The purpose of this research paper is to assess the perception of urban women towards having an insurance policy as a precaution against cervical cancer. Data required for the research have been collected from primary data source taking into consideration total 170female as respondents who have been living in Barishal city with at least 18 years old. Frequency distribution has been used to explain the response of 27 questions comprising demographic and financial aspect of the respondents. Reliability of the survey has been tested by Cronbach’s Alpha with satisfied value of more than 0.705. Moreover, a regression analysis has been used for finding out the most significant factors influencing the willingness of purchasing cervical cancer insurance policy in near future covering 7relevant variables. Overall, it has been found that approximately 23% respondents from the surveyed sample has a history to be encountered with cervical problems like ovarian cyst, uterus infection etc. However, most of them neither had any screening nor have any health insurance policy as a precaution against cancer. Moreover, significant number of participants are willing to purchase a cancer insurance policy if it is with a very reasonable premium.

## I. INTRODUCTION

Cervical cancer developed in a woman's cervix is the fourth most common cancer in women. In 2018, an estimated 5,70,000 women were diagnosed with cervical cancer worldwide and about 3,11,000 women died from the disease (WHO,2018). Each year, many countries from developed world publishes reports on early cancer detection; which is absolutely absent in most developing countries like Bangladesh. Very limited evidence is found on the role and acceptance of Pap test among the women of Bangladesh in determining cervical cancer. More research and updates are needed relating Pap test in early detection of cervical cancer (Mustari, S. 2017).

In the coming decades, cancer is foreseen to be a more significant cause of mortality in Bangladesh. The projected frequency of new cancer cases will be 21.4 million by 2030 (Hussain and Sullivan, 2013). However, women, their partners and families are often not aware of the disease and its consequences. (Ahmed T 2008) They come for diagnosis and treatment usually when it is too late. This is the reason why approximately 18,000 of Bangladeshi women reported new cases of cervical cancer on annual basis and out of which amounting to over 10,000 women die from it. "According to hospital records in Bangladesh, it constitutes about $22 - 29\%$ of all female cancers". "Two-third $(69.2\%)$ of the women referred for cervical cancer screening aware of cervical cancer and half of the women $(47.4\%)$ know about prevention of the disease" (Nessa et al., 2013).

In the absence of health insurance, treatment of critical illnesses like cancer poses a formidable financial challenge to affected individuals, their immediate and extended family, and the society at large. Patients often fail to complete the course of treatment due to unaffordable costs and yet face the prospect of bankruptcy. Against this backdrop, we propose a two-tiered novel insurance scheme for cancer care, involving all the major stakeholders. (Hussain MZ 2016). Due to high premium, poor coverage, relatively few choices, lack of promotional activities and most importantly reluctance to screening cervical cancer demotivate women to adopt any health insurance products. However, weather plenty of social awareness programs and very convenient featured cervical cancer insurance policy can motivate the women to invest for this deadly diseases or not is the main concern of this project.

The paper aims to find out the perceptions of women towards their knowledge and sincerity of screening particularly cervical cancer along with willingness to purchase an insurance policy as a precaution against it hereafter. It has been organized as follows. Firstly, there is an introduction; second section consists of literature review, followed by a rational of the study as section three; section four consists of methodology; section five includes result and analysis; the last section concludes the paper with some recommendations.

## II. LITERATURE REVIEW

Cervical cancer ranks as the most prevailing cancer among Bangladeshi females (Ahmed and Rahman, 2008). Despite advances in screening and treatment during the past several decades, cervical cancer remains a major health problem for Bangladeshi women. The reason is, many women have never undergone a Pap test procedure, or are not tested regularly. Like other less developed countries, low socioeconomic status, poverty and lack of knowledge are considered as the reasons for the low test rates on Bangladeshi women (Austin et al., 2002).

A questionnaire-based survey of 400 Bangladeshi urban women was evaluated by on their socio-demographic characteristics, knowledge and attitudes towards Pap testing. In general, the findings reveal that respondents have a good understanding of the purpose of Pap test screening with 3.92 (Mean score). With 3.54 Mean score, the respondents believed that Pap tests are recommended to women who are married and with 3.45 mean score women believed that Pap tests are recommended only to those who have children. Generally, respondents possess good knowledge of Pap test and its purpose (Mustarietel 2017).

Health, medical consumption, and on socioeconomic characteristics like age, income, education and family size has been considered as a key factors can influence the purchasing decision health insurance policy. Health, medical consumption and income are found to have a significant influence on the decision with respect to the type of insurance. The result gives an indication of the degree of adverse selection that may take place if health insurance policies are offered with the option to take a deductible in exchange of a premium reduction. (Bernard and Van 1983) Advertising is positively correlated with the purchase decisions of unsought product while personal selling is statistically significant and positively correlated with the purchase decision of life insurance product. (Abdullah et el 2015).

Slattery (1989) puts the customer in the focus of insurance marketing. Integrity and trust are highly important to win over a customer's decision to buy a life insurance product. The perceived risk of the customer in buying a life insurance product is dependent on the service of the insurer and its personal equation with the customer. Gronroos (1984) pointed that insurance get influenced by the external aspects such as brand image while judging the service. The various causes outlined by Wells & Stafford (1995) and supported by Cooper & Frank (2001) are low quality of service, unawareness of specific needs of customers, inferior service design and very poor insurance service delivery process. Customer's expectation of the agent's service is the standard to be used by the insurers while evaluating their services (Walker & Baker, 2000).

There is a positive influence of certain sociodemographic characteristics on the decision to enroll and renew health insurance policy. Negative perceptions about the NHIS and the quality of care decreased the likelihood of enrolling in the scheme. It can be concluded that, improvement in the technical processes in the scheme management and the quality of care will stimulate voluntary enrollment and renewal rate of the health insurance policy. A health insurance policy is influenced by scheme factors (convenience, price and benefits), individual factors (gender, religion, marital status, perceived health status) and provider factors (quality of care, staff provider attitude) Daniel and Dadson (2013)

Asensoetel (1997) people are willing to pay higher premiums for health insurance. The reasons for the low enrolment are problems in ability to pay the premium, poor quality of health care, the rigid design in terms of enrolment requirements and problems of trust are other important reasons for people not to join. Logistic and OLS regressions are used by Liu and Chen (2002) to examine the factors influencing the probability and amount of private health insurance purchased. Higher income and education levels Married females, the employed and household heads working in state-run enterprises are more likely to purchase private insurance than their counterparts. The likelihood of private insurance purchase also tends to rise with advancing age and larger family sizes. The environment rating, residence, income, education, age, smoking and marital status variables were all found to have a statistically significant (at $95\%$ confidence level) positive relationship with ownership of health insurance schemes. Contrastingly, the other covariates, namely: health rating, age squared, household size, occupation, employment, alcohol use and contraceptive use had a significantly negative relationship with health insurance ownership. Joses et el (2010).

