I. INTRODUCTIONS

The COVID-19 epidemic affected all industries, and its effects continue to be felt, raising questions regarding the future of different markets and the economy. The World Health Organization (WHO) has classified this pathogen as a "global pandemic" (Mohiuddin, 2020). The pandemic COVID-19 has significantly impacted many economies, including Bangladesh. The manufacturing industry, small and medium-sized businesses (SMEs), the financial industry, and individuals have been tremendously hit by the epidemic. Early in March 2020, Covid-19 is discovered for the first time in Bangladesh. The government of Bangladesh has primarily endured ignorance regarding the nature and methods of preventing the proliferation of this infection, just like all other countries. Therefore, immediately following the discovery of this virus in a human body on national soil, a strict lockdown was enforced throughout the country, mimicking Western policies. To keep adequate physical space between residents and implement stringent policies by law enforcement agencies to prevent the spread, the government was initially motivated by an unidentified fear. In 2020, this closure lasted much longer than it should have because it was repeatedly stretched by changes to government notices. Consequently, it also has a significant effect on the nation's commercial operations. Indeed, such severe precautionary steps had an impact on both the actual and monetary industries of the economy. 2020 saw production in all sectors, but particularly in the manufacturing sector, stopped for an extended period due to delays brought on by these extreme anti-spreading measures (Kashem, 2022).

Even before COVID-19, the financial sector of Bangladesh was driven by many issues. As a result, the banking industry struggled to keep the necessary capital sufficiency, make provisions for non-performing loans (NPLs), and comply with international banking rules. The NPLs now account for over of some banks' total loan portfolios, e.g., Basel Accords (Robin et al., 2018). The COVID-influenced era has worsened the situation in the banking industry in Bangladesh (Karim et al., 2023). The COVID-19 epidemic has had a detrimental impact on the financial sector's investment potential and production. Thus, the financial industry also experiences an instant economic decline due to the pandemic. People are alarmed by the prospect of growing NPLs in the global financial system due to the extreme economic decline brought on by the Covid-19 epidemic and the level of debt on a worldwide scale (Park & Shin, 2021).

A severe economic downturn brought on by the COVID-19 epidemic resulted in unemployment issues, which have a negative impact on the transfer of funds and investment in the economy (Gurhy et al., 2020). Thus, some predicted devastating failures have occurred in the banking industry throughout the globe due to the COVID-19 outbreak. Wilson (2020) highlighted the danger of insolvency, increasing failure rates, declining credit growth, and the possibility that funds will be withdrawn due to the global pandemic. The epidemic has worsened the problems with bad debt, shaken administration, delays, and precarious financial conditions. In recent years, the amount of problematic loans in the financial sector has already gotten out of hand. The advent of COVID-19 had an impact on all business operations in the nation, forcing the government to provide financial aid to the impacted businesses in order to aid in their ability to recoup their losses. Due to the decline in the financial standings of the debtors, NPLs do not return to the record after departing institutions (Babu, 2020). The ability of banks to make loans are limited by high problematic debt rates, which also raise stockholder risk by the middle of 2020, the majority of banks were in danger of not generating an operating profit.

The financial sector has been negatively affected by the negative growth of the real estate sector as it is closely connected to the overall economy. However, the government and the central bank of Bangladesh have eased a number of regulatory policies to aid the financial sector and introduced a number of policies to encourage companies and firms. The real estate and financial industries were not entirely capable of being saved by such expansionary policies. The banking industry is likely to make more money if the central bank implements expansionary policies because the banking system mainly transmits the monetary policy of the economy (Kashem, 2022).

Impact Covid-19 appears to affect all sectors, particularly the economic sectors of all affected countries in the world, followed by the severely harmed banking sector (Athari, 2021; Park & Shin, 2021). Even before COVID-19, the banking system of Bangladesh was riven by a number of issues like NPLs and the hit of COVID-19 made the banking industry more vulnerable as it struggled to maintain capital adequacy, make provisions for high NPLs, and comply with international banking regulations during COVID-19-affected period.

