I. INTRODUCTION

WHERE ARE WE AT PRESENT?--What has he done to wear so many scars?

Does he change the course of rivers? Does he pollute the moon and stars?(Bob Dylan) To put matters crudely, despite calls to advance the green transition and strong growth in renewables, fossil fuels remain dominant, contributing to of our total energy consumption.

Global energy demand rose by to 604 exajoules, a new record in 2022. While the growth rate has slowed modestly, this might have been due to specific factors. Still, global energy consumption has doubled since 1985.

Oil and renewables saw the largest increase in demand in terms of units of energy (exajoules), while natural gas and nuclear energy consumption fell in 2022. Fossil fuels' share of global primary energy demand fell slightly from to , while renewables' share rose from to .

The path to decarbonizing the world remains a long one. With global energy demand expected to rise sharply in the years ahead, to enable emerging nations to develop, we should see significant investments across all energy sources. In all, this should enable attractive, multi-decade investment opportunities.

Meanwhile, calls to advance the green transition supported the growth in renewables, which rose in 2022, slightly above the annual growth rate of over the last 10 years. As a result, the share of renewables in primary global energy consumption rose from to a new record high of . Renewables will continue to expand at a strong pace over the coming years, though from a relatively low base compared with traditional sources. Accordingly, fossil fuels remain king for a while and make up the lion's share of our thirst for energy, accounting for nearly of the global demand.

As a result of higher absolute consumption of fossil fuels last year (up by 2.3 exajoules), energy-related carbon dioxide emissions (from industrial processes, flaring, and methane) rose to a new record of 34.4 gigatons of CO2 equivalent in 2022. Emissions rose the most in Indonesia, India, the US,

Clearly, the progress in renewables is not making a dent in CO2 emissions, and a growing consensus is slowly emerging that the decarbonation race is not just about expanding renewables, but embracing risk and resilience consideration in climate change policy formulations, embracing proper feedback loops from civil society to ensure that there is a proper response to market demands, and building the necessary governance arrangements that are crucial in any "structural" changes to ensure that all interests are properly represented and responded to, and generate genuine sustainable solutions for all.

HOW DID WE GET HERE?-History does not repeat itself, but it rhymes (Attributed to Mark Twain)

Every so often, throughout history, humanity touches the seeming limits of development, leading to crises that forces us to rethink and change the way further growth and wellbeing can be achieved. This happened with population growth, with the attendant preoccupation on how limited agricultural output could accommodate the growing demand for food, and associated claims on limited agricultural land. The agricultural revolution and the ensuing productivity increase capable to surpass population growth, in the endenabled further enhancement of wellbeing for a growing population.

This seems to be happening at present again, when growing economic activity appears to be hitting the limits that nature is able to accommodate. As enhanced economic activity has hitherto been underpinned by growing energy use to replace human and animal toil for small engines, the carbon emissions of such equipmentisaccumulating in the atmosphere to the point that it is producing global warming threatening human existence in the longer term.

The Paris Agreement on climate change aims at precisely limiting global warming to no more than of pre-industrial levels by building a decarbonized economy by mid-century.

Such goal implies investments of at least US$16.5 trillion, and a profound transformation in production and transportation practices, investments in renewable energy, and other actions never seen to date.

Of course, no political, social or moral achievement of this magnitude or complexity is without formidable obstacles. There are vested interests to be

confronted, attitudes to be changed, resistances to overcome. The problems are immediate, the ultimate goal frustratingly far away. So, the issue hinges on how to reconcile these seemingly conflicting strands.

The crisis triggered in Europe by the suspension of Russian gas supply, together with decisions to curb production of hydrocarbons, illustrate such conflict and, more importantly, the disconnect of the actions taken with geopolitical realities. These have triggered price increases to record levels, and a gap between the goals and achievements of the Paris agreements. A transition towards the agreed objectives will demand a decidedly more strategic and coherent approach. Just to mention a couple of real-life constraints, this will require special attention to:

- Coal-dependent economies, such as India and South Africa – which generate more than 70 and of their electricity, respectively, from low-cost coal, with serious social and economic repercussions that will need more nuanced approaches to transition than those applied to date;

- Countries with important power generation facilities that are in energy-intensive and harder-to-abate sectors, which are difficult to decarbonize, such as mining and extractive industries, which constitute the mainstay of a good number of emerging economies.

- Any effort of this nature will require important human and financial resources to make progress within the absorption capacity of each country. Forcing ambitious and distant goals, or discouraging certain technologies with arbitrary regulations will not generate progress, and may even generate civil resistance and associated instabilities.[2]

THE PEBBLES ON THE ROAD--Success is stumbling from failure to failure with no loss of enthusiasm(Winston Churchill)

The energy sector, and society more generally, face significant challenges as we navigate the transition to a low carbon energy system. That will require understanding and judgement, both of which will have to rely on empirical data and analyses that are usually presented to justify political postures to depict advancement in the global debate on the issue.

In fact, if one takes the goals and pledges agreed at the proceedings of Conference of the Parties (COP) meetings of the UN Climate Change Conference, one could easily conclude that all what is needed is to live up to the commitments to achieve the goals of a low carbonized economy. That said, the projections have an inevitable promotional aim to meet the political imperatives agreed at original Paris agreements, and are perilously dependent on underlying assumptions. Chief among them isconomic growth (and associated energy demand), availability of financial resources, future technological development, which may not

necessarily take place – at least at the pace assumed in the documentation underpinning COP meetings. In this connection:

First; a serious focus is needed on such assumptions, which have yet to be supported by detailed plans or executed to move them from studies and proposals to execution, specifically concerning economic and affordability aspects, their organizational and governance implications, as well as the energy coverage that will be provided. Nor will execution be trivial, as it would require careful balancing of shorter- and longer-term risks that can make all the difference between viability, sustainability and ultimately the support that such programs among energy consumers — be itcivil society or enterprise sector.

Second; renewable technologies are heavily location-specific and weather-dependent, and thus tend to have lower load factors than traditional sources,

thereby requiring a proper energy base to provide backup from regular resources, such as gas fired generating facilities to provide low cost relatively limited CO2 emitting facilities. For the time being, and until the intermittent energy supply can be overcome due to weather related conditions of most renewables, power sector grid integration will be required through transmission investments over longer distances to link areas with adequate wind regimes or solar radiation, with household consumers and industrial areas.

