I. INTRODUCTION

The company's is often considered a complex entity whose various activities and the requirement of economic performance require regular and permanent control. Given the importance of these issues, it is essential that the diverse internal and external control systems are constantly imposed on the companies' to improve the efficiency and functioning of its activities.

In general, the issuance of an audit report meets different normative and legislative standards [2, 33]. Indeed, each country has its regulations which distinguish it, but also which differ from other countries, which makes necessary the use of a single model of the audit report that could be applied to all contexts, like the international audit report. The role assigned to the external auditor consists of giving his opinion on the accounts and the economic statements of the companies as well as on the various information such as the activity reports provided to the shareholders. He is thus the guarantor of the regularity and the sincerity of the data presented in the context of carrying out the due diligence deemed necessary according to the profession's standards. This description of the auditor's role shows that he is indeed a regulator of the accounting quality and financial information. However, it should be noted that this task requires permanent control of the company's accounting system 1.

The external auditor's report is often considered a significant communication tool for users of financial statements. It is, therefore, interesting to study the auditor's role, as an intermediary between the company and external investors. However, it's possible to understand this role through a theoretical and econometric analysis of the informative content of the auditor's report and, in particular, of the reservations that he has formulated.

This contribution attempts to answer an essential question: what behaviors do shareholders adopt around the dates on which auditors issue reservations on certain accounting items likely to affect the financial statements materially? To provide some answers, we wanted to understand the impact of the auditor's report through the study of the evolution of company prices at the time of its publication.

In the first section, we will make a synopsis of the primary research carried out in the field, the second section will detail the approach followed for the collection of data, the sources of the data, the rules retained in the constitution of the sample, the methodology adopted as well as than statistical tests. A third section after that will present the various tests carried out on the price share behavior around the dates on which the auditor's issue reservations on certain accounting items likely to affect the financial statements and last section significantly will summarize the main results and conclude.

II. OVERVIEW OF PREVIOUS RESEARCH

a) Some preliminary observations

One of the pioneering studies, from the point of view of the methodology used, and the size of the sample of audit reservations, is that of 2, who highlighted three series of methodological difficulties faced by event tests in general and in particular those concerning the effect of the auditor's stock price reservations. The authors show that, on the whole, the informative content of the auditor's report for the American market seems relatively weak, and, limited to the most serious cases of reservations. In another study, [15] concluded that press announcements of audit reserves "subject to" are rare, but if they occur, they induce adverse heritage effects on the stock price concerned. The study done by [17] leads to the same result. However, these results contrast with several other studies, which did not detect this adverse price reaction.

[14](DDHL hereafter) studied the behavior of stock prices around the dates on which auditors express reservations relating to uncertainty regarding certain accounting items, significant delays likely to materially affect the financial statements ("Subject to" qualified audit opinion). The sign and the significance of the abnormal returns of the shares of the companies for which the auditor could not express an opinion, for lack of having the necessary means for his audit work ("disclaimers of audit opinion") are also examined.

The authors consider all of these methodological, conceptual, and procedural problems by developing an original methodology. Indeed, unlike previous studies, DDHL took care to identify the announcement date with great precision.

Their sample is large enough to allow them to analyze the effects on prices of several types of reservations issued by the auditor. The tests on the behavior of cost and the underlying informative content of the reservations issued by the auditor come up against three significant problems: the definition of the date of public announcement, the anticipations, and the previous revelations, and finally, the concomitant revelations.

Regarding the first obstacle, the problem of identifying the announcement date arises in the majority of event studies. The difficulty here stems from the fact that, the first public announcement of a qualified opinion auditor's reservation may occur when the annual accounting result is publicly announced for the first time, when the annual report is available to the public, when the 10-K is revealed to the public or else when the company publishes an announcement in the press stating the auditor's reservations and often the difficulties encountered by the company. Studies that assume that the public announcement of a formulated reservation by the auditor is linked to a fixed date (for example the first announcement of accounting profit in the Wall Street Journal) therefore, have a minimal scope. Research undertaken by the authors reveals that it is difficult, if not impossible, to specify a single event date that represents the date of the public announcement of reserve notices for all companies.

Regarding the second hurdle, a qualified audit opinion is informative only to the extent that it reveals information not embodied in the lectures. Some reservations have been anticipated by the market following previous details. Thus, a reservation opinion which a priori is not good news for the company, can represent positive (negative) information for the market if the latter had expected a more (less) severe judgment from the auditor. The authors did not content themselves with observing the sign and the significance of average abnormal returns. They were able to control the problems related to expectations by constructing initial tests based on the technique of squared standardized forecast errors, developed by 3 and [35].

The problem of concurrent information is also difficult to solve. To reduce the impact, the authors examined abnormal returns over short intervals (3 to 5 days), ensuring that the publication of the accounting results is earlier.

b) Process for changing audit reports in France

For a very long time in France, audit reports have suffered from a negative image among readers who say they do not use them as a privileged source of information. These reports are often assimilated by their readers into a component of financial statements devoid of any actual informational content [38].

"N°2-601: general report on the annual accounts" for the annual accounts of individual companies and standard "No. 2-602: report on the consolidated accounts" for the consolidated statements. The same year, there was the integration by the . Of the second part of the audit report, "Justification of the assessments" of the auditor.

Another milestone in the process of changing the audit report in France corresponds to the introduction of the "NEP 700 and 705." standards respectively in 2007 and 2006. It should be noted that since the LSF in 2003, the standards audit has acquired the status of a ministerial decree which has made it possible to reinforce their applicability. This public nature makes these NSPs opposable to third parties and institutionalizes the normalizing role of the Company4.

c) Perception of the usefulness and use of the audit report by shareholders and other economic actors

Shareholders and investors nowadays seek to diversify the sources of information they consult to form an opinion on the solvency and profitability of the company. Among the documents required, we can cite the certified financial statements, mentioning the auditor's opinion on the reliability of the audited accounts. The place of audit reports among the sources of information mobilized by bankers, for example, has been dealt with by certain researchers) [31,32; 19; 5;25;4; 30]. The main observation resulting from this work reveals that this report is only one element among others that shareholders and potential investors consult [25; 39; 21; 38]. In addition, the usefulness of this report varies according to its informational content, more particularly, according to the nature of the audit opinion expressed.

In France, [38] specifies that the audit report occupies the 3rd place among the sources of information used by bankers, just after the financial statements, the appendices, and economic and sectoral data. In a study by [33]concerning the perception of audit reports with reservations by a sample of users, including bankers, the authors point out that the latter have difficulty understanding the sampling principle "testing" applied by auditors during their account verification. As for [33; 2], they highlight bankers' perception of the level of assurance provided by the audit report. Indeed, the audit opinion constitutes a form of guarantee for users regarding the reliability of the company's accounts. Similarly, this level of commitment is, in some cases, confronted with the materiality of the audit, which favors quantitative techniques, subject to criticism from bankers. These increasingly recurrent criticisms, open the way to materiality of the audit5 based on qualitative factors [29].

