010). The relationship between firm age and profitability is also convex, indicating that younger firms may exhibit signs of profit reduction but can transition to profitability as they mature (Elif, 2016). Kajola et al. (2022) found an inverse relationship between firm age and profitability, whereas Kaoje et al. (2022) observed a positive relationship. This research measures firm age from the date of incorporation.

## V. FIRM SIZE

Firm size is one of the pivotal attributes of any organization that influences its control mechanisms and operations. Companies' assets, turnover, and liquidity are affected by it. Firm size can be measured by the volume of total assets, total sales, or primarily by market capitalization (Dang et al., 2018). The management of most companies is mainly concerned about the influence of firm size on their operations and profitability. The study of Izvorni (2012) stated that firm size is not the primary determinant of performance; other factors, particularly internal and external factors, also contribute to performance. Patrizio and Fabiono (2003) revealed that larger firm size influences productivity growth, allowing a firm to maximize the associated returns from research and development. The study by Daye et al. (2021) stated that the market value of stock primarily measures the effect of size, and firm size measured in that way is typically larger than measurements conducted using other variables, such as total assets or total turnover. Firm size plays a significant role in determining the relationship a given firm has with its internal and external operating environments. The size of a firm is crucial in shaping how it interacts with its inner workings and external surroundings. The scale of a firm increases its power to affect multiple stakeholder groups. Firm size plays a significant role in determining an organization's performance. Larger firms enjoy economies of scale and are mostly able to withstand unfavourable pressures, which helps to lower their failure rate (Pila, 2022). The study of Dogan (2023) on the effect of firm size on profitability of quoted firms found a positive relationship between firm size and profitability. Firm sizes can be measured using the natural logarithm of an organization's total assets (Idris & Adediran, 2023). Therefore, this study adopts moderating firm size to examine the effect of firm characteristics on the financial performance of industrial goods firms in Nigeria, combining two financial variables (liquidity and leverage) and non-financial variables (firm age).

## VI. THEORETICAL FRAMEWORK

Dynamic capability theory (DCT) propounded by Teece et al. (1997) supports this study. This theory was developed to address the weaknesses of Resource-Based Theory. Bleepy et al. (2018) stated that Resource-Based Theory has limitation in interpreting the development of an organizational and the adoption of resources and capabilities can help to access the rapidly changing business environment. Teece et al.(1997) defined DCT as "the firm's ability to integrate, build, and reconfigure internal and external competencies to address rapidly changing environments". DCTs are thus "the organizational and strategic routines by which firms achieve new resource configurations as markets emerge, collide, split, evolve, and die" (Eisenhardt & Martin, 2000).This suggests that organizations with greater dynamic capability tend to perform better than those that lack them. The utilization of dynamic capabilities can create and sustain a competitive advantages by responding effectively to environmental changes. Dynamic capabilities, also called 'first-order' capabilities, lead to intentional product changes, production processes, and market adaptations within an organization. An organization possesses dynamic capabilities when its internal and external characteristics adjust to environmental changes. The theory posits that an organization's systems facilitate the gathering and modification of operations, enabling it to thrive in its environment by creating new ventures and strategic positioning, which grants it a competitive advantage. Firm characteristics are resources that can influence an organization's profitability compared to its competitors in the industry. This theory enhances profitability by creating a dynamic market that embraces new technologies and adapts to the competitive environment. According to Schumpeter (1934), profitability arises when an organization innovates in new areas, whereas profitability diminishes when innovations are replicated. Profitability is ensured when capabilities are innovative in a changing environment.

## VII. EMPIRICAL REVIEW

Many studies have investigated the relationship that exists between liquidity and profitability. Tanko et al. (2024) examined the impact of firm characteristics on environmental performance using multiple regression. They found that liquidity has an insignificant effect on the environmental performance of consumer goods firms. The study indicated that management should not rely on liquidity as a significant factor in determining spending on waste management, as it will not enhance environmental performance. Etukudo et al. (2022) studied how leverage, liquidity, operating expenses, and firm size significantly affect the profit after tax of consumer goods companies listed in Nigeria. The variables demonstrated significant effects on Return on Assets (ROA) and an inverse effect on Return on Equity (ROE). Consequently, the study recommended that consumer goods companies in Nigeria maintain adequate liquidity to strengthen their financial performance. Chabachib et al. (2020) examined the literature supporting the positive effect of liquidity on consumer goods companies on the Indonesia Stock Exchange for the period of 2014-2018. The study utilized path analysis derived from multiple regression, along with bivariate analysis, and concluded that liquidity has a positive and significant effect on profitability. As an intervening variable, profitability also influences companies' liquidity and value. These studies reveal that the relationships between liquidity and profitability are consistent with the theory of firm characteristics.

Some studies have related leverage to profitability. Study of Irwansyah et al. (2023), examined how the COVID-19 pandemic affected consumer goods firms' performance and found that larger firms, mainly in Europe, America, and Asia-Pacific, developed more tenacity and performance during the pandemic. Consequently, companies with debt in their capital structure in the Americas and Asia-Pacific supported performance during the pandemic are better than those without debt.

Isaiah et al. (2022) conducted a study on firm-specific characteristics and financial performance of publicly listed consumer goods companies in Nigeria, focusing on the effect of specific characteristics and profitability. The study found that financial leverage hurts performance, as measured by ROA. In using leverage as a moderating effect in the study of firm characteristics and performance, Adenle et al. (2024) used panel regression, correlation analysis, and descriptive statistics. The study found that leverage had a notable and essential moderating effect on the ROA of consumer goods firms in Nigeria. This study posits that companies should develop optimal financial strategies with less debt risk.

Other studies look at the relationship between firm age and profitability. Azlan et al. (2022) empirically examined firm characteristics and profitability of consumer goods companies in Malaysia and found that firm age had an insignificant relationship with profitability. The study recommends that consumer goods companies should focus less on firm age as it hurts profitability. A similar survey by Nangih et al. (2023) found that age significant and negative affect performance measured by the ROA of listed consumer goods companies in Nigeria. The study recommended that the management of consumer goods firms should be mindful that the older the firm, the more profitable it is.

Accessing the research work of Abel et al. (2024) on firm characteristics and financial performance in Nigeria, they found that firm age has a negative and significant impact on the performance of consumer goods firms; therefore, it is recommended that consumer goods firms adopt other means to have an upper share of the market through diversification.

## VIII. METHODOLOGY

Aquantitative and an ex-post facto research design was adopted for the study. Descriptive statistics, correlations, and multiple regression techniques were utilized to analyze the data. This study utilizes secondary data on the chosen company attributes of Nigerian consumer goods companies from 2013 to 2022, including liquidity, leverage, firm age, and profitability (ROA). The study sample comprises 16 consumer goods companies in the Nigerian Exchange Group (NGX) as of December 31, 2022. A purposive sampling technique was used based on the availability of data. Data were analyzed using Stata 14. Multiple regression models were employed to evaluate our hypotheses. The equation for this model is as follows:

### Model

Model 1: When the moderating variable is not applied

$$

\mathrm{ROA_{it}} = \beta \mathrm{O} + \beta 1 \mathrm{LQD_{it}} + \beta 2 \mathrm{LEV_{it}} + \beta 3 \mathrm{FA_{it}} + \varepsilon_{i} \tag{eq.1}

$$

Model 2: When the Moderating Variable is Applied

$$

\mathrm {R O A i t} = \beta \mathrm {O} + \beta 1 \mathrm {L Q D i t} + \beta 2 \mathrm {L E V i t} + \beta 3 \mathrm {F A i t} + \beta 4 \mathrm {L Q D i t} ^ {*} \mathrm {F S I Z E i t} + \beta 5 \mathrm {L E V i t} ^ {*} \mathrm {F S I Z E i t} + \beta 6 \mathrm {F A i t} ^ {*} \mathrm {F S I Z E i t} + \varepsilon \mathrm {i t}

$$

Where:

$$

ROA = Return on Assets

$$

LQD Liquidity

$$

LEV = Leverage

$$

$$

FSIZE = Firm Size

$$

$\beta O$ Constant to be estimated

$\beta 1 - \beta 6 =$ Coefficient of estimate ε Error term

$$

t = Period

$$

$$

i = Firm

$$

The variables used in this study were adopted from previous studies and are presented in Table 1.

