Annotation-In a crisis, different economic systems react differently to the emergence of imbalances. If the state regulation of economic processes is minimized in the market economic system, then in the command and administrative system the state has many tools for regulating the economy. The purpose of the study is to empirically demonstrate the co-directional and opposite dynamics of the development of modern economic systems in order to assess the conjuncture of socio-economic development in the conditions of the COVID pandemic. In the course of the study, it was revealed that the market economic system and the command and administrative system have both co-directional and multi-vector dynamics of economic development, which is reflected in the dynamics of the values of economic indicators. The study of empirical data showed that the co-directional vector of development has GDP, GDP per capita, gross savings, consumer spending, the share of income of 20% of the poorest population. A multidirectional vector of development of the economic systems of Russia and China is observed for such indicators as the level of inflation, imports of goods and services, external debt, and unemployment. It is worth noting that the indicators of co-directional dynamics are effective. GDP, GDP per capita, gross savings are the result of economic activity.

Annotation- In a crisis, different economic systems react differently to the emergence of imbalances. If the state regulation of economic processes is minimized in the market economic system, then in the command and administrative system the state has many tools for regulating the economy. The purpose of the study is to empirically demonstrate the co-directional and opposite dynamics of the development of modern economic systems in order to assess the conjuncture of socio-economic development in the conditions of the COVID pandemic. In the course of the study, it was revealed that the market economic system and the command and administrative system have both co-directional and multi-vector dynamics of economic development, which is reflected in the dynamics of the values of economic indicators. The study of empirical data showed that the co-directional vector of development has GDP, GDP per capita, gross savings, consumer spending, the share of income of $20\%$ of the poorest population. A multidirectional vector of development of the economic systems of Russia and China is observed for such indicators as the level of inflation, imports of goods and services, external debt, and unemployment. It is worth noting that the indicators of co-directional dynamics are effective. GDP, GDP per capita, gross savings are the result of economic activity. At the same time, indicators of multidirectional dynamics are factors of the internal economic environment and the object of regulation by state bodies. The results of the study show that the command and administrative system is more stable in times of crisis, characterized by greater stability of inflation, reduced dependence on imports and increased equity of income distribution. It is on these indicators of socio-economic development that the state has an influence. A system with a market economy is more susceptible to the volatility of inflation, but it is characterized by a decrease in unemployment, as the market reacts to an increase in inflation.

## I. INTRODUCTION

In modern different economic systems, the state role in regulating economic processes is significantly different. In market economies the state role is to ensure common rules for all economic actors and to protect competition. In countries with a command and administrative economy, the state acts as the main regulator of all economic processes. But in crisis times in both types of economic systems, the state main task is to minimize the negative socio-economic consequences for the national economy.

The economic crisis provoked by the COVID-19 pandemic is unprecedented in the consequences scale. In such conditions, state governments must ensure the development and implementation of socio-economic programs to support business and population. Countries with different types and mechanisms of economic systems will respond differently and at different speeds to emerging challenges. In addition, in the pandemic crisis context when imbalances in the economic system development are manifested and the need arises to correct their elimination [10, 12], one of the fundamental economic issues is actualized - which economic system model is more successful: market or command and administrative?

The market economic system is based on principles such as granting private property rights, free market economy and competition without state intervention or with minimal state intervention. Such a system has the great advantage that each economic entity is free in its activities and is limited only by the scope of the law. In such economic system, economic laws function quite well, and therefore such a system state can be predicted, and government intervention in the economy is limited. However the market economy main problem is income distribution inequality and external environment risks of the companies functioning.

The command and administrative economic system is an alternative to the market economic system. In the command and administrative system the state has unlimited influence on the economy, and economic laws may not operate in such a system in connection with directive regulation. Most commonly the state has tools and opportunities to influence the market, and competition in such a system does not play a decisive role in markets design shaping. Meanwhile, in crises times it is in the command and administrative economy that state intervention in economic processes can be maximized to correct market failures.

Due to the fact that these economic systems function differently, the question arises of how this affects their socio-economic development indicators. Is such a situation possible when one economic system development makes it more resistant to crises? This issue is more relevant than ever in the existing challenges of the COVID-19 pandemic, when countries of the world are faced with the problem of their national economies unpreposition before problems of this scale.

## II. LITERATURE REVIEW

This study section is devoted to the results search of comparing different economic systems and determining the approach to comparing them. The main task at this stage of our research is to find criteria for comparing market and command and administrative economic systems and determine by what indicators of socio-economic development they differ. The ECLAC report [11] affirms that the pandemic has affected the economies of South America and the Caribbean through the effects of external and internal factors. External factors are represented by global economic activity falling, especially in the United States, China and Europe, adversely affected trade volumes and prices in Latin America and the Caribbean, especially commodities. At the same time, this report does not consider the issue that the economic system of the United States and China are significantly different. The economic systems of Latin America countries are also different. Some key manufacturing sectors in the region's countries form part of the global value chains in which the United States and China play key roles, the report found. Furthermore Mexico and Central America are subject to a downturn in the United States economy due to a reduction in remittances from migrants; in Mexico's case this is compounded by falling oil prices. Internal factors are mainly provoked by external factors and the economies accumulated problems of the region countries. At the same time, the report does not consider the reasons for the dependence of Latin American countries on the United States, although this is one of the main countries economic systems characteristics in this region.

Other impact studies of the COVID-19 pandemic [26, 20] on the global economy consider its impact in the context of the economic and social effect on different countries. This does not take into account the differences between countries in their socioeconomic systems. The report provides statistical information on the change in the economic parameters of different countries' economies, while the differences in management systems in these countries are not considered, which does not allow to determine the differences between economic systems of different countries on the indicators of their socio-economic development.

A study of the pandemic global economic effect [18] examines countries in Europe, the United States, China and Japan. But when comparing the pandemic impact the factor of different economic systems of these countries is not considered. Since economic systems are organized and function differently, the pandemic effect and governments' response of these countries will be different both in their essence and in the form of measures implementation to reduce negative economic effects. Consequently by missing such a difference between countries, we cannot fully assess the development conjuncture of the socio-economic systems of these countries.

The UNCTAD study [30] examines the pandemic impact on international trade. The study demonstrates a volume decrease of international trade transactions in all countries, with an emphasis on different dynamics in different groups of goods. China's foreign trade is considered separately as the most significant player in the international market, but the countries' conditions in terms of economic systems are not compared. At the same time different economic systems provide a different response speed degree from the state to the global economic situation deterioration, which was not reflected in the study.

Particularly interesting from the point of view of the COVID-19 pandemic consequences is the study of the International Labor Organization [13]. Given the fact that countries with different economic models regulate the labor market differently, the study of the International Labor Organization does not take this factor into account when assessing the pandemic consequences on the countries of the world labor markets. We believe that differences in economic systems and their regulation types are an important factor that determines the development parameters of socio-economic systems of different countries and requires careful research.

In the COVID-19 potential effects study on GDP and trade [22, 4], the authors also do not take into account the differences in the economic systems of different countries. In this study the authors consider the pandemic consequences through a macroeconomic model, which includes the market for goods, market for resources, as well as the main economic agents- firms, households and the state. In doing so the distinction in the different countries economic systems also does not take into consideration, although this factor is important, since state policy directly affects the country's market.

