### The Energy-Environment Puzzle - Reconciling Conflicting Goals

## I. INTRODUCTION - MANAGING TRANSFORMATIONS

Zhou Enlai, the Chinese statesman who served as the first Premier of the People's Republic of China, was once asked what he thought of the French

Revolution. Popular lore has it that he responded that it was too early to tell.

Whether this is an accurate depiction of his thought or not, this cautious evaluation of such distant events could certainly apply to most revolutions, as he certainly must have learned -- as for that matter in any major change in structures and practices needed in recent developments on energy transition and environmental implications. A lot of assertions have been made on the role that growth of renewable sources of energy sources can play, the contamination that fossil fuels generate, and ultimately the type of energy mix one has to build -but, as in well-meaning revolutions, reality has shown to be more challenging to tame to produce the desired outcomes.

Conversely, limited attention seems to have been focused on the structural changes taking place in world economies and their impact on aggregate energy demand, affordability and reliability of different sources of energy. Ultimately, what matters is how all sources, put together, affect the trajectory of aggregate demand and their impact on carbon emissions and climate change.

After all, modern civilization, has acquired the power to prevent famines, contain epidemics, and mitigate natural disasters, such as hurricanes and even earthquakes. Energy, in its different forms is no different and ultimately is part of this evolution. In general, the acquisition of power and its different forms, the management among them, has enabled more effective management of risks, while simultaneously increasing the dangers that power systems may pose to themselves. For this reason, we must abandon both the naïve and populist views of imposing some arbitrary standards, and put aside our fantasies of infallibility, to commit ourselves to the hard and rather mundane work of building institutions and policies with strong self-correcting mechanisms to avoid misguided or ineffective efforts. This is perhaps the most important takeaway of development over the last decades, where the decarbonization efforts and the associated energy transition investments were ultimately aimed at reducing global warming that, for the time being at least, doesn't appear to be even near.

## II. SO, WHAT IS HAPPENING?

Technology is rarely deterministic, and the same technology can be used in various ways. While it has always been a catalyst for major historical changes -- sometimes positive ones, often not so, but it invariably creating new developments - oftentimes revolutions included side effects alongside. For this reason alone, such developments need concurrent tracking to ensure timely and proper corrective actions if such changes start generating undesirable or insufficient impact.

This, of course, is more easily said than done. Oftentimes, technological developments and associated institutional changes are more than capable of promoting distorted worldviews, enabling egregious abuses of power. Such developments have tended to instigate single-minded militant and promotional views, which have repeatedly throughout history generated extreme circumstances, with their share of terrifying new witch hunts.

## III. WHAT IS THE ACTUAL RECORD? - PROJECTIONS VS. OUTCOMES

Broadly speaking, leaving fine points aside, here is a broad-brush record and outlook of global supply and demand for energy of the last ten years and how we are headed into the future.

An international outlook serves multiple purposes. First and foremost, it establishes the basis for long-term business planning of all actors concerned. In general, the energy industry is capital intensive and long term by nature. We thus need to understand what the world could look like in coming decades to plan and deploy capital wisely. Emerging markets alone (where the bulk of growing energy demand is taking place as a result of economic growth and urbanization) developing countries will need to spend an additional $1 trillion per year on climate-related goals by 2025 and around $2.4 trillion per year by 2030.

Yet the global outlook serves a broader purpose as well. Energy and products are inseparable from modern life. Access to affordable and reliable energy drives unprecedented economic progress and improved living standards. They also contribute to global emissions. A global outlook provides essential insights into the economic advantages and environmental considerations that play a part in the future of energy.

The projections at the heart of the outlook represent a most likely (not single-minded) view of the world in 2050. It is generally scientifically grounded, based on detailed analysis of a variety of data sources and long-term assessments of market fundamentals, economic trends, technology advancements, consumer behavior and climate-related public policy. It is not an endorsement of a particular outcome, nor is it advocating for what any single source hopes will happen.

