The article examines the main features of the development of the digital economy in the developed countries of the world. Some aspects of the introduction of digital currencies, the impact of the digitalization process on the financial system and monetary policy of different countries are reflected, and the possibilities of legal regulation of the use of digital financial assets in developed countries of the world are highlighted. As a result of the research, a review of scientific, practical, statistical information was made, and the author’s conclusions were given.

## I. INTRODUCTION

The modern world is going through an era of significant transformations, many of which are related to the process of digitalization. This phenomenon has a profound impact on various aspects of society, primarily on the economy. The digitalization process not only makes adjustments to existing business models, but also contributes to the creation of new structures, mechanisms and platforms [2, pp. 36-37; 10].

## II. RELEVANCE

Special attention should be paid to the fact that digitalization helps the economy to be more flexible and adaptive to changes. This creates prerequisites for sustainable development and the improvement of the quality of life of the population. Thus, digitalization not only changes the existing world, but also contributes to the transition to a new era of significant global transformations. In the era of digitalization, we are witnessing the transformation of the economic environment, which led to the formation of such a concept as the "digital economy" [11].

The purpose of the study is to consider the main features of the transition to the digital economy in the developed countries of the world.

## III. MATERIALS AND METHODS OF RESEARCH

Analysis of scientific and practical, statistical information, generalization, synthesis of opinions, graphical interpretation of the results.

## IV. THE RESULTS OF THE STUDY

a) The development of financial technologies (Fintech) in different countries

The development of Financial Technology not only contributes to the creation of new value, but also plays a key role in the transformation of traditional financial institutions into their digital counterparts. The essence of Finance is to optimize financial processes, which leads to increased revenue and reduced costs.

The main aspects and advantages of Fintech include:

1. Transformation of material institutions: Financial technology allows banks and other financial institutions to move to a digital platform, providing faster and safer services.

2. Value creation: Innovations in the field of financial technologies are aimed at increasing efficiency, which leads to increased income and reduction of unnecessary expenses [4].

3. Fintech helps small businesses turn large amounts of information into manageable and understandable data.

4. Fintech provides access to a new type of service.

5. The use of Financial Technology allows you to significantly expand the financial capabilities of organizations.

6. The use of Financial Technology allows you to automate accounting procedures.

7. Many fintech applications simplify the process of creating accessible e-commerce websites for small businesses, allowing them to offer their products globally [10].

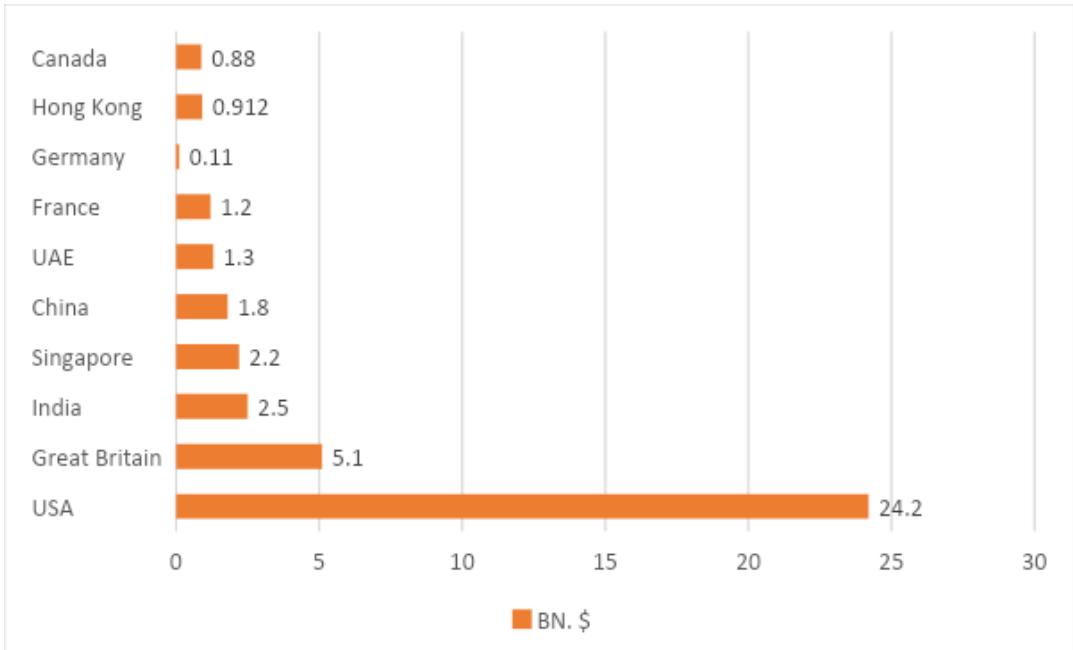

The development of Financial Technology is bringing significant changes to the financial services sector, which is confirmed by a number of studies. Research shows that over the past four years there has been a significant increase in interest in Fintech startups, which is reflected in the volume of investments. The highlights of these studies include:

Financing of Financial startups in the world has increased by more than $39\%$.