In another study carried out, the American context, 6 specify that the extent to which stakeholders use the standard audit report (SAR) depends on their understanding of the message transmitted by the auditor. The authors emphasize the persistence of the gap in bankers' knowledge of the audit message. The common use of the audit report by bankers cannot be explained solely by factors related to its content but also by the very architecture of this document, which lacks consubstantiality. Similarly, the length of the audit report [11; 34] and the brevity of the information it contains [28; 37] seem to be at the origin of the weak attractiveness of this report to users.

The review of these studies allows us to note the existence of a certain ambiguity around the working methods adopted by the auditors, also, in the understanding of specific technical terms 6, which therefore influence their perception of the audit opinion. Indeed, the vagueness that surrounds the auditor's work can then explain the low use of the audit report by bankers or even certain economic operators.

III. INFORMATIONAL AND

COMMUNICATIONAL VALUE OF THE

FRENCH AUDIT REPORT

The audit report has often been the subject of numerous criticisms relating to its informational contribution and the content of the message it conveys. The communicative value of this report is called into question by authors who highlight the limited communicative potential of this report that does not manage to compete with other information media.

a) Use of the audit report by companies

Audit reports used by several professionals has been the subject of several studies [19; 33], mainly in the Anglo-Saxon context. Most of this research shows the low usefulness of the audit report, which unfortunately does not constitute a significant source of information for readers.

In the French context, the work of [22] shows the insufficient attention paid by readers to the financial information contained in audit reports. These raises questions about the communication ensured by the audit reports. One of the elements that may explain the low attractiveness of the audit report is the binary nature of this document, whether or not it validates the financial statements, without providing additional information to these documents. In this sense, [34] specify that the communication model adopted in the audit report is triangular since it is the result of the interaction of the relationships between the person who produces the description (auditor), the message, or the text (the auditor's account). audit) and the referent (financial statements).

In the first study on the audit report, [21] analyses the information content and the communicative function of this document based on Shannon's communication model. The author studies the audit report forms used by professionals such as financial analysts. The main results of this research show that the French professionals interviewed do not use this report in their decision-making processes since it does not allow the audit opinion expressed by the auditor to be transmitted effectively.

b) Insufficient informational value of the audit report

The reliability and completeness of the financial information provided by companies are among the main criteria observed by users. They pay particular attention to the quality of the information disclosed and its informational potential. However, since this document is included in the annual report, it does not arouse the users interest in a significant way, and, it often goes unnoticed in the mass of information communicated. Thus, the audit report is often described as a "standard" report (Mock et al. 2013) with low communicative value [11; 12] with no accurate informational content [33].

The research conducted by [11; 12; 34] in different contexts leads to the same conclusions on several points. The audit report, although it is read by several users, is still considered a binary "pass/fail report," which does not provide additional information. The extent of the criticism leveled at this document, and its common use have prompted some legislators to rethink the form and content of this report so it can better meet the expectations of its readers. Therefore, [33] recommend adding additional information to the audit reporting process to strengthen communication around the work done by the auditor. Other authors [41] justify the low use of the audit report by the nature of the information it contains. The authors point out that the current form of this report lacks transparency since it does not provide information on the anomalies not corrected by the management of the company as well as the cases of disagreement with the management (in addition to those which are considered to be insignificant by the listener).

IV. DATA AND METHODOLOGIES

The study covers the period 2010-2020; it concerns 4,402 annual reports of 691 listed companies, according to the distribution indicated in table 1. The total number of consolidated statements is 2,0497.

| Year | Number of reports | Number of Companies | Year | Number of reports | Number of Companies |

| 2010 | 57 | 46 | 2016 | 610 | 18 |

| 2011 | 162 | 114 | 2017 | 623 | 10 |

| 2012 | 498 | 342 | 2018 | 606 | 17 |

| 2013 | 551 | 90 | 2019 | 107 | 3 |

| 2014 | 575 | 36 | 2020 | 30 | - |

| 2015 | 583 | 15 | 2010 to 2020 | 4 402 | 691 |

The review of the reports led to an initial taxonomy of the opinions expressed. The views expressed are divided into five major groups: reports without reservations and observations (01); reports with reservations (02); reports with comments (03), reports with remarks and findings (04); and finally, writes with refusal to certify .

The reasons that led to the formulation of these reservations are ten in number. Out of 304 counted reports, 288 are used8. Their breakdown by reason is given in Table 2.

| Year | Number of reports |

| Uncertainty | 88 |

| Limitation of work | 39 |

| Accounting principles | 40 |

| Non-recognition of transactions and provisions | 27 |

| Commitment to pensions and leave | 37 |

| Non-compliance with consolidated principles | 44 |

| Refusal to certify | 13 |

| Reports with reservations | 288 |

a) Choosing the date of the event

One of the hurdles of informational content event testing is the problem of identifying the announcement date. Previous research reveals that it is difficult, if not impossible, to specify a single (or pure) event date that represents the date of the public announcement of reserve notices for all companies.

For each of the companies selected, five dates was noted: the date of the General Meeting; the date of signature of the statutory auditor in the annual and consolidated report; the date of the end of the financial year; the date of publication of informations in the Bulletin d'Announces Legales Obligatoires (BALO); the date of announcement of reservations in the press.

It appeared that the report's publication in the BALO occurred after the date of signature by the auditor. As for the publication of reservations in the press, this practice is almost non-existent since only three announcements are listed there. Three hypotheses has been formulated: the first retains a date to fifteen days before the General Meeting of Shareholders (GM-15); the second corresponds to the date of signature by the statutory auditor of the annual and consolidated reports; the third corresponds to the average of the two dates.

Unlike the studies carried out in the United States, this study covers all the reservations expressed on the accounts of listed companies. Despite their interesting methodological approaches, the three most important studies in this area [14; 15; 17] have certain limitations, particularly with regard to the informative content of audit reports.

Apart from the DDHL study, which uses the reservation "Subject to" and "the refusal to certify," and the study by [15], which uses the announcement of reservations in the press, the other works are entirely devoted to examining the first category of "subject" reservations. Part of this limitation is linked to the fact that the different types of reserves are not considered to be material elements, in particular by audit professionals in the United States. However, it should be remembered that opinions such as "adverse opinion" and "refusal to certify" can have a pretty different impact from that of "subject to," even if by the number, the latter is more important. In this study, all the types of reservations and the reasons concerned are examined to carry out various tests in this area.

In addition, in previous studies, several methodological obstacles, among which the determination of the date of event are observed. In this regard, DDHL considers a few critical issues in this type of event study: determining the size of the period, determining the date of publication of audit reports, the effect of concurrent information not taken into account by the models, and the rigorous integration of the phenomenon of anticipation.

The disclosure, for example, in the press of the reservations expressed by the auditor before the publication of the annual reports is rare, even in the United States. The study by [15] concerning this subject is carried out on 114 cases of "subject to" reservations published in the Wall Street Journal. In France, this phenomenon is almost non-existent. The publication of reserves, like other types of accounting information, is observed in the BALO simply after the publication of annual and consolidated reports.

b) Quantification of shareholder reaction

The shareholder's reaction to the publication of audit reports cannot be equated with observed profitability, insofar as other information published simultaneously is likely to affect prices. The methodology of the event study consists of a modeling of "normal" profitability, the "abnormal" part or attributable to the event studied being evaluated by difference with the observed profitability 9.

