Perspectives of the World Economy from a Geopolitical Perspective

α

Lucian Ivan Bucharest Academy of Economic Studies

Romanian Police Academy - the National College for Home Affairs

Romanian Defense University - the National Defense College

## I. INTRODUCTION

Forecasting trends in the world economy is very important, given the fact that without a relevant and pertinent forecast, it is not possible to carry out certain analyses that are useful for increasing the profitability of companies and, implicitly, for raising the standard of living worldwide. Major global geopolitical changes and the COVID-19 pandemic have had an impact on macroeconomic indicators, and the outlook is not encouraging, given the relatively indefinite continuation of the military conflict between the Russian Federation and Ukraine and the ongoing conflict in the Middle East. The outbreak of the COVID-19 pandemic has caused major disruptions in supply chains, and the military conflict provoked by the Russian Federation against Ukraine has triggered an unprecedented European energy crisis and a major food crisis, as well as a considerable increase in inflation leading to a synchronized global tightening of monetary policy.

Another important phenomenon to be taken into account in the evolution of the world economy is the dynamization of the flow of war refugees (in particular from Ukraine and Africa). A major risk is the possibility of an escalation of the military conflict in the Middle East, i.e. the generalization of the war between Israel and the Islamic Republic of Iran, which will lead to a massive flow of refugees from Israel in particular to Europe and the United States. For Europe, this refugee flow will overlap with the flow of economic and war-related migrants from the African region, which will put additional pressure on the European Union and on testing the resilience of European crisis prevention and crisis coping mechanisms. (European Union, 2024) The increase in the flows of war refugees and illegal migrants has led to the exacerbation of nationalist and sovereignist currents in several European countries, with effects including in the economic sphere, with populist measures being taken which will lead to a reduction in investment appetite and, implicitly, to a fall in economic growth.

Notwithstanding these negative developments, the global economy has shown a high degree of resilience, with stable and relatively steady growth, while inflation has returned to a normal trend, demonstrating the resilience and efficiency of the banking system. At the same time, the surge in inflation, despite its severity and the associated cost of living crisis, has not triggered uncontrolled price spirals worldwide. Thus, according to the International Monetary Fund (IMF) forecasts, global inflation is expected to fall from an annual average of $6.8\%$ in 2023 to $5.9\%$ in 2024 and $4.5\%$ in 2025, with advanced economies returning to their inflation targets faster than emerging and developing economies. The latest forecast for global growth over five years - $3.1\%$ - is at its lowest level in decades. The pace of convergence towards higher living standards for low- and middle-income countries has slowed, implying a persistence of large global economic disparities.

## II. SITUATION OF THE WORLD ECONOMY

Financial markets have reacted very well to the prospect of central banks exiting restrictive monetary policy. As a result, financial lending policies have eased, equities that had previously declined have risen by significant percentages, leading to a boost in capital flows to most emerging market economies. At the same time, resilient growth and faster disinflation point to favorable supply-side developments in international markets, including the unwinding of earlier shocks related to higher energy commodity prices, a remarkable rebound in labor supply supported by strong immigration flows in many advanced economies, particularly in the European area.

Despite these positive developments, many challenges remain and bold and decisive action is needed in view of the effects on the global economy. First, while inflationary trends are encouraging, long-term equilibrium in this economic indicator has not yet been reached. Somewhat worrying from a macro-economic point of view are the recent average headline and core inflation figures, which are on the rise. This may be short-term, but prudent measures need to be put in place that do not lead to higher inflation in the medium to long term.

