Small and medium-scale enterprises (SMEs) are important players in Ghana’s economic growth but are often prone to financial volatility due to ineffective financial management systems. The study investigates the influence of budgeting control practices on financial performance of SMEs, guided by agency and goal-setting theories. Drawing on a crosssectional survey of 200 SMEs, four dimensions of budgetary control formal budgets, review frequency, participative budgeting, and variance analysis were examined. Findings show that formal budgets, regular review, and participative budgeting significantly influence financial performance, while variance analysis doesn’t significantly influence financial performance. Managerial capacity and firm size mediate the relationships. The research concludes that effective budgetary control increases profitability and sustainability and recommends capacity building and flexible budgeting models to improve SME financial management in Ghana.

## I. INTRODUCTION

S MEs are globally recognized to be the backbone of developing economies, contributing to innovation, job creation, and income generation. In Ghana, they represent over $85\%$ of businesses, contribute around $70\%$ to GDP, and employ most of the workforce (Abor & Quartey, 2010; Ackah & Vuvor, 2021). Despite this contribution, the majority of them have poor financial management, poor managerial skills, and lack of internal controls (Boakye, 2022; Nyarko & Oppong, 2023), thereby recording high failure rates.

Budgetary control periodic preparation, implementation, and updating of budgets enhances planning, responsibility, and performance (Drury, 2018). It provides a vital tool for survival and growth for resource-constrained SMEs (Kpodo & Agyapong, 2020; Danso & Mensah, 2022). While previous studies in Ghana (Amoako, 2013; Susuawu, 2020) revealed that budgeting raises performance, they do not consider it as one construct, ignoring some aspects such as participation, review frequency, and variance analysis.

At the international level, prior studies suggest that participative budgeting enhances commitment and goal congruence (Shields & Shields, 1998; Hansen &

Van der Stede, 2004), while frequent review and variance analysis improves responsiveness in uncertain environments (Otley, 1999; Ahmad, 2019). However, these practices have not been properly explored in Ghana's SMEs whose management capacity and structural informality differ from their larger counterparts. This study therefore investigates how various aspects of budgetary control influence SME performance in Ghana and identifies contextual factors firm size, managerial competence, and sector that influence their effectiveness.

### a) Problem Statement

Despite their central role in the Ghanaian economy, SMEs suffer from long-term financial instability and short life spans linked with poor financial control and ineffective management control systems (Amoako, 2013; Boakye, 2022). Though budgeting has been recognized as a key performance driver (Drury, 2018), there is little empirical Ghanaian research. Existing studies (e.g., Susuawu, 2020) confirm the positive association between budgeting and performance but do not investigate its composing dimensions. Consequently, there is no knowledge concerning which of the four budgeting practices formal budgets, reviews, participation, or variance analysis are most effective in influencing profitability, liquidity, and sustainability. Closing this gap is critical in building managerial ability and crafting targeted policies that boost SME financial resilience.

### b) Research Objectives

The study aims to examine the effect of budgetary control on the financial performance of SMEs in Ghana. Specifically, it aims at:

### c) Research Questions

1. Determine the effect of formal budgets on financial performance.

2. Determine if review frequency affects performance budget.

3. Explore the effect of participative budgeting on SME financial outcomes.

4. Describe the role of variance analysis in improving performance.

5. Discuss how firm size, managerial capacity, and industry moderate these impacts.

6. What is the impact of formal budgeting on SME financial performance?

2. How is the frequency of budget reviews related to performance?

3. What is the effect of participative budgeting on SME financial outcomes?

4. How does variance analysis impact levels of performance?

5. Do firm size, managerial capacity, and industry moderate these effects?

### d) Significance of the Study

This study is both theoretically and practically contributory. It advances empirical knowledge in the disaggregated aspects of budgetary control and how they affect SME performance in developing economies. It informs SME managers about profit maximization and financial prudence through budgeting practices. Policymakers and support institutions can apply the findings in the design of capacity-development programs and financial literacy programs that promote SME sustainability. The research ultimately warrants Ghana's economic development agenda by addressing managerial deficiencies that hamper SME growth, competitiveness, and survivability.