The financial sector is the most expanding and influential sector in the economy of Bangladesh. In most instances, the financial industry determines the growth of an economy. In the highly competitive world of finance, banks are persevering by improving their performance and efficacy. The profitability of a bank depends on many external as well as internal factors. These factors attempt to influence the net income of a bank. The banking sector in Bangladesh is recovering from the pre-COVID-19 pace in its activities by regaining the economic boosters all around. A well-capitalized banking sector has a significant role in the pace and scope of economic slump recoveries. Low levels of capital have a detrimental impact on the loan supply in particular (Schularick et al., 2020). Liquidity, as well as profitability, are essential things for any type of firm, which ensures that the company can meet its extant obligations, whereas profitability management ensures that the company can generate sufficient income to cover its expenses (Chowdhury & Barua, 2009).

Bangladesh detected the first verified case of COVID-19 on March 8, 2020. The government adopted immediate measures to shut down the nation for nearly two months. The government suspended all services and prohibited social gatherings, with the exception of emergency services. The army of Bangladesh had been sent to assist the civil administration in containing the virus's spread. Green, yellow, and red zones denoted low-risk, moderate-risk, and high-risk areas, within major cities. The COVID-19 outbreak has brought an immense change in banking operations and the use of technologies in financial sectors all over the world (Pierri & Timmer, 2022; Rahman et al., 2020; Yan et al., 2021), which also makes a possible substantial difference in the liquidity and profitability status of all sorts of banks in Bangladesh. Thus, this paper intends to identify the changes in the profitability and liquidity positions of the commercial in Bangladesh during the pre-COVID-19 and post-COVID-19 pandemic. We have separated the study time span into two parts: the pre-COVID-19 the eight quarters (2018Q1 to 2019Q4), before the pandemic and post-COVID-19 the eight quarters (2020Q1 to 2021Q4) after the pandemic.

II. LITERATURE REVIEW AND HYPOTHESES DEVELOPMENT

Before the COVID-19 pandemic, the liquidity, as well as the profitability positions of banks were impressive. Das et al. (2015) found that the liquidity positions of commercial banks in Bangladesh were increasing rapidly due to rapid economic growth and the application of technologies in banking services. Abdullah (2015) evaluated the liquidity and profitability trend before the outbreak of the COVID-19 pandemic in Bangladesh. It was determined that, on average, all institutions were performing better in liquidity and profitability due to the technology implementation. A study conducted in India by Bharti & Singh (2004) and found that international and private banks possessed greater liquidity and profitability tendencies than public banks. Lartey et al. (2013) found that the liquidity and profitability trends were stable, and there was a positive correlation between the bank's profitability and liquidity. Similar findings have come out through the many other studies conducted in different countries (Al Nimer et al., 2015; Charmler et al., 2018; Ibrahim, 2017; Malik et al., 2016; Vesic et al., 2019).

While Akter & Mahmud (2014) found that there were differences in terms of the liquidity and profitability in the banks in different classes by analyzing the 12 banks— from four different sectors: state-owned commercial banks, Islamic shariah-based banks, international banks, and private commercial banks which are being operated in Bangladesh. Parvin et al.

(2019) found that the private banks in Bangladesh are doing in terms of liquidity. Using the linear regression model, they determined that government banks had variable liquidity, whereas banks in other sectors were stable. In addition, there were variations in profitability across all industries, and the study found no statistical correlation between profitability and liquidity in Bangladeshi banks serving various sectors. Paul et al. (2020) came to the conclusion that, generally speaking, liquidity influence has a significant impact on the revenue of the private commercial banks in Bangladesh.