Table 1: Variable Measurement and Justification

<table><tr><td>Variables</td><td>Type</td><td>Measurement</td><td>Justification</td></tr><tr><td>Return on Assets</td><td>Dependent</td><td>Net profit after tax/Total Assets</td><td>Irwansyah et al. (2023)

Yau et al. (2024)</td></tr><tr><td>Liquidity</td><td>Independent</td><td>Current assets to current liabilities</td><td>Kolawole et at.(2021)

Irwansyah et al. (2023)</td></tr><tr><td>Leverage</td><td>Independent</td><td>Total Debt to Total Assets</td><td>Abel et al. (2024)

Isaiah et al. (2022)</td></tr><tr><td>Age</td><td>Independent</td><td>Number of years the company has been in existence</td><td>Wahab et al. (2022)</td></tr><tr><td>Firm Size</td><td>Moderating</td><td>Natural Logarithm of a firm's Total Assets.</td><td>Kolawole et at.(2021)

Onatuyeh et al. (2024)</td></tr></table>

## IX. RESULTS AND DISCUSSION

The study examines the effect of firm characteristics on the profitability of consumer goods Companies in Nigeria. This study used 16 consumer

### a) Descriptive Statistics

goods companies' annual reports listed on the Nigerian Exchange Group (NGX) for 10 years between 2013 and 2022. The panel data amounted to 160 firm-year observations.

Table 2: Descriptive Statistics between Firm Characteristics, Firm Size and Performance

<table><tr><td>Variable</td><td>Obs</td><td>Mean</td><td>Std. Dev.</td><td>Min</td><td>Max</td></tr><tr><td>ROA</td><td>160</td><td>4.99</td><td>7.24</td><td>-18.28</td><td>26.49</td></tr><tr><td>Liquidity</td><td>160</td><td>124.14</td><td>130.61</td><td>7.4</td><td>1587.13</td></tr><tr><td>Lev</td><td>160</td><td>237.55</td><td>461.35</td><td>-298.28</td><td>4792.30</td></tr><tr><td>Firm age</td><td>160</td><td>54.56</td><td>24.7</td><td>9</td><td>123</td></tr><tr><td>Fsize</td><td>160</td><td>7.63</td><td>0.79</td><td>5.51</td><td>8.82</td></tr><tr><td>Lqd* fsize</td><td>160</td><td>921.22</td><td>868.60</td><td>51.5</td><td>10630.46</td></tr><tr><td>lev* fsize</td><td>160</td><td>1858.52</td><td>3758.48</td><td>-2076.31</td><td>41033.06</td></tr><tr><td>fa* fsize</td><td>160</td><td>423.93</td><td>206.03</td><td>49.56</td><td>988.60</td></tr></table>

Table 2 summarizes the descriptive statistics for the variables investigated in this study. As evident in the descriptive result, the profitability of the Nigerian consumer companies has a mean value of $4.99\%$ and a standard deviation for the ROA (profitability) of $7.24\%$. The result also shows a minimum value of $-18.28\%$ and a maximum of $26.49\%$, signifying that the average profitability of the companies has a significant variability. The average liquidity was 124.14 billion, with a standard deviation of 130.61 billion. This result demonstrates substantial liquidity and high variability. The mean leverage is 237.55 billion, with a standard deviation of 461.35 billion, indicating a high degree of debt financing in this sector. The mean of firm size is 7.63 billion, and

### b) Correlation Analysis

the standard deviation of 0.79 billion, suggesting limited variation in firm size among consumer goods companies. The average value for the moderating relationship between firm size and liquidity is 921.22 billion, with a standard deviation of 868.60 billion. The mean for the moderation relationship between firm size and leverage is 1,858.52 billion, accompanying by a standard deviation of 3,758.48 billion. The wide margin between the standard deviation and mean suggests a significant difference.

Finally, the average moderating effect of firm size and age is 423.93 billion, with a standard deviation of 206.03 billion, indicating a relatively small disparity among consumer goods companies' ages.

Table 3: Matrix of Correlations Analysis

<table><tr><td></td><td>ROA</td><td>Liquid</td><td>Lev</td><td>Firm age</td><td>Fsize</td><td>Lqd*FSIZE</td><td>lev*FSIZE</td><td>fa*FSIZE</td></tr><tr><td>ROA</td><td>1</td><td></td><td></td><td></td><td></td><td></td><td></td><td></td></tr><tr><td>Liquidity</td><td>0.1643</td><td>1</td><td></td><td></td><td></td><td></td><td></td><td></td></tr><tr><td>Lev</td><td>-0.1564</td><td>-0.3066</td><td>1</td><td></td><td></td><td></td><td></td><td></td></tr><tr><td>Firm age</td><td>-0.1233</td><td>0.0390</td><td>0.2420</td><td>1</td><td></td><td></td><td></td><td></td></tr><tr><td>Fsize</td><td>0.1201</td><td>-0.3331</td><td>0.2582</td><td>0.4238</td><td>1</td><td></td><td></td><td></td></tr><tr><td>Lqd*FSIZE</td><td>0.1871</td><td>0.9659</td><td>-0.2463</td><td>0.1072</td><td>0.1271</td><td>1</td><td></td><td></td></tr><tr><td>lev*FSIZE</td><td>-0.1423</td><td>-0.3498</td><td>0.9885</td><td>0.2919</td><td>0.3793</td><td>-0.2646</td><td>1</td><td></td></tr><tr><td>fa*FSIZE</td><td>-0.0899</td><td>-0.0667</td><td>0.2544</td><td>0.9587</td><td>0.5965</td><td>0.0425</td><td>0.3298</td><td>1</td></tr></table>

The table illustrates how return on assets, as the dependent variable, correlates with the independent variables of liquidity, leverage, and firm age, both with and without moderation. Consequently, the correlation coefficient matrix ranges from -1 to +1. According to the table, liquidity and profitability show a direct relationship, demonstrating that an increase in liquidity leads to a direct increase in profitability. Likewise, the moderating effects of firm size and liquidity are positive. This result indicates that high liquidity contributes to higher profitability. This suggests that consumer goods companies need liquidity to enhance profitability.

Conversely, the relationships between leverage, firm age, and their moderation with profitability are negative. Indicating an increase in these two variables may adversely affect the profitability of consumer goods companies. This study also reveals that older consumer goods companies may not adopt a profit-enhancement strategy.

### c) Empirical Results

Table 4: Hausman Specification Test

<table><tr><td colspan="2">Test of H0: Difference in coefficients not systematic</td></tr><tr><td>chi2(3) = (b-B)[(V_b-V_B)^(-1)](b-B) = 14.28</td><td>Prob> chi2 = 0.0064</td></tr></table>

Table 5: Breusch and Pagan Lagrangian Multiplier Test for Model 4

<table><tr><td></td><td colspan="2">Var</td><td colspan="2">SD = sqrt(Var)</td></tr><tr><td>Test: Var(u) = 0</td><td colspan="2">chibar2(01) = 114.13</td><td colspan="2">Prob> chibar2 = 0.000</td></tr></table>

Table 6: Heteroscedasticity Tests for Model 4

<table><tr><td colspan="2">Breusch-Pagan/Cook-Weisberg test for heteroscedasticity</td></tr><tr><td colspan="2">Assumption: Normal error terms</td></tr><tr><td colspan="2">Variable: Fitted values of ROA</td></tr><tr><td colspan="2">H0: Constant variance</td></tr><tr><td>chi2(1)</td><td>Prob> chi2</td></tr><tr><td>0.73</td><td>0.3922</td></tr></table>

Table 7: Direct Relationship Regression Result

<table><tr><td></td><td>Coefficient</td><td>T</td><td>P value</td></tr><tr><td>Liquidity</td><td>-0.229</td><td>-3.25</td><td>0.002</td></tr><tr><td>Lev</td><td>0.001</td><td>-0.13</td><td>0.896</td></tr><tr><td>Firmage</td><td>0.224</td><td>0.40</td><td>0.687</td></tr><tr><td>Lqd*FSIZE</td><td>0.034</td><td>3.24</td><td>0.001</td></tr><tr><td>lev*FSIZE</td><td>-0.000</td><td>-0.05</td><td>0.962</td></tr><tr><td>fa*FSIZE</td><td>-0.096</td><td>-1.70</td><td>0.091</td></tr><tr><td colspan="4">F-stat. = 6.18</td></tr><tr><td colspan="4">Prob. 0.00</td></tr></table>

## X. RESULTS AND DISCUSSION

Table 7 shows the direct relationship between the regression results of the moderating effect of firm size on the relationship between firm characteristics and the profitability of consumer goods companies in Nigeria. The results are as follows:

The Hausman Test (Table 4): The validity result of the Hausman test is given in Table 4, with a p-value of 0.0064, confirming the Random-Effect Model is more appropriate than the Fixed-Effect Model.

Breusch and Pagan Lagrangian Multiplier Test (Table 5): This yields a p-value of 0.000, suggesting that the analysis is better suited to the Random-Effect Model as opposed to the pooled effect.

Heteroscedasticity Test (Table 6): The result shows a p-value of 0.3922, which implies that the data have no heteroscedasticity problem. The Null hypothesis for the

Breusch-Pagan/Cook-Weisberg test for heteroscedasticity is that the data is homoscedastic and should not be rejected if the p-value is more than $10\%$.