Simulations by [8; 9] have shown that other simpler variants than the CAPM can be, under certain conditions, as efficient as the most sophisticated models. These results were confirmed by the studies of [16; 26, 27].

In the event of missing data, the missing prices are replaced by the uniform distribution method justified by [24]. The study window or event period is set at thirty sessions on either side of the announcement date.

Different approaches are used to define the norm: the naive system, which consists of equating the standards with the profitability of the market (which is equivalent to assuming that the beta of the security is equal to one), and the market model. In the latter case, several approaches have been used to estimate the beta coefficient: ordinary least squares (OLS), the estimator of 10, that of [36], and finally that of [20]. The index used is weighted by market capitalization. The results obtained using an equally weighted index are not significant. It could be linked to the fact that a substantial number of reservations expressed by auditors relate to large companies. Therefore, when estimating the market model and that of Dimson with an equal-weighted index, the importance of the capitalization of these companies is not reflected.

c) Testing the significance of shareholder reaction

The average return in excess at a given session is formulated by relation 1.

With the average abnormal return of the sample considered over the interval t; , the abnormal return of security i over the interval t and N the number of observations.

The cumulative average abnormal return at date ( ) is defined by relation 2.

A Student's test makes it possible to decide on the significant nature of a return; thus, for a given session , relation 3 gives the Student's tests applied to the average of the excess returns, and relation 4, that applied to the cumulative return mean.

The variance of the average abnormal return is estimated over a period preceding the study window and using two methods. The first assumes the independence of the excess average returns from one security to another: the standard deviation calculated on the time series is expressed according to relationship 5.

With

The second method:

With

The Student statistic as calculated assumes that:

from the assumption of serial independence.

For a significance level set at , the statistic follows a Student law with N-1 degrees of freedom where N is the number of securities in the sample.

V. THE REACTION OF SHAREHOLDERS TO THE PUBLICATION OF AUDIT REPORTS

In a first step, the behavior of share prices is studied around the dates on which the auditors issue reservations on the financial statements. The sign and the significance of the abnormal returns of the shares of the companies for which the auditor was unable to express an opinion are also examined, either because of the seriousness of the reservations observed in the financial statements, or because of the absence of sufficient means to carry out the verifications necessary for its mission.

Most of the studies carried out in the United States use the information contained in the "National Automated Accounting Research System" (NAARS) database to collect data concerning reservations expressed by auditors. In the absence of such a database in France, direct research is undertaken to gather the necessary information concerning this study. It can be considered an essential factor concerning the reliability and validity of the results obtained.

To better explain the impact of reserves on stock prices around the chosen event dates, the study is also conducted on the subgroups detailed in Table 2.

Empirical tests are performed on the following data:

- All reservations and refusals to certify are mentioned in the annual and consolidated reports;

- All reservations not explicitly mentioned in the paragraph of the auditor's opinion, in the annual and consolidated reports. It should be emphasized that certain information mentioned in words in the form of an observation or a remark is the basis of this investigation;

- All the reservations issued for the first time (and also for the second and third) in the annual and consolidated accounts of all the companies in the sample (the method chosen by DDHL);

- All of the reservations (except the first reservation) are expressed in the annual and consolidated accounts of the companies in the sample;

- All the reservations are expressed on the consolidated accounts from the year 2016.

All results assume an accumulation over the interval around the chosen announcement date. To facilitate the presentation of the results, the interval -15 to +25 is retained on the graphs, it can be reduced in certain tables.

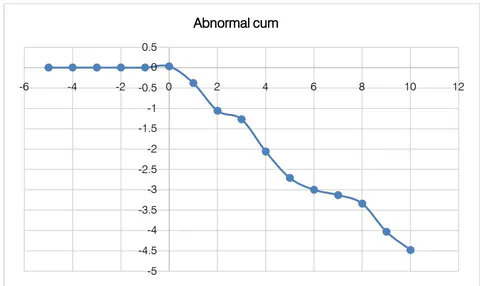

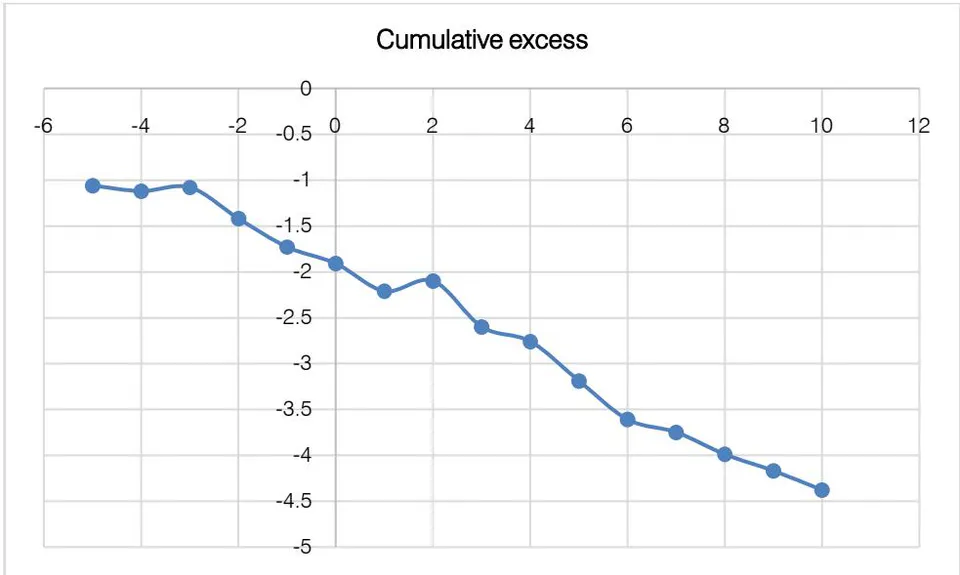

a) The impact of the announcement of reservations and the refusal to certify issued by the statutory auditors In a first step, the average abnormal return and the cumulative average abnormal return were calculated for all the reservations and refusals to certify issued by the auditors. Table 3 shows the reservations and denials to certify mentioned by the statutory auditors in the annual and consolidated reports of the companies in the sample.

The results show an adverse reaction around the event date (from twenty days before the event date until the end of the study period) . The average abnormal return is negative and significant one day before the event date with a t Student of 2.04). At date zero (date AG-15), the average abnormal return is (t Student 0.29) but is insignificant. The magnitude of negative profitability in the following days becomes increasingly essential. From the third day after the date of the event (the return is with a t Student of 2.94 on the date ), these returns are often negative11.