The profitability and liquidity of banks after the COVID-19 epidemic were not the same as they were in pre-COVID-19, as found in many studies conducted at home and abroad. Gazi et al. (2022) discovered that the profitability of listed private commercial banks in Bangladesh had been affected by high NPLs rates, maintaining more liquid assets, a substantial amount of hedging capital, and insufficient bank capacities. As a result, the banking sector of Bangladesh should be mindful of diversifying its holdings, keeping cash on hand when it's needed and appropriately authorizing and monitoring loans. Additionally, their research suggests that a lower level of leverage can boost the profitability of banks; as a result, banks should raise the necessary cash by issuing stocks.

Mohammed et al. (2022) made an effort to a study focusing on the bank spread, COVID-19, and net interest margins through the analysis using the Thomson Reuters DataStream database from 2016 to 2021 and imbalanced quarterly bank data of the major five economies in Europe and South Asia and found that the bank spreads decreased in Asia, whilst bank spreads increased in the EU during COVID-19. There is evidence that foreign banks have an arbitrage chance to engage in rising higher spreads. This would strengthen the financial systems of these nations, reducing net interest margins and bringing them closer to those of industrialized countries.

Jordà et al. (2021) have used newly created data for the balance sheet of banks in seventeen countries since 1870, the first comprehensive analysis of the long-term history of the capital structure of modern banking. They have found that the capitalization of the financial sector influences the macroeconomic rate of economic recovery. They research the connection between capital structure and financial volatility in addition to creating generalized facts about the shifting financing composition of banks. No correlation between more cash and a reduced chance of a financial catastrophe is found. However, as credit comes back more easily, countries with good-capitalized banking systems rebound from financial disasters more quickly.

Karim et al. (2021) discovered that COVID-19 had a significant adverse impact on the economic sectors of Bangladesh. To evaluate the liquidity, they used liquidity measures, and to assess the financial stability of non-manufacturing businesses, they updated Altman's Z-Score Model. To evaluate the effect, the rates are contrasted before and after the COVID-19 era. After the start of the epidemic, they discovered a decline in their financial and solvency positions. Even though the banks' cash levels and financial situation were terrible before the epidemic started, they got even worse in the second quarter of 2020. The majority of banks have weak capital balances and solvency levels. Comparatively, Islamic banks are in worse financial shape than conventional commercial banks, and all banks are in the danger zone overall. Due to the effects of COVID-19 on the Bangladesh banking sector, Barua & Barua (2021) predicted a decline in the risk-weighted value of assets, capital adequacy ratios, and interest revenue at the individual bank and sector levels for all banks. In addition, they recommended immediate and creative strategies to prevent a widespread and spreading financial meltdown in Bangladesh.

Li et al. (2020) attempted a study on the liquidity shock that banks in the United States suffered very much. They have found that as the COVID-19 crisis approaches, firms withdraw enormous quantities of money in expectation of cash flow and financial troubles. Small banks are experiencing a slower increase in liquidity needs. Because the largest banks service the largest firms, the increased demand for liquidity is centered on them, leading to the lack of liquidity. Banks, on the other hand, have dealt with it by relying on the Federal Reserve and deposits.

Demirgünç-kunt et al. (2020) discovered, by analyzing bank stock returns, government pronouncements, liquidity premiums, and the COVID-19 pandemic, that COVID-19's adverse effects on the banking industry were more pronounced and persisted longer than on other financial sectors. The authors discovered that despite the fact that larger, publicly traded institutions had greater liquidity and more potent cooperative abilities, their stock returns dropped as a result of having to cope with the COVID-19 disruption.

Dadoukis et al. (2021) found that banks that used modern IT before the pandemic fared better during the COVID-19 timeframe. They concentrated on the technologies employed by banks to provide a market-adjusted return. Their findings support that technology may promote financial stability by improving bank performance, liquidity, and resilience. While Albuquerque et al. (2020) discovered that in the first quarter of 2020, equities with higher environmental and social (ES) ratings had substantially higher returns, decreased return fluctuation, and increased operating profit margins. The findings of the study support the notion that increased investor and consumer loyalty is a necessary condition for the resilience of ES companies. Since they accounted for time-invariant unobservable firm impacts in the difference-in-differences regression analyses for high and low ES firms, it is unlikely that systematic unobservable differences between high and low ES firms explain their findings.