### Observations

#### 1. Effect of Liquidity and Profitability

The result reveals that liquidity has a negative and significant effect on profitability ( $\beta = -0.229$; $p = 0.002$ ). This finding is consistent with the study by Etukudo et al. (2022), which states that liquidity has a significant relationship with performance. However, this contradicts the findings of Tanko et al. (2024) that see excess liquidity as an indication of the inefficient use of resources that might lead to profit reduction.

#### 2. Effect of Leverage and Profitability

The regression results revealed that leverage has a positive and insignificant effect on profitability ( $\beta = 0.001$; $p = 0.896$ ). This finding suggests that higher leverage could contribute to the profitability of listed consumer goods companies with a limited effect.

This result is consistent with that of Irwansyah et al. (2023) but contradicts that of Isaiah et al. (2022).

#### 3. Firm Age and Profitability

The results also show that firm age has a positive and insignificant effect on profitability ( $\beta = 0.224$, $p = 0.687$ ). This study is in agreement with the studies of Azlan et al. (2022), which see the number of years of incorporation as a burden to improving profitability, but contradicts that of Nangih et al. (2023), which suggests that the greater the age of firms, the more profitability is derived from experience.

#### 4. Moderating Effect of Firm Size

The correlation between profitability, size, and liquidity has been verified, demonstrating a positive increase between profitability and size ( $\beta = 0.034$; $\rho = 0.001$ ). Additionally, the firm size introduction as a moderating variable highlights the balance between liquidity and profitability and confirming that enhanced liquidity can significantly drive the profit margins of consumer goods firms operating in Nigeria.

In analyzing the relationship between leverage and profitability, it was noted that the interaction of firm size with leverage demonstrates a negative and insignificant relation to profitability ( $\beta = -0.00$; $p = 0.962$ ). In this context, it can be assumed that higher leverage tends to diminish profitability due to the increased costs associated with servicing debt.

The coefficient of the interaction between firm size and age is negative and insignificantly related to profitability ( $\beta = -0.096$; $p = 0.091$ ) when moderated by firm size. This suggests that as the firm ages, profits may decrease, primarily due to the advanced age.

## XI. CONCLUSION AND RECOMMENDATIONS

This study aims to examine the relationship between firm characteristics- liquidity, leverage, and firm age- and profitability. It also assesses the moderating effect of firm size on the specific firm characteristics and profitability of listed consumer goods companies in Nigeria. The study recognizes liquidity, leverage, and firm age as exogenous variables, while profitability is treated as an endogenous variable. The findings, which provided insightful analysis, are divided into two parts. First, the panel multiple regression technique indicates that liquidity has a negative and significant effect on profitability. Conversely, leverage and firm age have positive but insignificant impacts on profitability. Second, the study uses the moderating effect of firm size on the relationship between firm characteristics and profitability. The panel regression results indicate that liquidity has a positive and significant effect on profitability, contrary to the earlier results. This suggests that the effective use of liquidity boosts the profitability of this sector. By contrast, leverage and firm age demonstrate a negative and insignificant effect on profitability when moderated by the size of listed consumer goods companies in Nigeria. Based on these findings, this study proposes the following: recommendations:

1. The management of consumer goods companies should put more effort into bolstering their liquidity by preventing unexpected cash falls, ensuring enough cash to bring about a significant positive increase in profitability, especially when the company experiences expansion.

2. Managers of consumer goods companies should balance the benefits of debt against its associated risks to increase profitability.

3. As companies age, their management should focus on achieving sustainable profits so that their continuous survival is not threatened.

### APPENDIXES

Single-user 8-core Stata perpetual license:

Serial number: 10699393

Licensed to: Stata 14

StataCorpLp

Descriptive Statistics

<table><tr><td>Variable</td><td>Obs</td><td>Mean</td><td>Std. Dev.</td><td>Min</td><td>Max</td></tr><tr><td>roa</td><td>160</td><td>4.991875</td><td>7.241041</td><td>-18.28</td><td>26.49</td></tr><tr><td>lqd</td><td>160</td><td>124.1461</td><td>130.6187</td><td>7.4</td><td>1587.13</td></tr><tr><td>lev</td><td>160</td><td>237.5549</td><td>461.352</td><td>-298.28</td><td>4792.3</td></tr><tr><td>fa</td><td>160</td><td>54.5625</td><td>24.70574</td><td>49.56</td><td>988.6</td></tr><tr><td>levsize</td><td>160</td><td>1858.52</td><td>3758.489</td><td>-2076.31</td><td>41033.06</td></tr><tr><td>fafsiz</td><td>160</td><td>423.9351</td><td>206.0362</td><td>49.56</td><td>988.6</td></tr><tr><td>Variable</td><td>Obs</td><td>W</td><td>V</td><td>z</td><td>Prob>z</td></tr><tr><td>roa</td><td>160</td><td>0.97171</td><td>3.479</td><td>2.836</td><td>0.00228</td></tr><tr><td>lqd</td><td>160</td><td>0.37257</td><td>77.165</td><td>9.886</td><td>0.00000</td></tr><tr><td>lev</td><td>160</td><td>0.32929</td><td>82.488</td><td>10.037</td><td>0.00000</td></tr><tr><td>fa</td><td>160</td><td>0.89165</td><td>13.326</td><td>5.891</td><td>0.00000</td></tr><tr><td>levFSIZE</td><td>160</td><td>0.31885</td><td>83.772</td><td>10.073</td><td>0.00000</td></tr><tr><td>fafsize</td><td>160</td><td>0.92625</td><td>9.070</td><td>5.016</td><td>0.00000</td></tr></table>

Normality Test: Shapiro-Wilk W test

Correlation Matrix

<table><tr><td></td><td>roa</td><td>lqd</td><td>lev</td><td>fa</td><td>fsize</td><td>lqdfsize</td><td>levsize</td></tr><tr><td>roa</td><td>1.0000</td><td></td><td></td><td></td><td></td><td></td><td></td></tr><tr><td>lqd</td><td>0.1643</td><td>1.0000</td><td></td><td></td><td></td><td></td><td></td></tr><tr><td>lev</td><td>-0.1564</td><td>-0.3066</td><td>1.0000</td><td></td><td></td><td></td><td></td></tr><tr><td>fa</td><td>-0.1233</td><td>0.0390</td><td>0.2420</td><td>1.0000</td><td></td><td></td><td></td></tr><tr><td>fsize</td><td>0.1201</td><td>-0.3331</td><td>0.2582</td><td>0.4235</td><td>1.0000</td><td></td><td></td></tr><tr><td>lqdfsize</td><td>0.1871</td><td>0.9659</td><td>-0.2463</td><td>0.1072</td><td>-0.1271</td><td>1.0000</td><td></td></tr><tr><td>levsize</td><td>-0.1423</td><td>-0.3498</td><td>0.9885</td><td>0.2919</td><td>0.3793</td><td>0.2646</td><td>1.0000</td></tr><tr><td>fafsize</td><td>-0.0899</td><td>-0.0667</td><td>0.2544</td><td>0.9587</td><td>0.5965</td><td>0.0425</td><td>0.3298</td></tr><tr><td></td><td>fafsize</td><td></td><td></td><td></td><td></td><td></td><td></td></tr><tr><td>fafsize</td><td>1.0000</td><td></td><td></td><td></td><td></td><td></td><td></td></tr></table>

Pooled OLS Regression

<table><tr><td colspan="6">Source | SS df MS Number of obs = 160</td></tr><tr><td colspan="6">Model | 1233.08753 6 205.514588 Prob> F = 0.0004</td></tr><tr><td colspan="6">Residual | 7103.70793 153 46.4294636 R-squared = 0.1479</td></tr><tr><td colspan="6">Total | 8336.79546 159 52.4326759 Adj R-squared = 0.1145</td></tr><tr><td></td><td></td><td></td><td colspan="3">Root MSE = 6.8139</td></tr></table>

<table><tr><td colspan="7">roa | Coef. Std. Err. t P>|t| [95% Conf. Interval]</td></tr><tr><td colspan="7">lqd | -.1061972.0470591 -2.26 0.025 -.1991667 -.0132277</td></tr><tr><td colspan="7">lev | -.0053483.0120676 -0.44 0.658 -.0291889.0184922</td></tr><tr><td colspan="7">fa | -.3172477.175679 -1.81 0.073 -.6643174.029822</td></tr><tr><td colspan="7">lqdfsize |.0156911.0070059 2.24 0.027.0018503.0295319</td></tr><tr><td colspan="7">levysize |.0003395.0014881 0.23 0.820 -.0026003.0032794</td></tr><tr><td colspan="7">fafsize |.0284256.0220829 1.29 0.200 -.0152011.0720524</td></tr><tr><td colspan="7">_cons | 9.619563 1.452417 6.62 0.000 6.750182 12.48894</td></tr></table>