In a study of a pandemic effects on the Irish economy [9], the authors use a modeling process to determine possible consequences. The influence model factors include production shock, consumption shock, labor market shock, trade shock, shock in the energy market, income shock. It should be noted that this approach generally takes into account the specifics of the Ireland economic system, since the model is based on its economy indicators, but there is no comparison with other economic systems. We believe that it is the comparison of different economic systems that will assess the situation of socio-economic development of different countries most reliably in the context of the COVID-19 pandemic crisis.

In other study the pandemic impact for Asian countries was assessed [1]. The research compares the economic indicators of the Asian countries development during a pandemic, but the whole comparison is limited directly by the dynamics of the socio-economic development values indicators. In so doing the difference in economic systems between Asian countries, which are significantly different and are an important factor in socio-economic development, is not considered.

The definition of the economic pandemic impact on the ASEAN countries economies [2] considers the forecast values of the main macroeconomic indicators. This also does not take into account the difference in economic systems, although at certain points the Chinese economy is compared with other countries. Apparently such a comparison is justified by the size of the country's economy on the scale of global markets. But the study authors do not compare the economies of countries with different economic systems and do not determine the differences in the consequences of a pandemic for such countries.

The pandemic impact study on the gender inequality [29] also does not take into account the difference in economic systems between countries. At the same time different economic systems have varying inclusivity and extractiveness degrees, which directly affects the development degree and efficiency of the human capital use. In our opinion the pandemic consequences assessment on the socio-economic development conjuncture should be considered through the distinctions prism in the economic systems of different countries.

The studies we provided insight into consider determining the economic pandemic effect without taking into account the differences between countries with different economic systems. Comparing countries with different economic systems is extremely difficult, since the mechanisms and conditions of their functioning differ. Moreover, as a rule, such countries are located in different economic regions, are different integration associations' members and have different foreign policy vectors. In this regard, it is difficult to find two similar countries with different economic systems to compare the dynamics of their development. However, the economic crisis caused by the COVID-19 pandemic, as well as the EU and US sanctions against Russia, together formed similar conditions for the external environment for Russia and China (Table 1), which are a prerequisite for comparing the economic systems of these countries. Russia and China are leaders in socioeconomic development in their regions. In addition, they have close economic relations and a common border, which in general makes the countries' economic systems comparable for our study purposes. Both economic systems entered an active growth phase not so long ago - since the end of the 20th century, as a result of which they are both equally influenced by the world crisis and world economic upswings that were being established on their internal development cycles. Also, the economic systems of Russia and China are under external restrictions: Russia under the conditions of EU and US sanctions; China under US protectionism.

Russia and China have a large population and territory, are endowed with many natural resources, which is an important component of socio-economic development. Given all the listed characteristics of the countries selected for the study, it is difficult to find another pair of countries with such comparable parameters, but different economic systems. A number of studies [7, 6] consider Russia and China as part of the BRICS as countries that increase their influence in the world and form a counterweight to economically developed countries with liberal systems [21].

Table 1: Prerequisites for Comparing the Socio-Economic Development of Russia and China in the Context of the COVID-19 Pandemic

<table><tr><td>Economic Systems Similarity Criterion</td><td>Russia</td><td>China</td></tr><tr><td>Sanctions or protectionism influence on the other countries economy</td><td>The EU and United States Sanctions</td><td>US protectionism</td></tr><tr><td>Regional Economic Centers</td><td>Regional Economic Center in the Post-Soviet Space</td><td>Regional Economic Center in Southeast Asia</td></tr><tr><td>Impact on global market conjuncture</td><td>Energy market</td><td>Commodity market</td></tr><tr><td>The UN classification of the country development level</td><td>Emerging economy country</td><td>Emerging economy country</td></tr><tr><td>Countries' territorial proximity</td><td>It has a common border with China, located in Asia</td><td>It has a common border with Russia, located in Asia</td></tr></table>

At the same time, having a number of similar characteristics, Russia is a country with a market economy, China has a command and administrative economic system. Given the fact that both countries are subject to the COVID-19 pandemic economic consequences, the purpose of our study is to

empirically demonstrate the co-directed and opposite dynamics of modern economic systems development in order to assess the socio-economic development situation in the COVID-19 pandemic context using Russia and China example.

## III. METHODS AND MATERIALS

To determine the differences between market and command and control economic systems, we will analyze empirical data that characterize the economic development of Russia and China. We use such indicators to perform this task (Fig.1).

Fig. 1: Economic System Development Indicators

Source:Developed by the Authors

The GDP dynamics analysis will allow to estimate the volume growth of goods and services production in absolute volumes. GDP per capita is a more informative indicator in the context of the two economic systems comparing, as it shows how much goods and services the economy produced per person. Since GDP is currently one of the main economic indicators, we also use it for our research purposes.

One of the important economic systems characteristics is the income distribution. In our study we use several economic indicators to estimate the income distribution in economic systems. The gross savings indicator makes it possible to assess the degree of wealth of the economy and its potential for development. Total income is allocated to consumption and savings, which can be further transformed into internal investments. Thus, gross savings show an unused income portion. The share measure of the $20\%$ poorest population income shows how much income is fairly distributed in the economic system. It is the indicator that is the stumbling block of the two economic systems. In the market system, the state practically does not redistribute income with the exception of social programs, and in the command and administrative redistribution of income it is advisable and is an advantage of this economic system, according to its supporters. Consumer spending shows the portion of income that households use to meet their needs. The greater the value of this indicator, the more households purchase goods and services.

The inflation indicator shows the effectiveness and the national monetary unit stability. Stable and low inflation allows you to ensure real economic growth and stimulate economic activity. In addition, stable inflation indicators show the economy condition in the market economic model. In the command and administrative system, inflation is almost entirely under state control. Economic factors affect the monetary unit stability much less than in the market system, and the main channel for inflation is the price of imported goods and resources.

The imports and exports volume shows the economy openness degree. The larger the GDP volume, the more the economy can export goods and services and the more it can purchase goods and services from other countries. The imports growth allows to increase the goods and services choice for the country population, which is regarded as an increase in wealth.

Foreign debt shows how much the country lent money in international financial markets. It is generally accepted that the smaller the external debt amount, the more financially independent the economy is. But in the modern world, the more important role is played not by the volume of external debt, but by its price. For example, Japan's external debt is almost equal to the GDP (91.9% of GDP [28]), but the borrowed funds cost is relatively low, which allows the Japanese economy to develop successfully.

Having analyzed the values dynamics of the described economic indicators, we will determine their trends. On the basis of the information received we will be able to compare Russian and Chinese economic systems and determine their co-directivity and multi-directivity development vectors. To determine these countries socio-economic development conjuncture during the COVID-19 pandemic, we will make a values forecast of the analyzed indicators of the economic systems development for 2021, 2022, 2023. Our study hypothesis is that a more stable and strong economic system is less susceptible to the crisis influence, which means it will have better indicators of socio-economic development in a pandemic. Consequently, we assume that the average trend in economic dynamics will be observed for the forecast period 2021-2023, given that in 2020 the economies of Russia and China as a whole adapted to crisis conditions and there was an economic activity resumption at the end of 2020.

For analysis, we use economic indicators data for the period from 1988 to 2020. For some indicators (gross savings, inflation, external debt, household consumption, $20\%$ of the poorest population income share, unemployment rate), values will be taken for the period after 1988 due to the fact that there is no data for an earlier period. All data were taken from the World Bank official website [27], statistics section. All calculations, chart construction and indicator values forecasting were carried out in the Microsoft Excel software product.