Li et al. (2020) discover that Paycheck Protection Program(PPP) lending by banks rises with typical metrics of association lending: greater for small banks, past expertise in the local market, commitment lending, and core deposits. Their findings suggest a new advantage for businesses with close ties with their banks, which are regularly the primary channel for accessing government subsidies. Using the framework of bank-level lending, they develop a local supply metric that influences the structure of banking systems.

Barua & Barua (2021) examined the consequences of the COVID-19 epidemic on three particular parameters — firm value, capital sufficiency, and interest income — under different NPL shock situations using a state-designed stress testing model. The results indicate that risk-adjusted asset values, capital adequacy metrics, and interest income are projected to decrease at both the individual bank and sectoral levels for all banks. Thus, many other studies done regarding the impact of the COVID-19 pandemic on profitability. Many studies found detrimental effects of the COVID-19 outbreak negatively affected the profitability of banks (Elnahassa et al., 2021; Katusiime, 2021; Lelissa, 2023; Qadri et al., 2023).

Thus, the study is guided by the following hypotheses based on the existing literature.

H1: COVID-19 pandemic has a significant impact on the liquidity position of commercial banks in Bangladesh.

H2: COVID-19 pandemic has a significant impact on the profitability position of commercial banks in Bangladesh.

III. OBJECTIVES

The study aims to assess the impact of COVID-19 on the financial sector in Bangladesh. The specific objectives of the study are:

To assess the pre- and post-COVID-19 profitability positions of the commercial banks of Bangladesh.

To evaluate the pre- and post-COVID-19 liquidity positions of the commercial banks of Bangladesh.

IV. METHODOLOGY

a) Sample and Data

This study uses a comparative quantitative approach and it compares the liquidity and the financial performance of Bangladeshi commercial banks before and after the COVID-19 pandemic. The sample in this study amounted to fifteen banks including 11 conventional banks and 4 Islami shariah-based banks using purposive sampling. These banks were chosen on the basis of the availability of data, their scale, their performance, and their importance in characterizing the economic conditions of Bangladesh. We used the econometric analysis technique on quarterly data of 4 years time series to observe the liquidity and bank profitability trends spanning of total 16 quarters—Q1 of 2018 to Q4 of 2021. The data of this study has been collected from the published quarterly financial statements of 15 out of 61 scheduled commercial banks in Bangladesh. The data were analyzed using descriptive statistics, trend analysis, and the paired sample t-test.

| Conventional Banks | Islamic Shariah-based Banks |

| 1. AB Bank | 12. First Security Islami Bank |

| 2. Bank Asia | 13. ICB Islamic Bank |

| 3. BRAC Bank | 14. Islami Bank Bangladesh |

| 4. Dutch-Bangla Bank | 15. Standard Bank |

| 5. Eastern Bank | |

| 6. IFIC Bank | |

| 7. Mercantile Bank | |

| 8. Mutual Trust Bank | |

| 9. One Bank | |

| 10. Trust Bank | |

| 11. United Commercial Bank |

To attain the specific objectives of the study, the data were analyzed using Microsoft Excel and STATA software to examine the tendencies of the profitability and liquidity of banks before and after the COVID-19 pandemic. A paired t-test was then conducted to ascertain whether there was a statistically significant distinction between the profitability and liquidity situation prior to and after the pandemic.

b) Variables Specification

The study uses two profitability and six liquidity measures established by the existing literature.