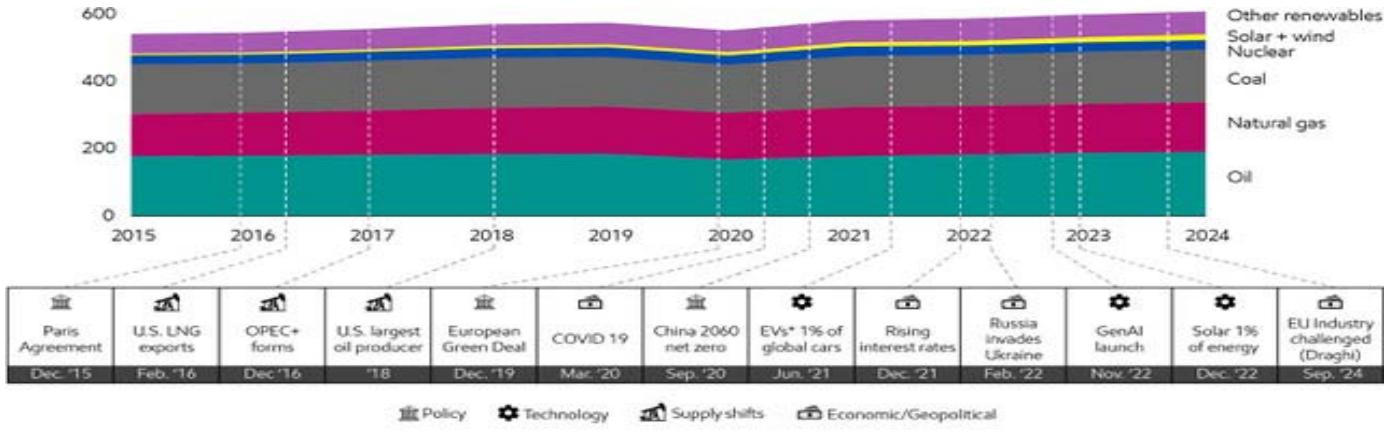

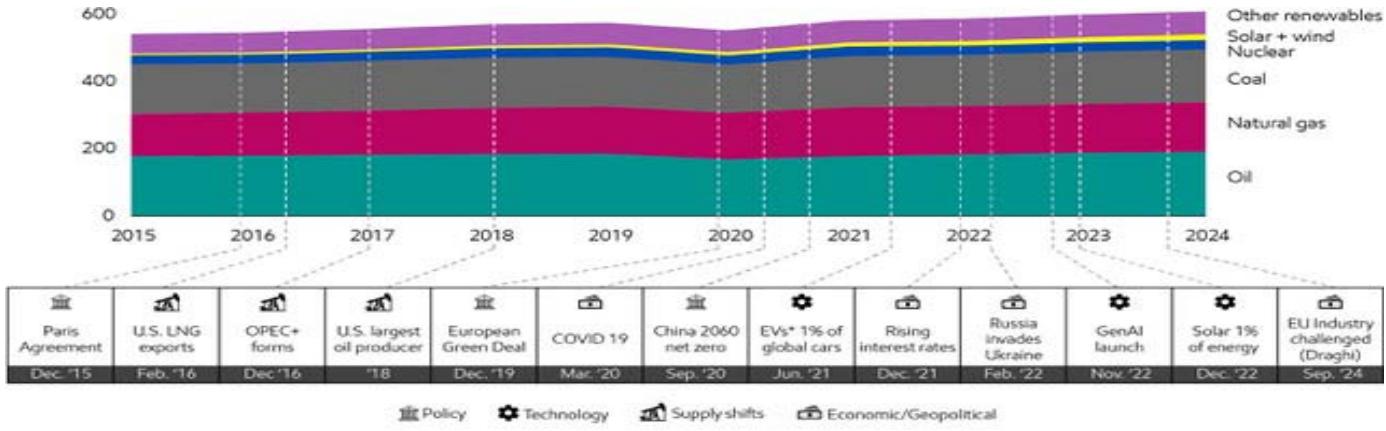

There is uncertainty inherent in any future projection, and it is essential to constantly learn and improve our insights and models – and adjust and plan accordingly. Think about it; over the last 10 years we've seen the signing of the Paris Agreement for climate action, a global pandemic, Russia's invasion of Ukraine significantly altered global gas flows, the reemergence of the U.S. as an oil exporter, and huge growth (yet limited in overall terms) in deployment of renewable energy.