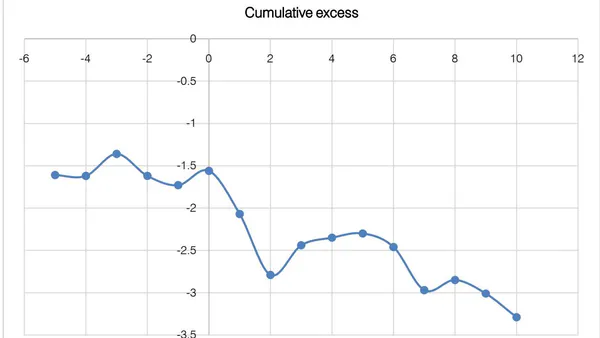

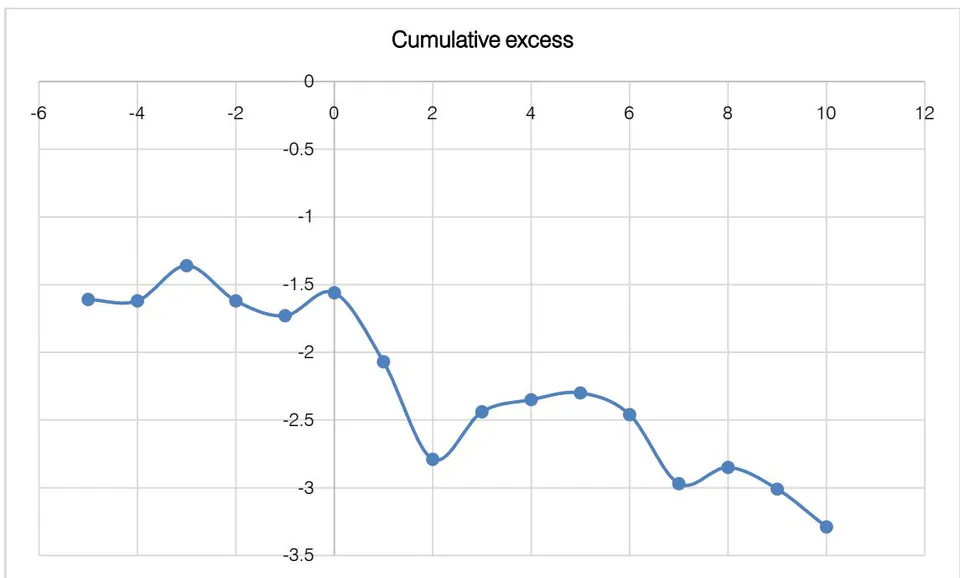

| Date | Excess profitability | Cumulative excess | T-test | Cumulative T-test |

| -5 | -0,30 | -0,82 | -1,93 | -1,04 |

| -4 | 0,06 | -0,76 | 0,41 | -0,94 |

| -3 | -0,13 | -0,76 | -0,01 | -0,97 |

| -2 | -0,19 | -0,96 | -1,27 | -1,14 |

| -1 | -0,32 | -1,28 | -2,04 | -1,49 |

| 0 | 0,04 | -1,23 | 0,29 | -1,42 |

| 1 | -0,24 | -1,47 | -1,55 | -1,67 |

| 2 | 0,11 | -1,36 | 0,71 | -1,52 |

| 3 | -0,46 | -1,82 | -2,94 | -2,00 |

| 4 | -0,12 | -1,94 | -0,76 | -2,10 |

| 5 | -0,22 | -2,17 | -1,43 | -2,31 |

| 6 | -0,43 | -2,60 | -2,77 | -2,74 |

| 7 | -0,04 | -2,64 | -0,25 | -2,75 |

| 8 | -0,24 | -2,88 | -1,51 | -2,95 |

| 9 | -0,09 | -2,78 | 0,60 | -2,81 |

| 10 | -0,27 | -3,05 | -1,73 | -3,05 |

Note: Returns (excess and cumulative) are expressed as a percentage. Abnormal returns are defined concerning the market model; the announcement is assumed to be 15 trading days before the general meeting, and the number of observations is 288.

From the results of the tests of the impact of the announcement of reservations and the refusal to certify issued by the statutory auditors on the annual and consolidated financial statements, three main ideas emerge:

- Average abnormal returns are negative around the different event dates. These returns are significant, especially in the interval -1, +3 (one day before and three days after the event dates);

- Among the event dates used, the one corresponding to 15 days before the general meeting gives the most satisfactory results;

- The application of the two market models, simple and Dimson, leads to often similar results in the case of each event date.

The issuance of reservations and the refusal expressed by the statutory auditors in the annual and consolidated reports have a negative and significant impact around the date of the event. It shows that the market reacts to this lousy news well before the announcement date (15 days before the date of the general meeting). This trend will also continue after the event date.

However, the choice of the announcement date is essential. Among the three hypotheses retained concerning the date of the event, it seems that fifteen days before the date of the general meeting, the announcement of reserves becomes public, and investors react unfavorably to this bad news.

b) The impact of reservations observed but not explicitly mentioned in the paragraph of the auditor's opinion To identify the reservations expressed by the statutory auditors, over four thousand annual and