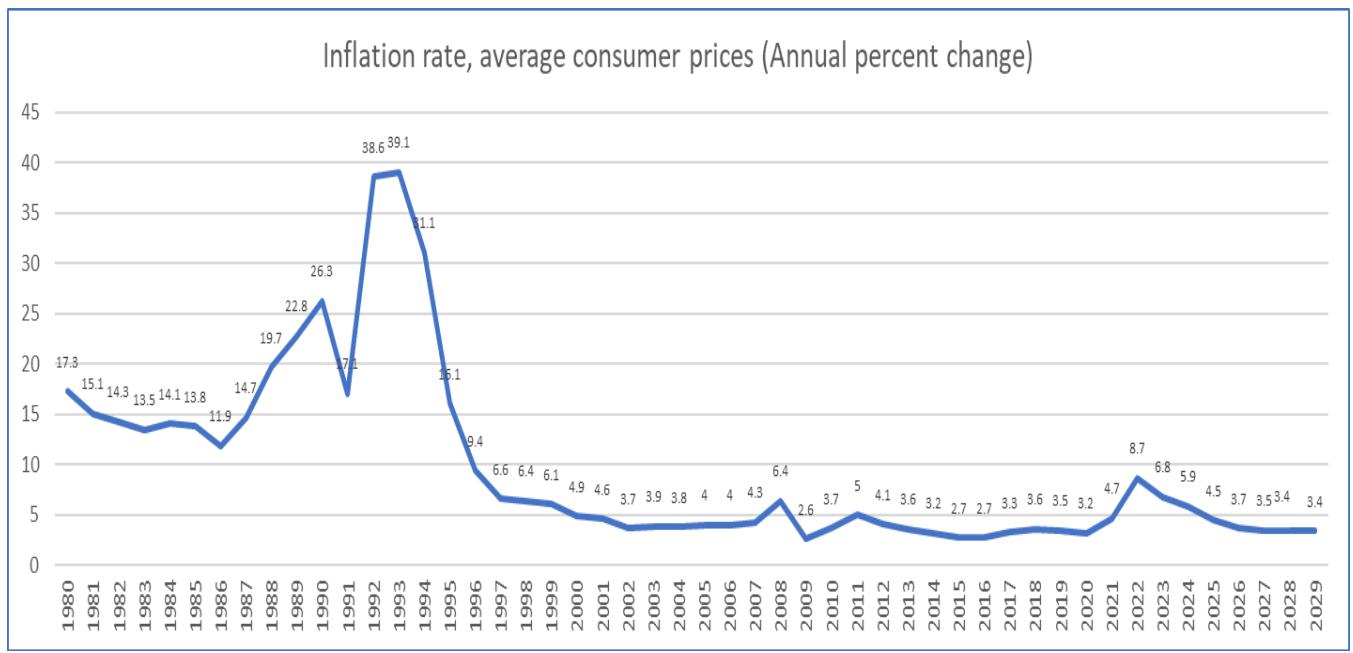

Graph No. 1: Estimated World Inflation Rate Relative to Average Consumer Prices (Annual Percent Change) Data source: IMF, own processing

Most of the progress in inflation came mainly from the fall in energy prices and consumer goods inflation below the average of recent years. Consumer goods inflation has been helped by the resolution of supply-chain disruptions as well as lower export prices of goods from China. A risk factor identified by economists is services inflation, which remains high and could derail disinflation. For the period ahead, it is essential that inflation rates return to a normal trend as estimated by the IMF in the graph above.

Second, the global outlook may mask strongly diverging trends both across countries and regions. The exceptional recent performance of the United States is certainly impressive and an important driver of global growth, but it also reflects strong demand factors, including a fiscal stance that is inconsistent with long-term fiscal sustainability. This poses short-term risks to the disinflation process, as well as longer-term risks to the fiscal and financial stability of the global economy, as it risks increasing overall financing costs.

In the euro area, growth will pick up in 2024, but from very low levels, as the lasting effects of monetary policy and past energy costs, as well as planned fiscal consolidation, weigh on economic activity. Continued high wage growth and persistently high inflation in the services sector could delay the return of inflation to equilibrium in the medium to longer term. However, unlike in the United States, there is little evidence of a stable economic recovery, and the European Central Bank will need to calibrate and proceed cautiously with monetary easing to avoid an excessive slowdown in economic growth and inflation below the current level. (International Monetary Fund, 2024).