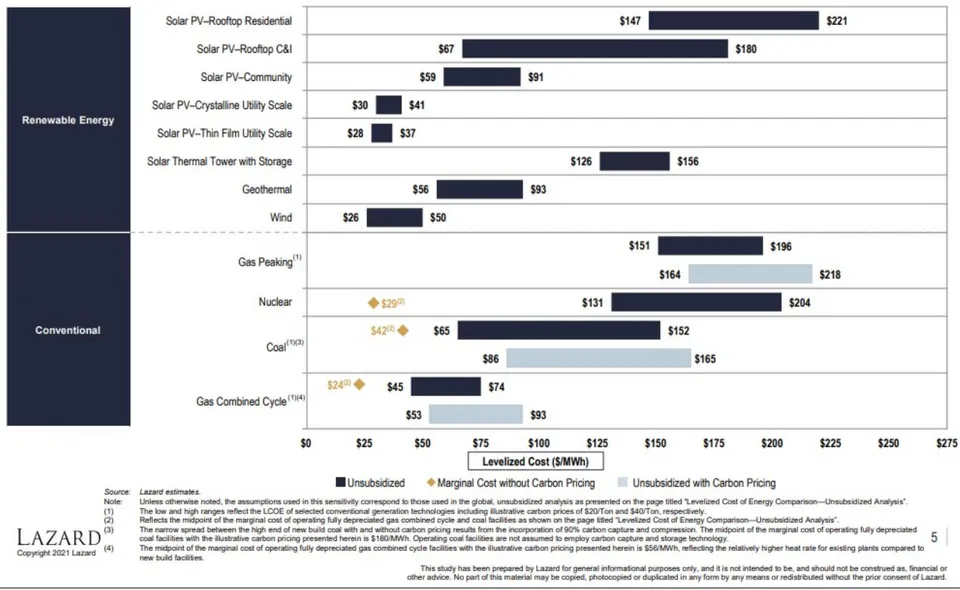

Third; while, there is no question that the economic viability of renewables has improved over time, and its costs are currently broadly "in the ballpark" of traditional sources, if adjusted or levelized for carbon emissions, as can be seen in the table below:

LAZARD

LAZARD'S LEVELIZED COST OF ENERGY ANALYSIS-VERSION 15.0

Levelized Cost of Energy Comparison—Sensitivity to Carbon Pricing

Carbon pricing is one avenue for policymakers to address carbon emissions via a market-based mechanism; a carbon price range of 40/Ton of carbon would increase the LCOE for certain conventional generation technologies to levels above those of onshore wind and utility-scale solar

Fourth; consider able work will be necessary to make renewable sources more reliable, such as energy storage (which is overly expensive for the time being), geothermal options, requiring proper risk intermediation vehicles to bridge the mining/ geological with the power generation risks, the up scaling of run-of-river facilities, etc. to properly complement the capacities of existing and foreseen

renewable facilities. In all, though, this situation will require for the time being traditional energy generating facilities for back-up and/or supplement the energy base of each country.

Adding such investments to overcome the constraints of current renewable sources, there should be no mistake: all indications are that low-cost energy and associated implications on economic growth,

appear to be a thing of the past. Accordingly, if this is the direction that energy sources are likely to emerge, a future decarbonized era will require an increasingly efficient use of more expensive energy sources, if further economic development is to be secured.

Beyond the possibility of any slippage decarbonization plans, the International Panel on Climate Change (IPCC) reports makes clear that all pathways that limit warming to may inevitably depend on some carbon removal. Accordingly, beyond deep emission reductions, taking carbon out of the air will be necessary. This will require natural solutions (such as forestation) as well as nascent technologies that pull carbon dioxide directly from the air, as is being experimented in several countries.

WHAT WILL IT COST, AND WHO WILL PAY?-People reach their pocketbooks without much grace(popular saying)

Of all issues, revamping of the energy matrix to replace its reliance on fossil fuels for renewables is perhaps the biggest challenge to meet the Paris goals. Above all, the orders of magnitude are such that the matter will be inherently controversial, as competing claims on funds will require discerning attention on priorities, economies, organizational requirements with far-reaching consequences for society. To put matters in perspective, two points merit special attention:

Public Resources. Capital spending on physical assets for energy and land-use systems in the net-zero transition to 2050 may amount about 9.2 trillion per year on average, an annual increase, or as much as 2.4 to 2.7 billion a year range in the 2000's. This in itself highlights the increasing effort that will be needed in resource mobilization, price increases, and other such actions, as fiscal budgets are already overstretched in current and foreseen economic conditions. On this scale alone, the WB and multilaterals are puny. Allowing them to grow to fill the gap, without considering their effectiveness, may well be an unbridgeable stretch. So, the role that the WB and similar institutions, must be in the main catalytic (and inevitably marginal in terms of financial resources). Accordingly, greater focus will be required on pricing, taxation arrangements, and generation of incentives for such investments. This is a dramatic change from what the WB and other multilaterals have been doing, which in turn makes one wonder whether they are fit in their current form for the proposed job.

Private Sector and Civil Society. Governments and official institutions are struggling to deal with the issue, and if such trends continue, the agreed goals will not be met. A profound transformation in

production and transportation practices, investments in renewable energy, fundamental recasting in the production of raw materials upstream and pricing policies are needed if decarbonization efforts are to succeed. As in other transformational efforts in the past, climate change will have to be solved by innovation and entrepreneurship, more than by multilaterals, governments and politicians. As throughout history, private enterprise cognizant of societal demands, and innovation will be required for transformational approaches. Any approach to the issue will ultimately have to rely more heavily on them. Official institutions may have to recast their approaches from a rhetorical and normative to a more open and enabling focus to problem-solving.

Accordingly, actions must be grounded on five points for a realistic chance of success:

- At present, more than 70 countries, accounting for more than 80 percent of global CO2 emissions and about 90 percent of global GDP have put net-zero commitments in place, as have more than 5,000 companies, as part of the United Nations' Race to Zero campaign. Yet even if all the existing commitments and national climate pledges were fulfilled, estimates suggest that warming would exceed the agreed above preindustrial levels. Moreover, most of these commitments have yet to be supported by detailed plans of action. Nor will execution be trivial, as it would require careful balancing of shorter- and longer-term risks. Today, while the imperative to reach net-zero is increasingly recognized, the issue is not solved. This should not be surprising, given the scale of the task at hand. Achieving net-zero emissions by 2050 would entail fundamental transformation of the global economy.

- The estimated capital spending on physical assets for energy and land-use systems mentioned above highlight the increasing resource mobilization efforts that will be needed, and ultimately the changed role that multilateral development banks must play in catalyzing the resource requirements over and above what official institutions can do to deal with the issue, including focus on pricing, taxation arrangements to mobilize resources and generate incentives for such investments.

- The macro projections prepared hitherto inevitably imply a significantly up scaled financial effort among many players to properly anchor investment plans. However, taking these projections as top-down targets would be akin to “throwing money at the problem”. The issue cannot be reduced to investing in a changed energy matrix to reduce carbon emissions. This is unlikely to occur, given the varying institutional capacities and other constraints in the countries concerned. Instead, an

effort will be required to involve stakeholders, bottom up, to identify the market demands to properly respond to them, including issues of affordability, energy security and coverage to avoid costly energy crises, and distorting subsidies of the past.

