This paper critically examines the policies and practices governing dividend payments in State-Owned Enterprises (SOEs), with a focus on India and selected foreign jurisdictions. The study begins with a comprehensive literature review of dividend theory, exploring its traditional interpretations and the unique adaptations necessary for its application in SOEs, which operate under distinct mandates compared to privately held enterprises. By analyzing the theoretical underpinnings, the paper sets the stage for an informed discussion on the rationale, mechanics, and implications of dividend payments by SOEs. In the Indian context, the paper addresses key questions: why SOEs pay dividends, how much they pay, who determines these payments, and the institutional machinery governing such decisions. These inquiries are explored against the backdrop of recent trends, such as the record � 61,149 crore dividend payout by Indian SOEs in FY 2023-24, a 22% increase from the revised estimate. This upward trend underscores the growing fiscal significance of SOE dividends in India’s public finances and necessitates a closer examination of the factors driving these payments and their broader economic implications. The governance frameworks and decision-making procedures that support dividend payments in SOEs are also examined. It explores the relationship between corporate governance standards, board independence, and governmental directives, pointing out points of agreement and disagreement. In order to identify best practices and creative strategies that may be modified for the Indian context, the research also examines dividend payment regulations in a number of international countries. The paper concludes with actionable recommendations to enhance dividend payment policies and practices in Indian SOEs. These include strengthening governance frameworks, balancing fiscal imperatives with enterprise sustainability, and fostering transparency and accountability in dividend-related decisions. By integrating insights from domestic and international practices, the paper aims to contribute to the ongoing discourse on optimizing the role of SOEs in economic development while ensuring their financial health and alignment with public policy objectives. The paper offers a critical perspective on the strategic role of SOE dividends in national economies and provides a roadmap for policymakers and stakeholders to refine dividend practices in India’s SOE ecosystem. dividend dilemma dividend policy dividends practices in indian soes foreign jurisdictions strategic role of soe dividends

# Introduction

ividends represent a portion of a company’s earnings distributed to its shareholders, serving as both a reward for investment and a signal of financial health and stability. Dividend policies, particularly in SOEs, carry distinct significance because these entities often balance commercial objectives with public policy mandates. Dividends provide shareholders with tangible returns on their investment, offering an incentive for continued investment in the company. For SOEs, dividends often serve as a key revenue stream for governments, helping fund public services and reduce fiscal deficits. Regular and predictable dividends indicate a company’s financial stability and profitability. They signal efficient operations and can boost investor confidence, making it easier to attract capital. In SOEs, dividends represent a mechanism for redistributing wealth from commercially successful enterprises to the public via government coffers, supporting broader socio-economic initiatives. Dividends impose discipline on management by requiring efficient allocation of retained earnings. This discourages overcapitalization and ensures better utilization of resources. Dividends reduce the free cash flow available to management, thereby limiting the potential for misuse of funds and aligning management's interests with those of shareholders.

A clear dividend policy ensures consistency in payout practices, fostering trust among shareholders and helping governments or investors plan their finances. For SOEs, a dividend policy helps balance the dual objectives of generating returns for the government and reinvesting earnings for long-term growth. It ensures that dividend payments do not compromise the enterprise’s financial sustainability or investment potential. A well-defined policy offers guidance on how much profit should be distributed as dividends versus its retention for future needs, providing a framework for decision-making. In SOEs, dividend policies align financial decisions with broader public policy objectives, such as infrastructure development or social welfare programs. An explicit policy facilitates benchmarking against international best practices, making the enterprise more competitive and attractive to potential investors. During economic downturns or financial crises, a robust dividend policy clarifies the adjustment of payouts, helping manage stakeholder expectations while preserving enterprise resilience.

**Significance**

In the context of SOEs, dividends are not just a financial obligation but a strategic tool to fulfil public policy mandates while ensuring the enterprise's commercial viability. A clear, consistent, and balanced dividend policy is essential to navigate the complex interplay between fiscal needs, enterprise sustainability, and investor expectations.