There is a large and persistent association between education and health and we suggest that increasing levels of education lead to different thinking and decision-making patterns. David and Adriana (2008) Wealth status, age, religion, birth parity, marriage and ecological zone were found to have significantly predicted health insurance subscription among women in reproductive age in Ghana. Hubbard (1995) Demand effects are dominated by the marginal impacts from existing purchasers of insurance. Although income and number of earners are both positively related to the demand for insurance, the marginal effect from an increase in income is greater for single-earner households than for multi-earner households. Also, as either family size or age increases, the marginal increase in insurance expenditure diminishes. Showers & Shotick (1994) Anjali (2018) surveyed 50 respondents in Kerala, India. And she tried to know the perception of customers towards health insurance. The study finds out the awareness level of people regarding health insurance, sources of awareness, and the factors which influence people to select the health insurance company.

Bawa and Ruchita (2011) studied 563 people and found that a low level of awareness and willingness to purchase a health insurance policy among people. And also found seven key factors which create a barrier to have a health insurance policy. Besides these, they have found significant existed relationships among age, gender, education, employment, income of respondents with their preparedness to pay for health insurance.

Panchal N (2013) found three factors that's why people have not any health insurance policy. These are low consciousness level among people, lack of efficient financial tools, and the high premium charged by the company. Nekmahmud, Shahedul and Ferdush (2017) they researched to know the perception of people regarding life insurance. They found a large number of people are aware of life insurance. It emphasized mass communication to raise awareness among people. Joshi and Shah (2015) try to know the perception of the customers to Health Insurance of different service providers and to find out customers purpose and numerous factors for buying Health Insurance policy.

## III. RATIONALE OF THE STUDY

Cervical cancer is predicted to be an increasingly important cause of morbidity and mortality in Bangladesh in next few decades. Moreover, health insurance policy is not yet an effective measure to health and financial coverage for the people here. Most of the people are not concerned regarding the effectiveness of this cooperative service due to some personal, financial and social factors. As frequency and possibility of women being affected by the fatal diseases like cervical cancer, ovarian cancer and breast cancer is very high in South Asian region in recent years, it's very crucial to find out the attitude of women in our country to have cancer insurance policy as a precautions to face this types of unexpected situation in future. The paper would help to motivate further research to pick up the scenario from all over the country that would grow sincerity to the general women, the service provider and government as well to make cancer insurance policy as a common defensive tools for fighting against unanticipated future. Government could insist the insurance company to launce special policy for woman with convenient features.

## IV. METHODOLOGY

The research is basically quantitative in nature and primary data has been used to prepare the project report. The study was conducted in Barishal city where the data collection started in March 2023 and continued till mid of April 2023. A questionnaire with both structured and unstructured questions has been used to collect the data where 5-points Likert scale was also used to assess the opinions of the respondents regarding cancer insurance policy. In total, 170 women were surveyed ages between 18-60 years as sample from which finally 142 respondents were evaluated for the study. The analysis is based on data from cross sectional household sample. Frequency distribution of the collected sample have been prepared while Linear Regression, Chi Square test and Cronbach's Alpha has been run with the software SPSS to analyze the collected data. No experimental research has been conducted in the proceedings of this project. The model used for the analysis is given below.

$$

\begin{array}{c} \text{WILLINGNESS} = \alpha + \beta 1 \text{MINPREMIUM} + \beta 2 \text{SUSPECTION} + \beta 3 \text{PENCCOunter} + \beta 4 \text{EDU} + \beta 5 \text{TABILITY} \\+ \beta 6 \text{FINCOME} + \beta 7 \text{INSUPOLicy} + \beta 8 \text{MOTIVATION} + \beta 9 \text{COST} + \varepsilon \text{i t} \end{array}

$$

Where $\alpha$ represents constant. $\beta 1, \beta 2, \ldots, \beta 9$ indicates the regression coefficient for the independent variables, namely $x_{1} = \text{Minimum amount of Premium}$, $x_{2} = \text{Suspension}$, $x_{3} = \text{Previous occurrence history}$, $x_{4} =$

Education level, $x_{5} =$ Treatment ability, $x_{6} =$ Financial income per month, $x_{7} =$ Availability of insurance policy $x_{8} =$ Motivation to have insurance policy from the surroundings and $x_{9} =$ cost of the treatment.

## V. RESULT AND ANALYSIS

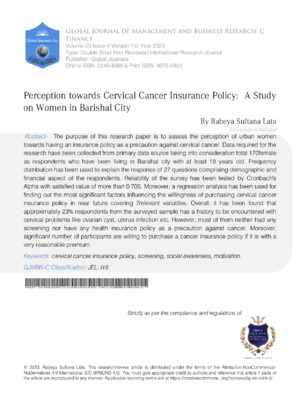

a) Frequency Distribution of the Questionnaire Figure No. 1: Source: Survey in Barishal, March –April 2023 From the above figure we can see that in total 127 response had been collected during the sampling study period among which more than $75\%$ are from ages between 18 years to 25 years old. Exactly $25\%$

respondents are from ages in between 26-45 and a very few senior female responded the questionnaire regarding the research.