| Variables | Measurement | |

| Profitability | Return on asset (ROA) | Profit before taxes/Total assets |

| Return on equity (ROE) | Profit before taxes/Shareholders' equity | |

| Liquidity | Cash ratio (CaR) | Cash and cash equivalence/Current liabilities |

| Current ratio (CR) | Current assets/Current liabilities | |

| Operating cash flow ratio (OCFR) | Cash flow from operations/Current liabilities | |

| Credit to deposit ratio (CDR) | Loan/Deposits | |

| Debt to assets ratio (DAR) | (Short-term debt + long-term debt)/Total assets | |

| Debt to equity ratio (DER) | (Short-term debt + long-term debt)/Shareholders' equity |

V. RESULTS

a) Descriptive Statistics

Table 3 shows the descriptive statistics of the overall data of profitability and liquidity, dividing the period into pre-and post-COVID-19 pandemic periods. The summary of data presented in the Table 3 revealed that the COVID-19 pandemic had a positive impact on profitability in terms of return on asset (ROA), but had a slightly negative impact in terms of return on equity (ROE). The mean of the pre-COVID-19 ROA and ROE were 0.006 and 0.095 and while these were 0.011 and 0.076 during the post-COVID-19 pandemic, respectively.

The overall liquidity position of the banks during post-COVID has gotten weaker than that of pre-COVID situation. The comprehensive liquidity positions measures—the cash ratio (CaR), the current ratio (CR), operating cash flow ratio (OCFR), and debt to equity ratio (DER)—used in this study was in better condition during pre-COVID times, except the credit to deposit ratio (CDR), and debt to equity ratio (DAR). The CDR and the DAR has had been found in a higher position than the pre-COVID times.

| Pre-Covid-19 | Post-Covid-19 | |||||||||

| Variable | Obs. | Mean | Std. Dev. | Min | Max | Obs. | Mean | Std. Dev. | Min | Max |

| ROA | 120 | 0.006 | 0.008 | -0.042 | 0.024 | 120 | 0.011 | 0.045 | -0.181 | 0.345 |

| ROE | 120 | 0.095 | 0.078 | -0.044 | 0.311 | 120 | 0.076 | 0.138 | -1.173 | 0.343 |

| CaR | 120 | 0.332 | 0.167 | 0.052 | 0.842 | 120 | 0.287 | 0.165 | 0.015 | 0.826 |