- To build up such frameworks, major banks and other international financial bodies may have to establish common practices and frameworks (in a manner akin to the preparation of the Equator Principles), perhaps sponsored by the World Bank to exchange experiences, streamline existing practices to evaluate investments involving climate implications, risk sharing and/or other

Energy consumption by fuel

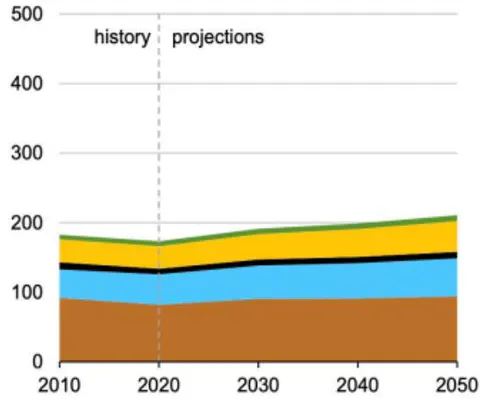

Delivered energy consumption by fuel, OECD

quadrillion British thermal units

arrangements to facilitate entrance of new players and resources to upscale the investment effort.

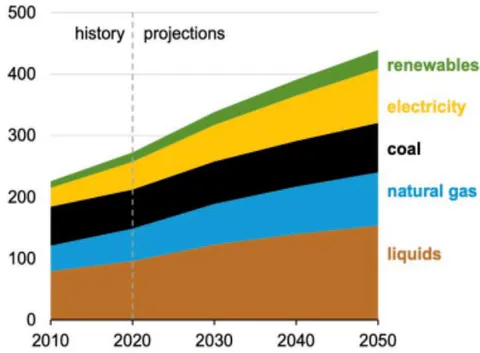

- The focus will have to concentrate in the main on emerging economies, where the bulk of economic growth, energy demand and CO2 emission growth is likely to take place, and thus the overall effectiveness of the effort. While OECD countries have essentially kept current levels for the past 10-15 years, non-OECD economies have increased some from similar levels at the beginning in the early 2000's — and if past trends continue, as is likely, non-OECD consumption levels will more than double those of developed countries by mid-century—as seen below:

Delivered energy consumption by fuel, non-OECD

quadrillion British thermal units

IEO2021 www.eia.gov/leo

Accordingly, energy transition and carbon emissions will hang largely on what will happen in emerging economies (particularly Asia), which merits focused attention and response to achieve significant decarbonization goals while meeting developing needs of those economies, where resource and funding mobilization constraints are the greatest.

Given the magnitude of the efforts involved, there is a tendency to seek top-down government-driven efforts to address the investment requirements. However, such efforts cannot rely exclusively on government or official institution through increasing targets and guidelines, clearance of environmental mitigation programs, tracking compliance arrangements. While they can be bureaucratic and complex to manage, they can help in some circumstances, particularly when institutional capabilities are strong, when decommissioning or complex repurposing existing investments are needed. On the

other hand, they can be problematic where institutions and accountability are weak, and thus pose a particular challenge in emerging economies.

Much of the effort may be needed in strengthening the policy environment, particularly for investments. Other things being equal, if incentives are right and the business is profitable, funding for investments is bound to flow, and carbon mitigation is going to take a hold — there are, of course, other underlying prerequisites (such as the existence of capital markets elements, an investment-friendly policy context, etc.)

HOW ARE WE DOING; WHERE ARE WE FALLINGSHORT?-Doubt is the father of invention (Galileo)

It is always helpful (though at times sobering), to look at the goals that need to be achieved and the actual record of performance, to get a sense whether

there is meaningful progress towards stated goals, the underlying quality of the programs that have been put in place, the way they are carried out and/or grounded on viable diagnoses of the issues being addressed.

Seen in that light, the Conference of the Parties (COP) tracking global carbon emissions basically

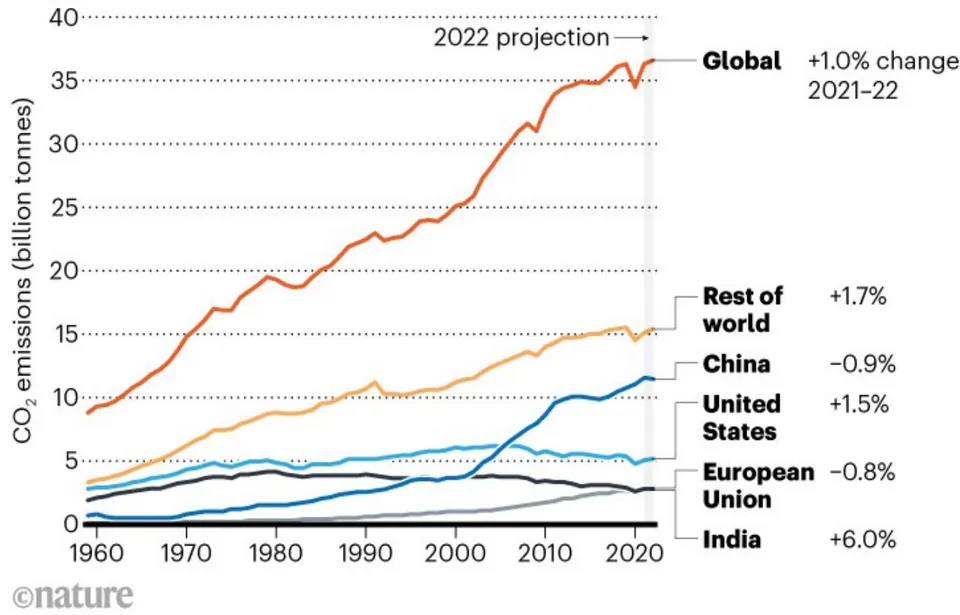

indicate that carbon emissions remained basically steady at some 35 billion metric tons over the last decade, which of course compares favorably with the increases over previous decades (see graph below), but is a far cry from reductions needed to meet the Paris agreement goals.

EMISSIONS UPDATE

After a dip in 2020 owing to the COVID-19 pandemic, global carbon emissions rebounded — and then some. Researchers predict a increase in worldwide emissions in 2022. India contributed strongly to that, with a predicted increase.