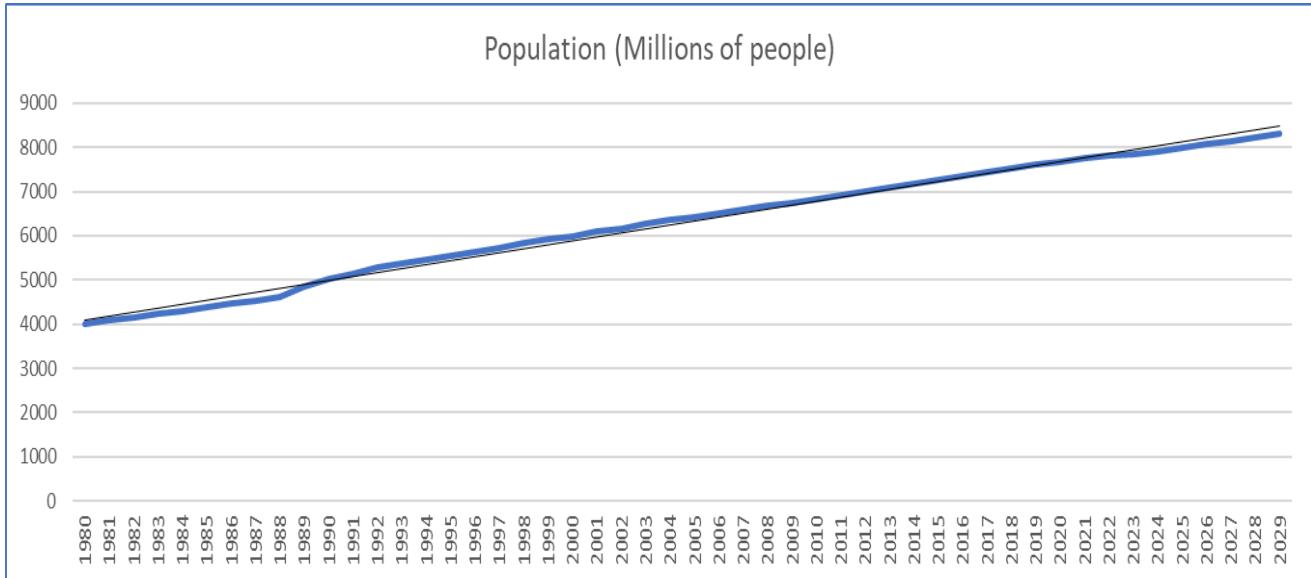

An important economic factor is global population growth. Currently the global population is 7.85 billion, and forecasts for 2029 estimate a global population of around 8.29 billion people. Global population growth must be matched by growth in the resources needed for life, especially food and water. This must be understood by economically developed countries, which must identify the resources needed to provide the necessities of life in disadvantaged areas in Africa and the Middle East in order to limit economic migration. One example of this is Ukraine, which exports large quantities of cereals to Africa, but, as a result of the war with the Russian Federation, there have been major shortfalls in the delivery of these quantities of cereals needed by African countries, which has made it necessary to find economically and logistically viable solutions quickly.

Data source: IMF, own processing

### Graph No. 2: World Population Estimates (1980-2029)

As can be seen from Graph 2, global population growth is a linear phenomenon, mainly due to the increase in life expectancy, against the background of the relevant development of medicine and the pharmaceutical industry worldwide. This population growth is not a brake on the world economy, given that there are enough resources on Planet Earth to feed a population perhaps twice as large as today. Technological progress in all areas can make up for the relative scarcity of resources, and the phenomenon of food wastage and over-allocation of resources that do not necessarily produce added value must be stopped as far as possible in developed countries.

Population growth is not uniform at global level, for example in European countries there is a decrease in the native population, but the lack of employees on the labor market is replaced by migrants, who are generally cheap labor, given that most of them coming from Africa and the Middle East do not have higher education, accepting jobs that do not require a high qualification and lower wages. For a while this policy had spectacular economic results in European countries, but with the extraordinary technological developments (e.g. the rapid development of artificial intelligence, automation of productive companies), some jobs will no longer be of interest in the medium and long term, which will lead to