## IV. RESULTS

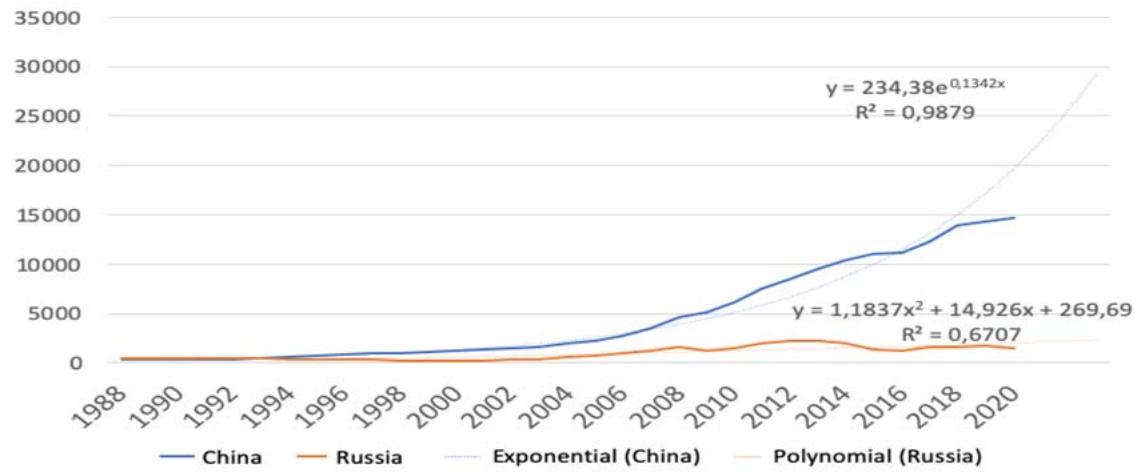

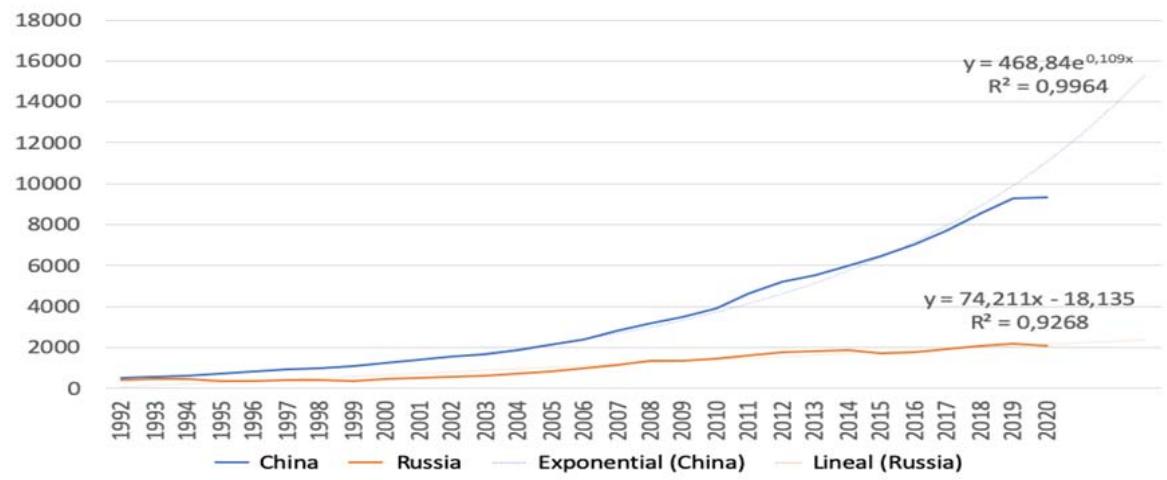

Our study results describe we will begin with the dynamics analysis of the economic systems indicators of Russia and China and for each indicator we will calculate the forecast values. Figure 2 shows that the GDP growth dynamics in countries has an upward trend, as evidenced by the trend lines.

Fig. 2: GDP Growth Dynamics in Russia and China, 1988-2020, Billion US Dollars [Compiled by the Authors on the Basis of 27]

In addition, the calculated correlation coefficient between the GDP of Russia and China is 0.83. This means that the countries' GDP dynamics is co-directed. It is possible that there is a certain GDP growth dependence of the studied economic systems on each other, but in this case we assume that such co-orientation is due to the general dynamics of global GDP growth. The GDP indicators forecast values for Russia and China are calculated on the exponential average basis with a reliability of $98\%$ and predicts further growth. In general, the forecast shows a significant gap in GDP growth rates, but the key is that in the COVID-19 pandemic context, GDP is predicted to increase in both economic systems, which is a positive trend. Figure 3 shows the GDP growth dynamics per capita.

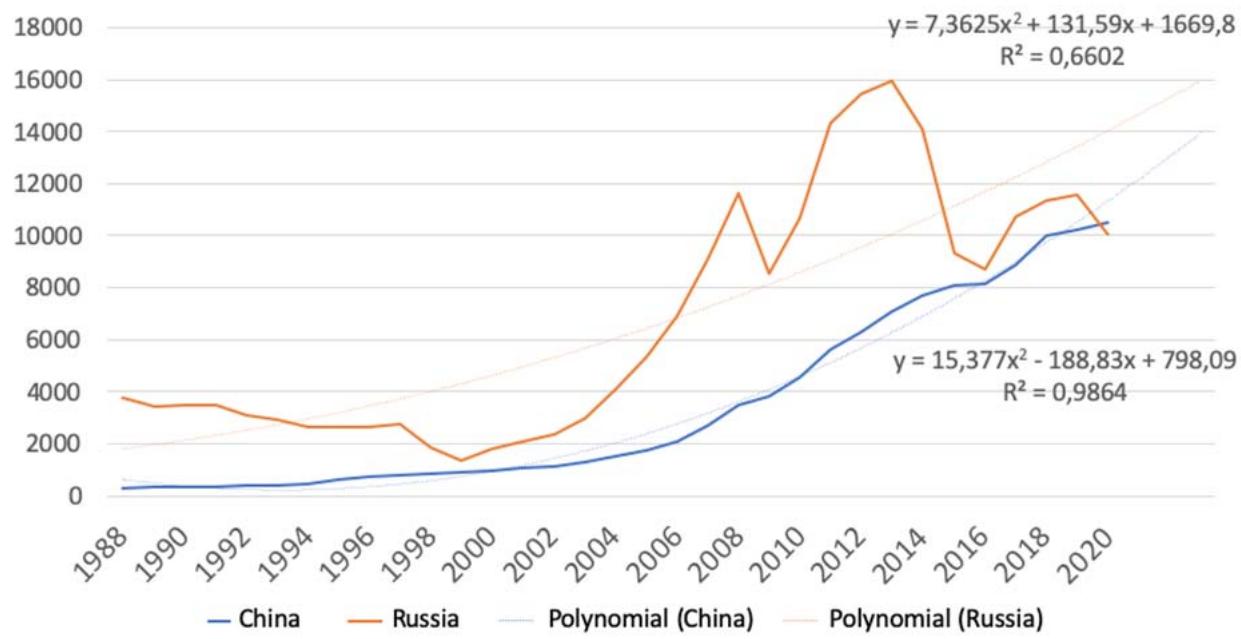

Fig. 3: Dynamics of GDP Growth per Capita in Russia and China, 1988-2020, US

$ [Compiled by the Authors on the Basis of 27]

Per capita GDP growth predictably has the same trend as the GDP absolute value. For the studied economic systems, co-directed GDP growth per capita is characteristic. The correlation coefficient between them is 0.83, which is also typical for the GDP correlation of these countries. But if China has more GDP in actual prices, then Russia has more GDP per capita. This is primarily due to the fact that the China population significantly exceeds the population of Russia. Also an economic systems hallmark is that China has a more robust trend towards GDP and GDP per capita growth. For Russia, GDP fell in 1998, 2008 and 2014 is on sight, which was due to crisis

phenomena. At the same time, the Chinese economy was also exposed to the 2008 crisis and US sanctions, but there was no decrease in GDP. This suggests that China's economic system is more resilient to crisis events and has domestic reserves for growth.