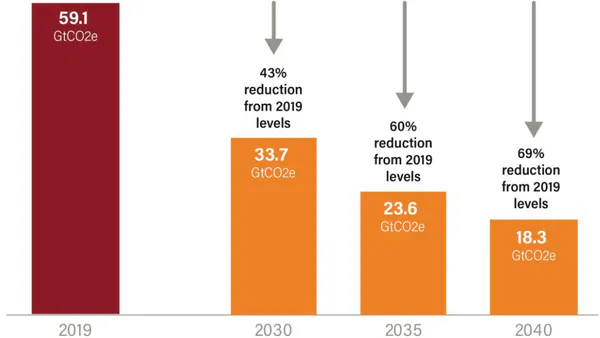

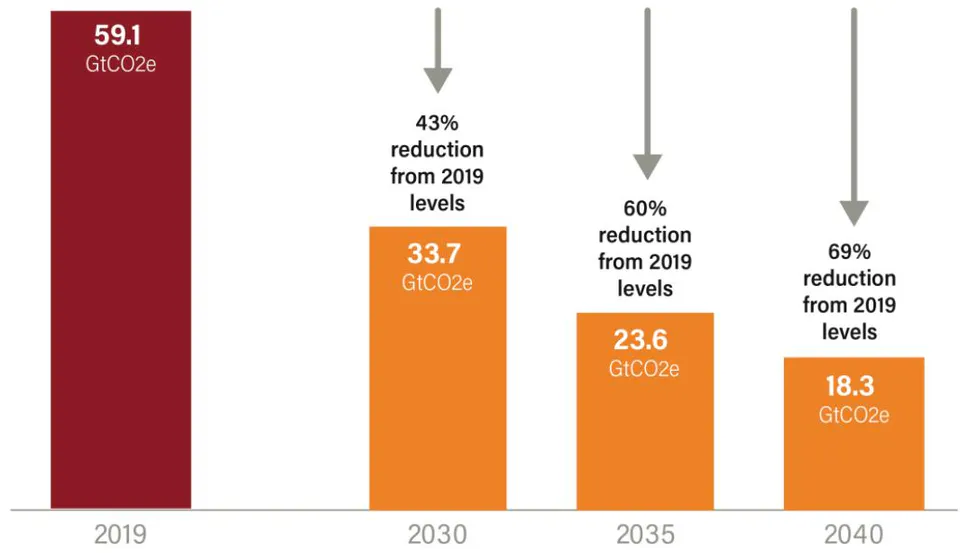

This in itself should alert us that what is required is nothing less than a fundamental change in the energy matrix. All this will call for much better performance in carbon reduction: than has been achieved so far, that only substantial Greenhouse gas (GHG) emission reductions to keep the 1.5C goal within reach, as can be seen in the graph below

GHG emission reductions needed to keep within reach

WORLD RESOURCES INSTITUTE

So far, much of the changes in GHG emissions have been related to overall economic activity, rather than outcomes of carbon reduction policies. In 2020, for instance, global emissions from fuel combustion showed an unprecedented decline of nearly as the COVID-19 pandemic slashed global energy demand.

In all, though, fossil fuels still represented of the total energy supply globally, with oil comprising , followed by coal and natural gas . Global emissions from fuel combustion were dominated by coal , followed by oil and natural gas . Under these conditions, three areas merit special attention.

First; the record seems to suggest that decarbonization goals may well be within reach in the more developed economies, which are increasingly moving towards service and value-added activities, often-times shedding industrial activities to emerging nations. Levelling of overall emissions have thus largely taken place in the US and the EU, and a more effective effort will be needed in changing the energy matrix to achieve the reductions envisioned in international agreements.

The effort will be more complex, and thus require more fundamental actions in emerging and industrializing countries, particularly in China and India, where emissions are still growing at a fast pace, given their continuing industrialization and integration to monetized economies.

Second; the goals and climate actions that are agreed tend oftentimes be taken at levels far removed, if not actually delinked, from "real life" realities on the ground, be it citizenry or industries.

Second; this has led to "solutions", without the slightest concern or knowledge of what final consumers want or need. No technical fixes, or push for certain aggregate goals is going to be effective or sustainable, unless it provides an adequate response to 'consumers' needs, a proper transition, and enterprises have a clear framework and incentives to operate and invest. In the end, it is at the kitchen table and the tightening purse strings that are the real drivers shaping emerging political alignments. It is difficult not to see the glaring gap between goals and achievements in the energy and environment debate at governmental levels, with the more here-and-now

concerns on energy affordability, security, and sustainability at household levels – and the tensions that are being built in the streets and public arena throughout much of the world.

Third; in view of the foregoing, given institutional weaknesses in emerging economies, top-down vehicles for planning, regulation and execution can be particularly vulnerable to imprecisions, discretionary actions that open conditions for corruption, and time-consuming processes that oftentimes exceed periods of execution. Accordingly, some form of pricing will be helpful to generate the incentives to attract resources to where they are needed. As long as externalities are not priced, in effect giving them out for free, it is difficult to "bring home" the impact of inaction. There are many ways of pricing emissions — from pricing them directly, instituting taxes to act as proxies for the cost of emissions, instituting industry standards akin to the Equator Principles, establishing various forms of regulations ranging from direct monitoring and public oversight all the way to accounting conventions requiring enterprises to recognize in contingent liabilities the environmental damage they may generate. Each of these options have trade-offs and institutional requirements that need to be assessed before implementation.

MANAGING THE TRANSITION--there is always another taller mountain; 總有一座更高的山 (Chinese proverb).

It has been over 30 years since the UN Framework Convention on Climate Change. Since then, numerous Agreements have been reached (including the historic 2015 Paris Accord), 27 COP meetings have taken place, pledges made, reports written, and yet little tangible evidence of progress, as far as one can tell, can be seen in the climate change agenda and results.

Various documents, including the recent IPCC Experts' Report unequivocally confirmed that we are already seeing negative impacts of rising sea levels, droughts and extreme storms. Much more progress is needed to "move the needle", particularly in the power sector, which absorbs more primary energy than any other sector. Leaving political correctness and finer points aside, the paucity of progress should be a warning that something is significantly amiss.

This paper is an attempt to point at some obvious issues: the inability and bureaucratization of oversight institutions in effectively tracking and supporting the necessary corrective actions; the lack of enabling conditions to mobilize human and financial resources for proper investments in this area; the enormous costs and risks involved in the face of binding fiscal constraints, overstretched indebtedness that leave little room for surpluses for investments in the climate change agenda; the need for much better understanding of the cyclical nature of economic and

associated issues affecting proper policy-making for climate and economic management issues.

While the challenge is immense, it is not un surmountable. It requires common sense, which is the less common of the senses, and a sharp focus on actions that respond to societal needs, including development, and thus incentives and accountability to produce results.

So much of the climate change debate has become deeply emotional and inflammatory, rather than open-minded and probing. The point of this paper isn't to take sides in what quite often are complex disputes. The lack of progress should in itself, however, be a warning that we are on a trajectory that is far from decisively correct.