Data source: IMF, own processing

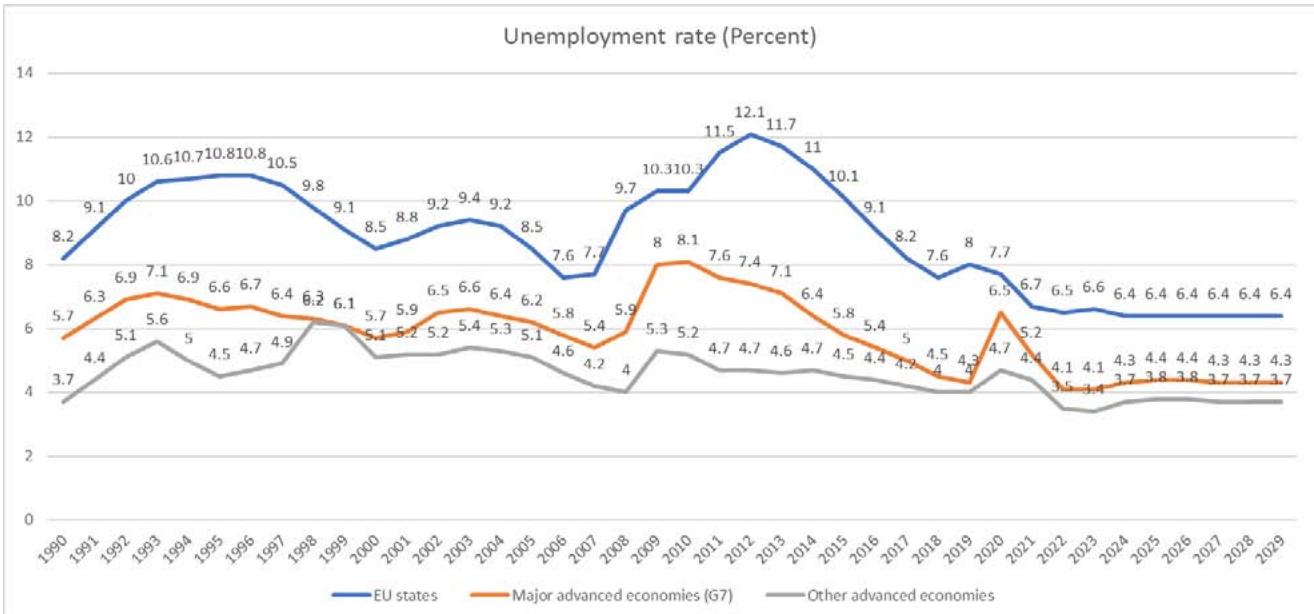

Graph No. 3: Estimated World Unemployment Rate (%)

The analysis in Graph no. 3 reveals differences in inflation rates across EU Member States, G7 and other advanced economies. Thus, the highest unemployment rate will be recorded in the EU Member States, which are not so well adapted to cope with the major technological changes that will become more pronounced in the near future, while the G7 Member States, particularly the United States, are investing heavily in technological developments, especially in the IT area and especially in the technological development of artificial intelligence. In fact, artificial intelligence is the inflection point for a new technological revolution, and the driving force behind this development is the USA, where the main companies developing this innovative and pioneering technology are based. In this context, we should also not overlook the technological development of China, which has recently been investing heavily in education and fundamental and applied research, with the aim of overcoming the technological gap with the USA and the developed economic countries as quickly as possible. In the meantime, European states, especially EU Member States, benefiting from US technological support will catch up with the existing technological gaps by adapting its policies to maximize the use of modern technologies and benefit from the gains brought by them. (European Union, 2024).

At the same time, there is a phenomenon of rejection of migrants in European society, with direct societal effects in the sense that nationalist and sovereignist currents have gained strength recently in some EU Member States. Even within the European Union there are divergent positions on the acceptability and reception of migrants and war refugees. Hungary and Austria, for example, strongly advocate banning migrants on their territory and deporting them to their countries of origin. Banning migrants in Europe is by no means a medium and long term solution, the only viable solution is to implement effective policies for their full inclusion in European culture through paradigm shifts and a flexible and open approach from European society as a whole.

Although the labor market appears solid, this solidity could prove illusory if European companies have been hoarding labor in anticipation of a recovery that has so far failed to materialize. Unfortunately, the European economy seems more traditionalist, in the sense that change is slower and economic reforms in the EU institutions are relatively late in coming, amid excessive bureaucracy in Brussels, due to the cumbersome and slow economic and political decision-making process. Already in some EU Member States (e.g. Germany) the economic momentum has slowed down considerably due to rising utility prices, especially energy prices, resulting in reduced exports and, in turn, rising unemployment and social tensions in German society. This substantial reduction in exports will also have horizontal repercussions. An example in this respect is Romania, which statistically exports the most to the German market, especially to the automotive industry. The fall in Germany's export figures will also have repercussions on the Romanian economy, with effects including an increase in unemployment and, implicitly, an increase in tensions at a societal level.