Analyzing the GDP per capita forecast values, this indicator value is expected to grow for Russia with a reliability of $66\%$ and for China $98\%$. In general, such forecast dynamic is consistent with the dynamics of GDP growth and is a positive trend in the socioeconomic situation development of the studied economic systems. Figure 4 shows the growth dynamics of gross savings in Russia and China.

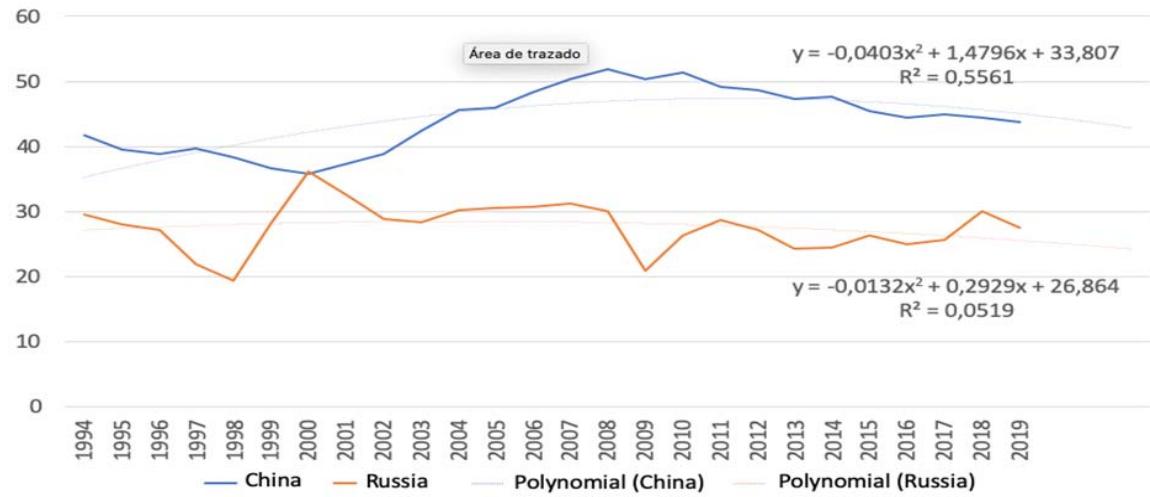

Fig. 4: Gross Savings Growth Dynamics in Russia and China, 1994-2019, % of GDP [Compiled by the Authors on the Basis of 27]

Gross savings are an internal factor in economic growth, as they can transform into domestic investment. We are seeing an upward trend in gross savings in China, with them averaging $40\%$ to $50\%$ of GDP. At the same time, in Russia there is a tendency to reduce gross savings, which on average amount to less than $30\%$ of GDP. According to this indicator, we see multidirectional vectors for the Russia and China economic systems development. It is important to note that the trend towards a decrease in gross savings in Russia is negative in the long term. We can assume that it is the decrease in gross savings that weakens the economy, which is especially evident in times of crises

(1998, 2008, and 2014) and reduces the ability to neutralize external economic shocks.

This indicator value forecast shows its fall in 2021-2023. For China, this trend is reliable by $55\%$, and for Russia by only $5\%$. It is worth noting that the $\mathsf{R}^2$ low level for the Russia forecast is due to a significant deviation of the actual indicators of gross savings from the trend value, which indicates other factors strong influence.

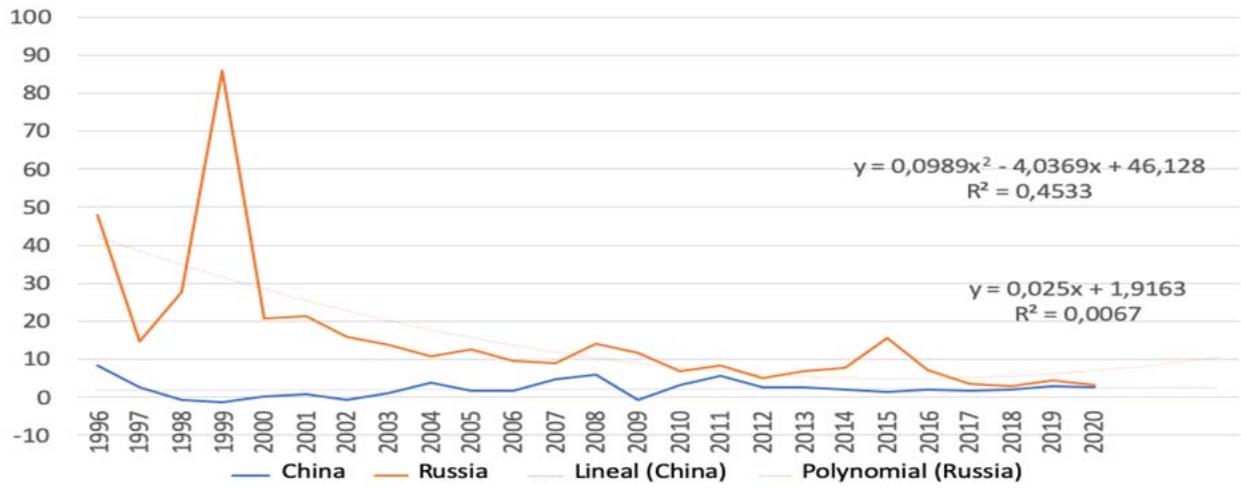

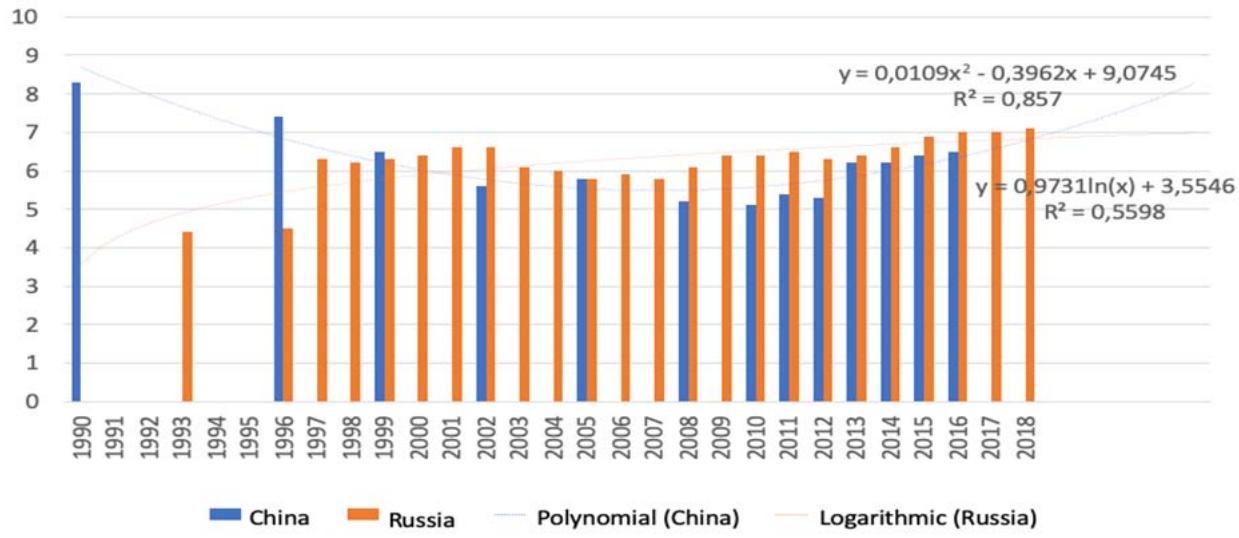

Inflation is one of the key indicators of the economy state and its development prerequisites. Inflation dynamics in Russia and China is shown in Figure 5.