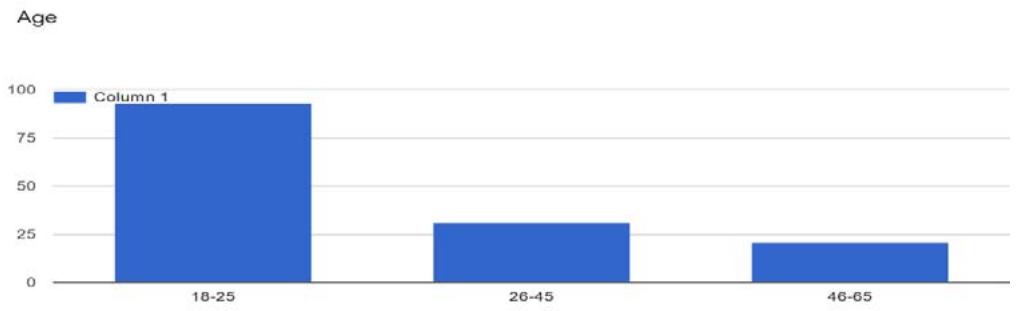

Educational Qualification Figure No. 2: Source: Survey in Barishal, March –April 2023 Figure 2 shows that highest number of respondents are graduate that is almost $50\%$ of the total sample whereas around $25\%$ of them are from post graduate level of education. On an average $10\%$ respondents have their education level up to higher secondary and a very insignificant portion are totally out of education.

### Family income per month

142 responses

Figure No. 3: Source: Survey in Barishal, March –April 2023

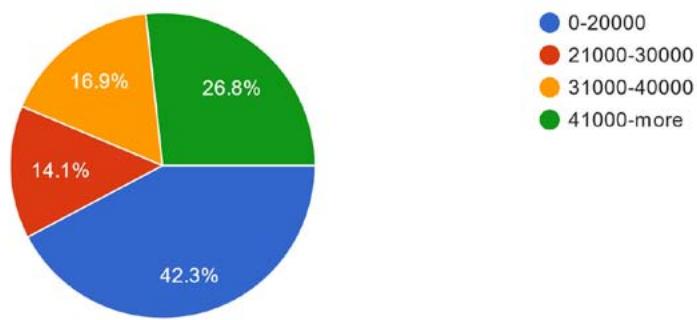

The first pie chart above represents that $67.7\%$ of the respondents are unmarried whereas $32.3\%$ are married. The second diagram above shows the family income of the respondents within various categories. Highest proportion of female have their family income within 20,000 taka. On the other hand $25.4\%$ have their family income level per month equal or more than 41,000 taka. However, the remaining two ranges have almost same number of respondents.

#### Employment Status

143 responses

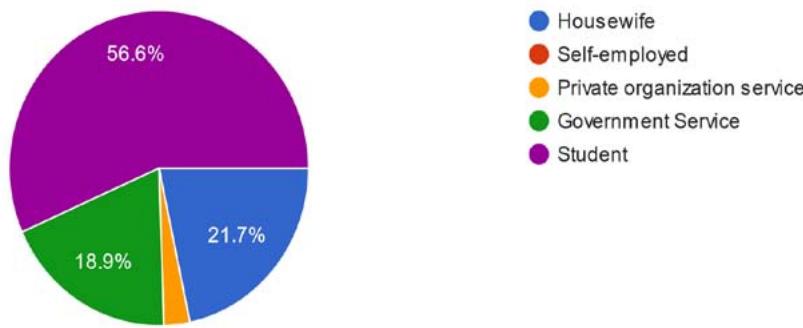

Figure No. 4: Source: Survey in Barishal, March –April 2023 Figure 4 shows that highest percentage of respondents having $63.8\%$ of the total sample are students whereas there is no self-employed persons here. $17.3\%$ of the sample are government employee and a very insignificant percentage are doing private organization service. Moreover, $15.7\%$ of the collected responses are from housewives.

If you are employed then does your employer cover any of your medical expenses?

90 responses

Figure No. 5: Source: Survey in Barishal, March –April 2023

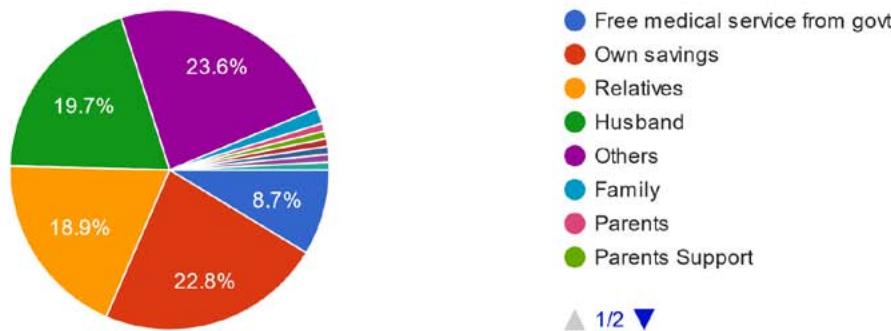

If you are not employed then what are the source of your medical expenses?

Figure No. 6: Source: Survey in Barishal, March –April 2023 From figure 6 it can be clear that $56\%$ of the respondents of the survey are employed but get no medical support from their employer whereas $44\%$ of them are fortunate to have medical facilities from their employer. However, almost $24\%$ of the correspondents arrange their medical expenses from their own savings while relatives and husband are the basis for the expense for around $17\%$ of the respondents (figure 7).

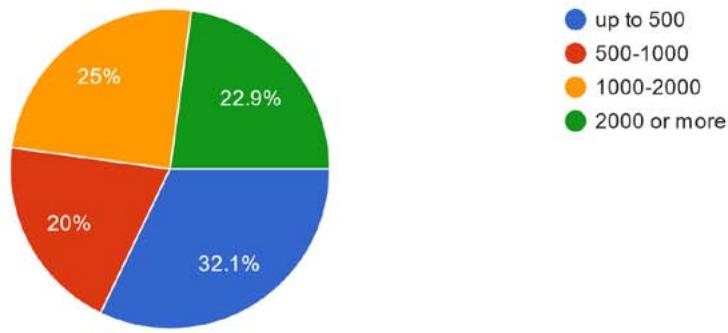

What is your average monthly medical expense?

140 responses

Figure No. 7: Source: Survey in Barishal, March –April 2023

The above graph show that around $32\%$ of the respondents out of 140 have their medical expense up to 500 taka while approximately $25\%$ of the sample have to spend 1000 -2000taka per month for their treatment purpose. On an average the remaining two groups have almost same number of samples in each (Figure 6).