### e) Paper Structure

The paper has a literature review and theoretical frameworks in Section Two, explanation of methodology in Section Three, results presentation and analysis in Section Four, and findings discussion, conclusions, and recommendations in Section Five.

## II. LITERATURE REVIEW AND THEORETICAL FRAMEWORK

### a) Conceptualizing Budgetary Control

Budgetary control is a routine process by which organizations set budgets, measure actual performance against targets, and take remedial steps to come back on track in terms of strategic goals (Drury, 2018). It functions as a resource planning tool for allocation and an efficiency monitoring and decision-making mechanism for control (Otley, 1999).

Key Factors Influencing Performance are:

1. Formal Budgets: Documenting a budget imparts discipline, reduces uncertainty, and focuses expenditure (Ahmad, 2019).

2. Review Frequency: Regular reviews allow early deviation detection and promote adaptability in changing environments (Van der Stede, 2001).

3. Participative Budgeting: Involving employees in budget creation enhances ownership, motivation, and goal congruence (Shields & Shields, 1998).

4. Variance Analysis: Actual vs. planned performance comparison detects inefficiencies and directs appropriate corrective actions on time (Hope & Fraser, 2003).

5. Budget Flexibility: Flexibility supports responsiveness to environmental change, builds resilience,

and reduces exposure to risk (Libby & Lindsay, 2010).

For finance and competition-constrained Ghanaian SMEs, these factors combined underpin financial prudence, adaptability, and sustainable performance.

### b) Empirical Evidence: African and Global Perspectives

#### 1. Ghana

There is evidence that budgetary control is positively related to the performance of SMEs. Susuawu (2020) found that budget practices explained $42.7\%$ of performance variance, and Amoako (2013) reported that firms using formal accounting and budgeting systems were more profitable and stable. Nevertheless, few studies have focused on what specific elements of budgets contribute the most to performance.

#### 2. East Africa

Results are homogeneous across the region. Kemunto (2022) indicated that participatory budgeting and reporting of variances improved finance performance in Kenyan microfinance institutions, and Nyakundi & Nyamita (2019) indicated corresponding effects for SACCOs.

#### 3. Fragile States (Somalia)

Despite weak institutions, Ali, Hassan, and Kadir (2023) found that formal monitoring and planning significantly improved SME stability and performance.

#### 4. Global Context

Global evidence confirms such patterns. Uwuigbe et al. (2019) noted higher accountability and financial performance in Nigerian SMEs that employed participatory budgeting. Hansen & Van der Stede (2004) reported enhanced performance where firms examined budgets on a regular basis, and Zhou et al. (2022) reported diminished budgetary slack where formal arrangements existed for planning and evaluation.

Generally, evidence exists that suggests budgetary control improves performance but varies based on firm size, management skill, and environmental uncertainty.

### c) Theoretical Perspectives

Budgetary control and financial performance can be linked to one another through some complementary theories:

1. Agency Theory (Jensen & Meckling, 1976; Eisenhardt, 1989): Mechanisms of budgeting such as formal written documentation, reporting of variances, and frequent examination minimize information asymmetry, connect managers' behavior to owners' interests, and enhance accountability.

2. Resource-Based View (Barney, 1991; Peteraf, 1993): Budgeting is an important, scarce, and imitable internal resource that enhances efficiency and

competitiveness, particularly for cash-hungry SMEs (Amoako, 2013).

3. Contingency Theory (Otley, 1980; Chenhall, 2003): Budgeting impact varies with context factors such as firm size, environment, and technology. There is no optimal way; effectiveness is context-dependent.

4. Goal-Setting Theory (Locke & Latham, 1990): Budgets introduce clear, challenging targets that improve performance, especially where workers participate in their development, thereby improving goal commitment and reducing slack.

These theories explain how budgetary control operates as both a monitoring tool (Agency Theory) and an internal resource (RBV), and how its effects depend on circumstances (Contingency Theory) and motivation (Goal-Setting Theory).

### d) Hypotheses Development

Based on the literature and theory, the study hypothesizes:

- H1: Formal budgets are positively related to the financial performance of SMEs.

- H2: Budget review on a regular basis is positively related to financial performance.

- H3: Greater management and employee participation in budgeting enhances financial performance.

- H4: Enhanced variance analysis is positively related to financial performance.