China's economy is being hurt by a sustained slowdown in real estate. Credit booms and crises are never resolved quickly and this is no exception. Domestic demand will remain weak for some time unless strong measures and reforms address the root cause. Public debt dynamics are also worrying, especially if the housing crisis turns into a local public finance crisis. With weak domestic demand, external surpluses could rise on the back of low prices charged by Chinese companies, which have a major advantage in that environmental regulations are very lax, and the fact that in some cases they receive substantial subsidies from the Beijing government authorities. The risk is that this will further exacerbate trade tensions in an already tense geopolitical environment, particularly on the relationship with the US and EU Member States. (OECD, 2024).

At the same time, many other large emerging market economies are performing robustly (e.g. India), sometimes even benefiting from the reconfiguration of global supply chains and rising trade tensions between China and the United States. Their footprint on the world economy is now growing and they will play an increasingly important role in sustaining global growth in the coming years.

A worrying development is the growing divergence between many low-income developing countries and the rest of the world. For these economies, growth is revised down while inflation is revised up. Worse, unlike in most other regions, the estimates for low-income developing countries, including some large countries, have been revised upwards, suggesting that the poorest countries are not yet in a position to recover from the pandemic and the cost of living crisis. In addition, conflicts continue to cause loss of life and increase geopolitical uncertainty. These effects are predominantly felt in sub-Saharan Africa, where countries relatively rich in mineral resources face persistent and bloody military conflicts. In this context, the following African states where bloody conflicts have occurred or are still occurring are worth mentioning: Burkina Faso, Burundi, Cameroon, the Central African Republic (CAR), Chad, the Democratic Republic of the Congo (DRC), Ethiopia, Kenya, Mali, Mozambique, Niger, Nigeria, Somalia, South Sudan and Sudan. (World Bank, 2024).

For these countries, investing in structural reforms to promote domestic and foreign direct investment that foster growth and enhance domestic resource mobilization can help manage borrowing costs and reduce financing needs while achieving development objectives. Efforts also need to be made to improve the human capital of the young and large population by providing education and by offering high quality health services to reduce mortality, especially infant mortality.

Third, even as inflation is falling, real interest rates have risen and sovereign debt dynamics have become less favorable, especially for highly leveraged emerging markets. In this context, these highly indebted countries should turn their attention to efficient mechanisms to collect taxes and duties from companies and the population. Only credible fiscal consolidation contributes to reducing financing costs and genuinely strengthening financial stability.

In a world with much more frequent adverse shocks than in other historical periods, characterized by major disruptions in the supply of raw materials and growing fiscal needs, adaptation to climate change, digital transformation, energy security and defence consolidation should be a policy priority. However, this is never easy to achieve, given that fiscal consolidations are more likely to succeed when they are credible and implemented in periods when the economy is growing, rather than when markets dictate their terms.

In countries where inflation is under control and which are engaged in a credible multi-year effort to strengthen fiscal policies, monetary policy can help support activity. The successful policy of fiscal consolidation and monetary accommodation of 1993 in the US can be evoked in this context.

Fourth, medium-term growth prospects remain historically weak. The main cause is the lower growth of the total productivity of the relevant economic factors. A significant part of the decline stems from the misallocation of capital and labor within productive sectors and states. Facilitating a faster and more efficient allocation of resources used in the production process can help stimulate sustainable growth in the medium and long term. Currently, economists are mainly counting on the fact that artificial intelligence (AI) will generate strong increases in productivity in the medium and long term. It is statistically possible for this to happen, but the potential for serious disruption to labor and financial markets is extremely high. Maximizing the potential of AI for all relevant actors (e.g. government institutions, companies, population) will require states to be able to improve their digital infrastructure, invest in human capital and coordinate on global norms on movement of goods and services.