Fighting global warming requires a broader and more nuanced understanding of how different sectors interact with each other. Merely adopting new environmental laws, creating new commissions or environmental regulatory institutions, pushing for particular technological fixes, or launching another 'campaign' will not get the job done. Judging by the record so far, it appears rather unlikely that the goals that have been agreed are going to be achieved. Much can be accomplished with existing technologies. However, without game-changing approaches towards policy, scientific or technological, and financial dimensions, the climate challenge is unlikely to succeed. This will require tackling these issues more specifically:

II. THE POLICY GAP

As nations look to lower their emissions, they are simultaneously facing increasing energy demands of a growing global population and increasing economic activities, particularly in emerging countries. Reconciling both objectives requires a policy framework that properly integrate civil society and industry concerns – i.e., this cannot be seen as a race to renewables, but race to reduce carbon emissions across many fronts. Investment trends in recent years, however, have contributed to the situation we see today. Unbalanced and underinvestment in the sector inevitably lead to price hikes. For too long, the sector has not developed the resources and back-up to enable it to respond to changes in supply routes and upticks in energy demand.

For all the seductive talk about the new economy and technological development, one cannot easily overcome the gravitational pull of traditional technologies (including the much-maligned combustion engine and associated fossil fuels), whose sunk costs make them highly competitive when compared with the resources and risks in new production platforms. Resistance to new approaches cannot be belittled, since their increased costs and reliability inherent in

emerging technologies need weighing against their risk implications on economic development, which are particularly challenging in lower income countries.

Global energy policy discussions in recent years have focused on the importance of decarbonizing the energy system. The market (particularly civil society and industry) reminded though that this transition that it also needs attention to affordability, security, and sustainability that energy systems need to address coherently, rather than solely as an environmental or decarbonizing objective per se.

In the after light, over-reliance on any one kind of fuel or supply route leaves nations and the global market vulnerable to disruption, and that is what we have seen in recent years. Underinvestment in traditional energy (and inability of renewables to provide the required energy base to respond to increased demand, or provide reliability under changing weather conditions) has dragged global energy security and put strain on the energy transition.

Renewable forms of energy will play a growing role, but oil and gas are likely to remain an essential part of the energy mix for some time to come. While this may be an uncomfortable reality, it remains an undeniable fact, which recent years have brought to light. We cannot make a success of this transition if we neglect the foundations upon which industries stand – until the energy matrix has been radically changed, which inevitably will take long years to develop.

In part this is a symptom of a larger dysfunction -- the failure of policies to properly link incentives and emerging concerns on externalities, so that investments and consumption on the one hand, and supply response, on the other, respond to the delivery of public goods and private services demanded by society.

If international experience has anything to teach us, in the end each country will need to develop its own institutional infrastructure (for energy, transport and other sectors) to have a strategic framework on environmental concerns to face the development challenges of the years ahead. In doing so, however, oftentimes countries have inadvertently introduced competing and duplicative policies: operating at the national, regional (EU for example) and the international levels (leading, for example, to setting up over 15 different climate change ODA funds in the 2015's). The establishment of distortionary pricing policies and subsidies, led to difficult to reconcile conflicting signals, such as earmarked taxes on carbon trades to fund adaptation: taxing one public good (that governments want more of) to pay for another, and the establishment of earmarked funds to overcome distortions created by some funds or subsidies.

Governments will thus need to remain vigilant to avoid developing institutionally-intensive arrangements in institutionally-weak environments, since "institution-building" mentioned in the Paris Agreement is a long

and difficult road. Wherever possible, policy frameworks must enable key economic actors to interact organically, without too many constraints and avoid complicated regulatory systems (where duplication, offsetting incentives, etc.) all too often become a constraint to investment and development.

The rule should be to minimize the rules, and use pricing where at all possible, while allowing legitimate additional costs of compliance to environmental standards to be recouped through output prices — thereby avoiding energy development paths becoming costly and complicated.

From an energy perspective, recent disruptions to Russian energy supplies and consequent energy shortages seem likely to have had material impact on the energy system. The desire to bolster energy security by reducing dependency on imported energy (dominated by fossil fuels) by developing domestically produced energy, coming from renewables and non-fossil energy sources, suggest that the conflict may well accelerate the pace of energy transition.

On the other hand, the scale of the economic and social disruptions associated with the loss of just a fraction of the world's fossil fuels also highlighted the need for the transition away from hydrocarbons to be orderly, such that the demand for hydrocarbons falls in line with available supplies, avoiding future periods of energy shortages and higher prices.

In this regard, the lack of foresight, the low energy security of existing energy matrix, and the consequent crisis triggered by the conflict in Ukraine have prompted the 51 largest economies to double support for fossil fuels to almost $700 billion in 2021, and even larger amounts in 2022 -- mitigating energy price increases for consumers, and generating incentives for increased fossil fuels supply to achieve a quick response to overcome the crisis. This undermined removal of inefficient and distorting subsidies, undercutting environment friendly policies and pledges.

The consequent International Energy Agency (IEA) finding of 42 economies noted that consumer support increased to $531 billion in 2021, more than triple their 2020 level, driven by the surge in energy prices. Careful and planned investment in both renewables and hydrocarbons is thus essential for an effective energy transition.[5]

One hopes that with greater transparency on massive subsidies and associated misallocation of resources, corrective action could be seriously considered to get proper resource allocation towards the energy transition and the climate change agenda. Hiding in plain sight, the missing trillions for climate change are highlighted in a World Bank report, Detox Development: Repurposing Environmentally Harmful Subsidies. It shows the extent of global subsidies and the opportunity offered by repurposing them. Compared to what countries pledged in the Paris Agreement, every

year, they spend about six times that amount to subsidize fossil fuel consumption, which in turn exacerbates climate change, toxic air pollution, inequality, inefficiency, and mounting debt burdens. Redirecting these subsidies could unlock at least half a trillion dollars per year towards more productive and sustainable uses.[6]

III. THE TECHNOLOGICAL GAP

On the societal elements, it may be appropriate to recall that many, if not most, of the approaches used in technological approaches are a relic of a bygone era. The tendency to choose particular approaches (i.e., solar, wind or other) are grounded on the assumption that Authorities know better what is good for people, and that environment benefits accrue to the direct user, or their neighbors. Yet, CO2 emissions are invisible, and impact in the seemingly distant future. They actually go to the atmosphere, thereby affecting the global or worldwide (rather than solely to local) community.

Not surprisingly, there is limited consciousness or genuine groundswell constituency for CO2 emission reductions, and limited understanding of the impact or options, such as reducing waste, cutting meat consumption, taking fewer round-trip flight, reducing home electricity usage, living in car free environments, and/or purchasing carbon offsets. Actually, all research surveys done on the subject reveal that people "don't have much of a clue".

The introduction of renewables that generate energy without fossil fuels, and avoiding carbon emissions, makes intuitive sense. In practice, though, this approach is not without its share of constraints – chief among them is their heavy dependence on location and climate conditions, thereby becoming useful if properly backed up by traditional sources, so that they can deliver reliable energy supply(during evenings, in bad weather conditions, etc.), particularly for industries that require high load factors for their production. In fact, we cannot talk about solar or wind without also talking about its land-use or coastal areas and grid implications, the reserve capacity that will be needed to overcome the intermittent nature of most

renewables, and the investments needed to overcome such constraints, which are an inherent part (and cost) of the seemingly “free” feedstock of such options. In the end, making informed and well-grounded decisions will have to be rooted in making the invisible, visible.

