I. INTRODUCTION

Human Resources (HR) refers to core competencies, and knowledge creation and innovation and the creation of value above all material and financial resources. According to the resource-based as well as the existing theoretical knowledge, the success of contemporary organizations is no longer attributed extensively on physical capital but also to intangible assets such as human capital and therefore, human capital is the driving force of basic sustainable competitive advantage.

In developed countries, it is very common that the parent companies to have a formal disclosure HR practice in their annual report. However, in developing countries such as Bangladesh, and disclosure of human resources side is a very new concept, and it is still in the stage of naive. Although this is not mandatory for the detection of human resources information in the annual report for companies in Bangladesh, it is making some disclosure of human resources voluntarily. There was a dearth of research on the detection of human resources in the context of emerging economies (Khan and Khan,

2010). Human resources is also considered strategic capital, and accounting aspects and reports have become critical to the success of the organization. So far concern far as we know, there have been no acts of careful research Reports on human resources in the annual report of the banking sector in Bangladesh. Thus, this study is trying to find the pattern and extent of disclosure of human resources in the listed banking companies in Bangladesh and to justify the impact of the bank properties over the detection of human resources.

a) Objective

The main objective of this study is to evaluate the human resources disclosure practices in the annual report of the listed banking companies in Bangladesh. To achieve the main objective, the specific objectives of the study are as follows:

To find out disclosure practices of human resources at the bank's annual report.

To determine the extent of human resource information reported in the annual report of the corporate banking

b) Methodology of the study

This study was conducted on the basis of secondary data. Secondary data was collected from the annual reports of the selected listed banking companies in Bangladesh. The study took 30 banking companies enlisted in the Dhaka Stock Exchange (DSE) as the sample, that is, the population was considered of the study. The study was conducted in 2022 and hence data for this study was collected from annual report of 2021 to make study up to date.

II. LITERATURE REVIEW

It has been found disclosure of human resources to be supportive of the stakeholders to take appropriate investment decisions in an era of a knowledge-based economy (Sen 2008; Mamun 2009; Hussain Khan and YESMIN, 2004). HC reports that organizations can benefit by attracting and retaining the best talent and enjoy a competitive advantage (Adams2004; King 2002). As a result, it can be aspects of the preparation of external financial reports of human resources play an important role in facilitating the proper use of human resources in an organization (Mamun 2009). However, due to difficulties in measuring monetary value, it was not reported human resources in traditional financial statements of the organizations (Roslender and Dyson 1992). Therefore, voluntary reporting through annual reports is the best way to inform stakeholders about the value and practice of human resources. Non-disclosure of quantitative human resources may be due to the lack of a single agreed-upon method for measuring information and that only a few People in companies have enough knowledge to identify these statements (Abeysekera 2004; Goh and Li, j 2004).

In 1973, American Accounting Association defined HRA as "the process of identifying and measuring data on human resources and communicate this information to the parties concerned" (AAA 1973). It provides information about human values and resource costs, and works to facilitate the decision-making process, and stimulates decision-makers to adopt the perspective of human resources (Sackman, Flamholtz and Bullen 1989). Companies through the progressive in the world now have realized that human resources practices and disclosure of human resources for the stakeholders have a significant effect on performance (nose, Niemark and Gilani in 2010, Delaney and Huselid 1996; Sing 2004; Wright and McMahan, 1992; Youndt et al. 1996). The study points to the Watson Wyatt (2001) on human capital index that superior human resources practices are not only linked with better financial returns, they are, in fact, a leading indicator of increasing shareholder value. It has gained significant benefits from better information about human resources (Sackman, Flamholtz and Pullen 1989). According to Guthrie (2001), these information resources to be allocated more effectively within organizations may allow increase has enabled the gaps in skills and capabilities to be identified more easily. The study conducted by Khan and Khan (2010) on disclosure practices of HC in 32 largest manufacturing sector and services sectors listed in the Dhaka stock Exchange (DSE) found that the reporting of human resources of the most important companies in Bangladesh practices were not as low as expected. The researchers found training, number of employees, career development, and employment policies as elements of human resources the most common.