These are just a few examples, and yet as can be seen in the graph below, there hasn't been a year where there haven't been some significant macro development affecting energy development. Yet, through all of this, rising prosperity and energy demand have remained inextricably linked, and the global energy mix has mainly remained essentially unchanged.

Global energy mix has remained largely constant in a dynamic world (2015-24) Sources: UNFCC, EIA, OPEC, EU Commission, EIA, US Federal Reserve, Grantham Institute \*EVs include Battery Electric and Plug-in hybrids – Quadrillion BTU.

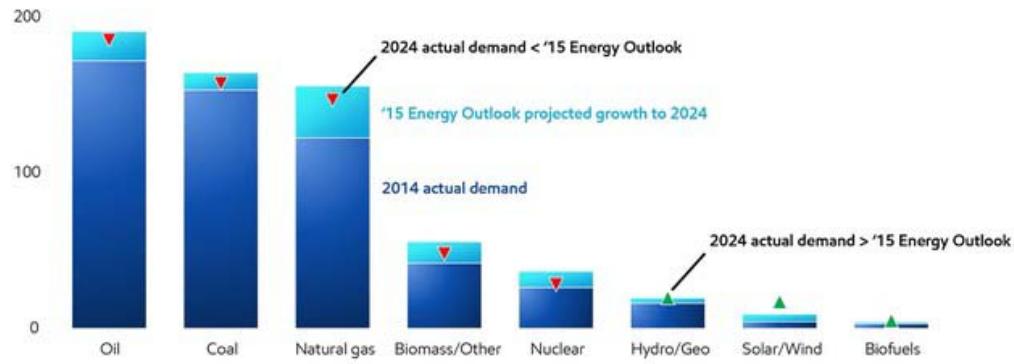

Looking back at outlooks prepared by important energy sector actors, like oil, gas or coal companies, or relevant research institutions, we can see that while projection weren't perfect, by and large they provided a sound basis for strategies and plans. Even so, these "look-backs" also highlighted the immense scale and

inertia of the energy system. Significant economic and geopolitical events had either near-term or localized impacts, but in the big scheme of events, only minor impact relative to the projections made ten years ago.

Energy trends over the past decade validate 2014 projections

Exxon Mobile (2015-2024 Energy Global Outlook)

Quadrillion BTU;

Low carbon includes Biomass, Biofuels, Nuclear, Hydro, Geothermal, Solar, and Wind.

Oil excludes biofuels.

Most striking of all is the marginal change in the energy mix over this decade, as traditional hydrocarbon sources (oil and coal) declined by just 1 percentage point each, while solar and wind grow by 2 percentage points, though from a very low basis to reach $3\%$ of total sources and natural gas 1 percentage point increased to reach close to a quarter of total (though contributing a lower emission footprint than traditional hydrocarbons):

Decarbonized energy sources increased marginally in energy mix in past decade

<table><tr><td rowspan="2"></td><td rowspan="2">2014 (actual)</td><td colspan="2">2024 share</td></tr><tr><td>'15 Energy Outlook projection</td><td>Actual</td></tr><tr><td>Oil</td><td>31%</td><td>30%</td><td>30%</td></tr><tr><td>Coal</td><td>27%</td><td>26%</td><td>26%</td></tr><tr><td>Natural gas</td><td>23%</td><td>24%</td><td>24%</td></tr><tr><td>Biomass/Other</td><td>9%</td><td>9%</td><td>8% ↓</td></tr><tr><td>Nuclear</td><td>5%</td><td>6%</td><td>5% ↓</td></tr><tr><td>Hydro/Geo</td><td>3%</td><td>3%</td><td>3%</td></tr><tr><td>Solar/Wind</td><td>1%</td><td>1%</td><td>3% ↑</td></tr><tr><td>Biofuels</td><td>1%</td><td>1%</td><td>1%</td></tr><tr><td>*Low carbon</td><td>19%</td><td>20%</td><td>20%</td></tr></table>