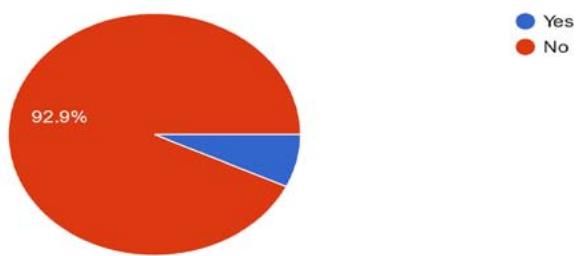

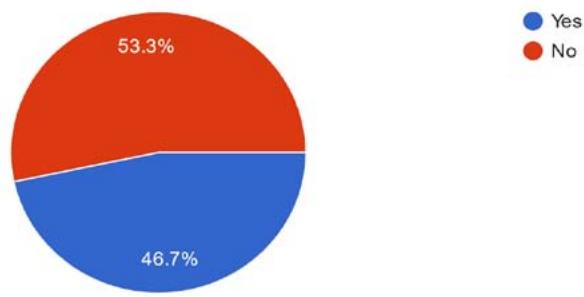

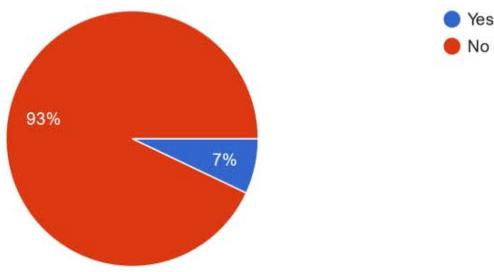

Do you have any health insurance/ life insurance policy?

143 responses

Figure No. 8: Source: Survey in Barishal, March –April 2023

Only a very few female from our sample have health insurance policy and their precaution against fatal diseases covering $7\%$ of the total alternatively $93\%$ of the respondents don't have any health insurance policy.

Although a significant number participants of our survey are educated they are not even still conscious regarding health insurance policy.

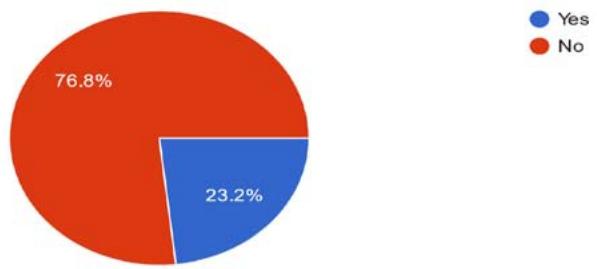

Have you encountered with any type of cervical problems (ovarian cyst/ uterus infection) in the past?

Figure No. 9: Source: Survey in Barishal, March –April 2023

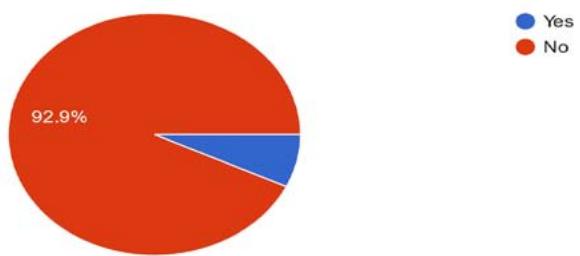

Have you ever participated in cancer screening test of your uterus/ ovary? 141 responses Figure No. 10: Source: Survey in Barishal, March –April 2023

Figure 9 indicates that approximately $23\%$ respondents from the surveyed sample have a history to be encountered with cervical problems like ovarian cyst, uterus infection etc. From the categorical review of the sample it has been found that married women have greater possibility of being affected by these above mentioned complexities. However, only $7\%$ of the total sample went through cancer screening test that means in spite of being affected by cervical problem they are not even serious of that issue.

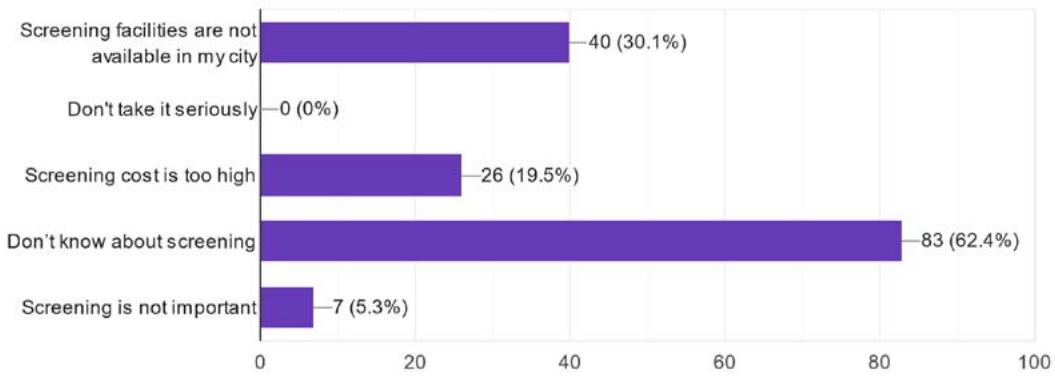

If not then what are the reasons? You can mark more than 1 option 133 responses Figure No. 11: Source: Survey in Barishal, March –April 2023

Firstly, figure 11 reveals the major causes of their reluctance on screening issue and found that almost $63\%$ of the respondents don't know about screening. Secondly, screening facilities are not available in their city is claimed by $30\%$ of the sample.

Thirdly, $26\%$ of the respondents accused high cost as their reason of not participating in cervical screening test. In addition, around $5\%$ of the respondents don't feel it important to test.