Also, medium and long-term growth prospects are affected by increasing geo-economic fragmentation and the sharp increase in trade restrictions and industrial policy measures, as early as 2019. Global trade linkages are already changing as a result, which may lead to potential efficiency losses and lower production yields. But the bigger damage is the one brought to global cooperation and multilateralism, aspects that will lead to affecting the business climate at the global level. At the same time, economists believe that huge global investments are needed for an ecological future and resistant to climate changes that produce relevant economic losses through the devastating effects of natural cataclysms produced worldwide.

As can be seen in recent decades, emission reductions are compatible with economic growth, where growth has become much less emissions intensive. However, emissions continue to rise amid environmental non-compliance by certain states (e.g. China, India) that do not have and/or implement effective environmental regulations to produce sustainable growth and with strict adherence to menu items dedicated to reducing the carbon footprint. Much more needs to be done in this area, and much faster. Thus, investments in ecology have expanded at a healthy pace in advanced Western states, but there are still many states that consider that these investments in protecting nature and environmental factors are not a priority at the moment.

Reducing subsidies to help reduce the use of fossil fuels cannot effectively contribute to the creation of the necessary fiscal space for the continuation of ecological investments. The greatest efforts must be made by other emerging and developing market economies, which must massively increase the growth of green investments and reduce their investments in fossil fuels. This will require technology transfer from other advanced economies as well as financing, much of it coming from the private sector. In terms of resolving these issues there is little hope for progress outside multilateral frameworks and consistent international cooperation worldwide.