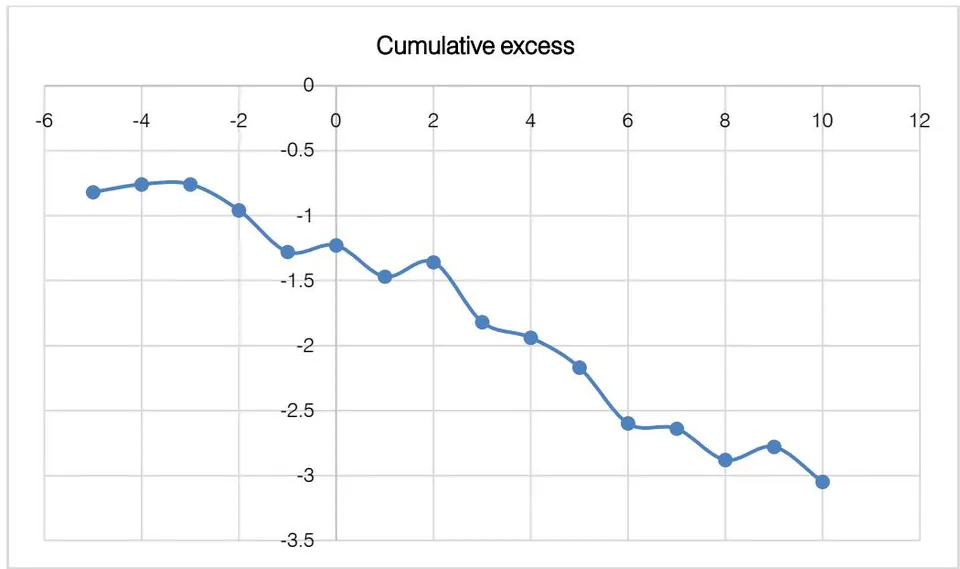

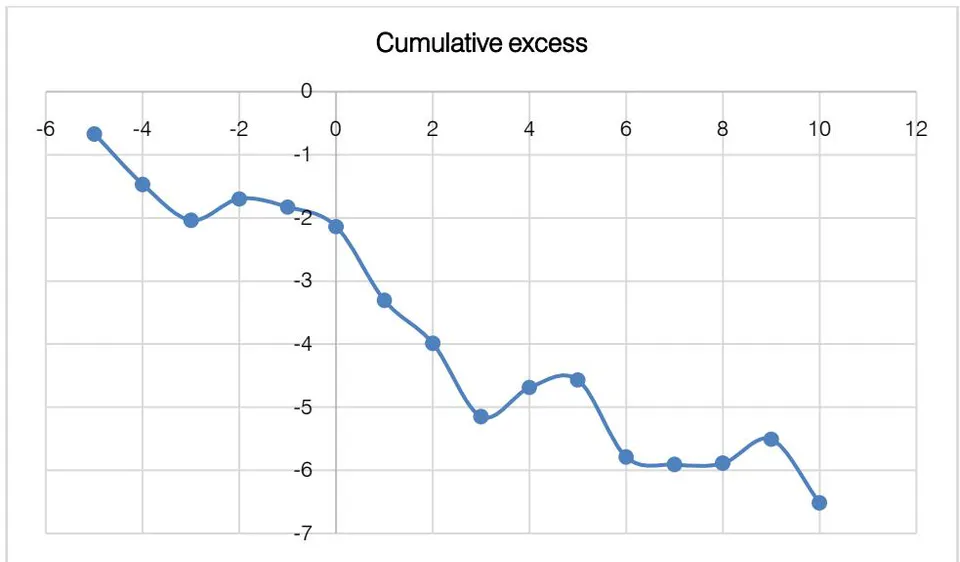

consolidated company reports were examined. Regarding the opinion of the auditors, several types are mentioned in the reports. These are opinions expressed mainly in reservations, observations, remarks, and refusals to certify. In addition, the research carried out reveals certain types of anomalies concerning the conformity of the contents of the reports with the standards established by the CNCC. Among these anomalies, we can mention elements of reservations that are gathered following the standards of the CNCC but that have not been the subject of formal mention in the paragraph reserved for the opinion of the auditor. According to the research, sixty-seven such reserves were observed over the study period. For this category of reservations, the tests concerned are carried out separately, out of caution, only the reservations formally issued by the statutory auditors are retained for the empirical study. However, it is interesting to see whether the publication of information that is not officially expressed in the form of reservations in the reports of the statutory auditors, but which nevertheless contains elements of reservations according to CNCC standards, has an impact or not on stock prices. The same tests carried out on the reservations formally expressed in the reports of the statutory auditors are applied to this type of reservation.

The results show (even though this information is not mentioned in the form of reservations formulated by the auditors in the annual reports) that the market reacts to this type of information. When we use the simple market model with a weighted index (Table 4), for the third event date (the average of two event dates), we observe negative abnormal returns, especially after the event date with a t Student of 2.17 on date

four days after the event date). These returns are often negative and significant in the days following the date of the event10.

Regarding the second and third event dates, the results obtained are not significant until a few days later. However, we still observe negative abnormal returns around the event dates.

| Date | Abnormal profitability | T-Test | Abnormal Cum. | T-test |

| -5 | -0,12 | -0,38 | 0 | 0 |

| -4 | -0,10 | -0,33 | 0 | 0 |

| -3 | -0,18 | -0,56 | 0 | 0 |

| -2 | -0,54 | -1,72 | 0 | 0 |

| -1 | -0,50 | -1,59 | 0 | 0 |

| 0 | 0,02 | 0,08 | 0,03 | 0,08 |

| 1 | 0,01 | 0,32 | -0,38 | -0,69 |

| 2 | -0,14 | -0,44 | -1,06 | -1,50 |

| 3 | -0,03 | -0,09 | -1,27 | -1,52 |

| 4 | -0,69 | -2,17 | -2,06 | -2,17 |

| 5 | -0,53 | -1,67 | -2,71 | -2,58 |

| 6 | -0,45 | -0,44 | -3,00 | -2,63 |

| 7 | -0,72 | -2,27 | -3,13 | -2,56 |

| 8 | -0,02 | -0,07 | -3,34 | -2,56 |

| 9 | -0,71 | -2,25 | -4,03 | -2,93 |

| 10 | -0,29 | -0,93 | -4,48 | -3,09 |

As in the previous case (when the second and third event dates are used), average abnormal returns are observed around the intervals used. These results, although significant, are less good than those obtained by using the event date the day (d0 -15) before the date of the general meeting.

Note that, in the previous table, for a date , the cumulative average abnormal return is calculated by the sum of the average abnormal returns between -t and +t. For example, for t5, this return represents the sum of the average abnormal returns from to .

These results show that the market is reacting to this bad news. However, this negative impact is less significant than when the reservations are clearly expressed by the auditors in the annual reports.

Insofar as these unmentioned reservations are expressed in the form of an observation or a remark which turns into a reservation in the following years, the market may interpret these observations or these remarks as valid reservations.

One of the significant difficulties concerning the interpretation of the reports of French auditors is the existence of several types of information such as observation, remark, observation, etc., that are not expressed in a standardized form. While the existence of such data in auditors' reports is considered valuable, it may increase the risk of misunderstanding by investors and other interested parties.

c) The reservations expressed by the auditors on the accounts of several years

i. The informative content of the first reservation issued by the statutory auditors

When the auditor notices errors, anomalies, or irregularities in the accounting principles application or when he sees one or more uncertainties affecting the annual or consolidated accounts, he expresses his opinion on the statement with a reservation. In subsequent years, the company is likely to take into account the opinion expressed by the auditor and correct any errors or anomalies mentioned in his report. However, there are several cases where the auditor says reservations about the accounts of a company for several successive years. For example, in the previous case, when anomalies that led to reservations or refusal to certify the annual or consolidated accounts for the previous financial year no longer exist at the end of the financial year, the auditor must examine the consequences possible of the impact of the reservations made on the accounts of the previous financial year. Another example relates to the anomaly or error that gave rise to a reservation that remains.

In order to determine the effect of the reservation expressed for the first time in the reports of the Statutory Auditors, the event tests are carried out on all the companies in the sample for which one or more reservations are expressed for the first time. This is consistent with the study done by DDHL, which consider only the first public announcement of a reserve.