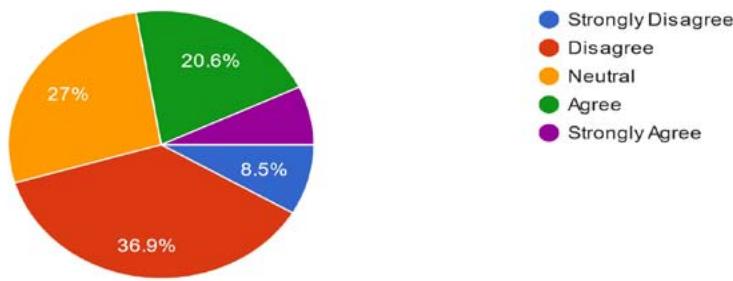

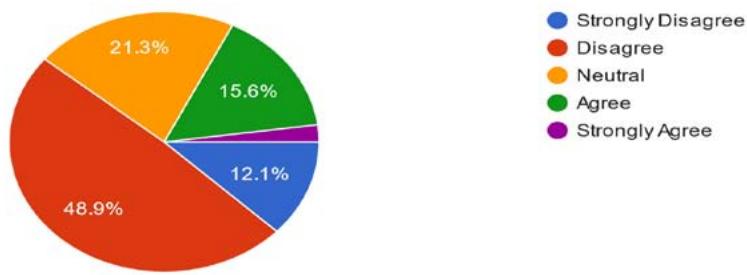

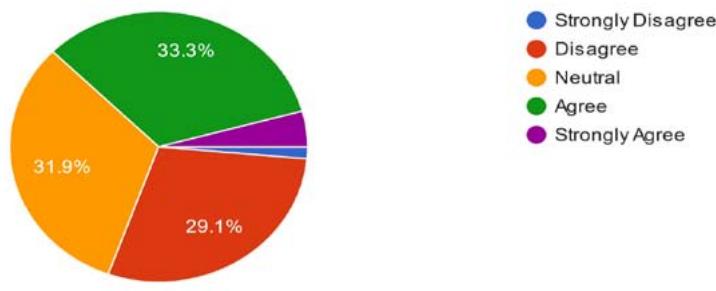

Women in your Surrounding/city are health conscious and motivate you to get ovarian screening as they practice.

Figure No. 12: Source: Survey in Barishal, March –April 2023

Around $37\%$ respondents are disagreed regarding the health consciousness of the surrounding woman of them whereas about $20\%$ have positive opinion regarding them. $27\%$ of the surveyed woman were reluctant to take any positive or negative sides but $8.5\%$ of the sample showed their strong negative opinion to the awareness and motivation issues of their surrounding woman. (Figure 12).

Cervical cancer is the 4th most common cancer among women;You are known and aware of it. 143 responses

Figure No. 13: Source: Survey in Barishal, March –April 2023

Diagram 13 depicts that on an average $64\%$ of the surveyed women are known about the widespread features of cervical cancer comprising response from the options agree and strongly agree. Around $30\%$

respondents have no idea about the severity of cervical cancer among women. A significant number, about $18\%$ are in neutral position without any positive or negative opinion in this respect.

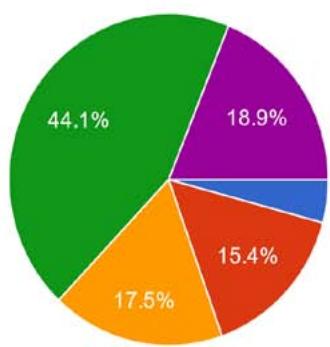

Practice Regular checkup of your ovarian/uterus condition as your physician/doctor suspect you to be affected.

136 responses

Figure No. 14: Source: Survey in Barishal, March -April 2023

An alarming scenario has been found from figure 14 that $34\%$ of the sample use to go for regular ovarian checkup as they are suspected to be affected by cervical problem according to their physician. In addition, $12.5\%$ strongly support their opinion. $23\%$ of the respondents are out of suspense to be affected by any cervical issues in future. Around $28\%$ of the sample have no straightforward response in this issue.

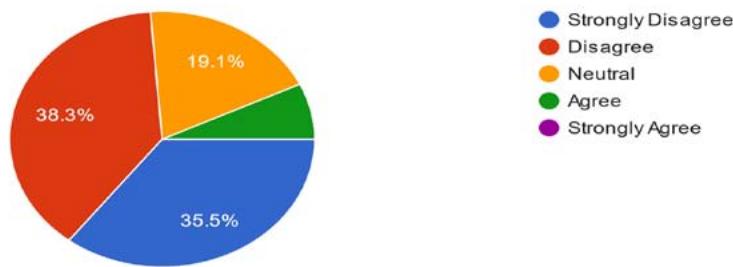

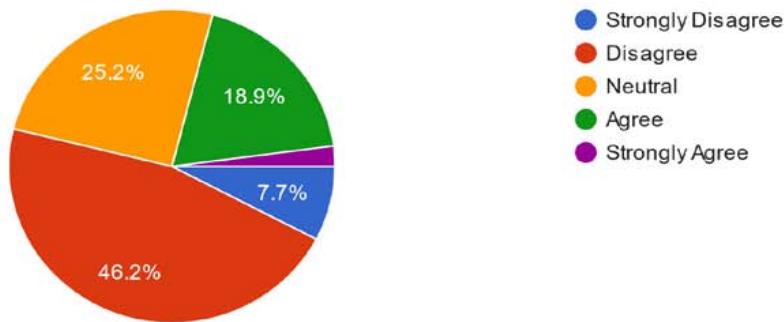

You are known about the cost of cervical cancer screening and treatment.

141 responses

Figure No. 15: Source: Survey in Barishal, March –April 2023

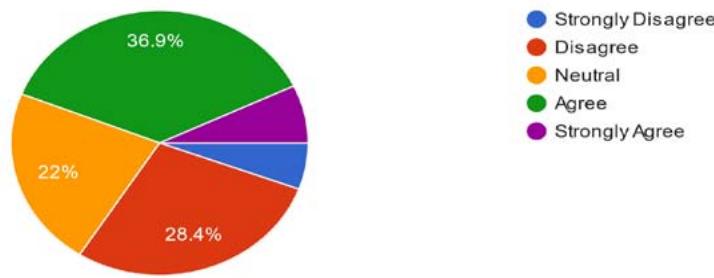

You are able to manage the treatment cost of cervical cancer even if it is more than 30 lac.

141 responses

Figure No. 16: Source: Survey in Barishal, March –April 2023

It has been found from the survey (Figure 15) that almost $50\%$ of the respondents don't have any idea regarding cost of screening and treatment of cervical cancer and $12\%$ of the total respondents strongly supported the opinion. Only $16\%$ of the sample have knowledge in this respect whereas just above $20\%$ of them are reluctant to express their concrete views in this respect. When an approximate treatment cost was revealed to the surveyed women in total $74\%$ of them expressed their inability to carry the cost (Figure 16) of which $36\%$ strongly opined their incapability. Just above of $19\%$ participants are confused regarding this issue and only $8\%$ of them believe in their capacity to arrange the required cost of cervical cancer treatment.