- H5: The above relationships are mediated by firm size, managerial ability, and industry type.

### e) Conceptual Framework

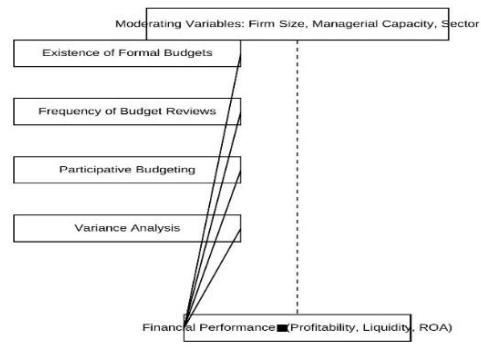

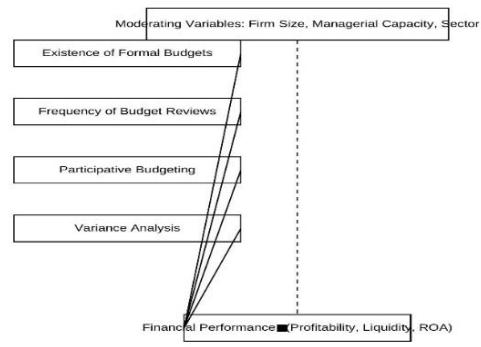

The proposed conceptual model illustrates that budgeting control practices- review frequency, formal budgeting, participative budgeting, and variance analysis- are expected to have positive relationships with SME financial performance. These are subject to contextual factors such as firm size, managerial ability, and industry features, which affect the extent to which budgeting practices are translated into performance results.

Conceptual Framework: Budgetary Control and Financial Performance Figure 1

The diagram illustrates the relationship between important budgetary control practices formal budgets, review period, participative budgeting, and variance analysis, and their supposed positive relationship with SME financial performance. Firm size, managerial ability, and nature of the business sector influencing the effectiveness of budgetary practices with different contexts moderate these relationships between these practices and financial performance.

## III. RESEARCH METHODOLOGY

### a) Research Design

The study employed a quantitative cross-sectional design using structured questionnaires to explore the relationships between key budgetary control practices- formal budgets, review frequency, participative budgeting, and variance analysis- and financial performance measures (profitability, ROA, and liquidity). The design captures associations at a point in time and thus suitable for testing relationships without suggesting causality. Financial figures were validated against firm records and endogeneity tests were performed to enhance reliability.

### b) Population, Sample, and Data Collection

#### 1. Population

Targeted population were Ghana's registered SMEs, according to the Ghana Statistical Service and NBSSI, as companies with 6-99 workers in manufacturing, services, trade, and agro-processing.

#### 2. Sampling

A Multi-Stage Sampling Strategy was used:

1. Stratified sampling by region (southern, central, northern Ghana).

2. Random selection of firms from databases such as the Registrar General's Department and AGI.

Sample Size: At least 384 SMEs were required through Cochran's (1977) formula (5% margin of error, 95% confidence level). For non-response reasons, 450 firms were contacted. Owner-managers or senior financial officers were interviewed.

Data Collection: Data were gathered using internet and personal interviews, with assistance from enumerators for low financial literacy respondents. Ethical approval and informed consent were obtained, and non-response bias was checked by comparing early and late respondents (n = 30 each).

### c) Variables and Measurement

Dependent Variable - Financial Performance:

Measured using both objective and perceptual measures:

- RXA = Net profit/Total assets

- NPM = Net income/Sales

- Current assets/Current liabilities = Liquidity Ratio

Econometric Model and Estimation Strategy

Model Specification:

Perceived performance (5-point Likert scale).

If required, factor analysis was used to determine a composite index.

Independent Variables - Budgetary Control Dimensions:

1. Formal Budget: 0 = None, 1 = Informal, 2 = Formal documented.

2. Review Frequency: 1 = Annual to 5 = Weekly.

3. Participative Budgeting: Shields & Shields (1998) Likert-scale items.

4. Variance Analysis: Frequency and corrective action rated on Likert scales.

5. Control Variables: Firm size, managerial ability (education, training, experience), industry, age of firm.

$$

[ F P _ {i} = \backslash b e t a _ {0} + \backslash b e t a _ {1} F B _ {i} + \backslash b e t a _ {2} R F _ {i} + \backslash b e t a _ {3} P B _ {i} + \backslash b e t a _ {4} V A _ {i} + \backslash b e t a _ {5} C V _ {i} + \backslash v a r e p s i l o n _ {i} ]

$$

Interaction terms (e.g., FB × firm size, PB × managerial capability) included to test for moderating effects.