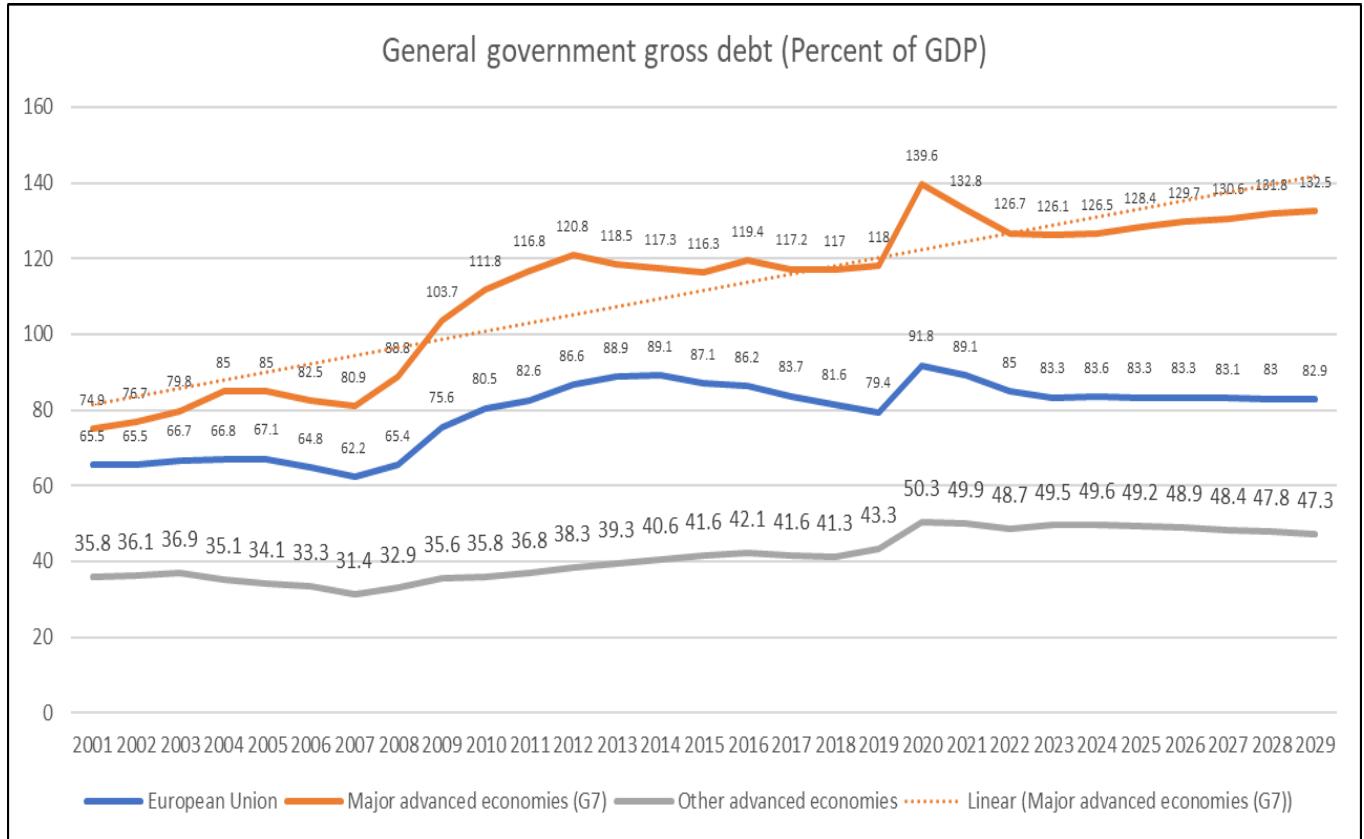

Global economic development cannot be achieved without increasing the sovereign debt of states. In this context, it is necessary for the states to be able to borrow from the financial markets, but a lot of attention is needed in the efficiency with which the amounts of money coming from government or private loans are used to achieve the proposed objectives. In this context, it is necessary for each state to act prudently with regard to the degree of indebtedness, with the aim of effectively managing the balance of trade and payments.