#### Came across advertisement/ social awareness program of cancer screening and insurance

policies

Figure No. 17: Source: Survey in Barishal, March –April 2023 From figure 17a mixed combination of responses has been originated from the question of social awareness program and advertisement concerning cervical cancer screening and insurance policy as a precaution against the treatment. Nearly

about $37\%$ of the participants previously noticed advertisement or social awareness program alternatively a little more than $28\%$ of the total sample responses against it. Of course very insignificant proportion expressed their opinion strongly.

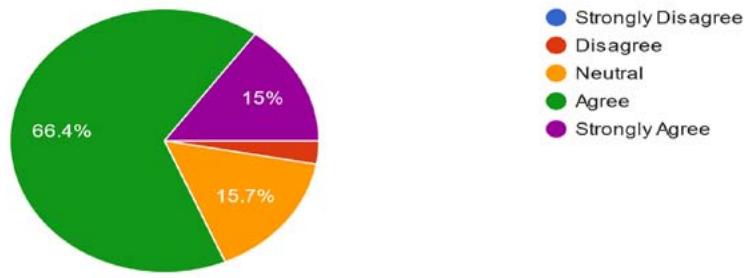

Cervical cancer insurance policy with minimum premium is a crucial need and can attract maximum number women in our society to adopt it.

140 responses

Figure No. 18: Source: Survey in Barishal, March –April 2023

Features with a very low premium can motivate a large number of women in Barishal city to purchase a cancer insurance policy is an opinion that is supported by almost $16\%$ of the participants. In addition, around $16\%$ of sample has strongly supported the opinion. A very insignificant proportion gave opposite reaction in this respect (Figure 18). Again, from figure 18, their ability along with willingness to pay premium within the range 1000- 2000 has been tried to be anticipated and almost same number of respondents answered both positively and negatively in answering the question $33\%$ and $29\%$ respectively. In addition, almost $32\%$ of the total sample are reluctant to give a straight opinion. The answer may be varied due to variation of the income level of the respondents. Premium less than the mentioned range may attract more positive response.

Able to pay cancer insurance policy premium per month maximum up to 1000-2000 taka

141 responses

Figure No. 19: Source: Survey in Barishal. March –April 2023

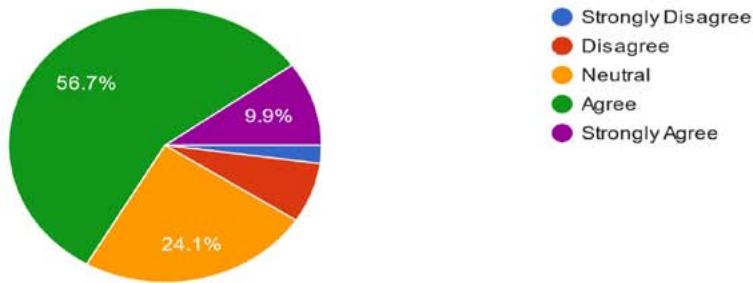

Prefer to purchase cancer insurance policy in near future as a precaution against treatment of cervical cancer

Figure No. 20: Source: Survey in Barishal, March –April 2023

Although most of the respondents have no health insurance policy having a brief previously regarding the severe effect of this deadly disease influenced them a lot in their purchasing decision of

cancer insurance policy that is resembled in figure 19. Almost $57\%$ of the total sample expressed their interest to purchase a cancer insurance policy within lowest level of premium in near future whereas $9.9\%$ women from sample strongly supported the statement. However,

24% of the participants are still in a gray area in setting their decision in this respect. If a standard cancer insurance policy with affordable features are offered to them, a revolution may be arisen.

Religious values prevents you to accept insurance policy 143 responses Figure No. 21: Source: Survey in Barishal, March –April 2023

Although around $20\%$ of the respondents accused religious values as an excuse against insurance policy, most of them denied the negative relationship between the two. Again, $25\%$ of the participants have no exact opinion. However, religious values influence the women in terms of screening and having insurance policy although the proportion is not so high. (Figure 21)

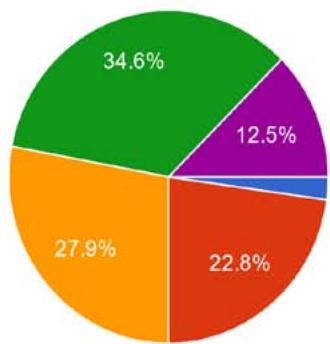

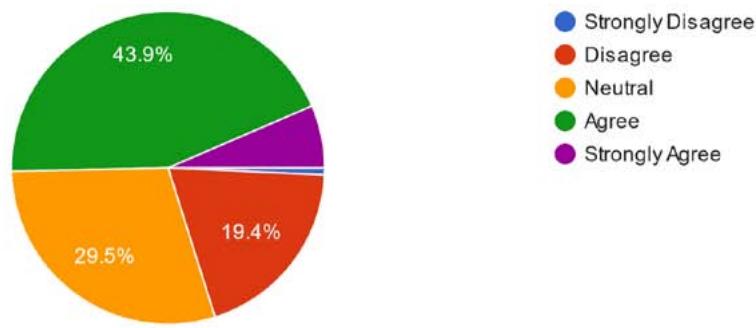

Social awareness provoke you on purchase decision of cancer insurance 139 responses Figure No. 22: Source: Survey in Barishal, March –April 2023

A very positive impression has been found in favor of social awareness to motivate the respondents to accept an insurance policy especially for cancer. Almost $44\%$ participants are agreed with it and $29.5\%$ are neutral whereas $19.4\%$ gave opposite reaction.

### b) Test of Reliability and Regression Analysis

Cronbach's alpha is the most common measure of internal consistency of data. It is frequently used when we have multiple Likert questions in a surveyor questionnaire that form a scale and we wish to determine if the scale is reliable. To measure the reliability of surveyed questionnaire in this research project Cronbach alpha was run by the software SPSS and the perceived values is 0.705which indicate acceptable internal consistency. (Appendix: Table no1).