**Research Methodology**

The data from the Department of Public Enterprises' Annual Surveys, and its Guidelines served as the basis for this aggregative analysis. The other sources included the World Bank Annual Report, the OECD Corporate Governance Factbook, and published works on SOEs in India and a few other countries.

**Limitations**

The paper excludes public sector banks, Government-owned and managed insurance companies, cooperative enterprises in the corporate sector, and municipal enterprises. The Foreign Jurisdictions include only 40 countries.

# Literature Review

Dividend policy has received considerable attention in financial research due to its impact on shareholder wealth, capital structure, and company value. This research compiles key contributions to the literature on issues, ideas, and empirical evidence related to dividend policy and dividend policy of state-owned enterprises.

Since shareholders may generate "homemade dividends" by modifying their portfolios, Miller and Modigliani (1961), in their groundbreaking study contend that dividend policy has no impact on business value in ideal markets. Subsequent research, however, has examined market flaws such as taxes, agency costs, and signalling, which make choosing a dividend policy crucial for businesses. According to the bird-in-the-hand hypothesis (Gordon, 1963; Lintner, 1962), investors value companies with consistent dividend payments more highly because they choose the certainty of dividends above possible capital gains. However, according to the tax preference hypothesis of Brennan (1970), investors may choose capital gains since they have lower tax rates than dividends. Several macroeconomic and firm-specific factors influence dividend decisions. According to Rozeff (1982), there is a trade-off between transaction costs and agency costs. While dividends might help with free cash flow issues, they may also restrict chances for reinvestment. In a similar vein, Fama and French (2001) discovered that business size, growth prospects, and profitability are important factors that influence dividend distribution practices. The catering theory of dividends is one study that highlights the importance of investor emotion (Baker & Wurgler, 2004). According to this hypothesis, companies modify their payout policy in response to market sentiment to accommodate investor desires.

The viability of several hypotheses in diverse marketplaces has been examined through empirical investigation. The agency cost perspective is supported by DeAngelo, DeAngelo, and Stulz (2006), finding that companies with concentrated earnings typically pay greater dividends. Meanwhile, Allen and Michaely (2003) offer proof that dividend changes indicate management's optimism about future profits, supporting the signalling hypothesis. According to cross-national research, institutional and legal considerations have a big impact on dividend policy (La Porta et al., 2000). Businesses are more likely to pay dividends to shareholders in nations with robust investor protection, which is consistent with the dividend outcome model.

Traditional dividend theories' applicability has been re-examined in light of the increase in share repurchases. According to Skinner (2008), companies are increasingly choosing buybacks over dividends due to their flexibility and tax effectiveness. Farre-Mensa, Michaely, and Schmalz (2014) contend, however, that buybacks and dividends have complementary functions in corporate payment strategy. Furthermore, dividend policy research has taken on new aspects as a result of the adoption of environmental, social, and governance (ESG) standards. According to research by Fatemi, Glaum, and Kaiser (2018), companies with better ESG ratings are more likely to continue paying dividends steadily, demonstrating their dedication to long-term stakeholder value.

The hybrid structure of SOEs, which combine economic and public policy aims, makes them a unique framework for examining dividend programs. The factors, theoretical underpinnings, and empirical data pertaining to dividend policy in SOEs are examined in this paper.

In contrast to private companies, SOEs frequently face two demands on their operations: making money and meeting their socioeconomic obligations. Their dividend policy and other financial actions are impacted by this dichotomy. Since dividends are frequently a source of fiscal income, SOEs with government ownership tend to pay out bigger dividends (Bai & Xu, 2005; Megginson & Netter, 2001). Decisions on dividends in SOEs are influenced by the government's significant ownership interest. Research indicates that governments, particularly in developing nations, give dividends top priority as a steady source of revenue for fiscal budgets (Lin et al., 2018). This propensity may outweigh traditional variables, such as profitability and growth possibilities. In the context of SOEs, agency theory highlights the tension between executive discretion and governmental goals. By lowering the amount of free cash flow available for perhaps wasteful investments, high dividend distributions are frequently employed as a strategy to offset agency costs (Jiang et al., 2011). Political factors frequently influence dividend policy in SOEs. For instance, governments may prioritize short-term budgetary demands above long-term company development by pushing for larger rewards during fiscal deficits or election cycles (Chen et al., 2017). SOE dividend policies are heavily influenced by institutional elements including regulatory supervision, legal safeguards, and governance norms. To satisfy political demands in countries with poor governance, SOEs may pay out disproportionate dividends, sometimes at the price of operational effectiveness (La Porta et al., 2000).