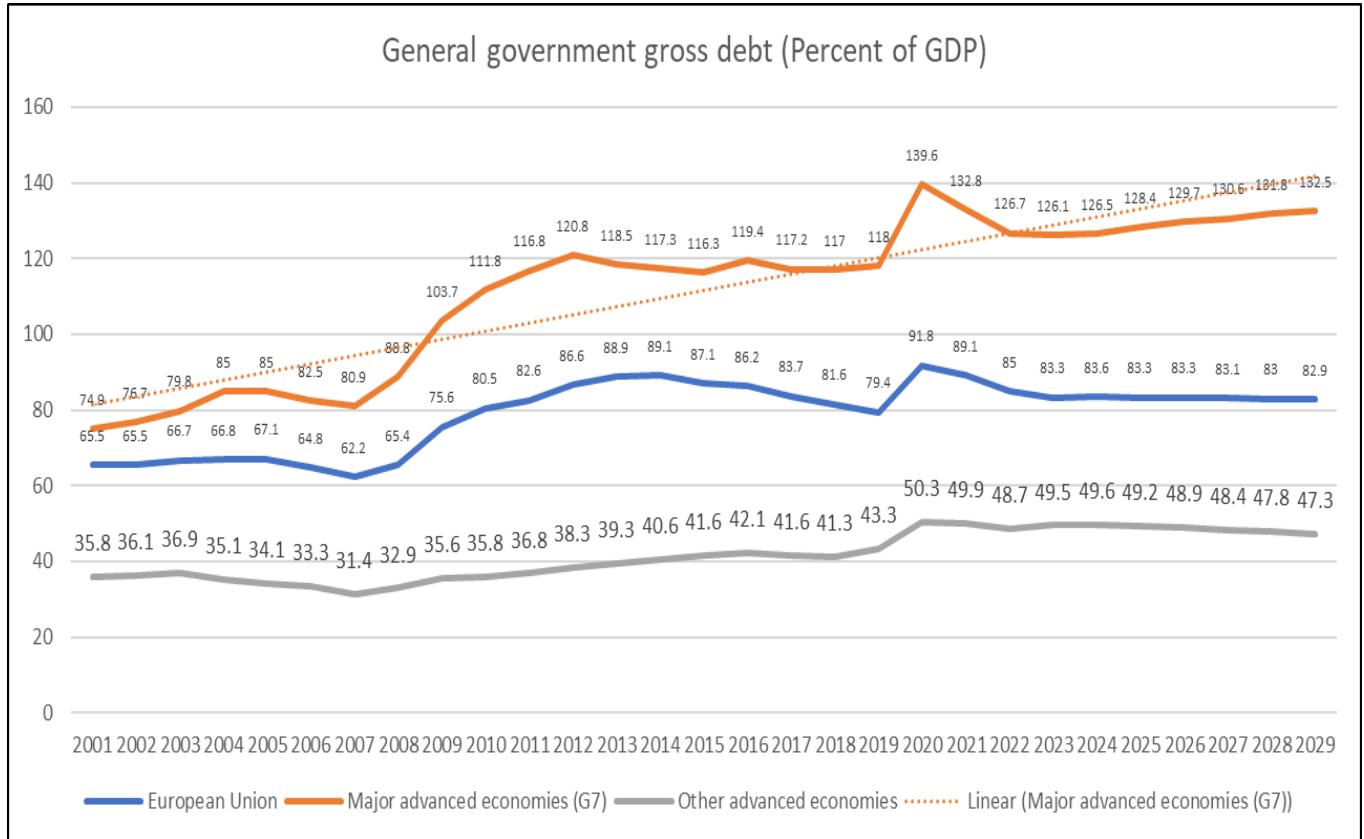

Graph No. 4: Estimated Global Debt (Percentage of GDP) Data source: IMF, own processing

Analysis of Chart no. 4 reveals the increasing trend of government and private debts in the most economically developed states (G7 Group), while at the level of the EU member states and other advanced economies, the decreasing trend of these debts will be noted, on the background of more restrictive commercial policies that aim to reduce the trade balance deficit, including by sharply reducing budget expenditures.

## III. CONCLUSIONS

Risks to the global outlook are currently largely balanced. On the negative side, further increases in prices, including energy raw materials, generated by geopolitical tensions, including those generated by the war in Ukraine generated by the Russian Federation and the conflict in Gaza and Israel, could, together with persistent core inflation in the conditions where labor markets are still tight, to raise interest rate expectations and lower asset prices.

The resilience of global economic activity has been compatible with falling inflation due to a postpandemic supply-side expansion. Better-than-expected labor force growth amid robust employment growth supported activity and disinflation in advanced economies and several large emerging market and middle-income economies.

Also, a divergence in the pace of disinflation among major economies could cause currency moves that put financial sectors under pressure. High interest rates could have a bigger-than-expected chilling effect as fixed-rate mortgages reset and households face high debt, causing financial stress. In China, without a comprehensive response to the property sector experiencing major problems, economic growth could be inconsistent in the medium to long term, affecting trading partners. Against the backdrop of high public debt in many economies, a disruptive shift towards raising taxes and cutting spending could weaken economic activity, erode confidence and reduce support for reforms and spending to reduce the risks of climate change.

GEOEconomic fragmentation could intensify, with greater barriers to the flow of goods, capital and people, implying a slowdown in the world economy. On the other hand, a looser fiscal policy than needed and assumed in the projections could increase economic activity in the short term, although it risks a more costly adjustment of economic policy in the long run. Inflation could fall faster than expected amid further increases in labor force participation, allowing central banks to get ahead of easing plans. Artificial intelligence and stronger-than-anticipated structural reforms could boost labor productivity.

In conclusion, as the world economy approaches a linear and relatively slow securitization trend, the short-term priority of central banks is to ensure that inflation settles on a safe trend, without prematurely relaxing financial policies and monetary prudential and without delaying too much the adoption of economic, fiscal and monetary reforms to overcome possible risk situations.

Generating HTML Viewer...

Funding

No external funding was declared for this work.

Conflict of Interest

The authors declare no conflict of interest.

Ethical Approval

No ethics committee approval was required for this article type.

Data Availability

Not applicable for this article.

How to Cite This Article

Lucian Ivan. 2026. \u201cPerspectives of the World Economy from a Geopolitical Perspective\u201d. Global Journal of Management and Business Research - B: Economic & Commerce GJMBR-B Volume 24 (GJMBR Volume 24 Issue B2): .

Explore published articles in an immersive Augmented Reality environment. Our platform converts research papers into interactive 3D books, allowing readers to view and interact with content using AR and VR compatible devices.

Your published article is automatically converted into a realistic 3D book. Flip through pages and read research papers in a more engaging and interactive format.

Our website is actively being updated, and changes may occur frequently. Please clear your browser cache if needed. For feedback or error reporting, please email [email protected]

Thank you for connecting with us. We will respond to you shortly.