| CR | 120 | 0.814 | 0.306 | 0.236 | 1.696 | 120 | 0.684 | 0.316 | 0.097 | 1.709 |

| OCFR | 120 | 0.104 | 0.579 | -0.075 | 6.370 | 119 | 0.042 | 0.050 | -0.022 | 0.329 |

| CDR | 120 | 0.073 | 0.031 | 0.004 | 0.137 | 120 | 0.096 | 0.048 | 0.000 | 0.300 |

| DAR | 120 | 0.704 | 0.129 | 0.481 | 1.197 | 120 | 1.806 | 7.496 | 0.380 | 62.894 |

| DER | 120 | 9.904 | 4.137 | 0.553 | 20.846 | 120 | 9.838 | 4.118 | 1.010 | 18.726 |

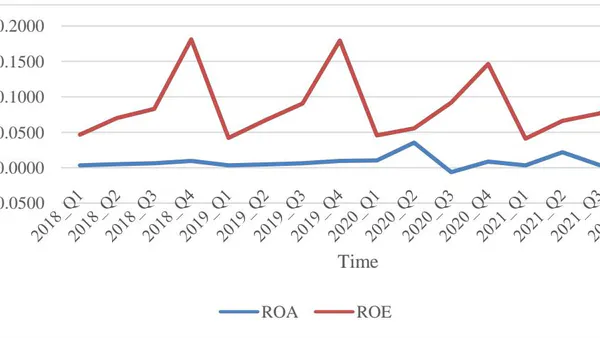

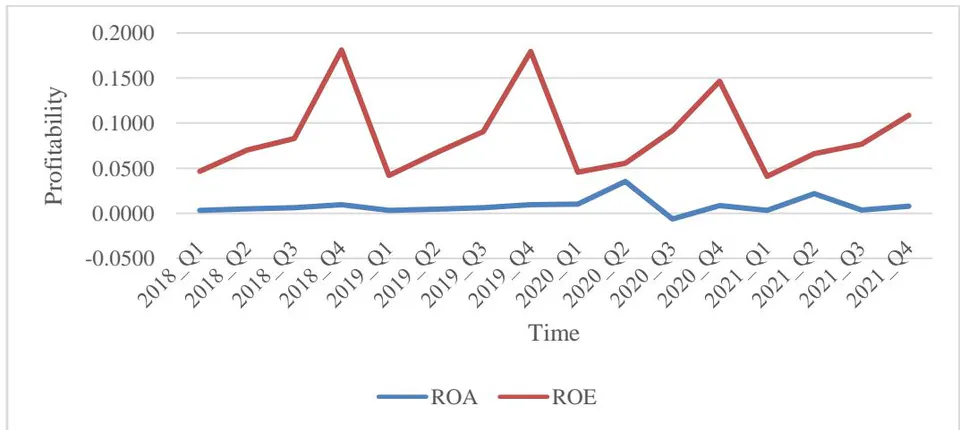

b) Trends in Profitability and Liquidity

The trends of the profitability and liquidity positions with the mean scores of quarterly data from the sample banks have been presented in Table 4. The trends of the profitability can be found in Table 4 and in the visualized Figure 1. The findings show that the ROE was more volatile over the period than the ROA. Figure 1 revealed that both profitability measures went down during the start of the COVID-19 pandemic in Q1 of 2020, and in Q3 of the same year, and it became negative in terms of ROA. Then from the Q2 of 2020, profitability began to rise slightly to the pre-pandemic times. At the start of the lockdown in Bangladesh in Q1 of 2020, the government announced some incentives to boost the economy, which may lift the profitability of the banks during Q2 of the same year. The overall profitability position of the banks during the post-COVID period was better than the pre-COVID period, especially in terms of ROA.