In SOEs, dividends can be used as a tool to regulate inefficiencies and limit managerial discretion, in line with Jensen's (1986) free cash flow theory. Because SOEs have preferential access to government-sourced capital, the pecking order theory's usefulness in this context is restricted. It is still useful, nevertheless, for comprehending how dividend distributions fluctuate across various SOEs. Governments employ SOEs as tools to achieve budgetary and socioeconomic goals, according to political economic viewpoints. As a result, dividend policies frequently depart from strictly economic justifications (Shleifer & Vishny, 1994).

Empirical research shows that different nations have different SOE dividend policy practices. According to Lin et al. (2018), government pressures for fiscal contributions lead Chinese SOEs to pay bigger dividends than private companies. Similarly, Gupta and Rustagi (2019) discover that government fiscal requirements have a greater impact on dividend payments in Indian SOEs than do firm-specific elements like profitability or investment prospects. In SOEs, sectoral differences in dividend policy are noticeable. For example, industrial SOEs may have more fluctuating policies because of cyclical market conditions, but energy and utility SOEs frequently maintain consistent dividends because of their strategic importance and strong profitability (Megginson et al., 1994). However, studies have highlighted potential drawbacks of politically driven dividend systems. Overpaying dividends could deter investment in SOEs, ultimately diminishing their long-term value creation and competitiveness (Chang & Jin, 2016).

The effect of corporate governance changes on SOE dividend policy has been the subject of several studies. More balanced dividend plans in SOEs have been associated with better governance systems, including independent boards and performance-based incentives (Liao et al., 2020). Furthermore, dividend decisions are rapidly being influenced by the incorporation of environmental, social, and governance (ESG) factors in SOEs, which aligns them with more general sustainability objectives (Fatemi et al., 2018).

**Dividend Policy in SOEs in India**

The dividend policy in SOEs in India has evolved over more than five decades. The first flush could be ascribed to the *Public Accounts Committee*, 1962-63, according to which declaring dividends from the general reserve funds was to be discouraged for dividend payments from the current year’s earnings only. The *Committee on Public Undertakings*, 1967, stressed the idea of indicating the percentage of profit for building up internal resources for saving surplus for dividends.

The second flush emanated from the *Government of India (GoI) directive issued in* 1967 stating that annual profits were to be apportioned under various heads and the balance available be declared as a dividend. The Guidelines maintained that the SOE in the manufacturing and service sectors declare at a rate of 6-15 percent and 10-15 percent respectively. The third flush occurred in 1992 when the GoI made it obligatory for profit-making SOEs to declare at least 20 percent of PAT as dividends. SOEs already declaring dividends were required to pay 50 percent more than the existing dividend, subject to a minimum of 20 percent of PAT. SOEs were obliged to declare a minimum possible dividend to maintain both visible and feasible dividend rates over the years. The fourth flush in 2016 sought every SOE to pay a minimum annual dividend of 30 percent of PAT or 5 percent of the net worth, whichever was higher, subject to the maximum dividend permitted under the extant legal provisions. The SOEs having reserves over three times their paid-up capital should immediately consider the scope for issuing bonus shares. Companies with high market prices of shares will consider stock splits. The following are to be considered while making dividend decisions: Net worth of the CPSE and its capacity to borrow; Long-term borrowings; Capital Expenditure for Business Expansion needs; Retention of profit for further leveraging in line with the Business Expansion needs; and Cash and bank balance. Until October 2024, the policy continued to follow the basics of the 2016 policy with an accent on special dividends and quarterly payments of dividends and was heavily fiscal considerations driven. This was done to obliterate the non-achievement of disinvestment targets during the last several years (The Economic Times, 2024).