In 2023, the global financial technology market experienced a significant decrease in investment activity, as shown by data published by Innovate Finance on January 10, 2024. The amount of investments in this sector fell to $51.2 billion, which is

Figure 1: The volume of investments in Finance by developed countries [9]

b) The development of digital currency in developed countries

- The digital currency, which appeared quite recently, has already established itself as an important tool in the work of financial systems. In different countries of the world, it has received various statuses: from full recognition at the state level to a limited or even prohibited status. This diversity of approaches to digital currency regulation highlights their complexity and novelty for traditional financial systems. Central banks in various countries have begun to adapt their strategies for managing the monetary fund, taking into account the opportunities and challenges presented by digital currencies. Therefore, their introduction, although a relatively new phenomenon, has already had a significant impact on the market environment [6].

c) Analysis of the impact of digital currencies on the financial system and monetary policy of different countries

The introduction of a central banking digital currency (CBDC) represents a significant step in the evolution of the modern financial system. This new form of money, due to its unique characteristics, can radically change the approaches to conducting monetary policy. The issue of the potential possibility of accruing interest on the central banking digital currency is becoming particularly relevant, which could attract more users and increase its popularity among economic agents. Consideration of such an aspect as the accrual of interest to holders of digital currencies is becoming one of the key tasks in the process of developing and implementing a central banking digital currency. This function can play an important role in determining the degree of demand for this type of asset in the market. Depending on how interest charges are arranged, digital currencies can either stimulate economic activity or put pressure on traditional banking services.

The impact of a central banking digital currency on the financial system of developed countries will depend on many factors, including its acceptability and ease of use for the public and businesses. As different models and approaches to its management are approved and implemented, different impacts on the market environment can be expected. This, in turn, will have consequences for the regulatory structures and monetary policy of the state. To support economic activity and strengthen financial stability during periods of economic downturn, Central Banks of developed countries actively apply monetary policy measures, including both conventional and innovative approaches. In these circumstances, they seek to regulate interest rates to stabilize the financial system and reduce economic risks. This time is often characterized by a decline in the creditworthiness of financial institutions, which underscores the importance of moving to the full use of digital transformation opportunities.

d) Development of digital financial assets in the USA, Russia and other countries

Recently, the digital asset industry, in particular cryptocurrencies, has faced significant difficulties, described as a "crypto winter", which has stimulated analytical speculation about its future. However, an interesting reason for this decline is that the actions of regulators, who accused key figures of fraud, unexpectedly contributed to the identification of organizations seeking to offer real and practical solutions. This process was most often typical for the United States. It seems that the future of digital assets will be determined by: acceptance into the digitalized financial system, the reliability of the products offered and strict compliance with regulatory requirements.

Currently, in developed countries (USA, Russia, China, etc.), there is an increasing trend of integration of decentralized finance (DeFi) with long-existing financial systems (TradFi) on the market. In the past, traditional financial institutions were extremely skeptical about cryptocurrencies, but over the past year there has been a noticeable jump in their interest in blockchain technologies. An example of this is the actions of BlackRock, which applied to create ETFs for bitcoin, Ethereum and HSBC, while starting cooperation with Metaco to develop custodial services for tokenized securities.

In the run-up to 2024, the emergence of bitcoin as an institutional asset is becoming more and more obvious. Global financial institutions, including major players such as JPMorgan Chase, Morgan Stanley and Goldman Sachs, are actively forming teams specializing in cryptocurrencies and blockchain technology, which indicates the strategic nature of their interest in this sector. They strive not only to satisfy customer needs, but also to expand their own influence in the market. This process is not limited to the impact only on the United States, as financial institutions around the world are actively exploring the possibilities of Digital Assets. The expectation of Bitcoin ETF approval from the SEC also helps to strengthen the confidence of many global communities in Central Asia at the institutional level [8].