A regression has been run with the software SPSS to determine the factors significantly influencing the inclination of the women towards having an insurance policy particularly for cervical cancer. To run the model willingness to purchase has been considered as a target variable whereas 9 independent variables were used to find out the degree of relationship between the two categories. The coefficient of correlation R is 0.690 which indicates a moderately good relationship among the variables while the coefficient of determination R Square value is almost $50\%$ (0.482) that means only $50\%$ variation of dependent variable due to independent variables has been explained by the model. Adjusted R Square is not in a satisfactory level and depicts that more relevant variable can bring a standard score of adjusted R square to explain the relationship between dependent and independent variables. However, Education level, Financial income per month, Motivation from the surroundings, Suspect to future occurrence, cost of the treatment and Minimum /Lower amount of Premium are positively related to the willingness of purchasing decision of cancer insurance policy in near future. Among them Minimum amount of Premium has the highest score of coefficient 0.381 which is statistically significant while future suspect holds the lowest score of coefficients. Alternatively, previous encounter history, having insurance policy and treatment ability have negative coefficients designate the adverse relationship with dependent variable.

## VI. CONCLUSION

Cervical cancer is one of the neglected diseases in Bangladesh. Promotions, campaigns, screenings and financial security of women are overlooked in this country due to the lack of consciousness about this disease. Public awareness is much needed to reduce the number of deaths from cervical cancer. Both government and non-government organizations should work together to make Bangladeshi females more aware and well-informed about screening and having a cancer insurance policy as a financial backup. If a well-balanced and convenient insurance policy for various categories of woman are issued by all insurance companies mandatorily, Bangladesh will be benefitted economically and socially. This is an academic research to know the attitudes of Bangladeshi women about cancer insurance policy and strongly advocates in policies' development to introduce cancer insurance policy as early as possible. Education level, cost of treatment, minimum amount of premium and social motivation are the key factors should be considered in this respect.

### APPENDIX

Table 1

<table><tr><td rowspan="2"></td><td colspan="3">Case Processing Summary</td><td></td><td rowspan="6"></td><td colspan="3">Reliability Statistics</td></tr><tr><td colspan="2"></td><td>N</td><td>%</td><td rowspan="3">Cronbach's Alpha</td><td rowspan="3">Cronbach's Alpha Based on Standardized Items</td><td rowspan="3">No. of Items</td></tr><tr><td rowspan="3">Cases</td><td colspan="2">Valid</td><td>142</td><td>99.3</td></tr><tr><td colspan="2">Excludeda</td><td>1</td><td>.7</td></tr><tr><td colspan="2">Total</td><td>143</td><td>100.0</td><td>.705</td><td>.702</td><td>6</td></tr><tr><td colspan="5">a. Listwise deletion based on all variables in the procedure.</td><td></td><td></td><td></td></tr></table>

Table 2

<table><tr><td colspan="7">Inter-Item Correlation Matrix</td></tr><tr><td></td><td>Motivation</td><td>Willingness</td><td>Suspection</td><td>Cost</td><td>Advertisement</td><td>Social Aware</td></tr><tr><td>Motivation</td><td>1.000</td><td>.275</td><td>.271</td><td>.281</td><td>.345</td><td>.221</td></tr><tr><td>Willingness</td><td>.275</td><td>1.000</td><td>.308</td><td>.380</td><td>.242</td><td>.167</td></tr><tr><td>Suspicion</td><td>.271</td><td>.308</td><td>1.000</td><td>.337</td><td>.500</td><td>.172</td></tr><tr><td>Cost</td><td>.281</td><td>.380</td><td>.337</td><td>1.000</td><td>.308</td><td>.268</td></tr><tr><td>Advertisement</td><td>.345</td><td>.242</td><td>.500</td><td>.308</td><td>1.000</td><td>.156</td></tr><tr><td>SocialAware</td><td>.221</td><td>.167</td><td>.172</td><td>.268</td><td>.156</td><td>1.000</td></tr></table>

Table 3

<table><tr><td colspan="6">Item-Total Statistics</td></tr><tr><td></td><td>Scale Mean if Item Deleted</td><td>Scale Variance if Item Deleted</td><td>Corrected Item-Total Correlation</td><td>Squared Multiple Correlation</td><td>Cronbach's Alpha if Item Deleted</td></tr><tr><td>Motivation</td><td>16.54</td><td>9.385</td><td>.428</td><td>.191</td><td>.669</td></tr><tr><td>Willingness</td><td>15.65</td><td>9.859</td><td>.418</td><td>.202</td><td>.671</td></tr><tr><td>Suspicion</td><td>16.17</td><td>8.993</td><td>.504</td><td>.309</td><td>.643</td></tr><tr><td>Cost</td><td>16.94</td><td>9.492</td><td>.486</td><td>.252</td><td>.651</td></tr><tr><td>Advertisement</td><td>16.32</td><td>8.873</td><td>.492</td><td>.309</td><td>.647</td></tr><tr><td>SocialAware</td><td>15.98</td><td>10.773</td><td>.288</td><td>.100</td><td>.706</td></tr></table>

Table 4 Table 5

<table><tr><td colspan="5">Model Summary</td></tr><tr><td>Model</td><td>R</td><td>R Square</td><td>Adjusted R Square</td><td>Std. Error of the Estimate</td></tr><tr><td>1</td><td>.690a</td><td>.482</td><td>.389</td><td>.710</td></tr><tr><td colspan="5">a. Predictors: (Constant), MINPREMIUM, SUSCEPTION, PENCOUNTER, EDU, TABILITY, FINCOME, INSUPOLICY, MOTIVATION, COST</td></tr></table>

<table><tr><td colspan="7">ANOVAa</td></tr><tr><td colspan="2">Model</td><td>Sum of Squares</td><td>df</td><td>Mean Square</td><td>F</td><td>Sig.</td></tr><tr><td rowspan="3">1</td><td>Regression</td><td>46.005</td><td>9</td><td>5.112</td><td>10.154</td><td>.000b</td></tr><tr><td>Residual</td><td>66.453</td><td>132</td><td>.503</td><td></td><td></td></tr><tr><td>Total</td><td>112.458</td><td>141</td><td></td><td></td><td></td></tr><tr><td colspan="7">a. Dependent Variable: Willingness(perception to cancer insurance policy)</td></tr><tr><td colspan="7">b. Predictors: (Constant MINPREMIUM, SUSPECTION, PENCOUNTER, EDU, TABILITY, FINCOME, INSUPOLICY, MOTIVATION, COST</td></tr></table>