In November 2024, the Department of Public Enterprise and the Department of Investment and Capital Asset Management DIPAM (2024), Government of India, announced a new dividend policy that requires the SOEs to pay an annual dividend equal to at least 30 percent of net profit or 4 percent of net worth, whichever is higher. According to DIPAM standards, SOEs in the financial sector, such as NBFCs, are permitted to pay a minimum yearly dividend of 30 percent of PAT, subject to any applicable limits imposed by existing laws. Within its scope, the new regulation specifically mentions SOEs in the banking sector. According to the updated criteria, SOEs with a net worth of at least ₹3,000 crore and cash and bank balances of more than ₹1,500 crore may also think about repurchasing their shares if the market price of their shares has continuously fallen below the book value during the previous six months. Additionally, it states that if an SOE-defined reserve and surplus equal or exceed 20 times its paid-up equity share capital, it may think about issuing bonus shares. Any listed SOE may think about separating its shares with a cooling-off period of at least three years between two consecutive share splits if its market price has continuously exceeded 150 times its face value during the previous six months. The rule also applies to SOE subsidiaries in which the parent central public sector organization owns more than 51 percent of the share capital.

According to the updated requirements, SOEs must think about paying an interim dividend at least twice a year or every quarter following quarterly results. According to the standards, all listed SOEs must pay interim dividends in one or more payments that equal at least 90percent of the anticipated annual payout. In September of each year, shortly after the AGM concludes, the last fiscal year's dividend must be paid. By giving SOEs greater operational and financial freedom, the updated rules aim to increase their performance and efficiency while also increasing the SOE's value and overall returns for shareholders. Additionally, it would allow more investors to take part in SOE's wealth development.

India is a union of states. The various states have their independent policy regarding the payment of dividends by SOEs owned and controlled by them. Table 1 depicts the dividend payment policy of the various states.

**Table 1: Dividend Payment Policy of the Various States**

<div class="fullwidthtable">

<div class="adjustbox">

max width=

| **States** | **Policy** |

|:---|:---|

| Assam | A minimum dividend of 20 percent on equity holding or 20 percent on profit after tax |

| Haryana | percent on paid-up share capital |

| Himachal Pradesh | percent on paid-up share capital |

| Karnataka | percent on shareholding |

| Kerala | percent of paid-up shareholding |

| Madhya Pradesh | percent on profit after tax |

| Maharashtra | percent on paid-up share capital |

| Odisha | percent on equity or 20 percent on profit after tax whichever is high. |

| Rajasthan | percent on profit after tax or 20 percent paid-up sharing whichever is lower. |

| Uttar Pradesh | A minimum return of 5 percent on the paid-up share capital |

| West Bengal | percent on profit after tax or 20 percent on shareholding. |

</div>

</div>

(Source: Budget Documents of the Various States)

**Dividend Management: Process, Mechanism, Reporting**

Several committees and bodies examined the various dimensions of dividend payments. These include the Investment Committee, Capital Markets Committee, Audit Committee, Independent Directors, Ex-officio Directors, Board of Directors, Administrative Ministry, Finance Ministry, and Department of Public Enterprises. The Audit Committee considers annual financial statements, periodic cash-flow projections, business plans, investment plans, or feasibility studies. Dividend payments are reported in the annual reports and websites of the concerned enterprise, reports of the administrative ministry, and the Annual Survey by the Department of Public Enterprises.

**Dividend Scenario in SOEs**

The state's expectations for increased dividend revenue are growing each year. SOEs have consistently met these expectations by providing substantial dividend payouts. Table 2 illustrates the dividend payment trends among SOEs.