<table><tr><td>Variable</td><td>VIF</td><td>1/VIF</td></tr><tr><td>lqd</td><td>129.39</td><td>0.007729</td></tr><tr><td>lqdfsize</td><td>126.82</td><td>0.007885</td></tr><tr><td>levysize</td><td>107.12</td><td>0.009335</td></tr><tr><td>lev</td><td>106.15</td><td>0.009421</td></tr><tr><td>fafsize</td><td>70.89</td><td>0.014106</td></tr><tr><td>fa</td><td>64.51</td><td>0.015501</td></tr><tr><td>Mean VIF</td><td>100.81</td><td></td></tr></table>

<table><tr><td>Variable</td><td>VIF</td><td>1/VIF</td></tr><tr><td>lqd</td><td>129.39</td><td>0.007729</td></tr><tr><td>lqdfsize</td><td>126.82</td><td>0.007885</td></tr><tr><td>levysize</td><td>107.12</td><td>0.009335</td></tr><tr><td>lev</td><td>106.15</td><td>0.009421</td></tr><tr><td>fafsize</td><td>70.89</td><td>0.014106</td></tr><tr><td>fa</td><td>64.51</td><td>0.015501</td></tr><tr><td>Mean VIF</td><td>100.81</td><td></td></tr></table>

Heteroskedasticity Test Random Effect Test

<table><tr><td colspan="2">Breusch-Pagan/Cook - Weisberg test for heteroskedasticity

Ho: Constant variance

Variables: fitted values of roa</td></tr><tr><td colspan="2">chi2(1) = 0.73</td></tr><tr><td colspan="2">Prob>chi2 = 0.3922</td></tr></table>

Breusch and Pagan Lagrangian multiplier test for random effects

$$

\operatorname{roa} [ \mathrm{i d}, t ] = X b + u [ \mathrm{i d} ] + e [ \mathrm{i d}, t ]

$$

Estimated results:

<table><tr><td></td><td colspan="2">Varsd = sqrt(Var)</td></tr><tr><td>roa</td><td>52.43268</td><td>7.241041</td></tr><tr><td>e</td><td>23.51201</td><td>4.848919</td></tr><tr><td>u</td><td>30.43419</td><td>5.516719</td></tr></table>

$$

\text{Test :} \quad \operatorname{Var} (u) = 0

$$

$$

\operatorname{chibar2}(\theta1) = 114.13

$$

$$

\text{Prob}>\text{chibar2} = 0.0000

$$

Random Effect Model Test

<table><tr><td colspan="2">Random-effects GLS regression Number of obs = 160 Group variable: id Number of groups = 16 min = 10 R-sq: Obs per group: within = 0.1667 between = 0.0224 avg = 10.0 overall = 0.0489 max = 10 Wald chi2(6) = 23.36 corr(u_i, X) = 0 (assumed) Prob> chi2 = 0.0007</td></tr><tr><td>roa | Coef.</td><td>Std. Err.</td><td>z</td><td>P>|z|</td><td colspan="2">[95% Conf. Interval]</td></tr><tr><td>lqd | -.1879629</td><td>.0640208</td><td>-2.94</td><td>0.003</td><td>-.3134413</td><td>-.0624846</td></tr><tr><td>lev | -.0045163</td><td>.0094039</td><td>-0.48</td><td>0.631</td><td>-.0229475</td><td>.013915</td></tr><tr><td>fa |.4019112</td><td>.3173304</td><td>1.27</td><td>0.205</td><td>-.2200449</td><td>1.023867</td></tr></table>

Fixed Effect Model

<table><tr><td colspan="3">Fixed-effects (within) regression Number of obs = 160

Group variable: id Number of groups = 16

R-within = 0.2118 mn = 10

within = 0.2118 min = 10

between = 0.0305 avg = 10.0

overall = 0.0333 max = 10

F(6,138) = 6.18

corr(u_i, Xb) = -0.8977 Prob>F = 0.0000</td></tr></table>

<table><tr><td colspan="7">roa | Coef. Std. Err. t P>|t| [95% Conf. Interval]</td></tr><tr><td colspan="7">lqd | -.2289003.0708189 -3.23 0.002 -.3689307 -.0888699</td></tr><tr><td colspan="7">lev | -.0012313.0093723 -0.13 0.896 -.0197631.0173005</td></tr><tr><td colspan="7">fa |.2243502.5553927 0.40 0.687 -.8738298 1.32253</td></tr><tr><td colspan="7">lqdfsize |.034163.0105324 3.24 0.001.0133373.0549887</td></tr><tr><td colspan="7">levsize | -.0000559.0011587 -0.05 0.962 -.002347.0022352</td></tr><tr><td colspan="7">fafsize | -.0962719.056623 -1.70 0.091 -.2082328.015689</td></tr><tr><td colspan="7">_cons | 30.9055 9.623206 3.21 0.002 11.8775 49.9335</td></tr><tr><td colspan="7">sigma_u | 12.857708</td></tr><tr><td colspan="7">sigma_e | 4.8489186</td></tr><tr><td colspan="7">rho |.87548759 (fraction of variance due to u_i)</td></tr></table>

<table><tr><td></td><td colspan="4">Hausman Test</td></tr><tr><td></td><td colspan="4">--- Coefficients ---</td></tr><tr><td></td><td>(b)</td><td>(B)</td><td>(b-B)</td><td>sqrt(diag(V_b-V_B))</td></tr><tr><td></td><td>fe</td><td>re</td><td>Difference</td><td>S.E.</td></tr><tr><td>lqd</td><td>-.2289003</td><td>-.1879629</td><td>-.0409373</td><td>.03531</td></tr><tr><td>lev</td><td>-.0012313</td><td>-.0045163</td><td>.003285</td><td>.0022778</td></tr><tr><td>fa</td><td>.2243502</td><td>.4019112</td><td>-.1775609</td><td>.4775638</td></tr><tr><td>lqdfsize</td><td>.034163</td><td>.0277779</td><td>.0063851</td><td>.0052506</td></tr><tr><td>levysize</td><td>-.0000559</td><td>.0002699</td><td>-.0003258</td><td>.0002852</td></tr><tr><td>fafsize</td><td>-.0962719</td><td>-.0702939</td><td>-.0259781</td><td>.044037</td></tr></table>

b = consistent under Ho and Ha; obtained from xtreg

B = inconsistent under Ha, efficient under Ho; obtained from xtreg

Test: Ho: difference in coefficients not systematic

$$

\begin{array}{l} \operatorname{chi2}(4) = (b - B) ^ {\prime} \left[ (V _ {-} b - V _ {-} B) ^ {\wedge} (- 1) \right] (b - B) \\= \quad 14.28 \\\text{Prob} > \text{chi2} = 0.0064 \\\end{array}