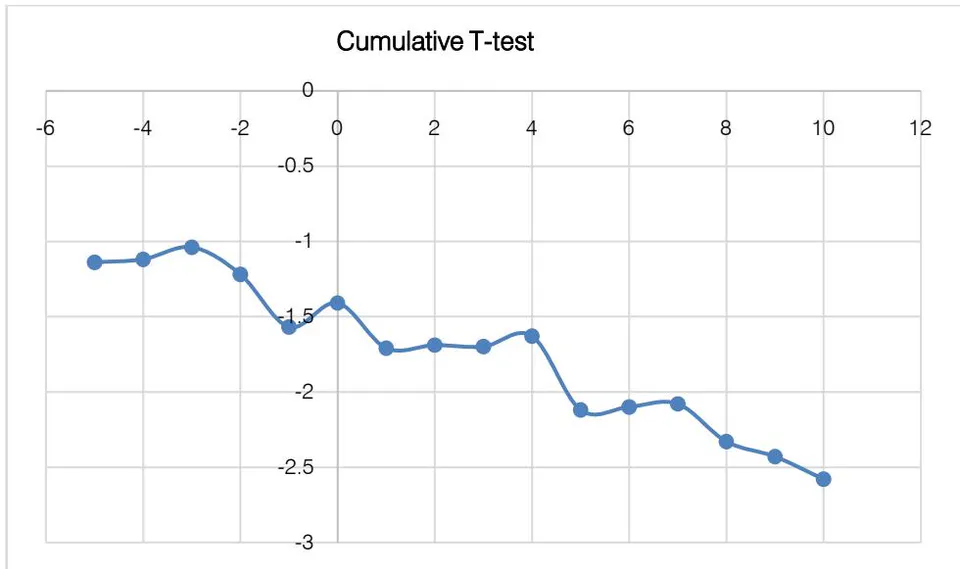

| Date | Excess return | T-test | Cumulative excess | T-test on cumulative |

| -5 | -0,08 | -0,43 | -0,60 | -0,67 |

| -4 | 0,15 | 0,89 | -0,45 | -0,49 |

| -3 | -0,04 | -0,24 | -0,49 | -0,53 |

| -2 | -0,05 | -0,30 | -0,54 | -0,57 |

| -1 | -0,31 | -1,78 | -86 | -0,89 |

| 0 | 0,25 | 1,44 | -0,60 | -0,62 |

| 1 | -0,19 | -1,07 | -0,78 | -0,79 |

| 2 | 0,11 | 0,61 | -0,68 | -0,68 |

| 3- | -0,38 | -2,16 | -1,06 | -1,04 |

| 4 | -0,05 | -0,28 | -1,11 | -1,07 |

| 5 | -0,05 | -0,31 | -1,16 | -1,11 |

| 6 | -0,43 | -2,44 | -1,59 | -1,49 |

| 7 | 0,04 | 0,25 | -1,54 | -1,43 |

| 8 | -0,25 | -1,44 | -1,79 | -1,64 |

| 9 | 0,36 | 2,07 | -1,43 | -1,30 |

| 10 | -0,35 | -1,99 | -1,78 | -1,59 |

Table 5 shows the average abnormal returns around the first event date (AG - 15) using the simple market model. As this table shows, average abnormal returns are negative around the event date. These returns are significant, particularly on the third day after the event date (-0.38% with a Student's t of 2.16) and on date, t6 (-0.43% with a Student's t of 2.44).

Note: Based on the data in Table 5. The points joined by a solid line represent the average cumulative abnormal returns (CMARt). Graph 3: Announcement of reservations and refusal to certify issued for the first time

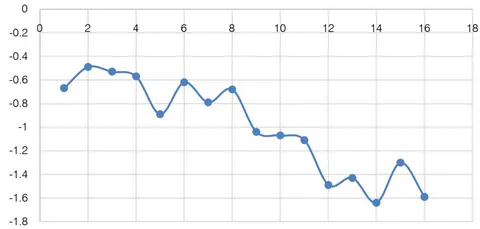

ii. The impact of all the reservations except that of the first reservation

After examining the informative content of the reservations issued for the first time, one can wonder whether all the reservations mentioned in the auditor's reportsin the following years can have an impact on stock prices. These makes it possible to show the importance of the reaction of the stock market to the information mentioned in the reports of the auditors, knowing that the investors already hold information concerning the reserves announced in the first year.

Despite information concerning reservations due to the announcement of this by auditors on company accounts in the past, the following results show that the impact of reservations and refusals to certify on stock prices is always negative and significant. Table 6 shows the average and cumulative abnormal returns around the first event date (AG-15). These returns are unfavorable well before the event date. For example, five days before the event date, profitability is significantly different from zero at the threshold (-0.50% with a t student of 2.04). These results show that investors can anticipate reservations issued by auditors on specific companies, because the information of the first reservation on these companies already exists. In addition, the significance of the results after the event date shows that the renewal of reservations and refusals to certify a very significant impact on the share prices of the companies concerned.

| Date | Excess return | T-test | Cumulative excess | T-test on cumulative |

| -5 | -0,50 | -2,04 | -1,06 | -0,85 |

| -4 | -0,06 | -0,23 | -1,12 | -0,87 |

| -3 | 0,04 | 0,04 | -1,08 | -0,83 |

| -2 | -0,35 | -0,35 | -1,42 | -1,08 |

| -1 | -0,31 | -0,31 | -1,73 | -1,28 |

| 0 | -0,19 | -0,19 | -1,91 | -1,39 |

| 1 | -0,29 | -0,29 | -2,21 | -1,59 |

| 2 | 0,12 | 0,12 | -2,10 | -1,49 |

| 3 | -0,51 | -0,51 | -2,60 | -1,82 |

| 4 | -0,15 | -0,15 | -2,76 | -1,89 |

| 5 | -0,44 | -0,44 | -3,19 | -2,17 |

| 6 | -0,41 | -0,41 | -3,61 | -2,41 |

| 7 | -0,14 | -0,14 | -3,75 | -2,48 |

| 8 | -0,24 | -0,24 | -3,99 | -2,60 |

| 9 | -0,19 | -0,19 | -4,17 | -2,69 |

| 10 | -0,21 | -0,21 | -4,38 | -2,79 |

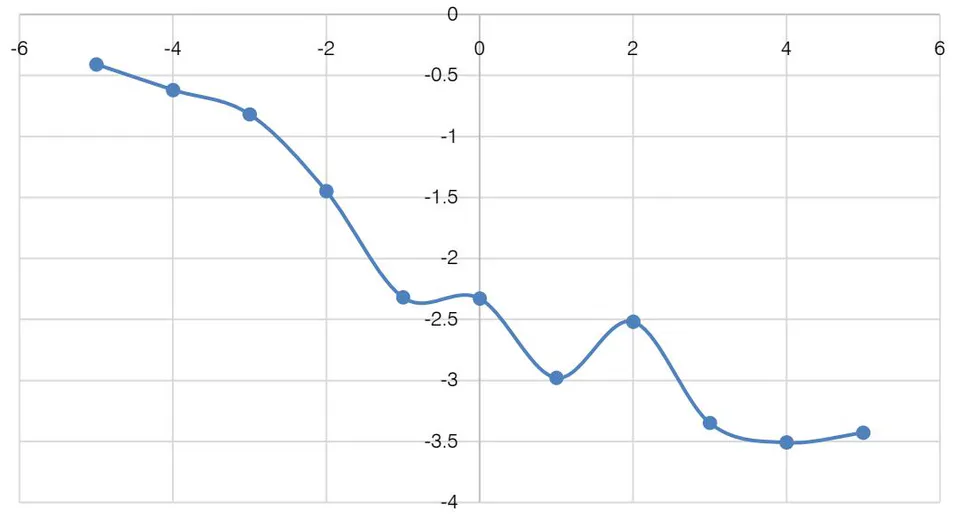

iii. The impact of reservations issued on company accounts for the second time

According to the standards established by the CNCC, when elements give rise to a reservation from the auditor on the financial statements of a company in a specific year and persist the following year, the latter can mention in his report the reservation expressed previously. Three cases are mentioned in the CNCC standards under the heading of "resumption of reservations and refusal to certify from the previous year."

- The reasons for the reservation or refusal remain: the auditor quantifies the impact on the result and

expresses a reservation or refuses to certify the annual accounts.

- The reasons for the reservation or refusal no longer exist due to the corrections made by the company, the modifications have affected the result of the current financial year and justified a new reservation.