**Table 2: Dividend Scenario in SOEs**

(Lakh Crore ₹)

<div class="fullwidthtable">

<div class="adjustbox">

max width=

| **Particulars** | **2017-18** | **2018-19** | **2019-20** | **2020-21** | **2021-22** |

|:---|:---|:---|:---|:---|:---|

| Total number of SOEs | | | | | |

| Number of operating SOEs | | | | | |

| SOEs under Construction | | | | | |

| SOEs not under operation | | | | | |

| Listed SOEs | | | | | |

| SOEs declaring Dividends | | | | | |

| Amount of Dividends declared | | | | | |

| Paid up capital | | | | | |

| Dividends as % of paid-up capital | | | | | |

| Net Worth | | | | | |

| Dividends as % of Net Worth | | | | | |

</div>

</div>

(Source: Annual Survey of Public Enterprises: 2017-2022, Department of Public Enterprises, Government of India)

**Cognate Group-wise Dividend Declared by SOEs**

The prominent sectors yielding dividends are related to coal, crude oil, minerals and metals, petroleum, heavy and medium engineering, power generation, power transmission, contract and construction and technology, and financial services. Table 3 shows the cognate group-wise dividend payments by SOEs.

**Table 3: Cognate Group-wise Dividend Payment by SOEs**

> (Lakh ₹)

<div class="fullwidthtable">

<div class="adjustbox">

max width=

| **Cognate Group / SOE** | **2021-22** | **2020-21** | **2019-20** |

|:---|:---|:---|:---|

| Agro-based | | | |

| Coal | | | |

| Crude Oil | | | |

| M&M | | | |

| Steel | | | |

| Petroleum | | | |

| Fertilizers | | | |

| Chemicals & Pharmaceuticals | | | |

| Heavy & Medium Engineering | | | |

| Transportation | | | |

| Industrial & Consumer Goods | | | |

| Textiles | | | |

| Power Generation | | | |

| Power Transmission | | | |

| Trading & Marketing | | | |

| Transport & Logistic Services | | | |

| Contract & Construction and Technology Services | | | |

| Hotel & Tourist Services | | | |

| Financial services | | | |

| Telecommunication & IT | | | |

| Grand Total | | | |

</div>

</div>

(Source: Annual Survey of Public Enterprises: 2017-2022, Department of Public Enterprises, Government of India)

A further probe points out that despite the quantum of dividend payments increasing substantially, only a few enterprises dominate the dividend payment scenario. This is in line with Table 3, which points out the stronghold of a few sectors such as coal, crude oil, minerals and metals, petroleum, heavy and medium engineering, power generation, power transmission, contract and construction and technology, and financial services. Table 4 depicts the top five dividend-declaring SOEs in this context.

**Table 4: Top Five Dividend Declaring SOEs**

> (Lakh ₹)

<div class="fullwidthtable">

<div class="adjustbox">

max width=

| | | | | | | | |

|:---|:---|:---|:---|:---|:---|:---|:---|

| | | | | | | | |

| | **Profit reported** | | **Profit reported** | **Dividend paid** | **Profit reported** | **Dividend paid** | |

| Oil & Natural Gas Corporation Ltd. | | ,44800 | | ,20200 | | | |

| Indian Oil Corporation Ltd. | | ,5050 | | ,9370 | | ,9200 | |

| Power Grid Corporation Of India Ltd. | | ,81200 | | ,82200 | | | |

| NTPC Ltd. | | | | | | ,11679 | |

| Coal India Ltd. | | ,78500 | | ,70300 | | ,71419 | |

</div>

</div>

(Source: Annual Survey of Public Enterprises: 2019-2022, Department of Public Enterprises, Government of India)

**Are Dividend Payments by SOEs Adequate?**

Although the quantum of dividend payments is progressively increasing, a question crops up: are dividend payments by SOEs adequate? The SOE companies tend to declare the highest amount of dividends coupled with certain corporate groups. They have given the highest dividend yield, which also led the entire outflow to a five-year high. It has been noted earlier that only a few sectors of SOEs dominate the dividend payment scenario with a handful of SOEs taking the lead. This situation is changing with the Government’s mandate of listing SOEs on bourses. However, the real question is not the quantum or the number of SOEs declaring dividends but the method of calculating dividends. In our view, SOEs have huge tangible and intangible assets. Therefore, dividends should be calculated based on the valuation balances of these assets.

**Dividend Payment Policies and Practices in Foreign Jurisdictions**

The OECD-World Bank Group study on dividend payment for SOEs presents a macro picture and brief case studies of select SOEs on dividend policies and practices (OECD/World Bank, 2024).