### e) Analysis of the legal regulation of Digital Assets

From 2019 to 2024, the introduction of a new legal approach in the field of digital tokens in some countries began, including the development of specialized procedures for their issuance, storage and exchange using DLT technologies. Subsequently, in 2020, the European Commission presented an initiative to introduce regulations for the experimental application of distributed ledger technology in the financial infrastructure, which provides for the circulation of shares and bonds with registration through DLT. This practice has been actively investigated in Europe since 2021, including Germany, where appropriate electronic legislation has been introduced.

In Switzerland, the DLT registry has begun to be used to issue limited liability shares and debt obligations, including bearer bonds.

In the United States, cryptocurrencies can be classified in different ways, depending on their use: as a means of payment, as property, or as an exchange commodity. At the federal level, the main focus is on legislation aimed at countering the legalization of criminal proceeds, while existing legal norms are applied to other aspects. Issues related to the specific application or the complete prohibition of cryptocurrencies are left to the discretion of the legislatures of individual states.

Since 2021, a new Federal Law No. 259-FZ has been in force in Russia [12]. According to Federal Law 259-FZ, "digital financial assets are digital rights, including monetary claims, the possibility of exercising rights under equity securities, the right to participate in the capital of a non-public joint-stock company, the right to demand the transfer of equity securities provided for by the decision on the issue of DFA."

It allows the creation of digital assets similar to securities. The definition of the DFA under paragraph 2 of Article 1 includes not only monetary claims, but also opportunities related to equity securities, including participation in the capital of closed joint-stock companies and the right to demand the transfer of these securities. Currently, two ways of tokenizing assets are regulated in Russia: firstly, by issuing DFAs for existing securities, and secondly, by issuing shares in the DLT system, where such shares are recorded and stored without the need to contact traditional depositories.

Table 1: Comparison of CFA regulation in Russia and the world [13]

<table><tr><td>Legislation of the Russian Federation</td><td>An analogue in the foreign market</td></tr><tr><td>DFA (Part 2 of Article 1 of the DFA Law)</td><td>Security tokens

Digital analogues of securities or financial instruments. Certify the rights to own shares in the company, participate in management and/or receive income (dividends, profits). Regulation of the securities market is applied. Issuer: relevant: company or its authorized partner. Example: Tokenized TBILL Treasury bonds.</td></tr><tr><td>DFA (Part 2 of Article 1 of the DFA Law)</td><td>Asset-backed tokens

They are provided with real liquid assets: both services and goods, for example, oil or gold. The issuer guarantees that one token corresponds to a certain amount of a real asset and owns the required amount of this asset. Example: A Pax Gold token (PAXG) backed by gold stored in LBMA's London vaults.</td></tr><tr><td>DFA (Part 2 of Article 1 of the DFA Law)

Hybrid Digital Rights (Article 6, Article 1 of the Federal Law on DFA) = DFA + accounting and system cryptocurrency platforms</td><td>Stable coin (backed by flat money and real assets)

Some of these tokens are backed by real assets, such as metal, while others may be linked to cryptocurrencies. In the first case, they are more correctly attributed to asset-backed tokens, and in the second — to payment tokens.</td></tr><tr><td>Hybrid Digital Rights (Article 6, Article 1 of the Federal Law on DFA) = DFA + accounting and system cryptocurrency platforms</td><td>NFT

Non-interchangeable tokens can be used to create, trade and exchange unique digital objects, for example, objects of digital art. Example: NFT based on Gucci Ghost graffiti, Cryptokitties.</td></tr></table>

Digital financial assets can be divided into five types:

- Monetary requirements.

- The possibility of exercising rights on equity securities.

- The right to participate in the capital of a non-public joint-stock company.

- The right to demand the transfer of equity securities. Hybrid digital financial assets.

In accordance with the law, digital financial assets are not a means of payment, but at the same time, any actions provided for by the Civil Code of the Russian Federation can be performed with the DFA: buy, sell, exchange, mortgage, donate, inherit.

DFA issuance and repayment are carried out by information system operators (ISO), and their secondary handling of settlements within the framework of the platform is carried out by DFA exchange operators. An OIS differs from an exchange operator in that it can issue (issue) DFA and organize their trading on its platform, and does not have the right to trade DFAs issued by another ISO. The exchange operator, on the contrary, can organize the trade of DFAs that were previously issued by other market participants, but does not have the right to issue DFAs. At the moment, ten information system operators are included in the register of the Central Bank of the Russian Federation: Alfa-Bank JSC (A-token), Atomize LLC, Sberbank PJSC, Lighthouse LLC, Distributed Registry Systems LLC (Masterchain), Tokens LLC (Tokeon), EUROFINANCE MOSNARBANK JSC, SPB Exchange PJSC, LLCBlockchain Hub", NPOs of JSC "NSD". The exchange operator is only one organization - PJSC Moscow Exchange [14].