- Corrections made by the company corrected the anomaly without impacting the current result. If the statutory auditor deems it necessary to ensure a follow-up, he may mention it in the context of the observations provided for by the regulations in force.

| Date | Excess return | T-test | Cumulative excess | T-test on cumulative |

| -5 | -0,21 | -0,74 | -0,41 | -0,01 |

| -4 | -0,61 | -2,12 | -0,62 | -0,41 |

| -3 | -0,20 | -0,69 | -0,82 | -0,54 |

| -2 | -0,63 | -2,18 | -1,45 | -0,93 |

| -1 | -0,87 | -3,01 | -2,32 | -1,47 |

| 0 | -0,01 | -0,05 | -2,33 | -1,45 |

| 1 | -0,65 | -2,27 | -2,98 | -1,83 |

| 2 | 0,46 | 1,59 | -2,52 | -1,53 |

| 3 | -0,83 | -2,88 | -3,35 | -1,99 |

| 4 | -0,16 | -0,55 | -3,51 | -2,06 |

| 5 | 0,08 | 0,28 | -3,43 | -1,99 |

Note: Returns (excess and cumulative) are expressed as a percentage. Forty-nine reservations and refusals to certify are used. The assumed announcement date is that of the report's signature by the auditors. Abnormal returns are defined regarding the market model .

To examine the impact of the reservations expressed by the auditors on the financial statements of the companies in the following years, various event tests are carried out. Table 7 shows the average and cumulative abnormal returns around the second event date (date of the signature of the report by the auditor) using the simple market model. It should be recalled that the use of the Dimson model leads to similar results.

As shown in Table 7, the reversal of reserves and the refusal to certify the previous year have a negative and very significant impact on the prices of the securities of the companies in the sample. The average abnormal returns are very substantial over the interval - 1, +1, (-0.87% with a t student of 3.01 and -0.65% with a t student of 2.27, respectively).

Note: according to the data in Table 7. The points joined by a solid line represent the cumulative average abnormal returns .

Graph 5: Announcement of reservations and refusal to certify issued for the second time

It means that users of the auditors' reports examine with greater attention the impact of the reservations made on the annual and consolidated accounts for the previous financial year. It is observed that these results are more significant than those of the reservation formulated for the first time. In addition, even if the nature of the reservations is often identical, the impact of these reservations is considered by investors as bad news, mainly when information concerning these reservations in the first year is available.

However, when reservations expressed for the third time (25 reservations) by the auditors on the annual or consolidated financial statements are used, the results (average abnormal returns) are not significant. However, there are always negative returns around the event date.

d) The informative content of the various reasons for reservations mentioned in the annual and consolidated reports As shown in Table 2, 304 reservations and refusals to certify are broken down by reason into ten different classes. For the following six types of reservations observed in the annual or consolidated reports of the companies in the sample, event tests are carried out: uncertainty, limitation of work, accounting principles, non-recognition of operations and provisions, pension commitments, and leave, non-compliance with international regulations. In this work, the results

concerning three types of reservations are presented: "uncertainty," "limitation of work," and "disagreement on accounting rules and principles."14

i. The informative content of the "uncertainty" reservations

In certain circumstances, the company's managers do not have sufficient information to translate a situation according to which a concrete decision can be made. For example, when the auditor prepares his report, there are risks relating to certain transactions which cannot be provisioned, or the amount of which can only be provided to a reasonable approximation because their amount is uncertain or not known, or the probability of occurrence is doubtful.

Whether the risk is provisioned or not, the auditor could not obtain sufficient evidence to justify the amount provided or the absence of provision. In addition, going concern risk may be a particular case of uncertainty.

In the present study, among the 304 reserves that are the subject of event tests, 88 are for reasons of uncertainty. Table 8 shows the results for event tests performed on the uncertainty reserves, choosing the third event date (the average between the first two dates).

| Date | Excess return | T-test | Cumulative excess | T-test on cumulative |

| -5 | -0,26 | -1,02 | -1,61 | -1,21 |

| -4 | -0,01 | -0,04 | -1,62 | -1,19 |

| -3 | 0,26 | 1,01 | -1,36 | -0,99 |

| -2 | -0,26 | -1,02 | -1,62 | -1,16 |

| -1 | -0,11 | -0,43 | -1,73 | -1,22 |

| 0 | 0,17 | 0,66 | -1,56 | -1,08 |

| 1 | -0,51 | -1,97 | -2,07 | -1,41 |

| 2 | -0,71 | -2,75 | -2,79 | -1,87 |

| 3 | 0,35 | 1,34 | -2,44 | -1,62 |

| 4 | 0,09 | 0,36 | -2,35 | -1,53 |

| 5 | 0,08 | 0,18 | -2,30 | -1,48 |

| 6 | -0,16 | -0,64 | -2,46 | -1,56 |

| 7 | -0,51 | -1,95 | -2,97 | -1,86 |

| 8 | 0,12 | 0,45 | -2,85 | -1,76 |

| 9 | -0,15 | -0,59 | -3,01 | -1,83 |

| 10 | -0,29 | -1,10 | -3,29 | -1,98 |

Note: Returns are expressed as a percentage. sixty-nine events are used. The assumed announcement date is set in the middle of the interval between 15 days before the date of the AGM and the date of signature of the reports by the auditor. Abnormal returns are defined regarding the Dimson model, according to the specification:

With RM the index returns, and e the excess returns.

ii. The "work limitation" reserve and its impact on stock market prices

According to the standards established by the CNCC, the limitations constitute an impossibility for the statutory auditor to implement the procedures that he deemed necessary, and those concerning the collection of evidence.

| Date | Excess return | T-test | Cumulative excess | T-test on cumulative |

| -5 | -0,52 | -0,99 | -0,67 | -0,25 |

| -4 | -0,79 | -1,50 | -1,47 | -0,54 |

| -3 | -0,58 | -1,08 | -2,04 | -0,73 |

| -2 | 0,34 | 0,65 | -1,70 | -0,60 |

| -1 | -0,14 | -0,26 | -1,83 | -0,64 |

| 0 | -0,31 | -0,59 | -2,14 | -0,73 |

| 1 | -1,16 | -2,21 | -3,31 | -1,11 |

| 2 | -0,69 | -1,31 | -3,99 | -,132 |

| 3 | -1,16 | -2,20 | -5,15 | -1,68 |

| 4 | 0,46 | 0,88 | -4,69 | -1,51 |

| 5 | 0,12 | 0,23 | -4,57 | -1,45 |

| 6 | -1,22 | -2,23 | -5,79 | -1,81 |

| 7 | -0,12 | -0,23 | -5,91 | -1,82 |

| 8 | 0,02 | 0,04 | -5,89 | -1,78 |

| 9 | 0,37 | 0,71 | -5,51 | -1,66 |

| 10 | -1,01 | -1,92 | -6,52 | -1,94 |

Note: The returns (excess and cumulative) are expressed in percentages. Twenty-five events are used. The assumed announcement date is set 15 days before the AGM date - Abnormal returns are defined regarding the Dimson model, according to the specification:

With RM the index returns, and e the excess returns.

Limitations may be imposed by circumstances or by company management. In the first case, the statutory auditor could not carry out the due diligence he considered necessary. This type of certification is used when the limitation, although significant, is insufficient to refuse to certify. For example, the appointment of the auditor after the end of the financial year prevented him from attending the physical inventories, and he was unable to ascertain the quantities by other means of control.