$$

#### Cross-sectional Dependence Test

Pesaran's test of cross-sectional independence $= 1.005$, $\Pr = 0.3151$

Average absolute value of the off diagonal elements = 0.329

<table><tr><td>S/n</td><td>company</td><td>year</td><td>ROA</td><td>LQD</td><td>LEV</td><td>FA</td><td>LQD*FSIZE</td><td>LEV*FSIZE</td><td>FA*FSIZE</td><td>FSIZE</td></tr><tr><td>1</td><td>Cadbury</td><td>2013</td><td>13.95</td><td>182.33</td><td>79.92</td><td>48</td><td>1392.18</td><td>610.26</td><td>366.50</td><td>7.64</td></tr><tr><td>1</td><td></td><td>2014</td><td>5.25</td><td>87.85</td><td>149.70</td><td>49</td><td>655.32</td><td>1116.65</td><td>365.51</td><td>7.46</td></tr><tr><td>1</td><td></td><td>2015</td><td>4.06</td><td>109.38</td><td>131.31</td><td>50</td><td>815.27</td><td>978.69</td><td>372.67</td><td>7.45</td></tr><tr><td>1</td><td></td><td>2016</td><td>-1.04</td><td>107.70</td><td>156.79</td><td>51</td><td>802.76</td><td>1168.63</td><td>380.12</td><td>7.45</td></tr><tr><td>1</td><td></td><td>2017</td><td>1.06</td><td>113.65</td><td>142.05</td><td>52</td><td>846.40</td><td>1057.85</td><td>387.25</td><td>7.45</td></tr><tr><td>1</td><td></td><td>2018</td><td>2.99</td><td>139.10</td><td>117.16</td><td>53</td><td>1034.83</td><td>871.62</td><td>394.28</td><td>7.44</td></tr><tr><td>1</td><td></td><td>2019</td><td>3.72</td><td>153.25</td><td>112.39</td><td>54</td><td>1143.16</td><td>838.35</td><td>402.81</td><td>7.46</td></tr><tr><td>1</td><td></td><td>2020</td><td>2.81</td><td>140.82</td><td>145.11</td><td>55</td><td>1059.16</td><td>1091.39</td><td>413.66</td><td>7.52</td></tr><tr><td>1</td><td></td><td>2021</td><td>1.03</td><td>139.10</td><td>220.38</td><td>56</td><td>1062.76</td><td>1683.82</td><td>427.87</td><td>7.64</td></tr><tr><td>1</td><td></td><td>2022</td><td>0.98</td><td>122.94</td><td>348.89</td><td>57</td><td>955.99</td><td>2712.93</td><td>443.23</td><td>7.78</td></tr><tr><td>2</td><td>Neatle Nigeria</td><td>2013</td><td>20.57</td><td>125.65</td><td>166.56</td><td>52</td><td>1009.36</td><td>1338.01</td><td>417.74</td><td>8.03</td></tr><tr><td>2</td><td></td><td>2014</td><td>20.96</td><td>84.78</td><td>195.11</td><td>53</td><td>680.36</td><td>1565.83</td><td>425.34</td><td>8.03</td></tr><tr><td>2</td><td></td><td>2015</td><td>19.91</td><td>81.56</td><td>213.67</td><td>54</td><td>658.61</td><td>1725.46</td><td>436.08</td><td>8.08</td></tr><tr><td>2</td><td></td><td>2016</td><td>4.67</td><td>80.75</td><td>449.21</td><td>55</td><td>664.62</td><td>3697.21</td><td>452.67</td><td>8.23</td></tr><tr><td>2</td><td></td><td>2017</td><td>22.97</td><td>94.55</td><td>227.12</td><td>56</td><td>772.26</td><td>1854.94</td><td>457.37</td><td>8.17</td></tr><tr><td>2</td><td></td><td>2018</td><td>26.49</td><td>89.81</td><td>223.24</td><td>57</td><td>737.33</td><td>1832.72</td><td>467.94</td><td>8.21</td></tr><tr><td>2</td><td></td><td>2019</td><td>23.62</td><td>85.26</td><td>324.46</td><td>58</td><td>706.47</td><td>2688.34</td><td>480.56</td><td>8.29</td></tr><tr><td>2</td><td></td><td>2020</td><td>15.93</td><td>91.25</td><td>740.31</td><td>59</td><td>765.67</td><td>6211.88</td><td>495.07</td><td>8.39</td></tr><tr><td>2</td><td></td><td>2021</td><td>12.91</td><td>104.30</td><td>1351.19</td><td>60</td><td>885.64</td><td>11473.44</td><td>509.48</td><td>8.49</td></tr><tr><td>2</td><td></td><td>2022</td><td>11.80</td><td>133.02</td><td>1270.18</td><td>61</td><td>1146.40</td><td>10947.13</td><td>525.73</td><td>8.62</td></tr><tr><td>3</td><td>PZ Cussion</td><td>2013</td><td>7.36</td><td>223.98</td><td>58.62</td><td>114</td><td>1760.32</td><td>460.68</td><td>895.94</td><td>7.86</td></tr><tr><td>3</td><td></td><td>2014</td><td>7.16</td><td>217.23</td><td>63.73</td><td>115</td><td>1705.52</td><td>500.39</td><td>902.89</td><td>7.85</td></tr><tr><td>3</td><td></td><td>2015</td><td>6.78</td><td>215.56</td><td>62.63</td><td>116</td><td>1687.55</td><td>490.29</td><td>908.12</td><td>7.83</td></tr><tr><td>3</td><td></td><td>2016</td><td>2.86</td><td>176.87</td><td>71.49</td><td>117</td><td>1392.28</td><td>562.71</td><td>920.97</td><td>7.87</td></tr><tr><td>3</td><td></td><td>2017</td><td>4.09</td><td>142.94</td><td>99.58</td><td>118</td><td>1137.02</td><td>792.16</td><td>938.66</td><td>7.95</td></tr><tr><td>3</td><td></td><td>2018</td><td>2.17</td><td>144.47</td><td>96.45</td><td>119</td><td>1148.18</td><td>766.53</td><td>945.74</td><td>7.95</td></tr><tr><td>3</td><td></td><td>2019</td><td>1.45</td><td>161.06</td><td>74.72</td><td>120</td><td>1272.81</td><td>590.45</td><td>948.31</td><td>7.90</td></tr><tr><td>3</td><td></td><td>2020</td><td>-9.23</td><td>129.49</td><td>127.00</td><td>121</td><td>1022.28</td><td>1002.65</td><td>955.28</td><td>7.89</td></tr><tr><td>3</td><td></td><td>2021</td><td>1.94</td><td>132.02</td><td>152.77</td><td>122</td><td>1048.37</td><td>1213.12</td><td>968.80</td><td>7.94</td></tr><tr><td>3</td><td></td><td>2022</td><td>6.12</td><td>135.89</td><td>190.07</td><td>123</td><td>1092.19</td><td>1527.69</td><td>988.60</td><td>8.04</td></tr><tr><td></td><td>Unilever</td><td>2013</td><td>10,99</td><td>65.35</td><td>353,90</td><td>90</td><td>499.36</td><td>2704.28</td><td>687.73</td><td>7.64</td></tr><tr><td>4</td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td><td></td></tr><tr><td>4</td><td></td><td>2014</td><td>5.27</td><td>58.30</td><td>511.54</td><td>91</td><td>446.54</td><td>3918.39</td><td>697.05</td><td>7.66</td></tr><tr><td>4</td><td></td><td>2015</td><td>2.38</td><td>60.55</td><td>526.90</td><td>92</td><td>466.24</td><td>4057.51</td><td>708.46</td><td>7.70</td></tr><tr><td>4</td><td></td><td>2016</td><td>4.24</td><td>77.63</td><td>520.12</td><td>93</td><td>610.20</td><td>4088.29</td><td>731.01</td><td>7.86</td></tr><tr><td>4</td><td></td><td>2017</td><td>6.15</td><td>245.15</td><td>59.51</td><td>94</td><td>1981.50</td><td>481.04</td><td>759.78</td><td>8.08</td></tr><tr><td>4</td><td></td><td>2018</td><td>6.93</td><td>234.69</td><td>59.25</td><td>95</td><td>1905.85</td><td>481.15</td><td>771.45</td><td>8.12</td></tr><tr><td>4</td><td></td><td>2019</td><td>-7.16</td><td>205.29</td><td>55.84</td><td>96</td><td>1645.85</td><td>447.67</td><td>769.64</td><td>8.02</td></tr><tr><td>4</td><td></td><td>2020</td><td>-4.33</td><td>230.15</td><td>47.30</td><td>97</td><td>1832.35</td><td>376.59</td><td>772.26</td><td>7.96</td></tr><tr><td>4</td><td></td><td>2021</td><td>0.64</td><td>213.61</td><td>64.67</td><td>98</td><td>1716.01</td><td>519.51</td><td>787.28</td><td>8.03</td></tr><tr><td>4</td><td></td><td>2022</td><td>3.56</td><td>187.62</td><td>733.88</td><td>99</td><td>1519.11</td><td>5942.14</td><td>801.59</td><td>8.10</td></tr><tr><td>5</td><td>VitafoamNIG.Plc.</td><td>2013</td><td>4.12</td><td>108.23</td><td>220.29</td><td>51</td><td>757.46</td><td>1541.64</td><td>356.91</td><td>7.00</td></tr><tr><td>5</td><td></td><td>2014</td><td>3.64</td><td>101.58</td><td>295.53</td><td>52</td><td>719.08</td><td>2092.13</td><td>368.12</td><td>7.08</td></tr><tr><td>5</td><td></td><td>2015</td><td>1.72</td><td>108.96</td><td>212.74</td><td>53</td><td>780.29</td><td>1523.52</td><td>379.55</td><td>7.16</td></tr><tr><td>5</td><td></td><td>2016</td><td>-0.24</td><td>92.76</td><td>280.38</td><td>54</td><td>660.81</td><td>1997.40</td><td>384.69</td><td>7.12</td></tr><tr><td>5</td><td></td><td>2017</td><td>-0.95</td><td>90.80</td><td>297.52</td><td>55</td><td>647.14</td><td>2120.45</td><td>391.99</td><td>7.13</td></tr><tr><td>5</td><td></td><td>2018</td><td>3.75</td><td>115.09</td><td>313.01</td><td>56</td><td>829.10</td><td>2254.96</td><td>403.43</td><td>7.20</td></tr><tr><td>5</td><td></td><td>2019</td><td>17.83</td><td>155.24</td><td>131.53</td><td>57</td><td>1108.43</td><td>939.10</td><td>406.97</td><td>7.14</td></tr><tr><td>5</td><td></td><td>2020</td><td>18.10</td><td>183.80</td><td>139.32</td><td>58</td><td>1348.09</td><td>1021.86</td><td>425.40</td><td>7.33</td></tr><tr><td>5</td><td></td><td>2021</td><td>14.46</td><td>151.90</td><td>145.75</td><td>59</td><td>1139.62</td><td>1093.49</td><td>442.64</td><td>7.50</td></tr><tr><td>5</td><td></td><td>2022</td><td>11.47</td><td>149.50</td><td>151.70</td><td>60</td><td>1135.51</td><td>1152.21</td><td>455.73</td><td>7.60</td></tr><tr><td>6</td><td>Champion Brewery</td><td>2013</td><td>-12.89</td><td>7.40</td><td>-298.28</td><td>39</td><td>51.50</td><td>-2076.31</td><td>271.47</td><td>6.96</td></tr><tr><td>6</td><td></td><td>2014</td><td>-7.87</td><td>43.00</td><td>63.40</td><td>40</td><td>300.23</td><td>442.67</td><td>279.28</td><td>6.98</td></tr><tr><td>6</td><td></td><td>2015</td><td>0.75</td><td>75.65</td><td>45.04</td><td>41</td><td>530.55</td><td>315.85</td><td>287.53</td><td>7.01</td></tr><tr><td>6</td><td></td><td>2016</td><td>5.32</td><td>98.10</td><td>29.86</td><td>42</td><td>685.24</td><td>208.56</td><td>293.37</td><td>6.99</td></tr><tr><td>6</td><td></td><td>2017</td><td>5.13</td><td>132.83</td><td>24.01</td><td>43</td><td>930.36</td><td>168.18</td><td>301.19</td><td>7.00</td></tr><tr><td>6</td><td></td><td>2018</td><td>-2.52</td><td>89.12</td><td>32.15</td><td>44</td><td>625.70</td><td>225.75</td><td>308.93</td><td>7.02</td></tr><tr><td>6</td><td></td><td>2019</td><td>1.53</td><td>91.15</td><td>36.72</td><td>45</td><td>641.83</td><td>258.59</td><td>316.86</td><td>7.04</td></tr><tr><td>6</td><td></td><td>2020</td><td>1.40</td><td>80.27</td><td>41.35</td><td>46</td><td>566.44</td><td>291.78</td><td>324.62</td><td>7.06</td></tr><tr><td>6</td><td></td><td>2021</td><td>7.30</td><td>118.35</td><td>46.28</td><td>47</td><td>843.91</td><td>330.02</td><td>335.13</td><td>7.13</td></tr><tr><td>6</td><td></td><td>2022</td><td>10.26</td><td>159.63</td><td>38.98</td><td>48</td><td>1147.82</td><td>280.27</td><td>345.14</td><td>7.19</td></tr><tr><td>7</td><td>Guiness Plc.</td><td>2013</td><td>9.80</td><td>62.87</td><td>162.95</td><td>51</td><td>508.20</td><td>1317.10</td><td>412.22</td><td>8.08</td></tr><tr><td>7</td><td></td><td>2014</td><td>7.23</td><td>92.30</td><td>193.66</td><td>52</td><td>749.51</td><td>1572.63</td><td>422.27</td><td>8.12</td></tr><tr><td>7</td><td></td><td>2015</td><td>6.38</td><td>72.69</td><td>152.88</td><td>53</td><td>587.82</td><td>1236.26</td><td>428.58</td><td>8.09</td></tr><tr><td>7</td><td></td><td>2016</td><td>-1.47</td><td>71.33</td><td>228.83</td><td>54</td><td>580.40</td><td>1861.92</td><td>439.38</td><td>8.14</td></tr><tr><td>7</td><td></td><td>2017</td><td>1.32</td><td>89.81</td><td>240.07</td><td>55</td><td>733.24</td><td>1960.05</td><td>449.04</td><td>8.16</td></tr><tr><td>7</td><td></td><td>2018</td><td>4.38</td><td>127.45</td><td>74.97</td><td>56</td><td>1043.17</td><td>613.62</td><td>458.34</td><td>8.18</td></tr><tr><td>7</td><td></td><td>2019</td><td>3.41</td><td>121.47</td><td>80.54</td><td>57</td><td>996.86</td><td>661.00</td><td>467.79</td><td>8.21</td></tr><tr><td>7</td><td></td><td>2020</td><td>-8.73</td><td>89.07</td><td>97.36</td><td>58</td><td>726.64</td><td>794.27</td><td>473.19</td><td>8.16</td></tr><tr><td>7</td><td></td><td>2021</td><td>0.74</td><td>90.09</td><td>128.04</td><td>59</td><td>741.23</td><td>1053.54</td><td>485.45</td><td>8.23</td></tr><tr><td>7</td><td></td><td>2022</td><td>7.26</td><td>103.40</td><td>139.68</td><td>60</td><td>861.79</td><td>1164.13</td><td>500.07</td><td>8.33</td></tr><tr><td>8</td><td>International Brew.</td><td>2013</td><td>10.88</td><td>84.34</td><td>145.59</td><td>42</td><td>620.87</td><td>1071.79</td><td>309.19</td><td>7.36</td></tr><tr><td>8</td><td></td><td>2014</td><td>8.64</td><td>84.41</td><td>116.24</td><td>43</td><td>623.60</td><td>858.74</td><td>317.66</td><td>7.39</td></tr><tr><td>8</td><td></td><td>2015</td><td>6.45</td><td>73.48</td><td>147.95</td><td>44</td><td>549.62</td><td>1106.69</td><td>329.12</td><td>7.48</td></tr><tr><td>8</td><td></td><td>2016</td><td>7.92</td><td>50.71</td><td>139.20</td><td>45</td><td>381.59</td><td>1047.51</td><td>338.63</td><td>7.53</td></tr><tr><td>8</td><td></td><td>2017</td><td>2.30</td><td>45.83</td><td>223.97</td><td>46</td><td>350.72</td><td>1713.99</td><td>352.03</td><td>7.65</td></tr><tr><td>8</td><td></td><td>2018</td><td>-1.25</td><td>55.14</td><td>782.45</td><td>47</td><td>468.18</td><td>6644.10</td><td>399.09</td><td>8.49</td></tr><tr><td>8</td><td></td><td>2019</td><td>-7.61</td><td>39.97</td><td>4792.30</td><td>48</td><td>342.25</td><td>41033.06</td><td>410.99</td><td>8.56</td></tr><tr><td>8</td><td></td><td>2020</td><td>-3.32</td><td>42.53</td><td>145.59</td><td>49</td><td>364.58</td><td>1247.97</td><td>420.01</td><td>8.57</td></tr><tr><td>8</td><td></td><td>2021</td><td>-3.76</td><td>57.89</td><td>247.33</td><td>50</td><td>498.39</td><td>2129.42</td><td>430.48</td><td>8.61</td></tr><tr><td>8</td><td></td><td>2022</td><td>-4.47</td><td>85.53</td><td>312.72</td><td>51</td><td>742.79</td><td>2715.97</td><td>442.93</td><td>8.68</td></tr><tr><td>9</td><td>Nigeria Brew.</td><td>2013</td><td>17.04</td><td>45.15</td><td>124.96</td><td>67</td><td>379.42</td><td>1050.03</td><td>563.01</td><td>8.40</td></tr><tr><td>9</td><td></td><td>2014</td><td>12.18</td><td>46.24</td><td>103.08</td><td>68</td><td>395.00</td><td>880.61</td><td>580.91</td><td>8.54</td></tr></table>