By the same token, decarbonization efforts in transportation via electronic vehicles (EVs) will not cut emissions to zero by itself – not until we have also decarbonized the steel used to make them, and the electricity that powers it (which otherwise would just move the emissions upstream from the refilling stations to the power generating plants). But it at least holds the potential to be a significant part of solution, if properly addressed through the supply chain – though, again, with their attendant share of costs.

Assessing actual decarbonization impacts thus need to focus on the full supply chain. Inputs required to produce low-emitting power generating facilities, require large quantities of rare earth elements, critical minerals and metals whose production comes from art-to-abate mining activities. To achieve the agreed global temperature goals will require a major uptake of wind turbines, solar panels, electric vehicles (EVs), as well as storage batteries — all of which are made with rare earth elements and critical metals, which include 17 rare earth elements, the 15 lanthanides plus scandium and yttrium. Elements such as silicon, cobalt, lithium, and manganese are not rare earth elements, but are critical minerals that are essential for the energy transition.

The demand for rare earth elements is expected to grow 400-600 percent over the next few decades, and the need for minerals such as lithium and graphite used in EV batteries could increase as much as 4,000 percent. Most wind turbines use neodymium-iron-boron magnets, which contain the rare earth elements neodymium and praseodymium to strengthen them, and dysprosium and terbium to make them resistant to demagnetization. Global demand for neodymium is expected to grow 48 percent by 2050, exceeding the projected supply by 250 percent by 2030. The need for praseodymium could exceed supply by 175 percent. Terbium demand is also expected to exceed supply. And to meet the anticipated demand by 2035 for graphite, lithium, nickel, and cobalt, some analyses project that over 380 new mines would be needed.

Similarly, copper is bound to become a foundational metal for the energy transition, electrification, and global growth, and demand may well double by 2035. According to some estimates, there will not be enough supply to meet the demand of Net-Zero-Emissions by 2050. At current levels of technological development, most mining activities constitute hard-to-abate sectors, and considerable technological work will be needed to ensure that mining can reduce emissions so that the supply chain, in its entirety, can respond to the CO2 emission reduction goals.

This is a tall order oftentimes overlooked. Supplying these vast quantities of such minerals in a sustainable manner will be a significant challenge, but scientists are exploring a variety of ways to provide materials for the energy transition with less harm to people and the planet than currently possible with current level of development.

Seen in this light, as already alerted by some IPCC members, greater attention should be focused on options being promoted that are grounded on "technological optimism", which require better scientific validation in terms of their full-cycle implications. An example that illustrates his point on how biodiesel allegedly lowers emissions, when it actually could generate up to twice the CO2 emissions when considering the deforestation necessary to produce the soy for fuel production.

Finally, on technical choices and the pacing of reforms, there is a lot to be learned from the various experiences being instituted around the world. It would be most helpful to review such experiences in terms of the impacts, cost, institutional requirements, etc. so that learning and optimum investment patterns can be embedded early on in ongoing efforts taking place worldwide.

In Germany, for instance, the widely applauded fast transition into a green economy and CO2 neutrality by 2050 or even 2045 will be extremely expensive. A study by Prognos for the public bank KfW estimates that it will take private and public investments in the amount of some 5,000 bn EUR in order to reach climate neutrality by 2045. It will be an open point for discussion why cheaper solutions for climate change adjustment or CO2 abatement abroad may not be pursued.

In Germany, the present transition of energy production as fixed by laws is loaded with problems, as there must be a replacement of the power generation facilities running on uranium or coal (hard coal and lignite), which are in an accelerated shut-down process. The only viable alternative is an interim switch to natural gas as a back-up energy for electricity generation; notwithstanding the increasing power demand from digitalization, E-mobility, and conversion of heating systems, there is a need for at the least an additional 70 GW of gas power. This increases the dependence on natural gas imports.

IV. THE INFORMATIONAL GAP

It is difficult not to see the gap between actions to address environmental problems and energy transition and the absence of tangible results. Ultimately, the problems seem to center on the fact that actions can only be taken at the local or national levels, and the implications ultimately yield at the global level. In other words. As long as the companies or individuals) that generate greenhouse emissions do not see the costs and obtain the benefits that they generate, it is unlikely

that the corrective action will be proportional to what is needed. No amount of regulatory enforcement or international agreements can easily overcome this basic gap.

Trying to "manage" this disconnect via the regulatory route has inevitable constraints, particularly when costs and benefits occur throughout supply chains, which cross a multitude of sovereign nations. Trying, for instance, to reduce emissions by electrifying transportation through electric vehicles (EVs), even within the confines of a single country, is bound to have its limits, as long as power generation is not decarbonized as well. Otherwise, emissions are only being transferred "upstream" to the power sector, where the resulting increased demand from EVs may well be met through increased fossil fuels-based power generation.

Furthermore, given the enormous scale of compiling emissions figures, which influence environmental policy and investment, particularly in solar energy, given the difficulties in collecting information from China. In fact, some sources, estimate the footprint of solar PV to be higher than current models used by the IPCC, even when compared to natural gas, with carbon capture.[8] It is thus hard to assert in a reliable fashion how much solar PV installations will reduce CO2 emissions.

In the absence of reliable primary-source or verifiable data, it would not be unreasonable to assume that China's competitive advantage in solar technology, with which they have conquered a large part of the world market, does not lie in a new innovative technological process, but rather in the same factors that the country has always used to overcome the production costs of Western countries: cheap coal power, massive government subsidies for strategic industries, and low cost human labor operating in poor working conditions. Similarly, when assessing the interaction between risk and resilience in the face of climate change, analysts are similarly hampered by tracking though accounting practices that track the symptoms, rather than the root causes of the of climatic calamities.[9]

V. THE FINANCING GAP

Bearing in mind the cumulative climate, health, energy and inflation crises have put on advanced and developing economies alike, the accumulated fiscal deficits and growing public debt have led to growing calls for a fundamental rethink of how the public sector supports and system for multilateral development finance should adjust to respond to increasing demands, particularly in low- and middle-income countries.

Hitherto, much of the focus of discussion and policy-making has centered on public sectors around the world, and as a result, efforts have centered too

much on overstretched governments that have hardly the wherewithal and resources to appropriately address the climate change issues in an effective manner. Support has unfortunately been rather ad hoc and reactive to the crises as they developed, particularly in Europe, as described above.

In light of inevitable limitations and conflicting claims on public sector resources in developed countries, the Multilateral Banks (MDBs, particularly the World Bank) must step up and revisit more aggressively their specific role in closing the climate and energy transition finance gap – both directly, and supporting much needed enabling investment and resource mobilization conditions. This would need to be done by “leveraging” more proactively their other essential roles in provision of development finance, up scaling their relationships with other institutions providing private and public climate finance, including the IMF's Resilience and Sustainability Trust (RST), and mainstreaming their technical assistance and policy advisory role to borrowing countries.