III. FINDINGS AND ANALYSIS

This section focuses on methods of detection of human resources, and the location of the detection, measurement and analysis of the detection of human resources contained in the annual report of the banking companies listed in Bangladesh.

a) HR disclosure

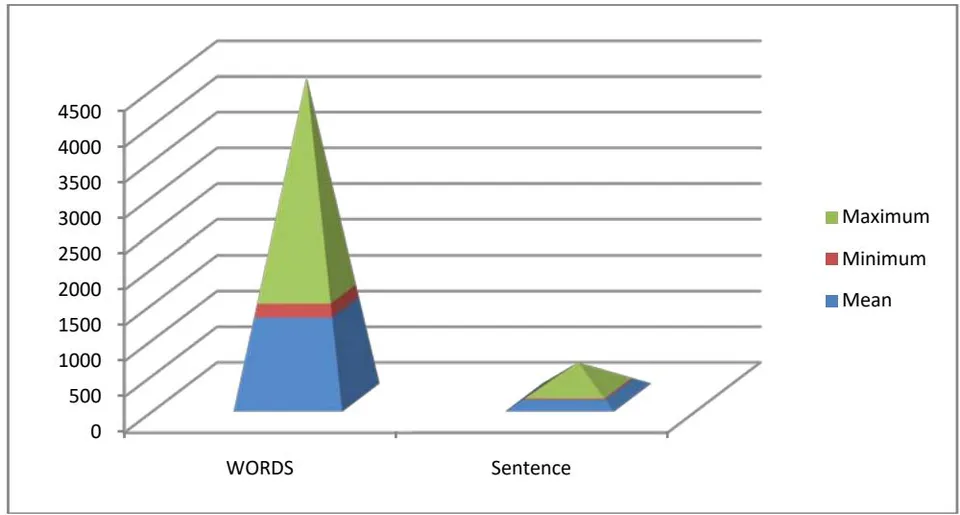

The data in Table NO.1 discover that the banking companies in Bangladesh revealed human resources information using text, chart, graph, and image. In the content analysis it was observed that the average corporate banks use 1264.33 words, maximum 3034 words and a minimum of 187 words; the camel 79.17 average, maximum penalties of 363 and a minimum of sentences 11 in the detection of human resources information in its annual report in maximum 2014. of the sample banks used 500-1,000 words (Appendix 3) and, more specifically, Prime Bank Limited uses a greater number of words and Dhaka Bank Limited the largest number of sentences in this regard (Appendix 4).