### Oil excludes biofuels

Digging deeper into this look-back analysis, there are several insights that inform our current Outlook and highlight some of the challenges society faces as it works to lower emissions while providing affordable, reliable energy that underpins economic growth. In 2024, for instance, global energy demand was $\sim 4\%$ lower than projected in the 2015 Outlook. Some of this difference is related to the pause in growth during the pandemic, but a bigger driver was slower economic development in Latin America and Sub-Saharan Africa. The 2015 Outlook had assumed rising prosperity in these regions, but income per capita was stagnant over the past ten years. These trends reinforce that rising prosperity and energy demand are inextricably linked.

Oil demand (excluding biofuels) was $2\%$ lower than projected, with the shortfall again due to slower economic development in emerging economies. Oil demand in high income OECD countries and China grew stronger than projected a decade ago, led by higher demand for transportation fuels.

Natural gas demand grew the most over the last decade, but 2024 demand was $6\%$ lower than 2015 Outlook projection. The developing world, excluding China, contributed, as did Europe, where the loss of pipeline gas and higher prices following Russia's invasion drove Europe's gas demand nearly $20\%$ below 2015 Outlook projections. Low-cost domestic gas resources in the United States and the Middle East drove stronger demand growth than the 2015 Outlook projection.

One can also see that solar and wind grew nearly twice as much as projected in the 2015 Outlook projections, with over half of the difference occurring in China. The combination of policy incentives and technology cost declines encouraged faster deployment. But even with the more rapid growth, solar and wind still only made up $\sim 3\%$ of the world's energy mix in 2024. This illustrates the massive scale of the global energy system.

Looking more broadly at low carbon sources, including nuclear and renewables, we see low carbon sources gained $1\%$ share over the past decade, aligned with the 2015 Outlook projection. The faster solar and wind growth was offset by a significant decline in nuclear energy, led by reactor shutdowns in Europe.

Given the uncertainty inherent in any projection, a range of sensitivities and scenarios – including those we view as remote – must be included to help inform strategic thinking. No future projection could exactly predict every new government policy, its effectiveness, or its unintended consequences. Similarly, the pace of technology advancements and extent of public support for more expensive, lower-emission solutions can influence how quickly or cost-effectively different energy pathways might develop.

All in all, the Global Outlook is made publicly available because it makes an important contribution to a variety of policy discussions – about energy, about economic development, and about the environment. By offering a clear-eyed, thoughtful view, the Outlook can enhance those discussions and – hopefully – lead to better decisions and policy outcomes.

## IV. KEY TAKEAWAYS WHEN RENEWABLES SOAR - JUST AS Fossil Fuels DO...

In a year when average air temperatures consistently breached the $1.5^{\circ}\mathrm{C}$ warming threshold, global $\mathrm{CO}_{2}$ -equivalent emissions from energy rose by $1\%$, marking yet another record, the fourth in as many years. Here are key factors explaining this overall outcome:

Wind and solar energy alone expanded by an impressive $16\%$ in 2024, nine times faster than total energy demand. China was responsible for $57\%$ of new additions, with solar almost doubling in just two years (from an admittedly low level). Yet this growth did not fully counterbalance rising demand elsewhere, with total fossil fuel use growing by just over $1\%$, highlighting a transition defined as much by disorder as by progress. In part, the results could be aligned with a better understanding of business conditions across countries to develop better energy investment responses to the different economic prospects among various jurisdictions.