To some up, the scale of global financing required to meet mitigation and adaptation needs is vast, to say the least: 6 trillion for repurposing finance that would otherwise go to high carbon assets; $3 trillion per year for new spending in incremental capacities.

However, the climate and energy transition finance situation in many low income and emerging economies remains extremely serious. Much of the finance in such countries will be needed for adaptation infrastructure. However, many of them face compelling and competing claims for public finance to meet education, health and social needs. They also have low tax raising capacities with low revenue to GDP ratios, and the availability of both public and private finance from global sources is limited by the already high, and rising sovereign debt distress. Today of low-income countries are already in debt distress, while a further are at high risk of debt distress.

Multilateral development banks' contributions can be leveraged by: (i) providing technical and analytical support for improving the overall policy and technical context for marshaling climate finance; (ii) lending directly to sovereign governments to improve policy and finance individual projects and improving the environment in which other publicly or privately financed projects can take place; (iii) integrating their respective private sector arms – such as the International Finance Corporation (IFC) and Inter-American Development Bank's IDB Invest to lend or invest directly in private companies in developing countries; underpin private financial flows to climate mitigation and adaptation projects by taking on some of the risks that the private sector is not willing or unable to bear, through provision of insurance, guarantees, or more complex risk sharing arrangements; promote innovative climate financing techniques in international capital markets by demonstrating what can be done and how to scale it.

As climate change is a global (not a local) issue and emissions have to be reduced to clip greenhouse effects in the atmosphere, it is difficult to "sell" locally the sacrifices to reduce global climate warming, as long as those concerned cannot see, tangibly, the effects of such efforts they need to undertake. As long as externalities are not priced, in effect giving them out for free, it is difficult to "bring home" the impact of inaction.

There are many ways of pricing emissions — from pricing them directly, instituting taxes to act as proxies for the cost generated by emissions, instituting industry standards akin to the Equator Principles, establishing various forms of regulations ranging from direct monitoring and public oversight all the way to accounting conventions requiring enterprises to recognize in contingent liabilities the environmental damage they may generate. Each of these options have their trade-offs and institutional requirements that need to be assessed before implementation.

Given the scale and the pivotal role that the private sector is bound to have in mobilizing the increasing human, technical and financial resources needed to address the changes needed to meet the international agreements, the question that remains to be fully flushed is whether organized voluntary carbon markets can help resolve these challenges by creating credible incentives for emissions reductions, and mobilizing the corresponding resources and incentives to resolve the climate change issues.

The global voluntary carbon market, and its supporting industry ecosystem, has grown substantially from its origins in the early 1990s. Despite this growth, voluntary markets have been hampered by reputational and functional concerns about offset quality and the space remains fragmented.

With no long-term regulatory, institutional obligations or pricing signals on carbon, firms are left to chart their net-zero paths with little guidance or policy vision. The question is whether organized voluntary carbon markets can help resolve these challenges by creating credible incentives for emissions reductions.

Recent initiatives aimed at creating more functional, transparent, and effective carbon marketplace are a good start. In many cases, there is a growing intersection between government and private sector activity in voluntary markets. governments and/or industry regulating processes could support the legitimacy and success of voluntary markets.

These novel initiatives demonstrate how market design choices imply different goals for voluntary markets. These models suggest new ways for to manage increasing demand for carbon credits, private firms and organizations have developed standards and maintained credit registries.

Today these are well-established players such as the American Carbon Registry (ACR), the Climate Action Reserve (CAR), the Gold Standard (GS), and the Verified Carbon Standard.

These agencies regulate the "supply" side of the market; they define project standards, verify compliance, and host registries that regulate the minting and retirement of credits. It is important to note that these remain nongovernmental and private; they earn revenue from the offsets they recognize.

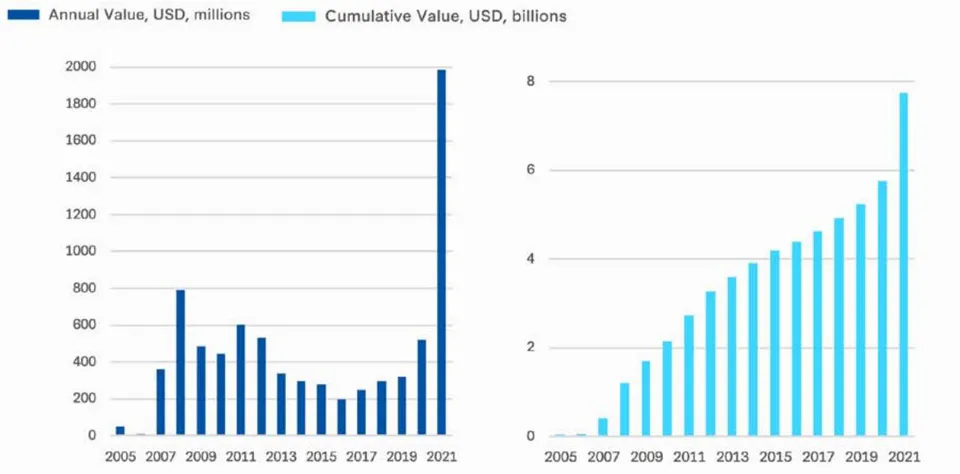

While the current voluntary market ecosystem is fragmented and dominated by decentralized, broker mediated, over-the-counter trades, there have been previous attempts to organize and regulate the space. In 2021, its market value reached nearly 200 million just five years prior.

The 2016 Paris Climate Agreement has created new opportunities for voluntary carbon markets. Article 6 of the agreement raises the possibility of countries using carbon offsets toward their Nationally Determined Contributions (NDCs). This provided official recognition of the offset model and the value of voluntary markets, pointing toward a future in which they could achieve international standardization. equivalent to that of large-scale compliance markets.

They thus can be seen as a critical tool for mobilizing finance for climate mitigation. However, the present global voluntary market, composed of unregulated demand, bespoke fractured trading systems, and a vast sea of heterogeneous supply, has demonstrated limited ability to deliver a price on carbon that The convergence between private carbon markets and governments, as well as the need to scale the trade of high-quality credits, has resulted in a number of new market initiatives, and growing activities through global voluntary carbon markets, as noted below:

Source: "Market Size by Traded Volumes of Voluntary Carbon Credits, Pre-2005 to 31 August 2021," Ecosystem Marketplace, https://data.ecosystemmarketplace.com/.

CSIS ENERGY SECURITY AND CLIMATE CHANGE PROGRAM

Various models show that voluntary efforts can be supported by state or other forms of collective validation to add credibility and centralization, which signal long-term recognition of the market as integral to achieving national climate goals.