In the second case, the elements of limitation constitute the offense of obstructing the mission of the auditor and must therefore be exceptional. In general, during the interview on the terms of implementation of the mission, the managers must be informed of the consequences of such a limitation on the general report. As an example, we can also cite the case where the management refuses the auditor to send documents confirming the balances when he considers this procedure essential.

Out of 304 reserves used to perform event tests, 39 are used for limitation reasons of various kinds. These reserves are subject to multiple event tests. Table 9 shows the results obtained by choosing the first date (AG - 15) as the event date.

The reading of the results shows that the average abnormal returns are negative and significant around the date of the event when we consider the impact on stock market prices of the reservation issued for a reason "limitation of work" by the auditor. This profitability is significantly different from zero at the threshold on date t +1 one day after the event date (GA -15). It should be noted that the reason for "limitation of work" is considered a relatively severe type of reservation. For this reason, the average abnormal returns are often negative and significant after the announcement of this type of reserve.

iii. The informative content of the reservation "disagreement on accounting rules and principles"

The auditor, having carried out the due diligence he deemed necessary, noted an accounting irregularity that management refuses to correct. This disagreement is significant enough to have an impact on the certification.

| Date | Excess return | T-test | Cumulative excess | T-test on cumulative |

| -5 | 0,08 | 0,21 | -2,41 | -1,14 |

| -4 | -0,05 | -0,01 | -2,41 | -1,12 |

| -3 | 0,12 | 0,31 | -2,28 | -1,04 |

| -2 | -0,43 | -1,05 | -2,72 | -1,22 |

| -1 | -0,83 | -2,02 | -3,55 | -1,57 |

| 0 | 0,31 | 0,75 | -3,24 | -1,41 |

| 1 | -0,75 | -1,83 | -3,99 | -1,71 |

| 2 | 0,02 | 0,05 | -3,97 | -1,69 |

| 3 | -0,13 | -0,31 | -4,10 | -1,70 |

| 4 | 0,12 | 0,29 | -3,98 | -1,63 |

| 5 | -1,26 | -3,06 | -5,25 | -2,12 |

| 6 | 0,01 | 0,01 | -5,24 | -2,10 |

| 7 | 0,03 | 0,09 | -5,21 | -2,08 |

| 8 | -0,81 | -1,98 | 6,02 | -2,33 |

| 9 | -0,32 | -0,78 | -6,34 | -2,43 |

| 10 | -0,48 | -1,17 | -6,83 | -2,58 |

Note: Returns are expressed in percentages. The supposed announcement date is set 15 days before the GA date. Abnormal returns are defined with reference to the market model .

The examination of the reports of the statutory auditors during the period 2010-2020 makes it possible to identify 40 reservations of reason "disagreement on the rules and accounting principles." These reserves are subject to various event tests (Table 10). The following results relate to the average abnormal returns around the second event date (date of the signature of the report by the auditor).

The results show that the average abnormal returns are negative before and after the event. These returns are significant, especially on the eve of the day event date (-0.83% with a Student's t of 2.02). After the event date, we can also observe an average abnormal return significantly different from zero at the threshold on date (-1.26% with a t student of 3.06), which means that the informative content of the "disagreement on accounting rules and principles" reservation on the price of securities can be considerable. However, the magnitude of these results is less significant than the two aforementioned types of reservations, which is consistent with the level of seriousness of this reservation.

VI. CONCLUSION

In this work, the analysis of 4,402 reports and 2,049 consolidated reports concerning 691 French companies from 2010 to 2020, as well as the systematic study of the reactions of shareholders to the announcement of the reservations issued by the auditors, was undertaken.

The results show that reservations and refusals to certify expressed by auditors hurt stock market prices. However, the choice of the announcement date is essential. Among the three hypotheses retained concerning the date of the event, it seems that fifteen days before the date of the general meeting, the announcement of reserves becomes public, and investors react unfavorably to this bad news.

Regarding the reservations which are not formally expressed by the auditors in the annual or consolidated reports, but which contain elements of reservations according to CNCC standards, the results are also significant. These results show that, when the information elements concerning the reserves are mentioned in the annual and consolidated reports (even if this was not done subject to the reservations expressed in the paragraph reserved for the opinions of the auditors) the market reacts to this bad news.

Moreover, it has been demonstrated that one of the significant difficulties concerning the interpretation of the auditor's reports is the existence of several types of information, such as observation, remark, and observation, which are not expressed, in a standardized form. Although the presence of such data in auditors' reports may be considered valuable, it may nevertheless create confusion.

In the case of refusal to certify, which constitutes the most severe reservation, the results show that the returns observed around the date of the event are not significant, even if they are often negative. However, the results should be interpreted with cautioned given the small sample size.

The comparative results concerning event tests applied in the case of annual and consolidated reports show that, even though the reservations and refusals to certify mentioned in the writings of the auditors on the annual accounts, have an impact negative on stock market prices, the results are often not significant. It can be explained by the fact that the annual report is not the most critical piece of information for investors. Consolidated reports that contain all the information regarding groups of companies are used more often by external investors and bankers in the decision-making process.

Concerning event tests carried out in the case of different types of reserves (uncertainty, limitation of the work of the statutory auditor, non-compliance with accounting principles, non-recognition of operations and provisions, and pension and holidays), as the results show, the average abnormal returns are negative around the date of the event. However, the extent of these results depends on the type of reservation, which is consistent with the level of seriousness of the reservations expressed by the statutory auditors on the accounts and financial statements of the companies.

Unlike the studies carried out in the United States, this study covers all the reservations expressed on the accounts of listed companies. The discrepancy between the results of this study and those of studies carried out in other countries, particularly the United States, undoubtedly finds its explanation in institutional, economic, and cultural factors - not to mention the differences in terms of accounting standardization and auditing practice. However, given the current trend of harmonizing organizational standards and practices globally, it is clear that such contradictions will diminish.

Footnotes

The communication model of Shannon and Weaver (1948) or the general system of communication. (p.4) ↩

For other types of reserves, see Soltani [1993] (p.13) ↩

Unqualified audit report. (p.3) ↩

Source: https://www.cncc.fr (p.3) ↩

The materiality of the audit allows the auditor to determine the extent of the audit work, to make a judgment on the material nature of the accounting anomalies that he may have identified and to ultimately issue an opinion on the reliability and the sincerity of the accounting documents. Materiality is set according to quantitative criteria, but also qualitative criteria defined by professional standards (Lahbari and Manita, 2011). (p.3) ↩

Certain reports concerning the period 2005-2009 were also examined. But due to their small number (34 in total), these reports are excluded from the study. (p.4) ↩

For three types of reserves, due to low numbers, event tests are not carried out. (p.5) ↩

The NEP 700 standard was revised and approved by order of May 26, 2017. (p.3) ↩

The use of the Dimson model with a weighted index leads to similar results, because at date (three days after the first event date), the average abnormal return is significant and different from zero (the return is with a t student of 2.11). (p.9) ↩ ↩2

When using the second and third event date, the results are also significant even one day after the event date. The average abnormal return is with a t Student of 4.12 on date t1 one day before the second event date; date of signature of the auditor's report. In the case of the third event date, the significance of the returns is observed from the first day after date zero (the return of with a t student of 2.84 on date t1, these results are not detailed here, see Soltani [1993]). (p.7) ↩