The DFA market is at the initial stage of development and is many times inferior in volume to the market of traditional financial instruments. However, since the release of the first deals in August 2022 to the present, the total volume of DFA issues has already amounted to over 74 billion rubles, which confirms the dynamic development of the digital finance segment and the growing interest from investors and market participants.

## V. CONCLUSION

Thus, according to the study, the digital transformation of the financial sector and the modernization of monetary policy around the world can be described as a multi-level and complex process. It includes the following key aspects:

1. Development of high-tech digital solutions.

2. The introduction of information technology in various spheres of life.

3. Integration of technological innovations into the national development of all industries.

In the economic sphere, the process of digitalization causes structural changes that can be observed in the following areas:

- Optimization of production processes.

- Personalization of products and services.

- Improve customer engagement through digital platforms.

- Introduction of Digital Assets and modernization of monetary policy.

The article considered the main aspects of the transition of developed countries to the stage of information modernization. The study reflects the features of the introduction of digital currency, the impact of Digital Rights on the Financial system and monetary policy of different countries, highlights some provisions of the legal regulation of the use of Digital Assets in developed countries of the world.

Generating HTML Viewer...

References

14 Cites in Article

Maria Girich,Ivan Ermokhin,Antonina Levashenko (2022). Comparative Analysis of the Legal Regulation of Digital Financial Assets in Russia and Other Countries.

V Iordanova (2022). The impact of digitalization of the world economy on economic growth in the countries of the world (on the example of China and the USA).

Elena Karanina,Dmitry Skopin (2023). DEVELOPMENT OF DIGITAL FINANCIAL ASSETS: FOREIGN EXPERIENCE.

Yu Mikerova Digital economy and the development of international finance.

F Mikerova,Kevorkov (2022). Economics and Business: theory and practice.

D Sakharov (2021). Digital currencies of central banks: key characteristics and impact on the financial system.

A Sigal,V Sigal,E Gusev (2024). Digital national currencies: the experience of introducing the digital ruble in Russia and comparison with analogues in other countries / A.

Renaud Foucart (2024). Curious Kids: how much money is there in the world?.

(2024). Fig. 2. Trends in the application of certain measures (URL: http://www.cdep.ru/?id=79) (access date: April 3, 2024).).

A Annex (2019). OECD/INFE Report on Financial Education in APEC Economies. Policy and practice in a digital world.

Hal Varian (2016). Grundzüge der Mikroökonomik.

A Torgersen (2020). On some topical issues of Regulatory Regulation of the Circulationof civilian weapons in the context of the Adoption of Federal Law No. 231-FZ dated June 28, 2021«On Amendments to the Federal Law «On Weapons» and Certain Legislative Acts of the Russian Federation».

(null). Figure 8: View of the annual financial statement of the MCB bank (Source: https://www.mcb.com.pk/assets/documents/Annual-Report-2020.pdf)..

No ethics committee approval was required for this article type.

Data Availability

Not applicable for this article.

How to Cite This Article

Yuriy V. Lyandau. 2026. \u201cThe Development of the Digital Economy in 2024 – Facts and Figures\u201d. Global Journal of Human-Social Science - E: Economics GJHSS-E Volume 24 (GJHSS Volume 24 Issue E2): .

Explore published articles in an immersive Augmented Reality environment. Our platform converts research papers into interactive 3D books, allowing readers to view and interact with content using AR and VR compatible devices.

Your published article is automatically converted into a realistic 3D book. Flip through pages and read research papers in a more engaging and interactive format.

The article examines the main features of the development of the digital economy in the developed countries of the world. Some aspects of the introduction of digital currencies, the impact of the digitalization process on the financial system and monetary policy of different countries are reflected, and the possibilities of legal regulation of the use of digital financial assets in developed countries of the world are highlighted. As a result of the research, a review of scientific, practical, statistical information was made, and the author’s conclusions were given.

Our website is actively being updated, and changes may occur frequently. Please clear your browser cache if needed. For feedback or error reporting, please email [email protected]

Thank you for connecting with us. We will respond to you shortly.