Endogeneity Considerations: Reverse causation addressed using.

1. Lagged performance where applicable.

2. Instrumental variables (IVs) such as managerial training and firm age.

3. Robust heteroscedasticity standard errors.

4. IVs and lagged data constraints were identified.

### d) Reliability and Validity

- Construct Validity: Based on established scales (Shields & Shields, 1998; Drury, 2018), enhanced through pilot testing of 20 SMEs.

- Reliability: Cronbach's alpha ≥ 0.70 confirmed internal consistency.

- Content Validity: SME and accounting scholars vetted.

- External Validity: Guaranteed through sectoral and regional coverage.

- Statistical Validity: Established using VIF (<10), and normality and homoscedasticity tests also confirmed model assumptions.

## IV. RESULTS AND DISCUSSION

### a) Introduction

### b) Firm Characteristics

The study presents a growing and formalizing SME sector in Ghana. Most firms (65%) were founded from 2010 to 2020, suggesting recent expansion. Services (34%) and manufacturing (28%) industries are dominant, and trade (25%) and agro-processing (10%) less frequent. About 42% of firms are small, and 40% medium-sized, providing more evidence of formalization than against national standards. Ownership is mostly sole proprietorships (46%), of which 34% are registered as limited liability companies. Finally, 55% of the respondents were owner-managers, pointing out their central role in financial decision-making. In total, Ghana's SME environment is increasing, becoming more organized, and better managed by managerial ability and formal organization.

<table><tr><td>Budgetary Control Practices Practice</td><td>Categories</td><td>% of Firms</td></tr><tr><td>Existence of Budgets</td><td>Formal written</td><td>54</td></tr><tr><td></td><td>Informal/unwritten</td><td>22</td></tr><tr><td></td><td>None</td><td>10</td></tr><tr><td>Review Frequency</td><td>Monthly</td><td>28</td></tr><tr><td></td><td>Quarterly</td><td>25</td></tr><tr><td></td><td>Semi-annual</td><td>18</td></tr><tr><td></td><td>Annual</td><td>12</td></tr><tr><td></td><td>Only when deviations occur</td><td>10</td></tr><tr><td>Variance Analysis</td><td>Monthly</td><td>30</td></tr><tr><td></td><td>Quarterly</td><td>25</td></tr><tr><td></td><td>Annually</td><td>18</td></tr><tr><td></td><td>Never</td><td>12</td></tr></table>

Figure 2

### c) Budgetary Controls Practices

Participatory budgeting in SMEs was moderately high with communication (3.9) and forecast accuracy (4.0) being high. Formal written budgets are used in around $54\%$, informal in $22\%$, and none in $10\%$, which indicates resource and capacity limitations. Budget reviews are conducted monthly ( $28\%$ ), quarterly ( $25\%$ ), or less frequently in smaller enterprises, mirroring

### d) Indicator Financial Performance

low monitoring. More formal reviews are followed by manufacturing and large services enterprises, compared to trade and agro-processing SMEs. Whereas variance analysis is common, $12\%$ disregard it and experience gaps in performance. Budgeting typically reflects average participation and communication, reflecting openness but variable involvement on the part of firms.

Table 4.3: Objective Performance Indicators

<table><tr><td>Indicator</td><td>Range</td><td>% of Firms</td></tr><tr><td>Net Profit Margin (NPM)</td><td>Loss</td><td>10</td></tr><tr><td></td><td>1–5%</td><td>18</td></tr><tr><td></td><td>6–10%</td><td>28</td></tr><tr><td></td><td>11–20%</td><td>26</td></tr><tr><td></td><td>>20%</td><td>18</td></tr><tr><td>Return on Assets (ROA)</td><td>Negative</td><td>12</td></tr><tr><td></td><td>1–5%</td><td>20</td></tr><tr><td></td><td>6–10%</td><td>27</td></tr><tr><td></td><td>11–20%</td><td>24</td></tr><tr><td></td><td>>20%</td><td>17</td></tr><tr><td></td><td></td><td></td></tr><tr><td>Current Ratio</td><td><1.0</td><td>18</td></tr><tr><td></td><td>1.0–1.5</td><td>32</td></tr><tr><td></td><td>1.6–2.0</td><td>25</td></tr><tr><td></td><td>>2.0</td><td>25</td></tr></table>