| Word | Sentence | |

| Mean | 1264.33 | 118.83 |

| Minimum | 187.00 | 11.00 |

| Maximum | 3034.00 | 363.00 |

b) Location of disclosure

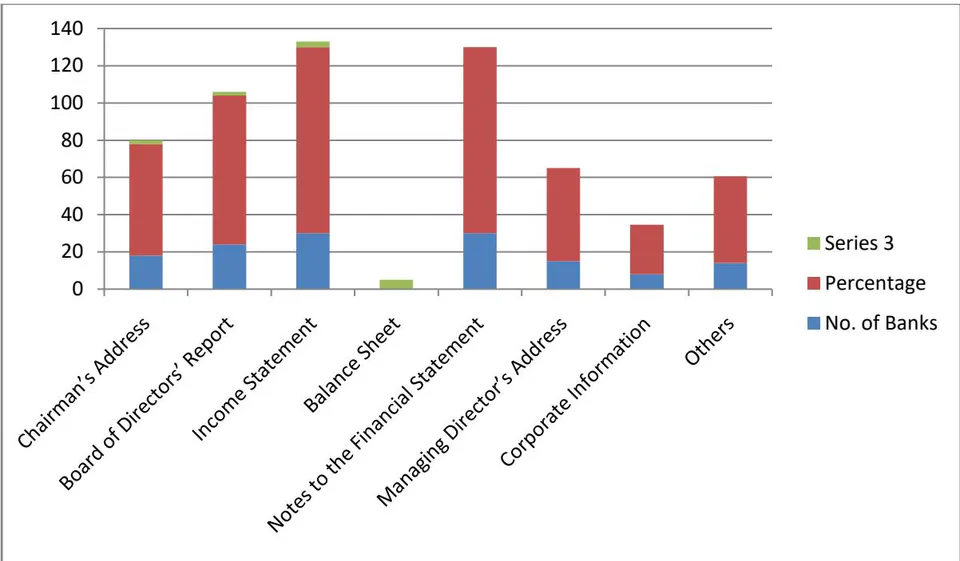

Analyze the detection of human resources information in the annual report for banking company in Bangladesh site, and found that the banking company discloses information on human resources in different locations or parts of the annual report. Table 2 shows that all (100%) banking companies revealed human resources information, which is, especially with respect to financial and human resources in the income statement and the notes to the financial statements information. The use of banking companies also other important parts of the annual report, such as the president title (60.00%), Managing Director of the "address (50.00%), and members of the Board of Director's report (80%). In spite of 46.67% of the banks' sample used for other areas of human resources and information disclosure, but No bank disclose any information on human resources in the balance sheet.

| Location | No. of Banks | Percentage |

| Chairman's Address | 18 | 60.00% |

| Board of Directors' Report | 24 | 80.00% |

| Income Statement | 30 | 100.00% |

| Balance Sheet | 00 | 00% |

| Notes to the Financial Statement | 30 | 100.00% |

| Managing Director's Address | 15 | 50% |

| Corporate Information | 8 | 26.66%% |

| Others | 14 | 46.67 |

c) Heading-wise HR Disclosure

Total has been ranked detection of human resources in its annual report to eight different categories to analyze the best and a number of selected items under each category are not on an equal footing. As the number of items contained in the human resources, finance is a maximum 20 items, so, it was observed that the banking companies in Bangladesh revealed that the maximum amount of information that is considered in the framework of this area (Appendix 1), but in percentage terms, the financial items HR- not in the highest position. Table 3 shows that the average banking companies detect of the human resources information selected, where the average maximum disclosure in the case of human resources development , followed by HR- policy and the average minimum detection it was in HR- health and safety areas . Observed maximum between the maximum disclosures in human resource development , followed by HR- relationship and culture (92.31%) and items HR- policy (90.91%) and the minimum between the minimum disclosure observed in human resources in the field of health and safety (0%) items and items followed by basic human resources (5.85%), and other human resource (0%). There is a

maximum variation in the case of the other terms of human resources (SD = 20.74), followed by items of basic human resources (SD = 18.48) and the minimum difference is in the case of financial items- HR (SD = 9.32).

| HR Policy | Basic HR | HR Fin. | HR Import | Health Safety | HR Develop | HR Relation | HR Other | Total Disclosure | |

| Mean | 75.00% | 49.44% | 66.00% | 53.33% | 19.45% | 91.25% | 60.27% | 32.00% | 59.25% |

| Minimum | 45.46% | 5.85% | 45.00% | 25.00% | 0.00% | 37.50% | 23.08% | 0.00% | 47.50% |

| Maximum | 90.91% | 84.62% | 80.00% | 75.00% | 50.00% | 100% | 92.31% | 80.00% | 78.75% |