Clearly, it is here where institutional development to build up from the experience so far, will be required to develop genuine carbon markets, to help mobilize resources where they are needed with the necessary validations. Hitherto, carbon market has historically been dominated by avoidance credits (i.e., projects that avoid emissions that otherwise would have occurred, such as preventing deforestation or building renewable energy where fossil fuel-fired resources would have been built). Challenging these are a new class of removal credits that certify direct removal and sequestration of carbon dioxide from the atmosphere. Further, the emissions reduction contribution is considered more scientifically rigorous relative to avoidance credits. Increasing the supply of carbon

removal credits is seen as a critical component in meeting net-zero goals. These factors combine to allow removal credits to command a premium from buyers and trade at many multiples of avoidance credits.

VI. CONCLUSION

The battlefield is a scene of constant chaos. The winner will be the one who controls that chaos, both his own and the enemies(Napoleon)

It is hard not to be puzzled by the obvious contradiction that can be seen in energy transition. On the one hand, taking at face value pledges, programs, goals articulated in COP meetings, it would seem that we are on our way to reach the climate target by mid-century. On the other, looking at actual, and the immensity of the infrastructure, policy and regulatory enabling issues to be addressed, it seems that the goals are illusory, and that we are barely prepared for a decisive move "from words to deeds".

Clearly, the confluence of a series of crises, almost in tandem, have overstretched the governance institutions that have been built for more stable and different times. The geopolitical conflicts for global preeminence between existing and emerging powers, the spread of the pandemic, growing dissatisfaction of civil societies with the distribution of opportunities and benefits of economic progress, have strained the capacity and imagination of all major actors leading governments.

The time has come to recast the overall global financing and governance architecture to mainstream key multilateral institutions (including World Bank and others), and draw-in private sector actors. MDBs have become notoriously bureaucratic, slow-moving, unresponsive to emerging demands, and require vehicles for transparency and accountability to properly respond to emerging needs without complicated multilayered and duplicative decision-making processes. Such change will be essential to rebuild stakeholder (and shareholder) confidence to facilitate improved and results-oriented resource use, and thus preparedness to support their mandates and management of their resources.

By the same token, the problem of climate change is going to be solved by innovation and entrepreneurship, more than by governments and politicians. This is in essence the role of the private sector, and the risk taking associated with it.

If societies are genuinely concerned about pollution, climate change, and are willing to let their purchasing decisions be guided to some degree by their concerns — to put their money where their mouths are, to put it crudely — then they can generate incentives to which the corporate world and civil society will respond, while accommodating lower income countries and population to manage their transition.[10]

Aware of such limitations, various Governments are working on actions aimed at overcoming at least partially the absence of carbon markets. The EU has established a Carbon Border Adjustment Mechanism to partially reflect to a price on the carbon emitted during the production of carbon intensive goods that are entering the European market, and to encourage cleaner industrial production in non-EU countries. Other countries, like Chile, have introduced pricing and taxation practices aimed at reflecting environmental costs, as an interim measure until carbon market legislation is issued for a more market driven pricing system. Israel is working on various alternatives to introduce some form of carbon pricing vehicles, In the case of the US, a deliberate hands-on policy seems to be taking shape aimed at pulling innovation, driving costs down while creating jobs within the country, and supporting specific industries that are considered foundational for economic growth, strategic from a national security perspective, and where the private sector is not considered to be poised to undertake investments on its own. To this end, an Inflation Reduction Act was enacted to support US production of some products (like EVs), to onshore and friend-shore supply chains to reduce dependence on major competing countries like China, and institute tax credits to generate demand for transportation electrification and other such activities in the US. As in any directive approach aimed at several objectives in tandem, it remains to be seen how effectively the industrial policy, environmental and geopolitical objectives can be reconciled in an effective manner, and what geopolitical ramifications it may have.

Perhaps, the International Renewable Energy Agency has pretty much encapsulated the thrust of this discussion when noting that "a profound and systemic transformation of the global energy system must occur in under 30 years", underscoring the need for a new approach to accelerate the energy transition. Pursuing fossil fuel and sectoral mitigation measures is necessary but insufficient to shift to an energy system fit for the dominance of renewables-- "the emphasis must shift from supply to demand, toward overcoming the structural obstacles impeding progress...through policy and regulatory enablers and well-skilled workforce, requiring significant investment and new ways of cooperation in which all actors can engage in the transition and play an optimal role."

- Precipitating Energy Transition" https://www.sur-invest.com/ Downloads Publications/Global Journal MS 10 June 2021.pdf Miguel Schloss; Oil, Gas & Energy Law Intelligence (OGEL-U.K.), Feb. 2023 "Changing the Conversation on Energy Transition — Aligning Interests or Mandating Actions to Combat Climate Change in Challenging Times" https://www.ogel.org/journal-author-articles.asp? key=367.

- IEA analysis OECD Inventory of Support Measures for Fossil Fuels. https://www.oecd- library.org/agriculture-and-food/data/fossil-fuel-support_d86aea00-en.

- World Resources Institute, WRI, Global Digest' June 2023 https://www.wri.org/climate?utm_campaign=WRIClima&utm_source=ClimateDigestNewsletter&utm_medium email&utm_content bannerIntergovernmental Panel for Climate Change, - IPCC 2022 Report on Climate Impacts, Adaptation and Vulnerabilityhttps://www.ipcc.ch/report/sixth-assessment-report-working-group-ii/.

- International Energy Agency - IEA analysis OECD Inventory of Support Measures for Fossil Fuels. https://www.oecd-library.org/agriculture-and-food/data/fossil-fuel-support_d86aea00-en World Bank; Detox Development: Repurposing Environmentally Harmful Subsidieshttps://openknowledge.worldbank.org/entities/publication/4217c71d-6cbc-46b6-942c-3e4651900d29.

- Gernot Wagner; How to Think About Climate Tech Solutions; Project Syndicate June 3013 https://www.project-syndicate.org/commentary/climate-tech-moral-hazard-how-to-identify-viable-solutions-by-gernotwagner-2023-06

- 8 C.P. Colum & Lea Booth; Solar Panels Are Three Times More Carbon-Intensive Than IPCC Claims; Public Substack, (Public, July 2023)https://public.substack.com/p/solar-panels-more-carbon-intensive?utm_source post-mail-title&publication_id &post_id 135388557&isFreemail true&utm_medium email

- 9 Vinod Thomas; Palgrave Macmillan, Singapore; "Risk Resilience in the Era of Climate Change"

- [10] Geoffrey Heal; Endangered Economics; Columbia University Press, 2017 https://www.thriftbooks.com/w/endangered-economies-how-the-neglect-of-nature-threatens-our-prosperity/geoffrey-heal/11610560/#edition=11182883&idiq=34742655[10]Miguel Schloss; Editorial Académica Española: "Cambiando la conversión energetica", 2023.