| Quarters | ROA | ROE | CaR | CR | OCFR | CDR | DAR | DER |

| 2018_Q1 | 0.0035 | 0.0466 | 0.3257 | 0.8465 | 0.0332 | 0.0650 | 0.6957 | 9.2029 |

| 2018_Q2 | 0.0051 | 0.0702 | 0.3269 | 0.8060 | 0.0319 | 0.0686 | 0.7164 | 10.5055 |

| 2018_Q3 | 0.0061 | 0.0829 | 0.3231 | 0.7936 | 0.0664 | 0.0683 | 0.7199 | 10.1742 |

| 2018_Q4 | 0.0095 | 0.1811 | 0.3282 | 0.8039 | 0.0487 | 0.0708 | 0.6967 | 9.5190 |

| 2019_Q1 | 0.0035 | 0.0421 | 0.3129 | 0.7614 | 0.4504 | 0.0673 | 0.7091 | 9.5878 |

| 2019_Q2 | 0.0046 | 0.0671 | 0.3543 | 0.8569 | 0.0347 | 0.0732 | 0.6987 | 10.2070 |

| 2019_Q3 | 0.0062 | 0.0905 | 0.3351 | 0.7901 | 0.0675 | 0.0876 | 0.6967 | 10.1740 |

| 2019_Q4 | 0.0094 | 0.1795 | 0.3531 | 0.8528 | 0.0983 | 0.0840 | 0.6958 | 9.8599 |

| 2020_Q1 | 0.0103 | 0.0456 | 0.3006 | 0.7115 | 0.0267 | 0.0781 | 2.0013 | 9.8143 |

| 2020_Q2 | 0.0354 | 0.0555 | 0.2655 | 0.6335 | 0.0265 | 0.0975 | 4.8815 | 9.9093 |

| 2020_Q3 | -0.0063 | 0.0920 | 0.2599 | 0.6201 | 0.0273 | 0.0984 | 0.7344 | 9.8334 |

| 2020_Q4 | 0.0086 | 0.1466 | 0.3342 | 0.7808 | 0.0860 | 0.1004 | 0.6943 | 9.7934 |

| 2021_Q1 | 0.0033 | 0.0410 | 0.3198 | 0.7552 | 0.0768 | 0.0953 | 0.6862 | 9.8698 |

| 2021_Q2 | 0.0217 | 0.0661 | 0.2681 | 0.6559 | 0.0320 | 0.1041 | 4.0765 | 9.7744 |

| 2021_Q3 | 0.0037 | 0.0766 | 0.2683 | 0.6544 | 0.0451 | 0.0970 | 0.6864 | 9.7790 |

| 2021_Q4 | 0.0080 | 0.1088 | 0.2760 | 0.6619 | 0.0681 | 0.0987 | 0.6859 | 9.9315 |

Source: Calculated Data

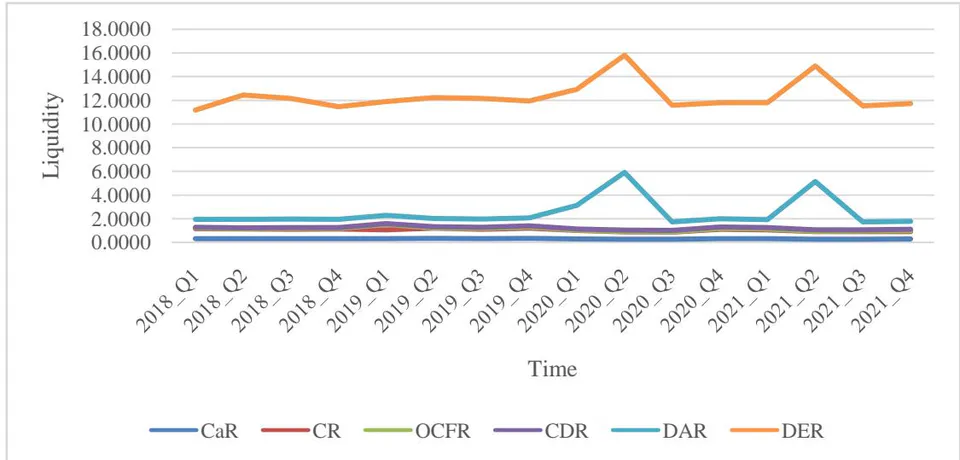

The liquidity position of the sample banks has also been presented in Table 4 and in Figure 2. From the results, it has been found that the trend line of the CaR, the CR, and the OCFR are almost straight, but there is a "downtrend" from Q1 to Q3 of 2020. This means the liquidity ratios declined significantly during the mentioned period. In the case of the DAR, another measure of bank liquidity has become more shaken during the post-COVID period, although it was almost the "straight line" before the pandemic. The DAR has become much higher in the Q1 to Q3 of 2020 and Q1 to Q3 of 2021 which has never happened during the prepandemic times. The DER of the sample banks behaved almost the same as the DAR over the period of the study. The DER also increased after the pandemic like DAR. The higher the DAR and the DER mean that banks borrowed more funds compared to the total assets and equity, which significantly decreased the liquidity level.

Source: Calculated Data

c) Paired Sample t-test Results

Before and after the COVID-19 crisis, the observed trend of profitability and liquidity was evaluated using a paired t-test. In practice, the acquired data (mean scores) from the sample banks were compared to assess whether the differences were statistically significant. The results of the paired sample t-test have been presented in Table 5.

With regard to profitability, the results revealed that the difference in the profitability position of the sample banks before and after the pandemic was statistically insignificant, indicating that the distinctions we have discovered in terms of profitability are not statistically significant as we have found p-values greater than 0.10.