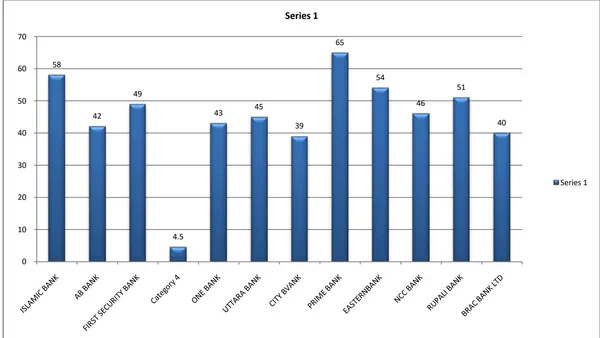

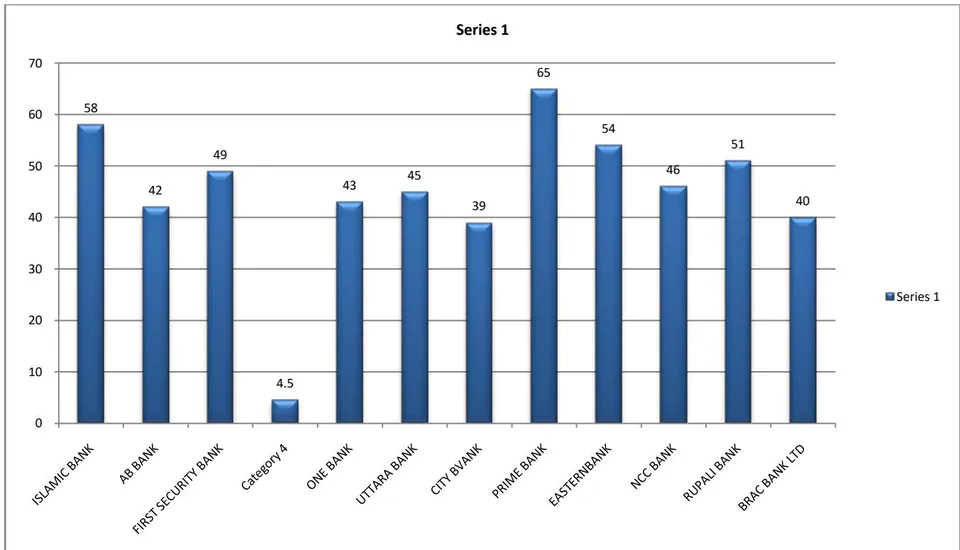

Table 4 the following chart 1 report the detection of human resources general corporate banking in Bangladesh in 2014. The position she found here that the Bank President, Ltd. has achieved the highest position by revealing the 65 (82.28%) of the specific elements of human resources in securing the annual report in 2014. the southern West Bank Limited and Trust Co., the second and third place by revealing the 63 (79.75%) of the specific elements of human resources, respectively. On the other hand, import and Export Co., Ltd. Bank and Standard Bank Limited combed Last place and 20th by the disclosure of only 38 (48.10%) of the specific elements of human resource.

| Rank | Bank Name | Total score | Percentage | Rank | Bank Name | Total Score | Percentage |