Fig. 5: Inflation Dynamics in Russia and China, 1996-2020, % of GDP [Compiled by the Authors on the Basis of 27]

The economic systems of Russia and China are characterized by different dynamics of inflation rates in the period 1996-2019. For China, the annual inflation rate did not exceed $10\%$ and on average there is a trend towards its stability below $5\%$, which is a very good indicator for the developing economy. Inflation at this level provides growth in gross output and at the same time real income growth in the economy. For Russia, inflation indicators are on average about $10\%$ since 2003-2004. Prior to this period, hyperinflation was observed, which in general created a downtrend of this indicator. In general, it can be argued that after 2004 inflation dynamics, although it has a weak downtrend, inflation indicators remain relatively stable.

The forecast inflation trend for Russia has an upward trend and by 2023 the inflation rate is predicted at $10\%$. The forecast reliability is $45\%$, but if we analyze the period of 2009 and 2015, we can see that after the crisis periods, the resumption of economic activity was carried out by increasing inflation. Thus, the expected inflation increase in 2021-2023 is somewhat cyclical for the Russian economic system. In China, the inflation dynamics forecast is also comparable to the last 10 years trend and a significant change in its dynamics is not expected.

Goods and services exports and imports are one of the main indicators of the economy openness and ensure the implementation of gross output produced. The dynamics of exports of goods and services is shown in Figure 6.

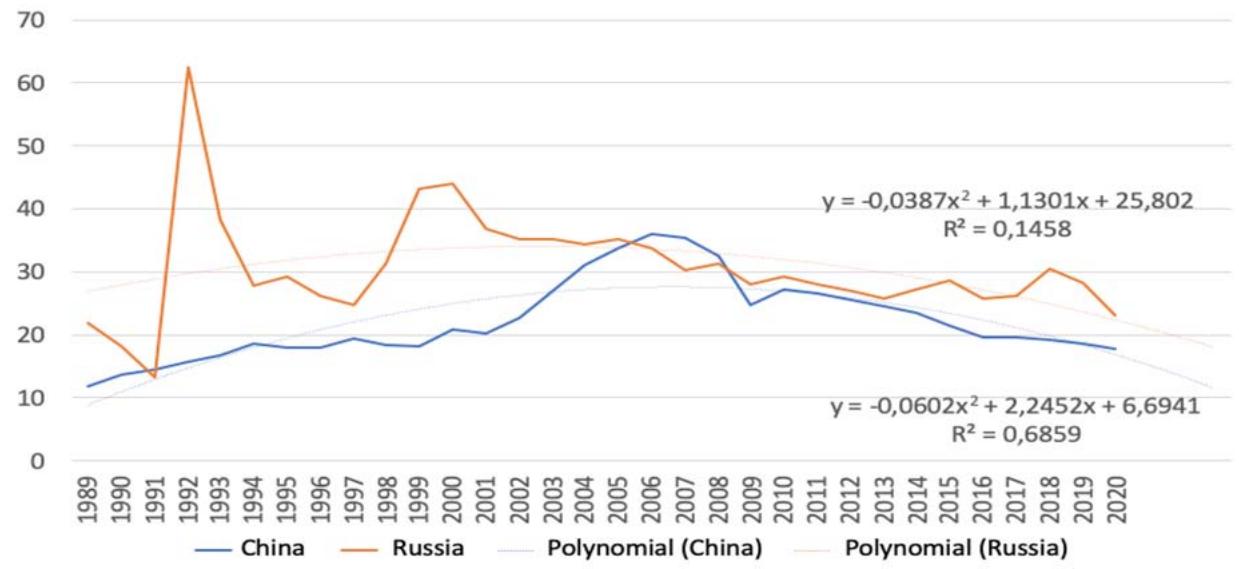

Fig. 6: Goods and Services Export Dynamics in Russia and China, 1989-2020, % of GDP [Compiled by the Authors on the Basis of 27]

Long-term trends in the goods and services exports dynamics of Russia and China are similar: until 2006 there was an increase in exports, and then a fall. But if we consider 'goods' and services exports dynamics of Russia and China more carefully, we can see that in general they are asynchronous. In those years when the exports share in Russia's GDP has increased, China has fallen. This is also confirmed by the correlation coefficient 0.11, which indicates that goods and services export dynamics vectors are multidirectional.

According to the forecast, a further significant downfall in the goods and services exports volume in Russia and China is expected. This trend is very expected in the context of crisis phenomena spread in the countries of the world and a decrease in the population purchasing power. In such conditions, the exports reduction is highly expected. Moreover, the economic development of national economic systems in a crisis is focused on the exports absorption by the domestic economy. A similar trend is observed in the goods and services import (Fig.7).

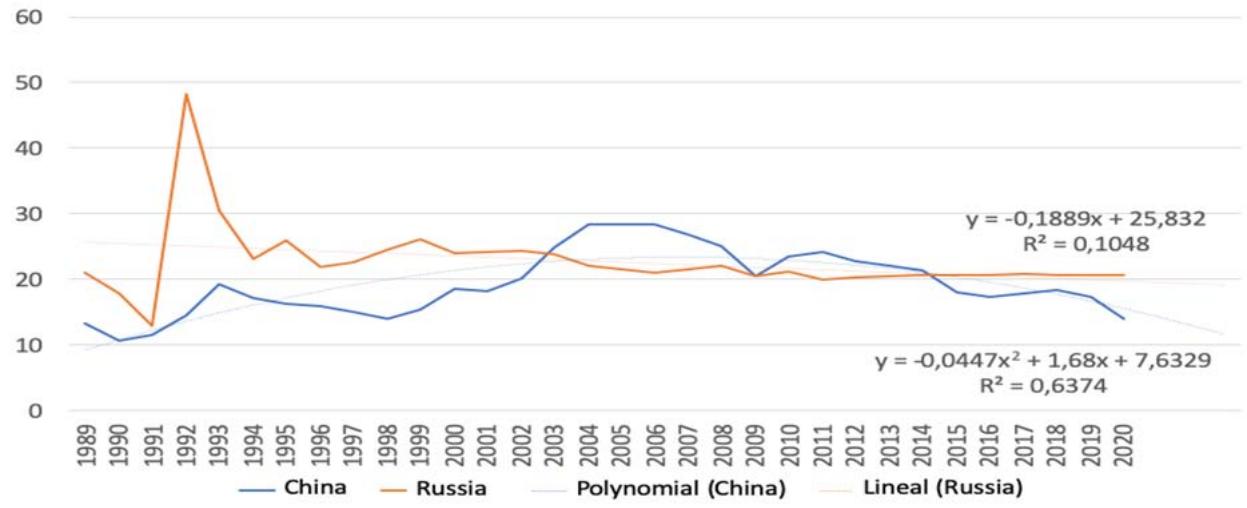

Fig. 7: Goods and Services imports Dynamics in Russia and China, 1989-2020, % of GDP [Compiled by the Authors on the Basis of 27]

The goods and services imports dynamics for Russia and China is multidirectional. If Russia is characterized by a decrease in the GDP imports share, then China is characterized by an increase in it. At the same time, for both economic systems, the imports share in GDP is less than the exports share, which

indicates a positive trade balance of countries. It is also important to indicate that after 2009, Russia is characterized by a practically stable share of imports in GDP with practically the same GDP dynamics (Fig. 2), and for China there is a tendency to reduce the imports share in GDP with significant GDP growth. From this we

can conclude that the Chinese economy is more independent of imports than the Russian economy. As for exports, there is also a decrease in the exports share relative to GDP for China. This means that the entire output gross volume is absorbed by the Chinese economy itself. The imports dynamics forecast of goods and services for Russia and China also indicates a trend towards its fall. This is partly due to the recent years'

trend, on which basis the forecast was carried out, and partly due to restrictions and irregularities in global supply chains, which significantly complicates the goods movement in the global market.