Table 4.4: Perceptual Performance Indicators (Means, 1-5 Scale)

<table><tr><td>Indicator</td><td>Mean</td></tr><tr><td>Profitability</td><td>3.4</td></tr><tr><td>Liquidity</td><td>3.3</td></tr><tr><td>Overall Sustainability</td><td>3.5</td></tr></table>

### e) Objective Financial Performance Indicators

SMEs' financial performance varied. About $28\%$ had 6-10% profit margins, 26% had 11-20%, and 18% had over $20\%$, while $10\%$ made losses. ROA followed the same patterns whereby $27\%$ had $6 - 10\%$, $24\%$ had $11 - 20\%$, and $17\%$ had over $20\%$, though $12\%$ were negative. The liquidity ratios showed that $32\%$ of the firms were quite liquid, yet $18\%$ were at risk of solvency. Compared to national standards (GSS, 2022), most firms performed at or above industry levels. Perceptual profitability (3.4), liquidity (3.3), and sustainability ratings (3.5) indicate overall positive but cautious managerial judgments.

### f) Moderating Variables

With regard to moderating attributes, $66\%$ hold degrees but $35\%$ never receive finance training and only

### g) Regression Analysis

$15\%$ are professionally qualified. Management background is relatively strong, with $64\%$ holding five or more years of management experience. Approximately $28\%$ of firms are in very uncertain industries, suggesting that education, training, and industry uncertainty are thus likely to influence the effect of budgeting practices on performance in subsequent regression models.

Table 4.6: OLS Regressions on Net Profit Margin (Dependent Variable: NPM,%)

<table><tr><td>Variable</td><td>Model 1 (Baseline)</td><td>Model 2 (+ Controls)</td></tr><tr><td>Formal Budget (1 = yes)</td><td>3.5*** (1.2)</td><td>3.2** (1.3)</td></tr><tr><td>Budget Review Monthly</td><td>2.1** (0.9)</td><td>1.9** (0.8)</td></tr><tr><td>Participative Score</td><td>1.5*** (0.5)</td><td>1.4*** (0.5)</td></tr><tr><td>Log Turnover</td><td>-</td><td>0.8** (0.3)</td></tr><tr><td>Firm Size: Micro</td><td>-</td><td>-1.5 (1.0)</td></tr><tr><td>Firm Size: Medium</td><td>-</td><td>0.9 (1.1)</td></tr><tr><td>Firm Size: Large</td><td>-</td><td>2.2* (1.2)</td></tr><tr><td>Manager Education (Bachelor+)</td><td>-</td><td>1.9** (0.8)</td></tr><tr><td>Account Training: Short Course</td><td>-</td><td>1.2* (0.7)</td></tr><tr><td>Sector Uncertainty</td><td>-</td><td>-1.5** (0.6)</td></tr><tr><td>Formal Budget × Sector Uncertainty</td><td>-</td><td>-</td></tr><tr><td>Participative × Manager Capacity</td><td>-</td><td>-</td></tr><tr><td>Observations</td><td>384</td><td>384</td></tr><tr><td>R-squared</td><td>0.12</td><td>0.25</td></tr></table>

### h) Regression Results

Regression results show that formal budgeting is associated with a 3.5 percentage point increase in net profit margins, with monthly reviews adding around 2 points and participative budgeting 1.2-1.5 points, especially under competent management. Both firms that are larger and those that have greater turnover perform better, and education or training of managers contributes 1-2 points to profitability. However, industry volatility diminishes margins by around 1.5 points, limiting budgeting effectiveness. Interaction effects show that budgeting performs optimally in stable industries with competent managers. The model's explanatory power rose from $R^2 = 0.12$ to 0.31, confirming that contextual variables have a significant impact on budget-performance relationships.