<table><tr><td>9</td><td></td><td>2015</td><td>10.68</td><td>38.05</td><td>106.72</td><td>69</td><td>325.41</td><td>912.59</td><td>590.05</td><td>8.55</td></tr><tr><td>9</td><td></td><td>2016</td><td>7.74</td><td>51.69</td><td>121.29</td><td>70</td><td>442.67</td><td>1038.79</td><td>599.53</td><td>8.56</td></tr><tr><td>9</td><td></td><td>2017</td><td>8.65</td><td>56.07</td><td>114.38</td><td>71</td><td>481.16</td><td>981.58</td><td>609.33</td><td>8.58</td></tr><tr><td>9</td><td></td><td>2018</td><td>5.01</td><td>61.77</td><td>132.73</td><td>72</td><td>530.50</td><td>1140.01</td><td>618.40</td><td>8.59</td></tr><tr><td>9</td><td></td><td>2019</td><td>4.21</td><td>51.98</td><td>128.18</td><td>73</td><td>446.17</td><td>1100.22</td><td>626.57</td><td>8.58</td></tr><tr><td>9</td><td></td><td>2020</td><td>1.65</td><td>44.28</td><td>176.62</td><td>74</td><td>382.99</td><td>1527.67</td><td>640.05</td><td>8.65</td></tr><tr><td>9</td><td></td><td>2021</td><td>2.61</td><td>44.09</td><td>182.42</td><td>75</td><td>383.02</td><td>1584.65</td><td>651.50</td><td>8.69</td></tr><tr><td>9</td><td></td><td>2022</td><td>2.13</td><td>38.12</td><td>244.55</td><td>76</td><td>335.18</td><td>2150.16</td><td>668.22</td><td>8.79</td></tr><tr><td>10</td><td>Dangote Sugar</td><td>2013</td><td>13.04</td><td>134.21</td><td>77.02</td><td>13</td><td>1062.94</td><td>610.00</td><td>102.96</td><td>7.92</td></tr><tr><td>10</td><td></td><td>2014</td><td>12.54</td><td>108.55</td><td>80.50</td><td>14</td><td>864.91</td><td>641.38</td><td>111.55</td><td>7.97</td></tr><tr><td>10</td><td></td><td>2015</td><td>11.24</td><td>107.57</td><td>76.49</td><td>15</td><td>861.90</td><td>612.87</td><td>120.19</td><td>8.01</td></tr><tr><td>10</td><td></td><td>2016</td><td>8.07</td><td>111.75</td><td>169.65</td><td>16</td><td>922.02</td><td>1399.72</td><td>132.01</td><td>8.25</td></tr><tr><td>10</td><td></td><td>2017</td><td>20.39</td><td>134.31</td><td>110.36</td><td>17</td><td>1113.44</td><td>914.90</td><td>140.93</td><td>8.29</td></tr><tr><td>10</td><td></td><td>2018</td><td>12.55</td><td>149.38</td><td>76.93</td><td>18</td><td>1231.31</td><td>634.14</td><td>148.37</td><td>8.24</td></tr><tr><td>10</td><td></td><td>2019</td><td>11.54</td><td>129.31</td><td>79.13</td><td>19</td><td>1071.71</td><td>655.82</td><td>157.47</td><td>8.29</td></tr><tr><td>10</td><td></td><td>2020</td><td>10.71</td><td>124.11</td><td>122.94</td><td>20</td><td>1048.00</td><td>1038.11</td><td>168.88</td><td>8.44</td></tr><tr><td>10</td><td></td><td>2021</td><td>6.13</td><td>98.30</td><td>179.49</td><td>21</td><td>834.14</td><td>1523.07</td><td>178.20</td><td>8.49</td></tr><tr><td>10</td><td></td><td>2022</td><td>11.12</td><td>108.86</td><td>187.59</td><td>22</td><td>946.19</td><td>1630.55</td><td>191.22</td><td>8.69</td></tr><tr><td>11</td><td>Flour Mill</td><td>2013</td><td>2.76</td><td>95.15</td><td>234.05</td><td>53</td><td>803.72</td><td>1977.06</td><td>447.70</td><td>8.45</td></tr><tr><td>11</td><td></td><td>2014</td><td>1.81</td><td>78.38</td><td>255.73</td><td>54</td><td>664.10</td><td>2166.77</td><td>457.53</td><td>8.47</td></tr><tr><td>11</td><td></td><td>2015</td><td>2.47</td><td>68.97</td><td>306.45</td><td>55</td><td>588.68</td><td>2615.63</td><td>469.44</td><td>8.54</td></tr><tr><td>11</td><td></td><td>2016</td><td>4.18</td><td>68.12</td><td>260.62</td><td>56</td><td>581.59</td><td>2225.11</td><td>478.12</td><td>8.54</td></tr><tr><td>11</td><td></td><td>2017</td><td>1.83</td><td>82.89</td><td>370.63</td><td>57</td><td>719.81</td><td>3218.52</td><td>494.98</td><td>8.68</td></tr><tr><td>11</td><td></td><td>2018</td><td>3.33</td><td>87.22</td><td>171.12</td><td>58</td><td>750.98</td><td>1473.43</td><td>499.42</td><td>8.61</td></tr><tr><td>11</td><td></td><td>2019</td><td>0.96</td><td>97.64</td><td>176.09</td><td>59</td><td>841.66</td><td>1517.93</td><td>508.59</td><td>8.62</td></tr><tr><td>11</td><td></td><td>2020</td><td>2.63</td><td>127.54</td><td>177.56</td><td>60</td><td>1101.40</td><td>1533.28</td><td>518.13</td><td>8.64</td></tr><tr><td>11</td><td></td><td>2021</td><td>4.72</td><td>145.93</td><td>211.96</td><td>61</td><td>1274.88</td><td>1851.80</td><td>532.92</td><td>8.74</td></tr><tr><td>11</td><td></td><td>2022</td><td>4.20</td><td>140.37</td><td>240.48</td><td>62</td><td>1238.67</td><td>2122.01</td><td>547.10</td><td>8.82</td></tr><tr><td>12</td><td>Honeywell Flour</td><td>2013</td><td>5.13</td><td>74.36</td><td>198.80</td><td>41</td><td>575.84</td><td>1539.45</td><td>317.48</td><td>7.74</td></tr><tr><td>12</td><td></td><td>2014</td><td>5.25</td><td>98.84</td><td>209.78</td><td>42</td><td>771.40</td><td>1637.28</td><td>327.80</td><td>7.80</td></tr><tr><td>12</td><td></td><td>2015</td><td>1.65</td><td>58.46</td><td>234.44</td><td>43</td><td>457.82</td><td>1836.07</td><td>336.77</td><td>7.83</td></tr><tr><td>12</td><td></td><td>2016</td><td>-3.98</td><td>50.34</td><td>364.76</td><td>44</td><td>396.73</td><td>2874.59</td><td>346.76</td><td>7.88</td></tr><tr><td>12</td><td></td><td>2017</td><td>3.80</td><td>49.44</td><td>116.21</td><td>45</td><td>398.14</td><td>935.83</td><td>362.39</td><td>8.05</td></tr><tr><td>12</td><td></td><td>2018</td><td>3.55</td><td>76.62</td><td>121.37</td><td>46</td><td>620.35</td><td>982.73</td><td>372.46</td><td>8.10</td></tr><tr><td>12</td><td></td><td>2019</td><td>0.05</td><td>72.92</td><td>142.65</td><td>47</td><td>593.56</td><td>1161.16</td><td>382.57</td><td>8.14</td></tr><tr><td>12</td><td></td><td>2020</td><td>0.46</td><td>68.94</td><td>148.34</td><td>48</td><td>562.00</td><td>1209.28</td><td>391.31</td><td>8.15</td></tr><tr><td>12</td><td></td><td>2021</td><td>0.76</td><td>74.16</td><td>154.27</td><td>49</td><td>605.71</td><td>1259.94</td><td>400.20</td><td>8.17</td></tr><tr><td>12</td><td></td><td>2022</td><td>-0.66</td><td>78.33</td><td>165.59</td><td>50</td><td>640.40</td><td>1353.84</td><td>408.80</td><td>8.18</td></tr><tr><td>13</td><td>McNichols Plc.</td><td>2013</td><td>7.29</td><td>136.02</td><td>69.42</td><td>9</td><td>749.02</td><td>382.27</td><td>49.56</td><td>5.51</td></tr><tr><td>13</td><td></td><td>2014</td><td>10.72</td><td>93.47</td><td>70.43</td><td>10</td><td>521.36</td><td>392.86</td><td>55.78</td><td>5.58</td></tr><tr><td>13</td><td></td><td>2015</td><td>14.36</td><td>114.34</td><td>61.31</td><td>11</td><td>643.00</td><td>344.79</td><td>61.86</td><td>5.62</td></tr><tr><td>13</td><td></td><td>2016</td><td>12.17</td><td>92.55</td><td>57.56</td><td>12</td><td>525.41</td><td>326.73</td><td>68.12</td><td>5.68</td></tr><tr><td>13</td><td></td><td>2017</td><td>7.09</td><td>89.54</td><td>65.52</td><td>13</td><td>513.21</td><td>375.56</td><td>74.51</td><td>5.73</td></tr><tr><td>13</td><td></td><td>2018</td><td>4.75</td><td>283.74</td><td>147.84</td><td>14</td><td>1678.86</td><td>874.75</td><td>82.84</td><td>5.92</td></tr><tr><td>13</td><td></td><td>2019</td><td>2.37</td><td>304.29</td><td>108.57</td><td>15</td><td>1782.77</td><td>636.08</td><td>87.88</td><td>5.86</td></tr><tr><td>13</td><td></td><td>2020</td><td>2.27</td><td>359.24</td><td>101.27</td><td>16</td><td>2102.26</td><td>592.63</td><td>93.63</td><td>5.85</td></tr><tr><td>13</td><td></td><td>2021</td><td>2.06</td><td>310.45</td><td>92.82</td><td>17</td><td>1813.19</td><td>542.09</td><td>99.29</td><td>5.84</td></tr><tr><td>13</td><td></td><td>2022</td><td>3.02</td><td>343.17</td><td>71.83</td><td>18</td><td>1995.69</td><td>417.74</td><td>104.68</td><td>5.82</td></tr><tr><td>14</td><td>Nascon Allied Ind.</td><td>2013</td><td>23.62</td><td>149.27</td><td>65.85</td><td>40</td><td>1053.35</td><td>464.67</td><td>282.28</td><td>7.06</td></tr><tr><td>14</td><td></td><td>2014</td><td>14.87</td><td>105.18</td><td>99.07</td><td>41</td><td>746.79</td><td>703.43</td><td>291.12</td><td>7.10</td></tr><tr><td>14</td><td></td><td>2015</td><td>12.92</td><td>118.03</td><td>129.89</td><td>42</td><td>851.28</td><td>936.76</td><td>302.91</td><td>7.21</td></tr><tr><td>14</td><td></td><td>2016</td><td>9.82</td><td>120.36</td><td>205.77</td><td>43</td><td>889.54</td><td>1520.86</td><td>317.81</td><td>7.39</td></tr><tr><td>14</td><td></td><td>2017</td><td>17.74</td><td>124.60</td><td>161.14</td><td>44</td><td>931.81</td><td>1205.11</td><td>329.06</td><td>7.48</td></tr><tr><td>14</td><td></td><td>2018</td><td>14.60</td><td>115.39</td><td>154.51</td><td>45</td><td>863.30</td><td>1155.98</td><td>336.66</td><td>7.48</td></tr><tr><td>14</td><td></td><td>2019</td><td>4.77</td><td>105.93</td><td>248.70</td><td>46</td><td>803.79</td><td>1887.09</td><td>349.03</td><td>7.59</td></tr><tr><td>14</td><td></td><td>2020</td><td>6.07</td><td>93.69</td><td>248.35</td><td>47</td><td>716.37</td><td>1898.95</td><td>359.38</td><td>7.65</td></tr><tr><td>14</td><td></td><td>2021</td><td>7.33</td><td>111.88</td><td>176.96</td><td>48</td><td>851.12</td><td>1346.23</td><td>365.16</td><td>7.61</td></tr><tr><td>14</td><td></td><td>2022</td><td>9.85</td><td>128.46</td><td>191.62</td><td>49</td><td>994.84</td><td>1483.94</td><td>379.47</td><td>7.74</td></tr><tr><td>15</td><td>Northern