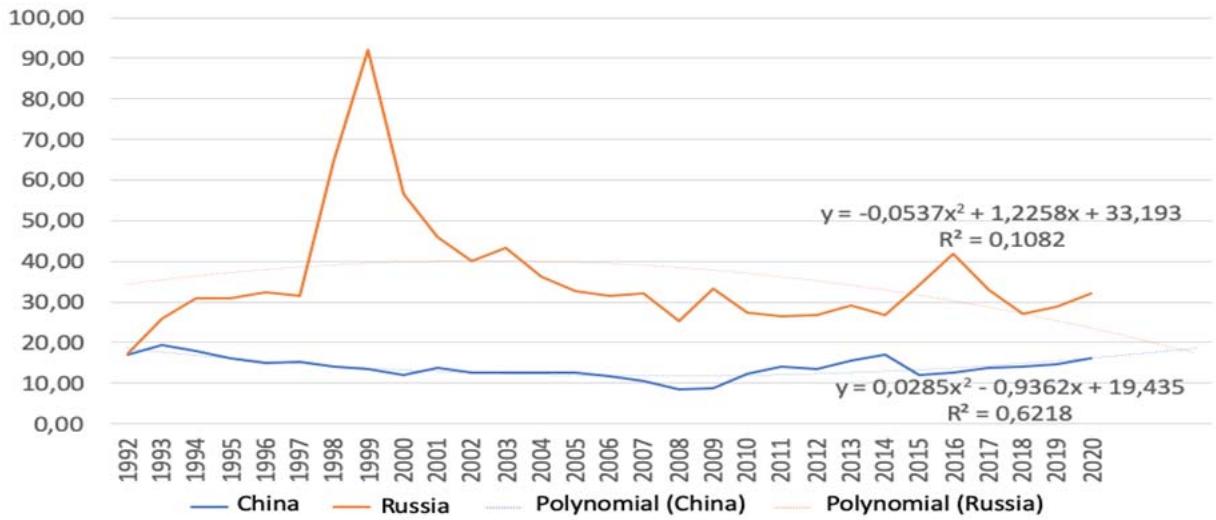

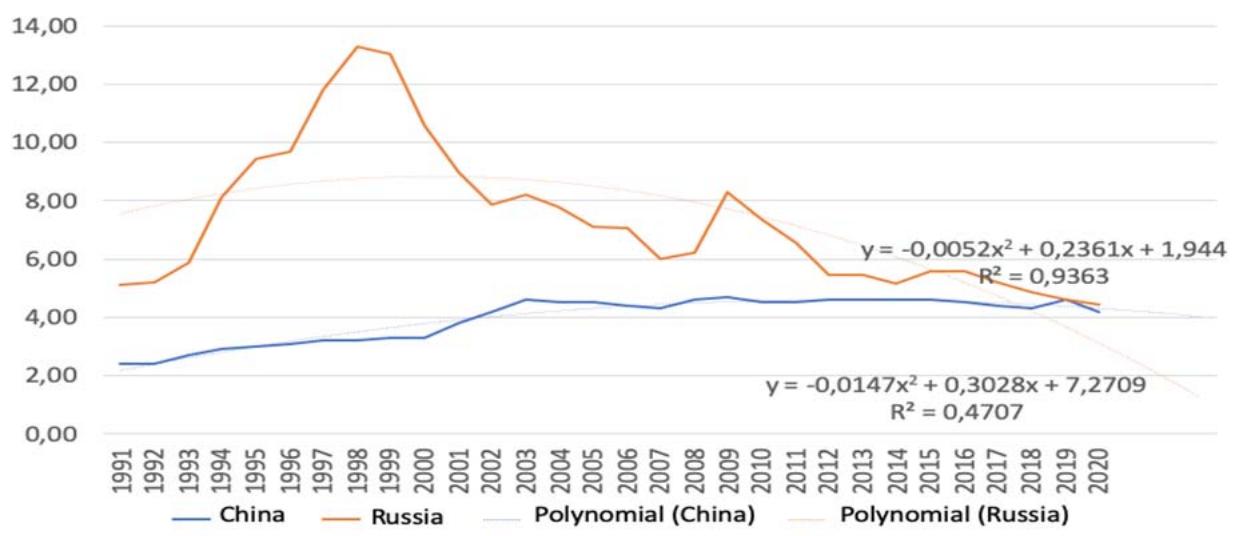

As for external debt, this indicator has a unidirectional dynamics vector for the Russian and Chinese economic systems (Fig. 8).

Fig. 8: External Debt Dynamics in Russia and China, 1992-2020, % of GDP [Compiled by the Authors on the Basis of 27]

China has significantly less external debt and averages $12\%$ of GDP. For Russia, this figure averages $35\%$ over the past 15 years. In general, the external debt dynamics for Russian and Chinese economies is similar and is characterized by the fact that in crises times the debt share relative to GDP is growing. In Russia, this trend was observed in 1997, 2008, 2014, and in China in 2008. We can conclude that the external debt indicator dynamics is co-directed in the economic systems of Russia and China, since on average there is a tendency towards an external debt decrease, but in crisis times it increases.

The external debt volume forecast dynamics indicates its decrease for Russia and an increase for China. Since Russia is under international sanctions, which, among other things, restrict access to international financial markets, we highly expect such a forecast. For China, a slight increase in external debt to GDP is predicted, which may be associated with China entering international markets to increase the economy capitalization in the post-crisis period.

An important indicator for assessing the country socio-economic development is household consumption, which dynamics is shown in Fig. 9.

Fig. 9: Household Consumption Dynamics in Russia and China, 1992-2020, Billion US Dollars [Compiled by the Authors on the Basis of 27]

The household consumption dynamics has a co-directed upward trend vector for both Russia and China. Consumption growth is generally interpreted as a positive characteristic for describing the economic system, because households have the opportunity to consume more goods and services. This implies both an increase in the produced goods volume and an increase in the population income. At the same time, this indicator is important to consider in the context of indicators such as inflation and income distribution. Consumption growth with relatively stable inflation is

evidence of real income growth, which is typical for both studied economic systems. Positive point is the positive forecast dynamics of increasing household consumption in Russia and China. The forecast accuracy is $98\%$ for China and $93\%$ for Russia. This dynamics indicates the withdrawal of economic systems from the crisis and an improvement in the socioeconomic situation. But an extremely important indicator of the socio-economic system development is the poorest population $20\%$ income share (Fig. 10).