- Crude oil demand in OECD countries remained flat, following a slight decline in the previous year. In contrast, non-OECD countries, where much of the world's energy demand growth is concentrated and fossil fuels continue to play a dominant role, saw oil demand rise by $1\%$. Notably, Chinese crude oil demand fell in 2024 by $1.2\%$, indicating that 2023 may have reached a peak. Elsewhere, global natural gas demand rebounded, rising by $2.5\%$ as gas markets rebalanced after the 2023 slump. India's demand for coal rose $4\%$ in 2024 and now equals that of the CIS, Southern and Central America, North America, and Europe combined.

- These trends underscore a stark truth: while renewable energy is scaling faster than ever, global demand is rising even faster. All-time records were reached across ALL forms of energy (coal, oil, gas, renewables, hydro and nuclear). Rather than replacing fossil fuels, renewables are adding (and till marginally) to the overall energy mix. This pattern, marked by simultaneous growth in clean and conventional energy illustrates the structural, economic, and geopolitical barriers to achieving a truly coordinated global energy transition.

- This year's data reflects a complex picture of the global energy transition. Electrification is accelerating, particularly across developing economies where access to modern energy is expanding rapidly. However, the pace of renewable deployment continues to be outstripped by overall demand growth, $60\%$ of which was met by fossil fuels. The result is a fourth consecutive year of record emissions, highlighting the structural challenges in aligning global energy consumption with climate goals.

- All primary energy sources, including nuclear and hydro, hit record consumption levels (for the first time since 2006), a reflection of surging global demand. No country has shaped this outcome more than China. Its rapid expansion of renewable capacity, alongside continued reliance on coal, gas, and oil, is driving global energy trends. The scale and direction of China's energy choices will be pivotal in determining whether the world can deliver a secure, affordable, and low-carbon energy future.

- Record-high GHG emissions and soaring temperatures in 2024 are a serious wake-up call. We have the strategies, technologies, and know-how to deliver the energy transition with potentially an integrated, secure, and people-centred approach. Now, we must move from action, at scale and at speed. With greater attention to investments in energy storage and transmission, there is potential to overcome the lower load factor and heavy weather- and location-reliance of renewables, thereby levelling their competitiveness with traditional sources of energy.

- Several countries have came forth with new climate plans and announcements at the UN High-Level Event on Climate Action. These lay out emissions targets through 2035, as waypoint on the path to net zero by mid-century. Yet, despite the commitments made many times in the past, even with the more ambitious goals compared to previous climate commitments, the targets announced to date, the trajectory and results fall far short of what's needed to stay within critical warming thresholds. By 2035, the world needs to cut 31.2 gigatons of emissions to stay on track for 1.5 degrees C, or 20.2 Gt for 2 degrees. By now, more than new goals, what is needed concrete strategies, action programs, proper economic and sector policies that provide the necessary conditions and incentive structures, so that productive sectors undertake the necessary investments to achieve this order of change and necessary resilience.

- Globally, we are still not at the pace required, as energy demand continues to rise. This year's data highlights how Europe has been facing a reality check, with rising effective interest rates and supply chain costs slowing progress on renewables, at the same time China and other emerging markets continue to drive growth at scale. What's emerging is not a uniform transition, but a need to address a highly diverse set of local conditions.

# V. WHERE DO WE GO FROM HERE

Rather than aiming to achieve artificial aggregate goals, and build more, costly and time-consuming oversight mechanisms, emphasis must shift towards practical strategies built for resilience, recognizing that energy security and affordability remain central concerns -- competing and in need to be reconciled with climate action.

In a world with greater volatilities and structural changes, policy-makers and business leaders must increasingly seek to navigate an uneven energy transition, one shaped by diverging regional trends, infrastructure constraints, policy fragmentation and institutional capabilities. Key questions to be henceforth considered in the investment process by business and policy leaders may have to include:

- What does it mean for a strategy when the energy mix is shifting, but not in the way many expected, with gas, oil and coal continuing to play significant roles?, and thus, how we can tilt incentives towards lower emitting hydrocarbons – i.e., towards gas and disincentivize coal?