Nig.Flour</td><td>2013</td><td>6.21</td><td>169.25</td><td>125.66</td><td>38</td><td>1110.13</td><td>824.20</td><td>249.25</td><td>6.56</td></tr><tr><td>15</td><td></td><td>2014</td><td>7.15</td><td>216.97</td><td>84.15</td><td>39</td><td>1413.33</td><td>548.15</td><td>254.05</td><td>6.51</td></tr><tr><td>15</td><td></td><td>2015</td><td>-4.85</td><td>54.29</td><td>20.29</td><td>40</td><td>359.11</td><td>134.20</td><td>264.57</td><td>6.61</td></tr><tr><td>15</td><td></td><td>2016</td><td>-5.01</td><td>288.08</td><td>16.51</td><td>41</td><td>1899.87</td><td>108.88</td><td>270.39</td><td>6.59</td></tr><tr><td>15</td><td></td><td>2017</td><td>-0.37</td><td>76.90</td><td>249.91</td><td>42</td><td>510.42</td><td>1658.73</td><td>278.76</td><td>6.64</td></tr><tr><td>15</td><td></td><td>2018</td><td>-1.03</td><td>110.12</td><td>403.95</td><td>43</td><td>745.74</td><td>2735.58</td><td>291.20</td><td>6.77</td></tr><tr><td>15</td><td></td><td>2019</td><td>-0.63</td><td>104.02</td><td>333.90</td><td>44</td><td>800.79</td><td>2570.46</td><td>338.73</td><td>7.70</td></tr><tr><td>15</td><td></td><td>2020</td><td>0.76</td><td>99.35</td><td>206.68</td><td>45</td><td>688.40</td><td>1432.10</td><td>311.81</td><td>6.93</td></tr><tr><td>15</td><td></td><td>2021</td><td>0.95</td><td>98.77</td><td>164.20</td><td>46</td><td>678.31</td><td>1127.59</td><td>315.89</td><td>6.87</td></tr><tr><td>15</td><td></td><td>2022</td><td>0.61</td><td>96.58</td><td>366.47</td><td>47</td><td>688.10</td><td>2610.83</td><td>334.84</td><td>7.12</td></tr><tr><td>16</td><td>Nig.Enamelware</td><td>2013</td><td>3.36</td><td>154.47</td><td>86.11</td><td>53</td><td>979.85</td><td>546.18</td><td>336.18</td><td>6.34</td></tr><tr><td>16</td><td></td><td>2014</td><td>2.79</td><td>130.30</td><td>148.39</td><td>54</td><td>845.55</td><td>962.95</td><td>350.41</td><td>6.49</td></tr><tr><td>16</td><td></td><td>2015</td><td>1.48</td><td>116.46</td><td>284.69</td><td>55</td><td>780.40</td><td>1907.70</td><td>368.55</td><td>6.70</td></tr><tr><td>16</td><td></td><td>2016</td><td>2.94</td><td>124.59</td><td>221.83</td><td>56</td><td>829.41</td><td>1476.76</td><td>372.79</td><td>6.66</td></tr><tr><td>16</td><td></td><td>2017</td><td>0.77</td><td>117.37</td><td>308.28</td><td>57</td><td>794.05</td><td>2085.62</td><td>385.63</td><td>6.77</td></tr><tr><td>16</td><td></td><td>2018</td><td>-0.07</td><td>124.83</td><td>221.41</td><td>58</td><td>831.41</td><td>1474.67</td><td>386.31</td><td>6.66</td></tr><tr><td>16</td><td></td><td>2019</td><td>-5.51</td><td>117.99</td><td>270.65</td><td>59</td><td>783.63</td><td>1797.56</td><td>391.86</td><td>6.64</td></tr><tr><td>16</td><td></td><td>2020</td><td>-7.03</td><td>1587.13</td><td>499.97</td><td>60</td><td>10630.46</td><td>3348.76</td><td>401.87</td><td>6.70</td></tr><tr><td>16</td><td></td><td>2021</td><td>-18.28</td><td>90.29</td><td>171.15</td><td>61</td><td>557.85</td><td>1057.36</td><td>376.87</td><td>6.18</td></tr><tr><td>16</td><td></td><td>2022</td><td>-9.78</td><td>89.04</td><td>2945.91</td><td>62</td><td>591.61</td><td>19573.59</td><td>411.95</td><td>6.64</td></tr></table>