### i) Qualitative Insights

Qualitative responses validated the quantitative findings. Inadequate accounting capacity, macroeconomic instability, and low staff motivation were cited by managers as major challenges to effective budgeting. Recommended solutions included training programs in accounting, affordable budgeting software, and policy-induced capacity building with emphasis on institutional and structural support for sustained budgeting practice.

### j) Discussion of Findings

The results show that formal, frequent, participative, and flexible budgeting are positively associated with SME financial performance but with varying effectiveness in different contexts. Formal budgets and high-frequency reviews encourage discipline and responsiveness, while participative budgeting results in better performance when there is capable management. Variance analysis supports strategic decision-making, and firm size, managerial ability, and sector volatility influence outcomes. SMEs that function in turbulent contexts need agile budgeting systems, supported by capacity building, sectoral arrangements, and digital tools to improve competitiveness and sustainability.

## V. SUMMARY, CONCLUSIONS, AND RECOMMENDATIONS

### a) Introduction

This chapter summarizes the major findings, presents key conclusions, and provides recommendations for SME managers, policymakers, and researchers. It concludes with reflections on the role of budgetary control in enhancing SME performance and sustainable growth in Ghana.

### b) Summary of the Study

The study investigated the effect of budgetary control on SME financial performance in Ghana, namely on four aspects formal budgets, frequency of review, participative budgeting, and variance analysis and firm size, managerial capability, and industry as intervening effects.

Quantitative cross-sectional survey of 384 SMEs in manufacturing, services, trade, and agro-processing industries was conducted, supported by qualitative inputs.

#### Key Findings:

- Firm Profile: Most of the SMEs were established between 2010-2020 and were sole proprietorship firms.

- Budgeting Practices: $54\%$ used formal budgets, with the remainder using informal or no systems. Frequent reviews (monthly/quarterly) were associated with improved performance. Participative budgeting was moderate, and variance analysis poorly utilized.

- Financial Performance: Firms overall recorded moderate to high profitability, decent liquidity, and stable ROA, albeit some firms threatened by insolvency.

- Moderating Factors: Education of managers and financial training improved results, with environmental instability detracting from them.

- Regression Analysis: Formal budgeting, frequent review, and participative budgeting significantly

enhanced profitability and ROA. Managerial training and company size enhanced these effects.

- Qualitative Insights: Barriers were limited financial literacy, poor record-keeping, and economic uncertainty. Intended solutions were training, computer-based budgeting, and more active participative involvement.

### c) Conclusions

The study proves that budgetary control matters to improve SME financial performance in Ghana. Formal budgets and regular reviews enhance profitability, responsiveness, and fiscal control, whereas participative budgeting fosters ownership and goal congruence. Though variance analysis is not extensively used, it remains vital for corrective action. Effective budgeting depends on managerial competence and the ability to react to unstable environments. However, sloppy records and external shocks chisel away at success. Budgeting in general is a strategic management tool requiring skilled leadership and flexibility.

### d) Recommendations

For SME Managers

1. Institutionalize formal written budgets to enhance planning and coordination.

2. Monthly or quarterly review of the budget for timely correction.

3. Institute variance analysis and corrective action on a regular basis.

4. Foster participative budgeting to enhance motivation and responsibility.

5. Provide financial training and install computerized accounting systems for efficiency.

Highest priority must be given to formalization and frequency of review, which offer the greatest performance improvement.

#### For Policymakers and Support Institutions

1. Promote financial literacy programs to strengthen managerial capability.

2. Enhance SME access to finance for training and digital software.

3. Develop sector-specific adaptive budgeting models.

4. Enable digital transformation through tax relief and software subsidies.

Capacity building and financing are the essence of SME resilience and control efficiency.

#### For Future Research

1. Conduct longitudinal studies to assess causal relationships among budgeting and performance.

2. Examine sector-specific analyses to adopt contextual differences.

3. Conduct cross-country comparisons to identify regional tendencies.

4. Use mixed-method approaches to gain in-depth behavioral insights.

### e) Final Conclusion

Effective budgeting and control systems are principal drivers of the performance of SMEs in Ghana. Their success depends on managerial capability, institutionalist, and responsiveness to change. Enhancing financial literacy, digital technology adoption, and the ease of attractive policy environments will enhance SME competitiveness and resilience.