- How does one respond when electricity demand surges, renewables can't keep up everywhere, and energy systems are already straining under the pressure?

- Are strategies focused where progress is happening –not just where it's expected?, and are we focusing on institutional and other constraints to open up investment opportunities, risk intermediation arrangements in other forms of energy not yet as widely in use, such as geothermal, green hydrogen, etc.?

- How does one prepare for a market where trade flows are shifting, policy signals are mixed, and volatility is here to stay?

- Can one's business thrive in a world where complexity, fragmentation, and disruption are now the norm? If so, how can we shift attention from processes, target-settings and other intermediary concerns to outcome, and results.

With world primary energy demand projected to increase by more than half over the next 25 years, we are facing the formidable twin challenges of finding secure and affordable supplies of energy while addressing the environmental impacts of that increased consumption. The geographic dislocation between the sources of energy supply and demand and the heightened geopolitical risk in some of the traditional energy-supplying regions is also encouraging consuming nations to cast their nets wider for alternative supplies of energy. The US, the world's largest consumer of energy, and China and India, the fastest-growing consumers, are all characterised by relatively low or declining oil and gas reserves. They all possess substantial reserves of coal... but coal is the most carbon-intensive of the fossil fuels.

The are important drawbacks with the current path and constraints, but there important efforts among companies leading the field in green-technology development. This is bound to take time, and the fact remains that most electricity is generated from fossil fuels and until it can be produced on a huge scale from economically feasible alternatives including renewable resources, the production, storage and transportation of hydrogen and other such sources on a commercial scale affect the climate no less than the refining of crude oil.

So, in the $21^{\text{st}}$ century, the world faces twin energy-related threats: that of not having adequate and secure supplies of energy at affordable prices and that of environmental harm caused by consuming too much energy in inappropriate ways.

A solution to either of these threats is relatively straight forward; however, a solution to both simultaneously is one of the great challenges of our times. With global energy demand expected to rise by $53\%$ over the next 30 years, and fossil fuels accounting for $83\%$ of the overall increase, simply calling for a cut in consumption is not a sufficient solution to the challenges we face.

Accordingly, in the short term, fossil fuels, including coal have an important role to play in enhancing energy security and fuelling both economic growth and poverty alleviation globally. Looking towards the medium term, however, greater efforts must shift towards: (i) technological development, including deployment of enhanced information technology for more rational use of scarce energy sources; and (ii) trimming energy demand though proper pricing (and taxation) of carbon emissions, to reflect the cost of environmental externalities in energy sources, thereby dampening energy demand to help reduce above-mentioned gap in the energy scenery. There are some 50 countries that have such initiatives in different (though mostly early) stages of development.

In the end, a more determined effort is needed to change the incentive structure and move such initiatives into implementation. This will be indispensable to narrow the gap to embed these costs into consumer behavior, and eventually meeting the global emission and climate change objectives.

Generating HTML Viewer...

References

5 Cites in Article

Roland Kupers,Gernot Wagner (2025). Getting to Greener Steel" and "Early Investment in Decarbonization Can Help Save Trillions in Climate Costs.

Irwin Rosenfarb (2024). PAF y terapias psicodinámicas.

M Schloss (2023). Unknown Title.

M Schloss (2024). World Production Gas, Natural Gas Liquids, Coal and Lignite, Electricity, Primary Energy.

Explore published articles in an immersive Augmented Reality environment. Our platform converts research papers into interactive 3D books, allowing readers to view and interact with content using AR and VR compatible devices.

Your published article is automatically converted into a realistic 3D book. Flip through pages and read research papers in a more engaging and interactive format.

Our website is actively being updated, and changes may occur frequently. Please clear your browser cache if needed. For feedback or error reporting, please email [email protected]

Thank you for connecting with us. We will respond to you shortly.