Fig. 10: Income Share Dynamics of the $20\%$ Poorest Population in Russia and China, 1990-2019, Population % [Compiled by the Authors on the Basis of 27]

Information on Figure 10 shows that a more socially equitable income distribution is observed in Russia, where the income share of the $20\%$ poorest population tends to increase. In China, on the contrary, this indicator tends to decrease until 2020 and after 2011 an increase trend begins. This conclusion is quite unexpected, since Russia belongs to countries with a market economic system, and China - to planned-administrative, where, in addition, a one-party political system with the ruling Communist Party. Ideological influence in China was supposed to contribute to a greater trend in income redistribution. In general, analyzing the last 10 years, we can argue that economic systems have a co-directed vector in the redistribution of income in favor of the $20\%$ of the poorest population. After a significant drop in the income distribution in China in the period 1990-2010, a significant increase is predicted in 2021-2023. We can assume that this trend will be due to significant growth in GDP and GDP per capita. The reliability of such a forecast is $86\%$. At the same time, for Russia there is a forecast trend towards a decrease in this indicator dynamics and in fact its fixation at the level of $7\%$. In general, this trend characterizes the socio-economic situation deterioration. In this context, it is important to consider the

unemployment dynamics, which is always a significant negative factor in the development of the country's economy (Fig. 11).

Fig. 11: The Unemployment Rate Dynamics in Russia and China, 1990-2020, % of the labor Force [Compiled by the Authors on the Basis of 27]

For China, there is a trend of an unemployment rate increase, while for Russia - an unemployment decrease trend. In this case, it is important to take into account the fact of the China population increase, which puts additional pressure on the labor market. There is no such factor in Russia, which contributes to the unemployment decrease rate after the crisis period of the 1990s. Thus, the unemployment rate dynamics for Russia and China is multidirectional. The unemployment dynamics forecast in Russia shows that it will decrease significantly. The reliability of such a forecast is $47\%$. It is important to underline that this forecast is statistical, that

does not take into consideration many factors affecting the labor market. It is more likely that unemployment, if it continues to decline, is at a much slower pace than the forecast shows. In China, an unemployment slight decrease is also expected with a reliability of $94\%$. On average, unemployment in China is expected at $4\%$ in 2021-2023, which is a very real forecast.

Having analyzed the indicators values dynamics of the economic systems socio-economic development of Russia and China, we can present the results obtained in Table 2.

Table 2: Significance Dynamics Co-directivity and Multidirectionality of the Russia and China Economic Systems Development Indicators

<table><tr><td>№</td><td>Indicator</td><td colspan="2">Actual indicators directional vector</td><td colspan="2">Forecast indicators directional vector</td></tr><tr><td></td><td></td><td>China</td><td>Russia</td><td>China</td><td>Russia</td></tr><tr><td>1</td><td>GDP</td><td>↑</td><td>↑</td><td>↑</td><td>↑</td></tr><tr><td>2</td><td>GDP per capita</td><td>↑</td><td>↑</td><td>↑</td><td>↑</td></tr><tr><td>3</td><td>Grossavings</td><td>↓</td><td>↓</td><td>↓</td><td>↓</td></tr><tr><td>4</td><td>Inflation</td><td>~</td><td>~</td><td>↓</td><td>↑</td></tr><tr><td>5</td><td>Goods and Services Export</td><td>↓</td><td>↓</td><td>↓</td><td>↓</td></tr><tr><td>6</td><td>Goods and Services Import</td><td>↓</td><td>↓</td><td>~</td><td>~</td></tr><tr><td>7</td><td>External Debt</td><td>↑</td><td>↑</td><td>↓</td><td>↓</td></tr><tr><td>8</td><td>Consumer Spending</td><td>↑</td><td>↑</td><td>↑</td><td>↑</td></tr><tr><td>9</td><td>20% Poorest Population Income Share</td><td>↑</td><td>↑</td><td>↑</td><td>~</td></tr><tr><td>10</td><td>Unemployment</td><td>~</td><td>~</td><td>↓</td><td>↓</td></tr></table>

The obtained study results indicate that inflation, goods and services imports and exports, external debt, all income share of the $20\%$ poorest

population, unemployment rate have a multidirectional trend in the indicators values in the long term. This indicates significant differences between the economic

systems of Russia (with a market economy system) and China (with a command and administrative economic system). The study results indicate that China's economic system is stronger in the forecast period 2021-2023, as evidenced by the declining inflation expected dynamics, and an increase in the income share of the $20\%$ poorest population. It is these indicators that distinguish the forecast of the socioeconomic situation of the Chinese economy from the Russian economy in 2021-2023. In general, positive dynamics of socio-economic conditions indicators in Russia and China is expected. Apparently, in the next three years, in both countries with different economic systems an economic activity and economic growth resumption will be observed.

## V. DISCUSSION

Our study results indicate an exit forecast from the economic downturn of countries with different economic systems - Russia and China. We compare the obtained results with the other studies results dedicated to the socio-economic development assessment of countries in the COVID-19 pandemic post-crisis period.

First of all, it is worth mentioning two International Monetary Fund studies, which assessed the economic resumption trend of the global economy after the pandemic. The first study [15] predicted a $3\%$ drop in global economic growth in 2020, while the second study [14] predicted a decline that worsened to $4.9\%$. In the 2021 study, the IMF predicts global economic growth in 2021 by $6\%$, in 2022 $4.4\%$ [16]. The results of our study also predict the studied economic systems economies growth, which is generally determined by the global dynamics.

Analyzing the ASEAN countries economic growth forecasts [3], it should be noted that there is also forecast economic growth at the level of $6.2\%$ for developed countries of Asia, $6.7\%$ for developing and new industrial countries of Asia, $7.3\%$ for the Chinese economy, and $4.7\%$ for countries of Southeast Asia. Such results are comparable to those of our study, in which we also forecast China's economic growth in 2021-2023.

In a study of the economic renewal effect plan based on the post-Keynesian approach [24], the authors conclude that both plans under consideration will lead to economic growth. According to their forecast, excluding the pandemic, global economic growth would average $7\%$ per year. In the post-pandemic context, depending on the impact scenario on the economy in different countries, the global economy forecast growth ranges from $2\%$ to $3.5\%$ per year. In addition, the plans under consideration for the economy resumption assume a decrease in consumption from $4.2\%$ to $6.3\%$ in 2022. According to

our study results, consumption is predicted to grow both in Russia and in China.

The study [17] affirms that the COVID-19 pandemic represents a unique shock to the economy, combining supply, demand and financial shocks and, therefore, requiring a political response that exceeds the standard set of monetary, tax and social protection measures that respond to shock. The study focuses on public policy and government programs as a response to the pandemic. But more detailed differences in the policies types of different economic systems are not considered in the study. In our study we also investigated different economic systems to determine their socio-economic conjuncture in a pandemic period. Our conclusions indicate that China economic system has a better socio-economic situation in a pandemic.

Another study [25] also does not address the question of the difference in economic systems and their socio-economic development in a pandemic. The author predicts the global GDP growth, but does not consider the economic growth dynamics in the different economic systems context. And Klein and Pettis [19] consider the role of trade wars without taking into account the distinctions in the different countries economic systems. Milanovich [23] views the capitalism future as an economic system, but does not compare it with other economic systems.

Various authors consider the same economic parameters of the economic systems functioning as we do. Using transaction-level household data, the authors [5] found that during the initial period, households dramatically increased their spending in certain sectors, such as retail and food spending. However, this increase was followed by a decline in overall spending. In our study, we forecast an increase in consumer spending in 2021-2023.