If SMEs apply budgeting as an adaptive and participatory management practice, they will be well placed to address uncertainty, enhance profitability, and make sustainable contributions to Ghana's economic development.

[^384]: out of 450 valid responses from the surveyed SMEs in Ghana (85.3% response rate) were used in this study. Results comprise firm characteristics, budgeting practices, financial performance, moderating variables, and regression findings. Based on both qualitative and quantitative data, the analysis provides a general picture of the impact of budget control on SME performance in Ghana. _(p.4)_

Generating HTML Viewer...

References

27 Cites in Article

J Abor,P &quartey (2010). Issues in SME development in Ghana and South Africa.

J Ackah,S Vuvor (2021). Digitalization and its Impact on Small and Medium-sized Enterprises (SMEs): An Exploratory Study of Challenges and Proposed Solutions.

N Ahmad (2019). Budgetary control, managerial performance and moderating effect of budget adequacy and budget feedback: Evidence from Malaysian local authorities.

H Ali,A Hassan,M Kadir (2023). The effect of planning and budget monitoring on SME performance in fragile economies: Evidence from Somalia.

G Amoako (2013). Accounting practices of SMEs: A case study of Kumasi Metropolis in Ghana.

J Barney (1991). Firm resources and sustained competitive advantage.

J Boakye (2022). Financial management practices and performance of small and medium enterprises in Ghana.

R Chenhall (2003). Management control systems design within its organizational context: Findings from contingency-based research and directions for the future.

W Cochran (1977). Sampling techniques.

A Danso,A Mensah (2022). Effect of Financial Literacy on Financial Performance of Small and Medium-Sized Enterprises in Kigali City, a case of Small and Medium-Sized Enterprises in Nyarugenge District.

Colin Drury (2018). Management and Cost Accounting.

Kathleen Eisenhardt (1989). Agency Theory: An Assessment and Review.

(2022). Ghana business register report: Performance of SMEs 2021-2022.

S Hansen,W Van Der Stede (2004). Multiple facets of budgeting: An exploratory analysis.

J Hope,R Fraser (2003). Beyond budgeting: how managers can break free from the annual performance trap.

M Jensen,W Meckling (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure.

Debrah Kemunto,John Cheluget (2022). Budgetary Controls and Financial Performance of Micro Finance Institutions (MFIs) in Kenya.

B Kpodo,A Agyapong (2020). Budgetary practices and SME growth in Ghana.

T Libby,R Lindsay (2010). Beyond budgeting or budgeting reconsidered? A survey of North-American budgeting practice.

No ethics committee approval was required for this article type.

Data Availability

Not applicable for this article.

How to Cite This Article

Lordwin Paa Kwesi Archer. 2026. \u201cThe Impact of Budgetary Control on Financial Performance: Evidence from SMEs in Ghana\u201d. Global Journal of Management and Business Research - A: Administration & Management GJMBR A Volume 25 (GJMBR Volume 25 Issue A6): .

Explore published articles in an immersive Augmented Reality environment. Our platform converts research papers into interactive 3D books, allowing readers to view and interact with content using AR and VR compatible devices.

Your published article is automatically converted into a realistic 3D book. Flip through pages and read research papers in a more engaging and interactive format.

Small and medium-scale enterprises (SMEs) are important players in Ghana’s economic growth but are often prone to financial volatility due to ineffective financial management systems. The study investigates the influence of budgeting control practices on financial performance of SMEs, guided by agency and goal-setting theories. Drawing on a crosssectional survey of 200 SMEs, four dimensions of budgetary control formal budgets, review frequency, participative budgeting, and variance analysis were examined. Findings show that formal budgets, regular review, and participative budgeting significantly influence financial performance, while variance analysis doesn’t significantly influence financial performance. Managerial capacity and firm size mediate the relationships. The research concludes that effective budgetary control increases profitability and sustainability and recommends capacity building and flexible budgeting models to improve SME financial management in Ghana.

Our website is actively being updated, and changes may occur frequently. Please clear your browser cache if needed. For feedback or error reporting, please email [email protected]

Thank you for connecting with us. We will respond to you shortly.