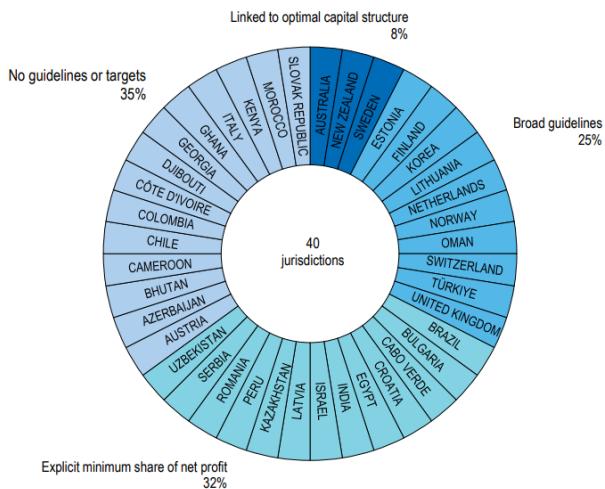

Figure 1 shows that different countries have different policies regarding dividend payments in SOEs. Certain nations adhere to minimum dividend payments. These legally required minimum payouts are based on net earnings. These nations include Chile, Bhutan, India, Brazil, Austria, Finland, and Italy. While minimum payment levels are specified in the majority of nations, a handful mandate that SOEs establish maximum dividend payout ratios. In many other nations, SOEs are obligated to pay dividends to match the dividend payout levels of private-sector businesses. Korea is included in this group of nations. In many countries, SOEs adhere to a predetermined annual schedule for dividend distribution, as exemplified by the United Kingdom, Norway, and the Netherlands. In certain nations, the preservation of a target credit rating serves as a valuable benchmark for achieving an optimal capital structure, which plays an essential role in shaping dividend expectations from SOEs. Sweden and New Zealand are notable examples within this category that successfully implement this approach for effective financial management in the SOEs.

**Figure 1: Typology of Dividend Policies and Practices in Foreign Jurisdictions**

<figure data-latex-placement="tbp">

<img src="https://doc.globaljournals.org/i55k3w_254298/ocr/media/image1.png" style="height:75.0%" />

</figure>

(Source: OECD/World Bank, 2024)

An intriguing picture emerges from the sectoral position of SOEs concerning dividend distribution policy. The payout ratio for SOEs in the power generation industry in Finland, Bhutan, New Zealand, and Bulgaria is over 80 percent. However, in Brazil, the Netherlands, and India, the payout percentage of these businesses is less than 40 percent. In the case of Colombia, the average dividend payout ratio for the extractive sectors is 80 percent, whereas in India, Austria, and Brazil, it is less than 40 percent. The average dividend payout ratio for SOEs in the extractive sectors ranged from 20 percent in Brazil to 160 percent in Norway. Switzerland, Norway, Finland, and Austria all had SOEs in the public utilities sector that paid comparatively modest dividends. The state owner may choose to declare SOE dividends in the annual aggregate report on SOEs, the government financial statement, or both. Budget planning and implementation reports, citizen budgets, and audited yearly financial statements of SOEs are a few examples of additional transparency channels. In conclusion, dividend policies aim to reconcile the perhaps conflicting demands of sufficient transfers back to the public budget and the SOE's financial stability.

**Conclusion and Way Forward**

A crucial component of SOEs' financial management is the payment of dividends. The central and subnational levels of SOEs have steadily changed their dividend policies. Dividend payments improve public resource allocation and corporate governance. In SOEs, dividends of all kinds have made their impact. For budgetary reasons, the State is becoming more and more dependent on dividends. The range of dividend distributions has been 18 to 30 percent of net assets. SOEs have strong procedures and systems in place for formulating and disclosing dividends. Coal, crude oil, minerals and metals, petroleum, heavy and medium engineering, power generation, power transmission, contract and construction, technology, and financial services are the main industries of SOEs that declare dividends. Policy changes in operations, strategy, and the market have the potential to increase dividends. More SOEs would be eligible to join the dividend club if the government mandated that SOEs list.