Table 6

<table><tr><td colspan="7">Coefficientsa</td></tr><tr><td rowspan="2" colspan="2">Model</td><td colspan="2">Unstandardized Coefficients</td><td>Standardized Coefficients</td><td rowspan="2">t</td><td rowspan="2">Sig.</td></tr><tr><td>B</td><td>Std. Error</td><td>Beta</td></tr><tr><td rowspan="10">1</td><td>(Constant)</td><td>-.097</td><td>.564</td><td></td><td>-.172</td><td>.864</td></tr><tr><td>EDU</td><td>.135</td><td>.066</td><td>.140</td><td>2.042</td><td>.043</td></tr><tr><td>FINCOME</td><td>.108</td><td>.050</td><td>.151</td><td>2.158</td><td>.033</td></tr><tr><td>PENCCOUNTER</td><td>-.213</td><td>.164</td><td>-.090</td><td>-1.296</td><td>.197</td></tr><tr><td>INSUPOLICY</td><td>-.365</td><td>.238</td><td>-.110</td><td>-1.534</td><td>.127</td></tr><tr><td>Motivation</td><td>.201</td><td>.066</td><td>.225</td><td>3.069</td><td>.003</td></tr><tr><td>Suspension</td><td>.092</td><td>.066</td><td>.103</td><td>1.389</td><td>.167</td></tr><tr><td>Cost</td><td>.326</td><td>.076</td><td>.329</td><td>4.308</td><td>.000</td></tr><tr><td>TAbility</td><td>-.231</td><td>.069</td><td>-.233</td><td>-3.329</td><td>.001</td></tr><tr><td>MiniPremium</td><td>.509</td><td>.095</td><td>.381</td><td>5.357</td><td>.000</td></tr><tr><td colspan="7">a. Dependent Variable: Willingness(perception to cancer insurance policy)</td></tr></table>

[^127]: responses _(p.5)_

[^141]: responses _(p.7)_

[^142]: responses _(p.6)_

Generating HTML Viewer...

References

21 Cites in Article

Tahera Ahmed,Ashrafunnessa,Jebunnessa Rahman (2008). Development of a visual inspection programme for cervical cancer prevention in Bangladesh.

Hubert Amu,Kwamena Dickson (2016). Health insurance subscription among women in reproductive age in Ghana: do socio-demographics matter?.

A Ansink,R Tolhurst,Haque,S Saha,S Datta (2008). Cervical cancer in Bangladesh: community perceptions of cervical cancer and cervical cancer screening.

L Austin,F Ahmad,M Mcnally,D Stewart (2002). Breast and cervical cancer screening in Hispanic women: a literature review using the health belief model.

B Stafford,M (1995). 093047 (E10) Consumer risk perceptions and information in insurance markets with adverse selection.

Daniel Buor (2005). Determinants of utilisation of health services by women in rural and urban areas in Ghana.

M Bundorf,B Herring,M Pauly (1001). Health Risk Income, and the Purchase of Private Health Insurance.

David Cutler,Adriana Lleras-Muney (2006). Education and Health: Evaluating Theories and Evidence.

A Daniel Band Dadson (2013). Health insurance in Ghana: evaluation of policy holders' perceptions and factors influencing policy renewal in the Volta region.

David Dror,S Hossain,Atanu Majumdar,Tracey Pérez Koehlmoos,Denny John,Pradeep Panda (2016). What Factors Affect Voluntary Uptake of Community-Based Health Insurance Schemes in Low- and Middle-Income Countries? A Systematic Review and Meta-Analysis.

C Gronroos (1984). A Service‐Orientated Approach to Marketing of Services.

R Hubbard,Jonathan Skinner,Stephen Zeldes (1995). Precautionary Saving and Social Insurance.

Biplob Hossain,Humaira Rashid,Zannatun Noor,Mamun Kabir,Sohag Miah,Abdullah Siddique,Rashidul Haque (2016). A systematic review of human giardiasis in Bangladesh: public health perspective.

S Hussain,R Sullivan (2013). Cancer Control in Bangladesh.

C Jehu-Appiah,G Aryeetey,I Agyepong,E Spaan,R Baltussen (2011). Household perceptions and their implications for enrolment in the National Health Insurance Scheme in Ghana.

J Kimani,R Ettarh,C Warren,B Bellows (2014). Determinants of health insurance ownership among women in Kenya: evidence from the 2008-09 Kenya demographic and health survey.

Joses Kirigia,Luis Sambo,Benjamin Nganda,Germano Mwabu,Rufaro Chatora,Takondwa Mwase (2005). Determinants of health insurance ownership among South African women.

Tsai-Ching Liu,Chin-Shyan Chen (2002). An analysis of private health insurance purchasing decisions with national health insurance in Taiwan.

S Mustari,B Hossain,Diah,S Kar (2019). Opinions of the Urban Women on Pap test: Evidence from Bangladesh.

James Mulenga,Bupe Bwalya,Yordanos Gebremeskel (2017). Demographic and Socio-economic determinants of maternal health insurance coverage in Zambia.

Ashrafun Nessa,Khadiza Nahar,Shirin Begum,Shahin Anwary,Fawzia Hossain,Khairun Nahar (2013). Comparison between Visual Inspection of Cervix and Cytology Based Screening Procedures in Bangladesh.

No ethics committee approval was required for this article type.

Data Availability

Not applicable for this article.

How to Cite This Article

Rabeya Sultana Lata. 2026. \u201cPerception towards Cervical Cancer Insurance Policy: A Study on Women in Barishal City\u201d. Global Journal of Management and Business Research - C: Finance GJMBR-C Volume 23 (GJMBR Volume 23 Issue C4).

Explore published articles in an immersive Augmented Reality environment. Our platform converts research papers into interactive 3D books, allowing readers to view and interact with content using AR and VR compatible devices.

Your published article is automatically converted into a realistic 3D book. Flip through pages and read research papers in a more engaging and interactive format.

Our website is actively being updated, and changes may occur frequently. Please clear your browser cache if needed. For feedback or error reporting, please email [email protected]

Thank you for connecting with us. We will respond to you shortly.