| 1 | Prime Bank Ltd | 65 | 82.28 | 12 | Mercantile Bank | 47 | 59.49 |

| 2 | Southeast Bank Ltd | 63 | 79.75 | 12 | NCC Bank Ltd | 46 | 58.23 |

| 3 | Trust Bank Ltd | 60 | 75.94 | 13 | Uttara Bank Ltd | 45 | 56.96 |

| 4 | SJIBL Ltd | 59 | 74.68 | 14 | SIBL | 44 | 55.70 |

| 5 | Dhaka Bank Ltd | 58 | 73.42 | 15 | Bank Asia Ltd | 43 | 54.43 |

| 6 | IBBL | 58 | 73.42 | 15 | One Bank Ltd | 43 | 54.43 |

| 7 | Mutual Trust Bank | 56 | 70.87 | 15 | Pubali Bank Ltd | 43 | 54.43 |

| 8 | Eastern Bank Ltd | 54 | 68.35 | 16 | AB Bank Ltd | 42 | 53.16 |

| 8 | Jamuna Bank Ltd | 53 | 67.09 | 16 | IFIC Bank Ltd | 42 | 53.16 |

| 9 | Premier Bank Ltd | 52 | 65.82 | 17 | PUBLIC Bank | 41 | 51.90 |

| 9 | Rupali Bank Ltd | 51 | 64.56 | 18 | BRAC Bank Ltd | 40 | 50.63 |

| 10 | FSIB Ltd | 49 | 62.03 | 19 | City Bank Ltd | 39 | 49.37 |

| 10 | UCBL | 49 | 62.03 | 19 | ICB Islami Bank | 39 | 49.37 |

| 11 | JANATA BANK | 48 | 60.76 | 20 | EXIM Bank Ltd | 38 | 48.10 |

| 12 | Dutch -Bangla Bank | 47 | 59.49 | 20 | Standard Bank Ltd | 38 | 48.10 |

d) Comparative total Human Resource Disclosure

From Table 4, it is revealed that the highest detection of human resources made by the President of the Bank, Ltd. was and the lowest was detected by the bank, whether Exim Limited and Standard Bank Limited was . Table 5 reveals that the following maximum 12 banks, i.e. of the sample of banks revealed of the specific elements of human resources included in the disclosure of human resources index in this study. Not disclosed any bank less than and more than of selected information and human resources. Only 6 of the sample banks detect - of the information in the annual report. Among a sample of banks, revealed that of them less than and of the sample banks detect more than of the specific elements of human resources.

| Range of total human Resource disclosure | No. of Banks | Percentage of Sample |

| Less than40% | 0 | 00% |

| 40% - 50% | 5 | 16.67% |

| 50% - 60% | 12 | 40.00% |

| 60% - 70% | 7 | 23.33% |

| 70% - 80% | 6 | 20.00% |

| Total | 30 | 100.00% |

If you compare the results of the current study with previous studies Imam (2000); Olssoon (2001); Hussain Khan and Youndt (2004);, it can be said Huang, and Jusoff (2008) that the disclosure of human resources in the banking companies in Bangladesh is in a good position. Finally, voluntary disclosure, the position public disclosure of human resources corporate banking in Bangladesh can be considered to be satisfactory.

IV. RECOMANDATIONS

Among other things, the effects of the main process of this study are: management and accountants banking companies on human understanding is expected to disclose the real resources of this research position, it is expected to be the motive in the disclosure of information resources more human in its annual report to also improve its image and attract more of promising workers for its banks. Researchers in the detection of human resources might be used beneficially issues raised in this article more comprehensive studies in the detection of human resources. It is expected to realize the real position of the detection of human resources corporate banking in Bangladesh, which will help them in the formulation of guidelines and laws in this regard to the disclosure of human resources in a certain framework, and to encourage banking companies in the detection of government regulators practices and other more information about resources Humanity.

V. CONCLUSION

The success of the organizations services geared primarily depends on the efficiency of human resources capabilities. Clients, borrowers, investors and other relevant parties of banking companies evaluate information related to human resources in the selection of a bank and valuable information on human resources of the organization are very important for decision-makers in the modern knowledge-based economy era. Although the disclosure of human resources in the banking companies can be said to be satisfactory level, but the framework of disclosure and the level of disclosure is not the same for all banks. Therefore, to achieve these disclosures in a certain framework, and to encourage more disclosure of information related to human resources, the government and other regulatory bodies should formulate relevant that might create a more favorable working environment provision Shum Resources in the banking companies in Bangladesh. Study some of the restrictions that will be considered in the use and interpretation of the results of the study. Home restrictions for this study include: The study used secondary data only. It is based on the listed banking companies choose deliberate Bangladesh used only and annual reports for one year to study. The study recommends the areas of detection of the following specific human resources for further research: Detection of human resources in the banking sector: the longitudinal evaluation. Comparative detection of human resources: study across the industry in Bangladesh.