Regarding liquidity, the findings of the study exposed that the differences in the liquidity positions of the sample banks in the case of the CaR, the CR, the CDR, and the DAR during the pre and post-pandemic period were statistically significant as we have p-values of less than 0.10. While the differences in the liquidity in terms of the OCFR, and the DER during the pre and post-pandemic period are statistically insignificant. This indicates that the OCFR and the DER do not significantly differ during the pre and post-COVID-19 period.

| obs. | Mean 1 | Mean 2 | dif. | St. Error | t-statistic | p-value | Sig. | |

| ROA | 120 | 0.006 | 0.011 | -0.005 | 0.004 | -1.100 | 0.266 | |

| ROE | 120 | 0.095 | 0.076 | 0.019 | 0.012 | 1.600 | 0.120 | |

| CaR | 120 | 0.333 | 0.287 | 0.046 | 0.013 | 3.500 | 0.001 | *** |

| CR | 120 | 0.814 | 0.684 | 0.130 | 0.026 | 5.050 | 0.000 | *** |

| OCFR | 120 | 0.104 | 0.042 | 0.062 | 0.053 | 1.150 | 0.247 | |

| CDR | 120 | 0.073 | 0.096 | -0.023 | 0.004 | -7.100 | 0.000 | *** |

| DAR | 120 | 0.704 | 1.806 | -1.102 | 0.685 | -1.600 | 0.099 | * |

| DER | 120 | 9.904 | 9.838 | 0.066 | 0.173 | 0.400 | 0.704 |

VI. DISCUSSION AND PRACTICAL IMPLICATIONS OF THE RESULTS

The results of the study revealed that the profitability during post-COVID-19 was significantly increased than the pre-COVID-19 pandemic. Although the results show that the profitability of banks after the pandemic was more volatile, especially in terms of ROE. But the results of the paired sample t-test confirmed that the differences in the pre and post-pandemic profitability measured by the ROA and ROE were statistically insignificant. This indicates that the COVID-19 pandemic did not significantly affect the profitability of the level of commercial banks in Bangladesh. These results contradict the findings of many of the results of the previous studies (Elnahassa et al., 2021; Gazi et al., 2022; Katusiime, 2021; Lelissa, 2023; Qadri et al., 2023). The findings of the study revealed that the liquidity ratios deviate a bit more than the profitability positions due to the pandemic. The results show that the differences in the liquidity positions during the pre and post-pandemic period are statistically significant, measured by the CaR, the CR, the CDR, and the DAR. At the same time, the results show that these differences are not statistically significant in terms of the OCFR, and the DER. Overall, the results exposed that the COVID-19 pandemic has significantly changed the liquidity positions of commercial banks in Bangladesh. The findings show that the liquidity position of the banks had been negatively affected by the COVID-19 outbreak. The results are aligned with the findings of previous studies(Almeida, 2021; M. R. Karim et al., 2021; Katusiime, 2021; Korzeb & Niedzióka, 2020; Mwangagi, 2021), but these findings contradict some other studies (Gazi et al., 2022; Marshal et al., 2020), which revealed a significant positive impact of COVID-19 on the liquidity positions of the banks. The dynamic nature of the Bangladesh economy with GDP growth may be one of the reasons that caused to maintain the profitability of the banks, while the liquidity position had been significantly reduced during the pandemic maybe for the panicked withdrawal of deposits by the customers.

VII. CONCLUSION

The study intended to evaluate the effects of the COVID-19 outbreak on the profitability and liquidity positions of commercial banks in Bangladesh. This study uses a comparative quantitative approach and compares the liquidity and the financial performance of commercial banks in Bangladesh before and after the COVID-19 pandemic through the analysis of the quarterly data. The results revealed that the profitability during post-pandemic times is more volatile and slightly increased than the pre-pandemic time, but the trend of the pre and post-pandemic profitability is almost the same and the difference is statistically insignificant. Whereas, the liquidity positions of the banks substantially reduced in the post-pandemic times and the differences of the pre and post-pandemic liquidity situations significantly differed. Thus, the study concludes that COVID-19 has brought a significant negative impact on liquidity, although the profitability level did not experience a significant change in the commercial banks of Bangladesh.