Different countries have different dividend distribution rules for SOEs. Nonetheless, the different nations might be divided into three groups: those that mandate yearly negotiations for dividend payout ratios, a group of nations where SOEs are directed by a maximum payout ratio, and those where SOEs are driven by a minimum payout ratio. Public utility SOEs pay modest dividends, whereas SOEs in the energy and extractive industries pay significant dividends. Dividend policies aim to reconcile the financially viable SOE with the possibly conflicting goals of sufficient payments back to the public budget.

It is necessary to reevaluate the way dividends are computed in SOEs, both in India and in other countries. Dividends may be computed on the basis of substantial investments in both tangible and intangible assets.

**Funding**

There is no funding support received for this paper.

**Competing Interests Declaration**

The authors declare that there are no financial, personal, or professional relationships that have influenced their work.

**Ethics declaration**

Not applicable.

**Data Availability Declaration**

The data support for this paper has been derived from the Annual Survey of Public Enterprises, Government of India, State Bureaus of Public Enterprises, and OECD Corporate Governance Factbook, for the various years.

Generating HTML Viewer...

Funding

No external funding was declared for this work.

Conflict of Interest

The authors declare that there are no financial, personal, or professional relationships that have influenced their work.

Ethical Approval

No ethics committee approval was required for this article type.

Data Availability

Not applicable for this article.

How to Cite This Article

Dr. Jyoti Pandit. 2026. \u201cDividend Payments Policies and Practices in State-Owned Enterprises in India and Foreign Jurisdictions: A Critical Analysis\u201d. Global Journal of Computer Science and Technology, Global Journal of Computer Science and Technology - G: Interdisciplinary GJCST-G Volume 26 (GJCST Volume 26 Issue G2): .

Explore published articles in an immersive Augmented Reality environment. Our platform converts research papers into interactive 3D books, allowing readers to view and interact with content using AR and VR compatible devices.

Your published article is automatically converted into a realistic 3D book. Flip through pages and read research papers in a more engaging and interactive format.

This paper critically examines the policies and practices governing dividend payments in State-Owned Enterprises (SOEs), with a focus on India and selected foreign jurisdictions. The study begins with a comprehensive literature review of dividend theory, exploring its traditional interpretations and the unique adaptations necessary for its application in SOEs, which operate under distinct mandates compared to privately held enterprises. By analyzing the theoretical underpinnings, the paper sets the stage for an informed discussion on the rationale, mechanics, and implications of dividend payments by SOEs. In the Indian context, the paper addresses key questions: why SOEs pay dividends, how much they pay, who determines these payments, and the institutional machinery governing such decisions. These inquiries are explored against the backdrop of recent trends, such as the record � 61,149 crore dividend payout by Indian SOEs in FY 2023-24, a 22% increase from the revised estimate. This upward trend underscores the growing fiscal significance of SOE dividends in India’s public finances and necessitates a closer examination of the factors driving these payments and their broader economic implications. The governance frameworks and decision-making procedures that support dividend payments in SOEs are also examined. It explores the relationship between corporate governance standards, board independence, and governmental directives, pointing out points of agreement and disagreement. In order to identify best practices and creative strategies that may be modified for the Indian context, the research also examines dividend payment regulations in a number of international countries. The paper concludes with actionable recommendations to enhance dividend payment policies and practices in Indian SOEs. These include strengthening governance frameworks, balancing fiscal imperatives with enterprise sustainability, and fostering transparency and accountability in dividend-related decisions. By integrating insights from domestic and international practices, the paper aims to contribute to the ongoing discourse on optimizing the role of SOEs in economic development while ensuring their financial health and alignment with public policy objectives. The paper offers a critical perspective on the strategic role of SOE dividends in national economies and provides a roadmap for policymakers and stakeholders to refine dividend practices in India’s SOE ecosystem. dividend dilemma dividend policy dividends practices in indian soes foreign jurisdictions strategic role of soe dividends

Our website is actively being updated, and changes may occur frequently. Please clear your browser cache if needed. For feedback or error reporting, please email [email protected]

Thank you for connecting with us. We will respond to you shortly.