Generating HTML Viewer...

Funding

No external funding was declared for this work.

Conflict of Interest

The authors declare no conflict of interest.

Ethical Approval

No ethics committee approval was required for this article type.

Data Availability

Not applicable for this article.

Dr. Idogho Abraham Momoh. 2026. \u201cFirm Characteristics and Profitability in Nigerian Consumer Goods Firms: Assessing the Moderating Role of Firm Size\u201d. Global Journal of Management and Business Research - D: Accounting & Auditing GJMBR-D Volume 25 (GJMBR Volume 25 Issue D1): .

This study examines the impact of firm characteristics on the profitability of listed consumer goods companies in Nigeria. The specific objectives are to assess the influence of firm characteristics (liquidity, leverage, and age) on the profitability of these companies in Nigeria, and to explore the moderating effect of firm size on the relationship between firm characteristics and profitability. The ex post facto research design was implemented for this study. The data were collected from secondary sources, particularly the audited financial reports of 16 consumer goods companies listed on the Nigerian Exchange Group as of December 31, 2022, spanning a decade (2013-2022) using purposive sampling techniques. The Descriptive and inferential statistics were employed to analyze the data. The Panel regression analysis was conducted for hypothesis testing, and pre-estimation and post-estimation procedures were executed. The Hausman test confirmed that the random effect model was appropriate. The findings indicate that liquidity has a negative and significant impact on profitability, while leverage and firm age exhibit positive but insignificant effects.

Our website is actively being updated, and changes may occur frequently. Please clear your browser cache if needed. For feedback or error reporting, please email [email protected]

×

This Page is Under Development

We are currently updating this article page for a better experience.

Thank you for connecting with us. We will respond to you shortly.