Binder [8] conducted an online survey of 500 consumers in the United States to understand their concerns and responses related to COVID-19, which indicates the consumption items on which they spend more or less. It found that $28\%$ of survey respondents had delayed or cancelled future travel plans and that $40\%$ had abandoned food purchases. Consumers tend to attribute heightened concerns about COVID-19 to higher inflation expectations, a sentiment that has emerged to be an indicator of "pessimism" or "bad times". In our study we predict an inflation increase in Russia and its invariability in China. At the same time the authors do not consider differences in consumer reactions depending on the economic system type.

Comparing the obtained results with the other studies results, it is quite difficult to find common points of intersection. The studies we analyzed focus on possible scenarios for post-pandemic economic development while our study focuses on differences in economic systems. At the same time, we see that our

indicators forecast values are supported by other studies. An important scientific result of our study is that the planned and administrative economic system of China will more rapidly emerge from the crisis in the post-pandemic period than the Russia market economic system.

Our study results may be applicable in several areas. Firstly, our results show that in a crisis, the government powers expansion in the economic regulation field can have a positive effect and reduce the economic recession period. This conclusion can be used in the economic regulation practice at the ministries and governments' level. Secondly, our study results open up opportunities for further investigation of the economic systems multidirectional development, including social and environmental effects.

## VI. CONCLUSIONS

The study results figured that the market economic system and the command and administrative system have both co-directional and multi-vector dynamics of economic development, which is displayed in the economic indicators dynamics. An empirical data study indicated that the co-directed development vector has GDP, GDP per capita, gross savings, consumer spending, and the income share of $20\%$ of the poorest population. According to these indicators, the Russian economy and the Chinese economy have the same trends towards a decrease or increase in indicators. A multidirectional development vector of Russia and China economic systems is observed for such indicators as inflation rate, imports of goods and services, external debt, unemployment rate. It is worth mentioning that the co-directed dynamics indicators are effective. GDP, GDP per capita, gross savings are the result of economic activity. While the multidirectional dynamics indicators are the internal economic environment factors and the regulation by state bodies. Inflation is targeted by the central bank, external debt is determined by the government, and the unemployment rate is also a tool associated with inflation (according to Phillips law). The study results indicated that China's economic system is more stable and resistant to crisis phenomena. If the inflation forecast for Russia is an increase, then for China there is no change with a low inflation rate on average. For China, an increase in the specific weight of income is predicted, which is owned by $20\%$ of the poorest population, then for Russia, the invariability of this indicator is predicted.

The study conducted has limitations. The methodological limitation is that the study looked at only two countries and the sample size could be increased. In addition, an important limitation is that there are much more market economies than countries with other economic models. As a result of this, it is difficult to form a sufficiently representative sample for the study. The disparity of the economies of Russia and China can also be considered as a limitation due to the significant prevalence of China's absolute indicators over Russia's. In this regard, we tried to use not absolute indicators, but relative ones, which allow us to level this difference in the scale of economies.

The implementation limitation is that our results study can be applied to the developing countries' economies. The main prerequisite for applying our results is the economy market laws functioning. In addition, we cannot univocally assert that the obtained results may be applicable to countries that are in a state of military conflict or state of emergency, in which a state has expanded powers in regulating economic processes in a country.

Generating HTML Viewer...

References

30 Cites in Article

Abdul Abiad,Mia Arao,Suzette Dagli,Benno Ferrarini,Ilan Noy,Patrick Osewe,Jesson Pagaduan,Donghyun Park,Reizle Platitas (2020). The Economic Impact of the COVID-19 Outbreak on Developing Asia.

Jayant Menon (2020). Assessing the economic impacts of COVID-19 on ASEAN countries.

(2020). Economic Impact of COVID-19 Outbreak on ASEAN.

David Bailey,Jennifer Clark,Alessandra Colombelli,Carlo Corradini,Lisa De Propris,Ben Derudder,Ugo Fratesi,Michael Fritsch,John Harrison,Madeleine Hatfield,Tom Kemeny,Dieter Kogler,Arnoud Lagendijk,Philip Lawton,Raquel Ortega-Argilés,Carolina Otero,Stefano Usai (2020). Regions in a time of pandemic.

Scott Baker,Nicholas Bloom,Steven Davis,Stephen Terry (2020). COVID-Induced Economic Uncertainty.

Mark Beeson,Troy Lee‐brown (2017). The Future of Asian Regionalism: Not What It Used to Be?.

Mark Beeson,Jinghan Zeng (2018). The BRICS and global governance: China’s contradictory role.

Carola Binder (2020). Coronavirus Fears and Macroeconomic Expectations.

Kelly De Bruin,Eoin Monaghan,Aykut Mert Yakut (2020). The environmental and economic impacts of the COVID-19 crisis on the Irish economy: An application of the I3E model.

J Diamond (2019). Upheaval. Turning Points for Nations in Crisis.

(2020). Measuring the Impact of COVID-19 with a View to Reactivation.

Economist (2020). Everything's under control. The state in the time of covid-19.

(2020). COVID-19 and the world of work: Impact and policy responses.

(2020). IMF World Economic Outlook (WEO) Update, July 2013.

(2020). IMF Managing Director's Statement to the Development Committee, April 2020.

(2021). World Economic Outlook, April 2021.

(2020). Socio-economic impacts of COVID-19, policy responses and the missing middle in South Asia.

J Jackson,M Weiss,A Schwarzenberg,R Nelson,R Sutter,M Sutherland (2021). Global Economic Effects of COVID-19.

M Klein,M Pettis (2020). Trade Wars Are Class Wars: How Rising Inequality Distorts the Global Economy and Threatens International Peace.

Melissa Leach,Hayley Macgregor,Ian Scoones,Annie Wilkinson (2020). Post-pandemic transformations: How and why COVID-19 requires us to rethink development.

E Luce (2017). The Retreat of Western Liberalism.

M Maliszewska,A Mattoo,D Mensbrugghe (2020). The Potential Impact of COVID-19 on GDP and Trade.

B Milanovic (2019). Capitalism, Alone: The Future of the System That Rules the World.

H Pollitt,R Lewney,B Kiss-Dobronyi,X Lin (2020). A Post-Keynesian approach to modelling the economic effects of Covid-19 and possible recovery plans.

Cristiana Vagnoni (2020). Long COVID: The long-term health effects of COVID-19.

(2020). How COVID-19 is Changing the World: A Statistical Perspective.

Maximilian Mücke (2021). worldbank: Client for World Banks's 'Indicators' and 'Poverty and Inequality Platform (PIP)' APIs.

No ethics committee approval was required for this article type.

Data Availability

Not applicable for this article.

How to Cite This Article

Zemskov Vladimir Vasilevich. 2026. \u201cThreats to the Global Economy in the Context of the COVID Pandemic on the Example of Russia and China\u201d. Global Journal of Management and Business Research - C: Finance GJMBR-C Volume 23 (GJMBR Volume 23 Issue C1).

Explore published articles in an immersive Augmented Reality environment. Our platform converts research papers into interactive 3D books, allowing readers to view and interact with content using AR and VR compatible devices.

Your published article is automatically converted into a realistic 3D book. Flip through pages and read research papers in a more engaging and interactive format.

Our website is actively being updated, and changes may occur frequently. Please clear your browser cache if needed. For feedback or error reporting, please email [email protected]

Thank you for connecting with us. We will respond to you shortly.